What Happened This Week

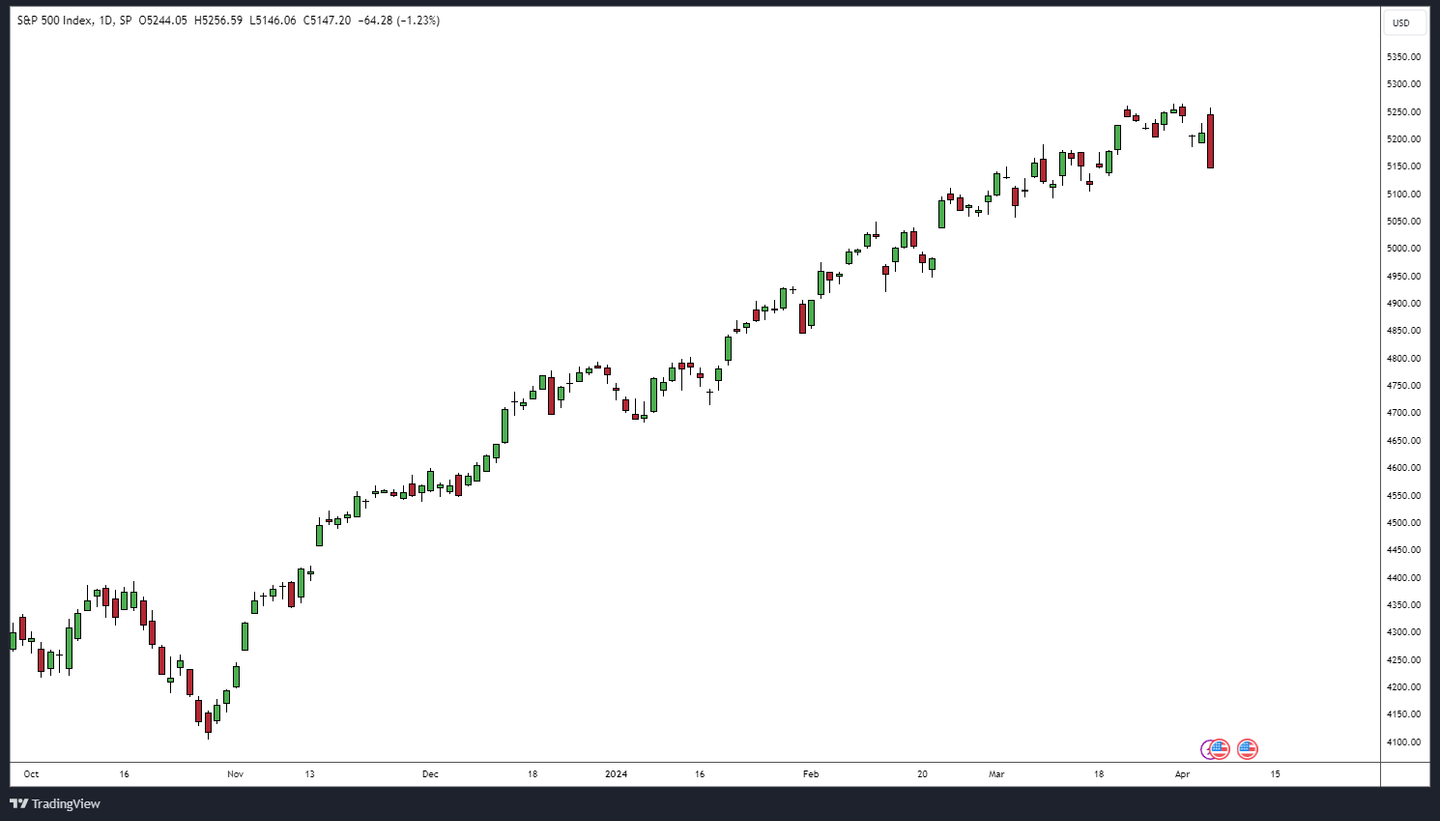

March was the 7th consecutive month with a positive performance for Bitcoin

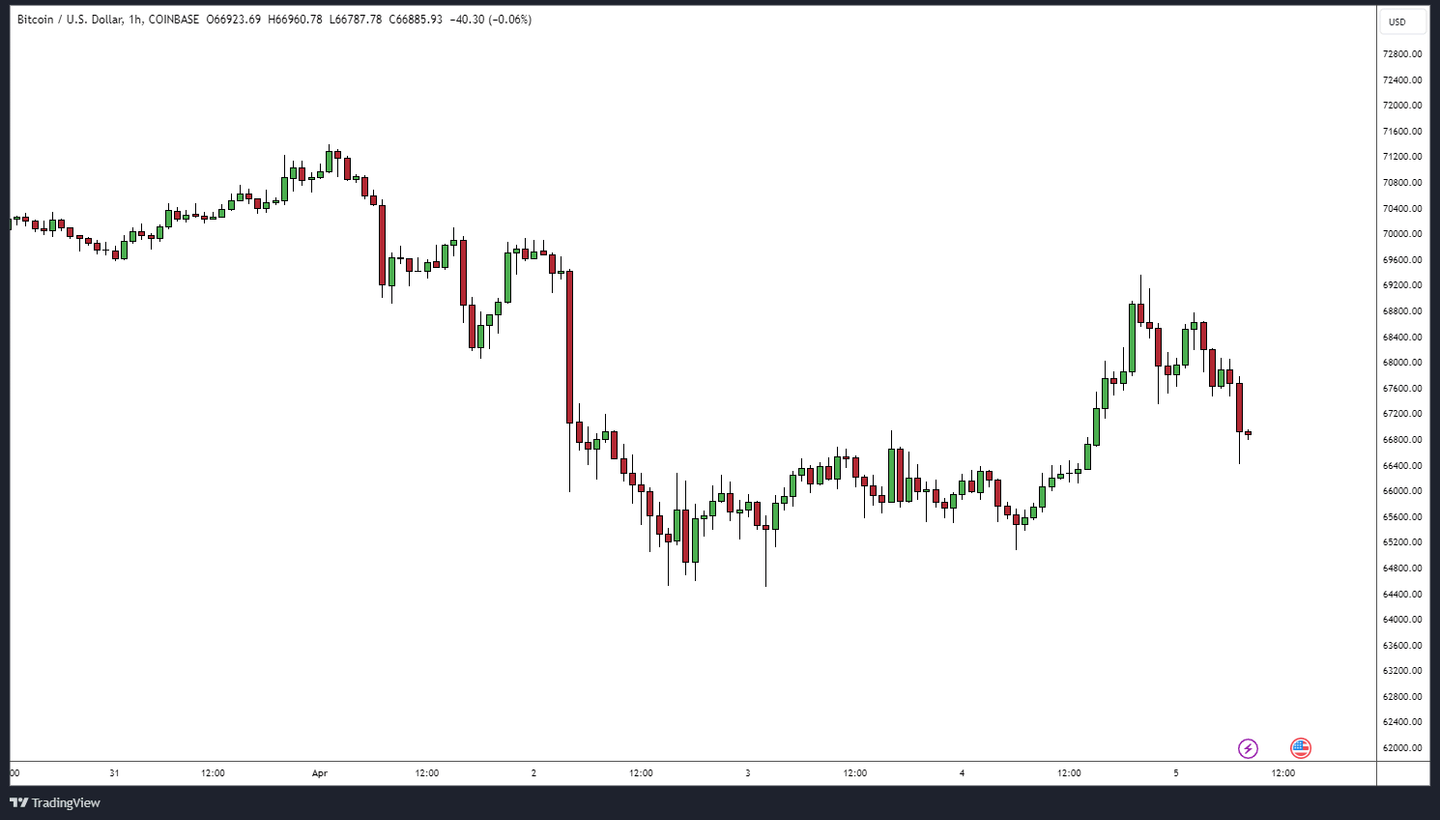

The last weekend in March was a rather quiet one for Bitcoin and the broader crypto market, with Bitcoin trading flat around the $70’000 mark. On Sunday evening, Bitcoin closed the month of March with a gain of over 16% resulting in the 7th consecutive positive month, which is a record. The monthly close at around $71’000 was also the highest one in the history of Bitcoin so far. The weekend was not spectacular for most altcoins either, with WIF, the new meme coin, being the exception. It increased over 25% over the weekend and traded just below $5 resulting in a new all-time high. Looking back at the week before, digital asset investment products saw a recovery in sentiment, with total inflows of $862 million. These inflows almost made up the weekly outflows from two weeks ago, when digital asset investment products saw an outflow of roughly $900 million.