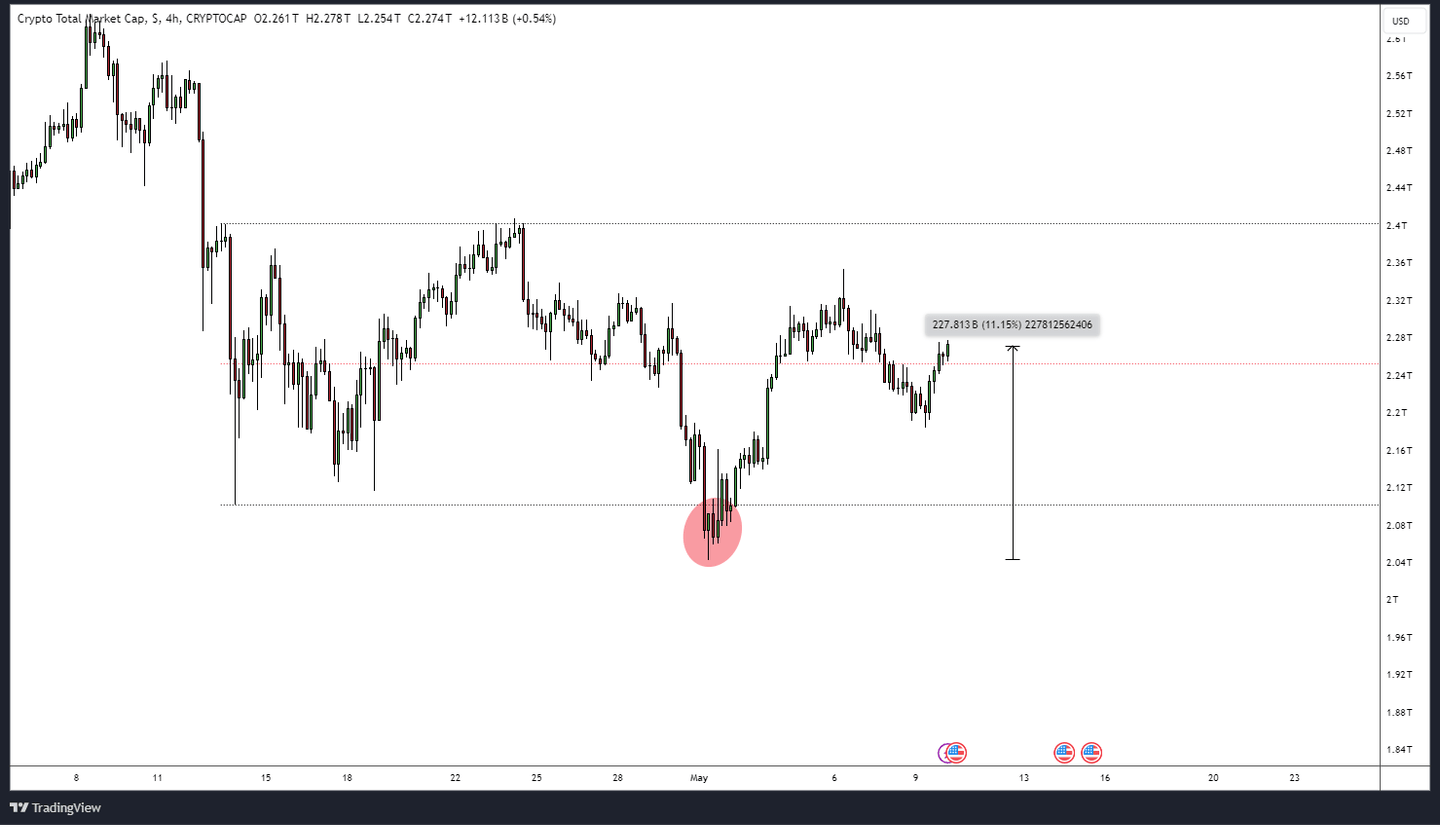

What Happened This Week

Last Friday, right around the time we sent out last week’s wrap, Bitcoin started rallying into the evening, and was able to sustain its rather positive price action for the weekend, trading slightly to the upside and closing the week in the green, up 1.45%. A quite impressive weekly close, considering BTC was down more than 10% during the course of last week. Last week was the first positive week for Bitcoin since the end of March. The positive sentiment in the U.S. equity market likely played a role in Bitcoin’s recovery at the end of the week and into the weekend. The S&P 500 closed the last week positive as well. The positive sentiment manifested itself in $378 million of inflows into the U.S. spot ETFs last Friday, adding fuel to the rally into the weekend.

