Uptick in U.S. inflation, and $1 billion of net inflows for spot ETFs on Tuesday

On Tuesday, TradFi markets, to the surprise of many, reacted bullishly despite the uptick in U.S. inflation in the CPI data release, which saw a small rise up to 3.2% in February, up from 3.1% in January. The Federal Reserve is still targeting a 2% inflation rate, and the FOMC meeting, scheduled for Wednesday next week, will be particularly interesting to observe, also because this upcoming FOMC meeting is one of four meetings in the year in which the Fed releases its dot plot, a summary of economic projections that includes expectations for where the Fed funds rate will be at the end of 2024.

On Tuesday, the daily net inflows for the Bitcoin spot ETFs reached a new high, with over $1 billion of daily net inflows. While the outflows from GBTC slowed down a little with only $79 million outflows, IBIT, the spot ETF of BlackRock saw daily net inflows of a record-high $849 million on Tuesday.

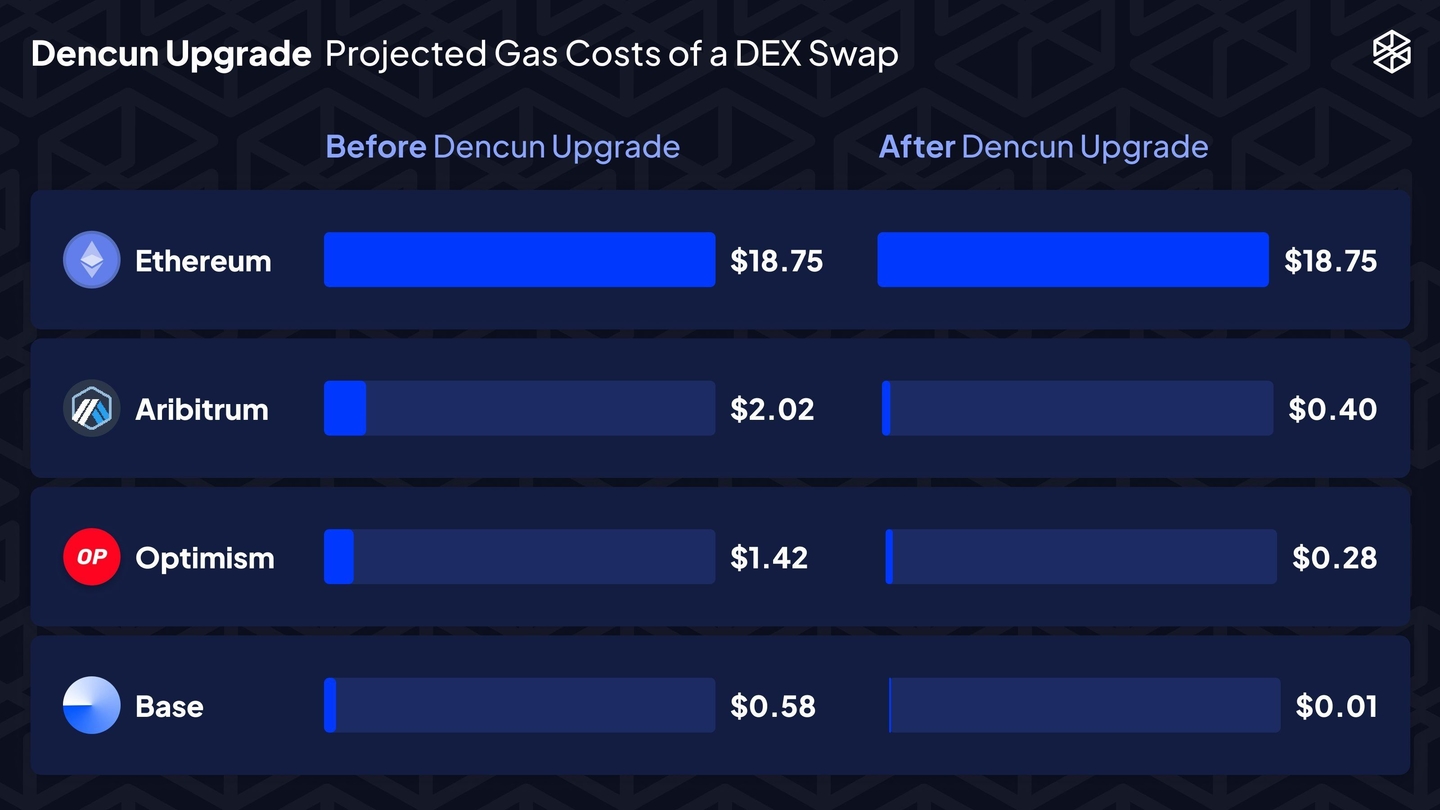

Dencun Upgrade on Wednesday

On Wednesday afternoon, the much-anticipated Dencun Upgrade went live on Ethereum. With the Dencun Upgrade comes Proto-Danksharding which is designed to reduce transaction fees for Ethereum rollups and brings consistent transaction fees by decoupling the resources dedicated to layer 1 smart contracts from the ones dedicated to rollups. In the chart below, you can see how the Dencun Upgrade impacts the fees on L2s like Arbitrum or Optimism. In terms of price action, Ethereum and L2s like ARB or OP did not react much after the Dencun Upgrade went live. On the other hand, Solana, as a competitor blockchain to Ethereum, went on a surge right after the Upgrade went live and closed the day on Wednesday up more than 10%.