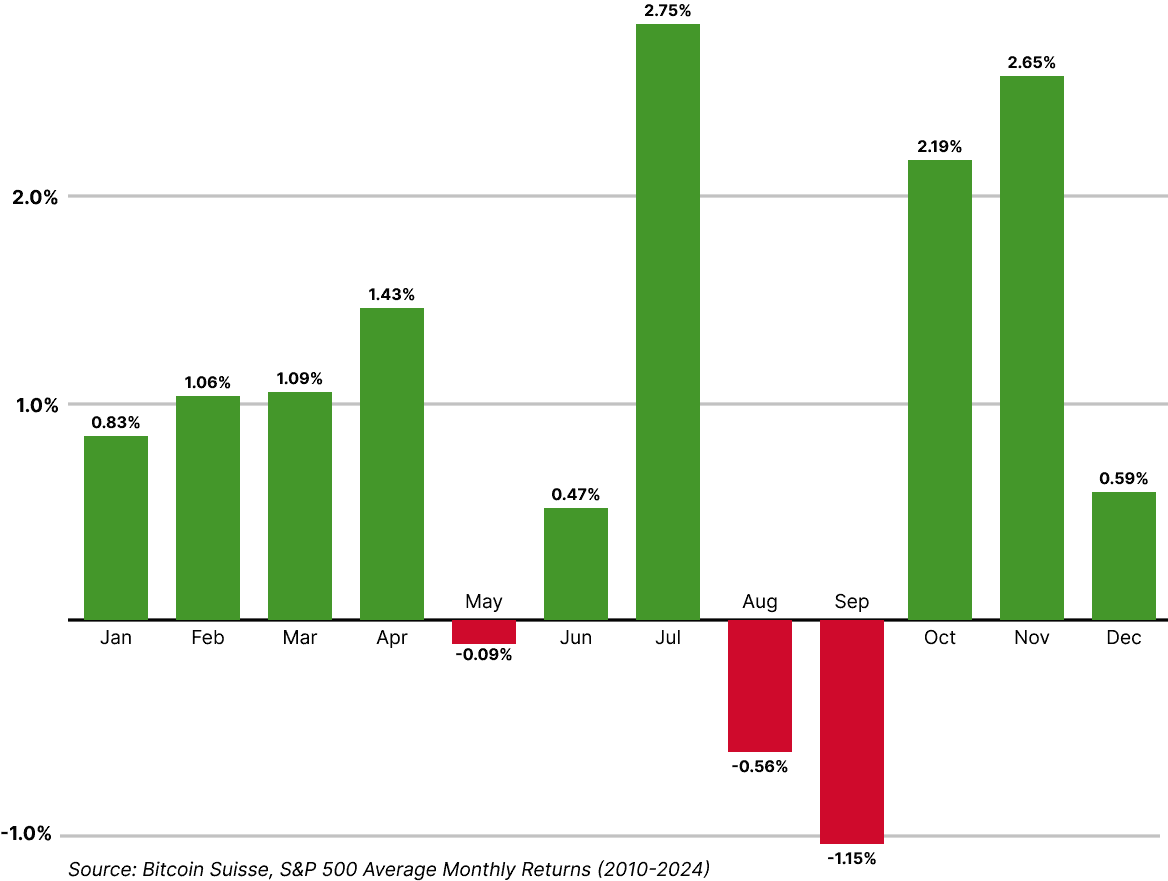

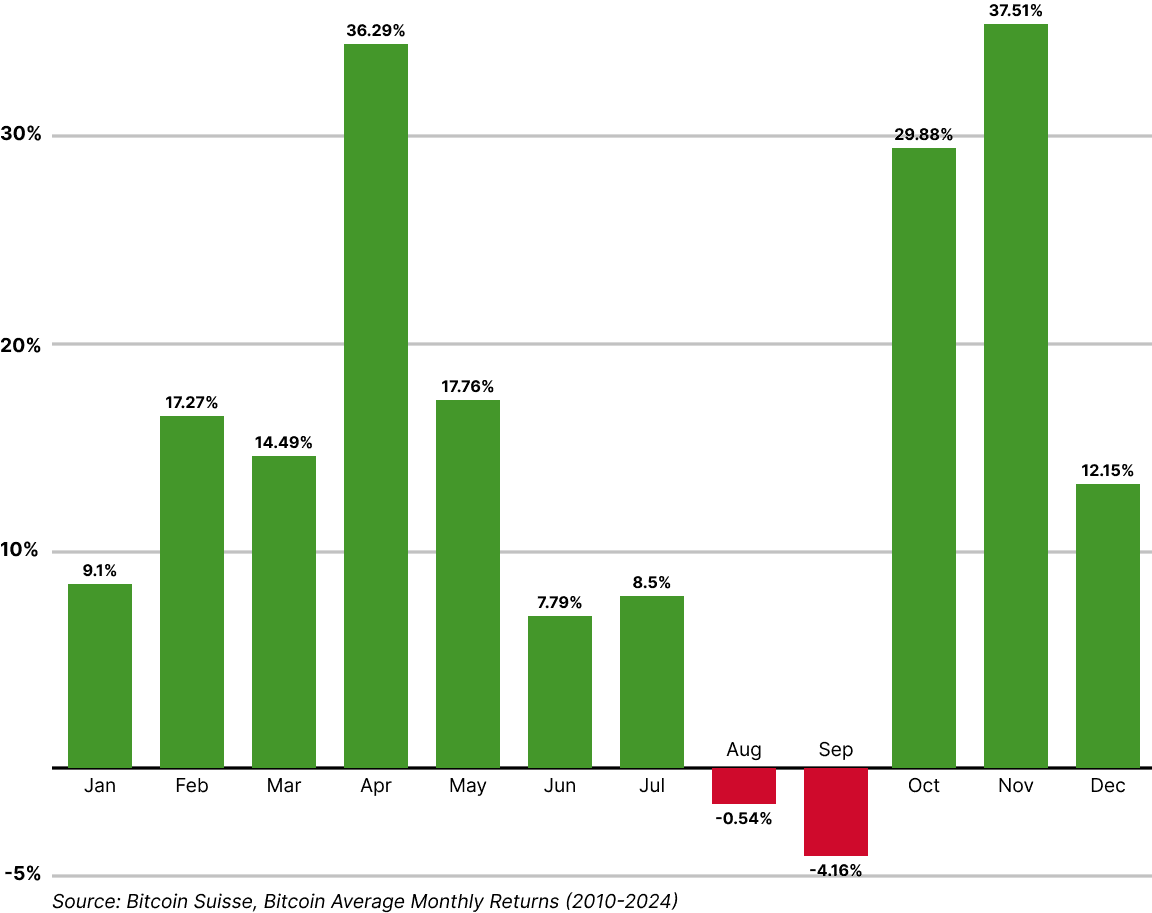

Sell in May and go away?

Interestingly, the chart above indicates that the well-known phrase "Sell in May and go away", which has circulated since the 19th century, has not proven particularly effective for investors in either the S&P 500 or bitcoin since 2010. A more appropriate phrase might be "Say Goodbye in July" only to return in September—echoing the industry wisdom "Remember to come back in September".

2024 – Anything but Normal

The seasonal trends discussed above offer a general overview for when investors and market participants might anticipate more volatile price movements, as well as when a more cautious, wait-and-see approach might be warranted. During the summer months, particularly August and September, many market participants take vacations, resulting in reduced trading volumes and lower market liquidity.

However, this year, August proved anything but tranquil. Recall early August, when the S&P 500 experienced a correction of nearly 10%, while bitcoin lost almost 30% in just a few days. Despite this turbulence, the S&P 500 concluded August with a modest gain of 2.28%, while bitcoin saw a decline of nearly 9%. In September the S&P 500 has climbed more than 1.5%, with bitcoin gaining 7.5%. Contrary to historical trends, the two weakest months have yielded positive results for the S&P 500, while bitcoin continues to trade below its August 1 price of $64,600.