Dampened Start into the Week

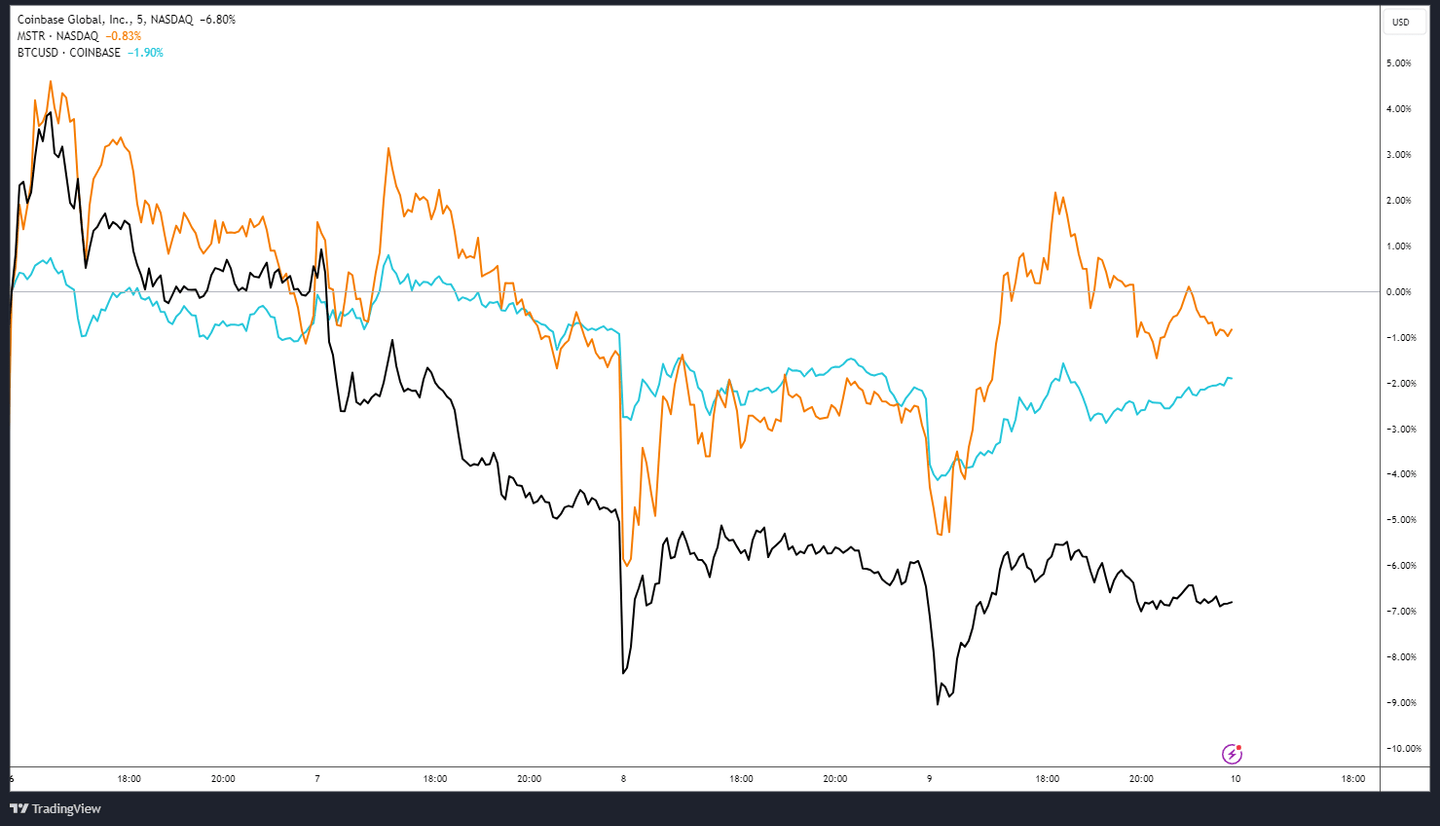

While the weekend price action looked promising, the current weekly high was reached on Monday, with BTC at $65’523. Bitcoin traded to the downside on Monday, finding a temporary low at around $62’700. The subdued price action for crypto was accompanied by the news that the U.S. Securities and Exchange Commission (SEC) issued Robinhood Crypto with a Wells Notice, citing alleged securities violations. This is the third prominent case of a Wells Notice in the last two months, after Uniswap Labs and Consensys both received a Wells Notice from the SEC in April.

While being busy with sending out Wells Notices, the SEC also communicated on Monday evening that they decided to postpone their decision regarding the Invesco Galaxy Ether spot ETF, setting the next deadline for the ETF to July 5, 2024. The crypto market likely did not take this decision as a surprise, since the optimism regarding a positive decision on any of the Ether spot ETFs has declined over the past months, and the probabilities of an approval in May have declined rapidly as well over the last months. Talking about ETFs, the U.S. spot ETFs saw another day with net inflows on Monday, with $217 million flowing into the U.S.-based products. Notably, GBTC saw its second straight day with net inflows on Monday. This is a very interesting development. If you would like to stay up-to-date regarding the spot ETFs, you can read a detailed update from us here.