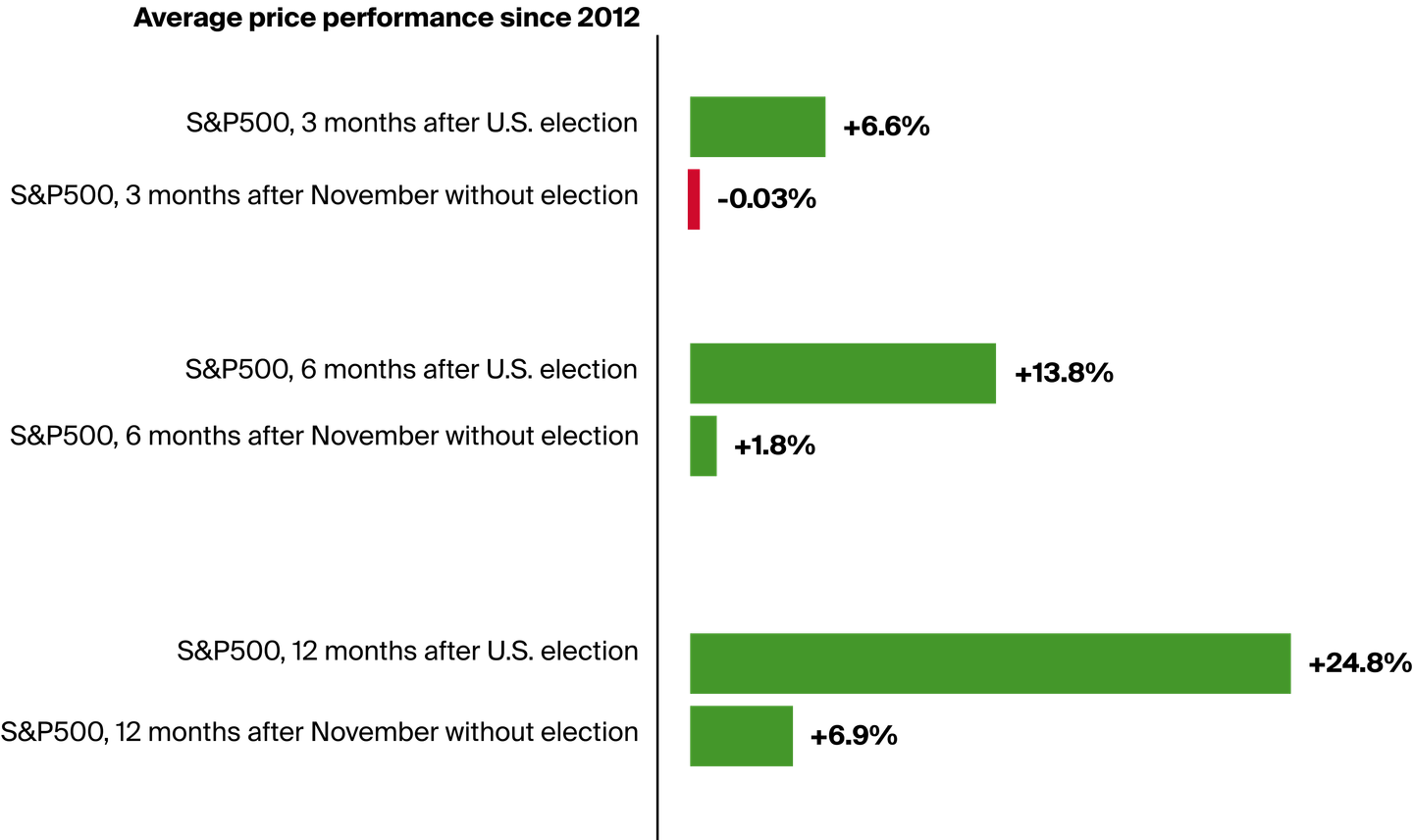

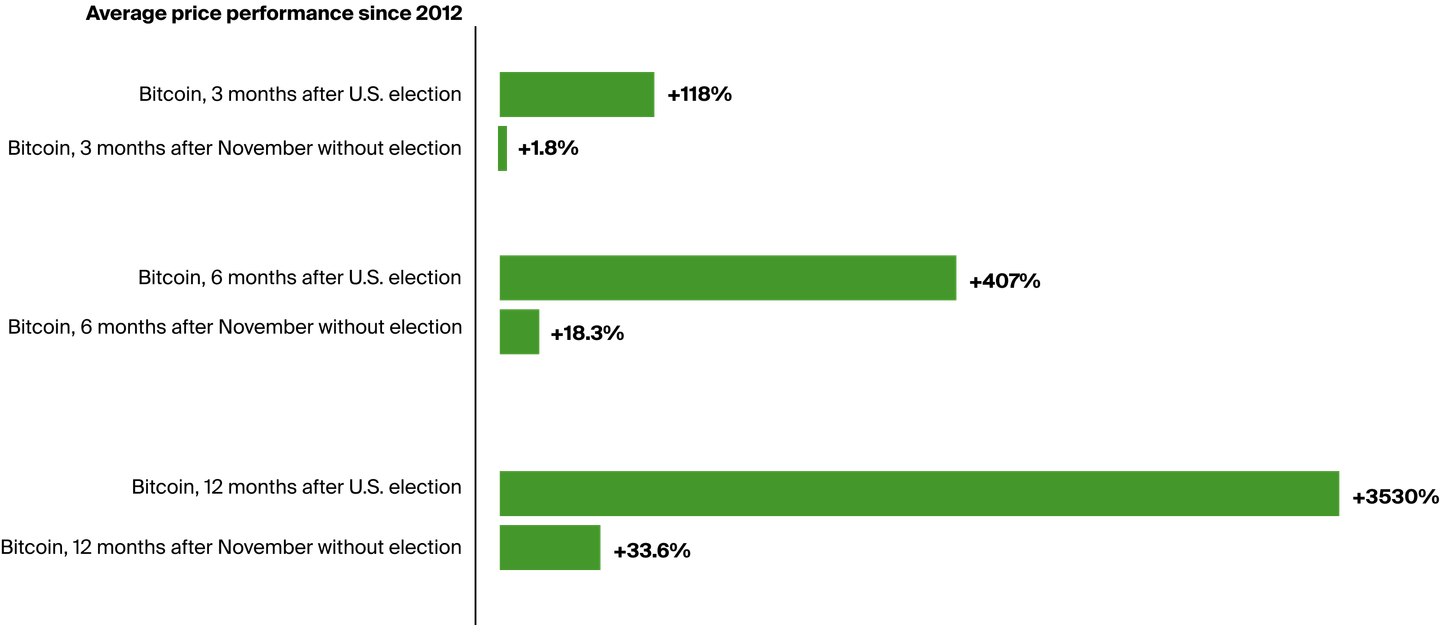

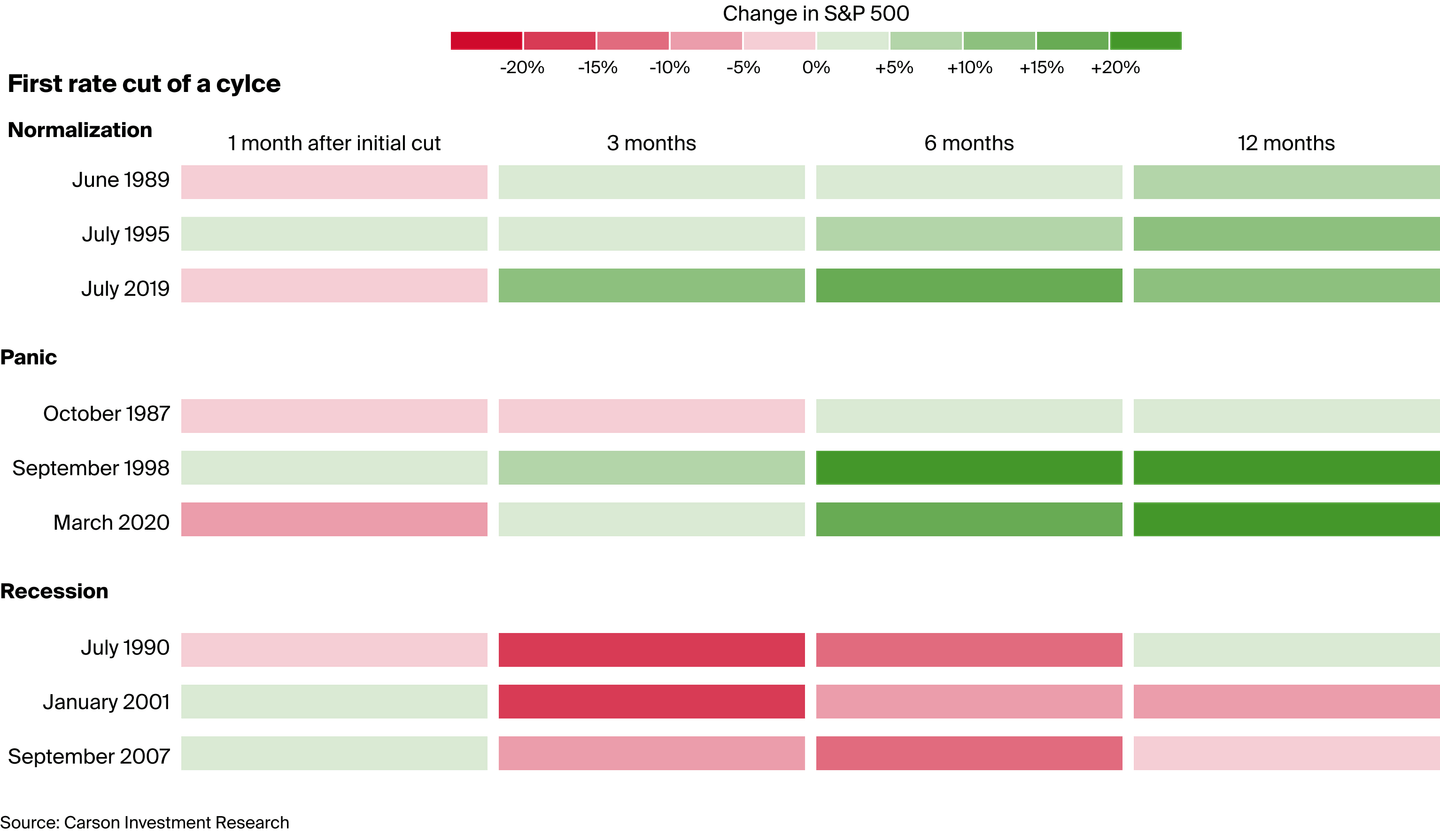

2024 is extraordinary for additional reasons. In November, the U.S. presidential elections will take place, with current President Joe Biden having withdrawn from the race over the summer, paving the way for his Vice President, Kamala Harris, to run against Donald Trump for the presidency. Additionally, the Federal Reserve cut interest rates in September for the first time since 2020, reducing them by a significant 0.5 percentage points.

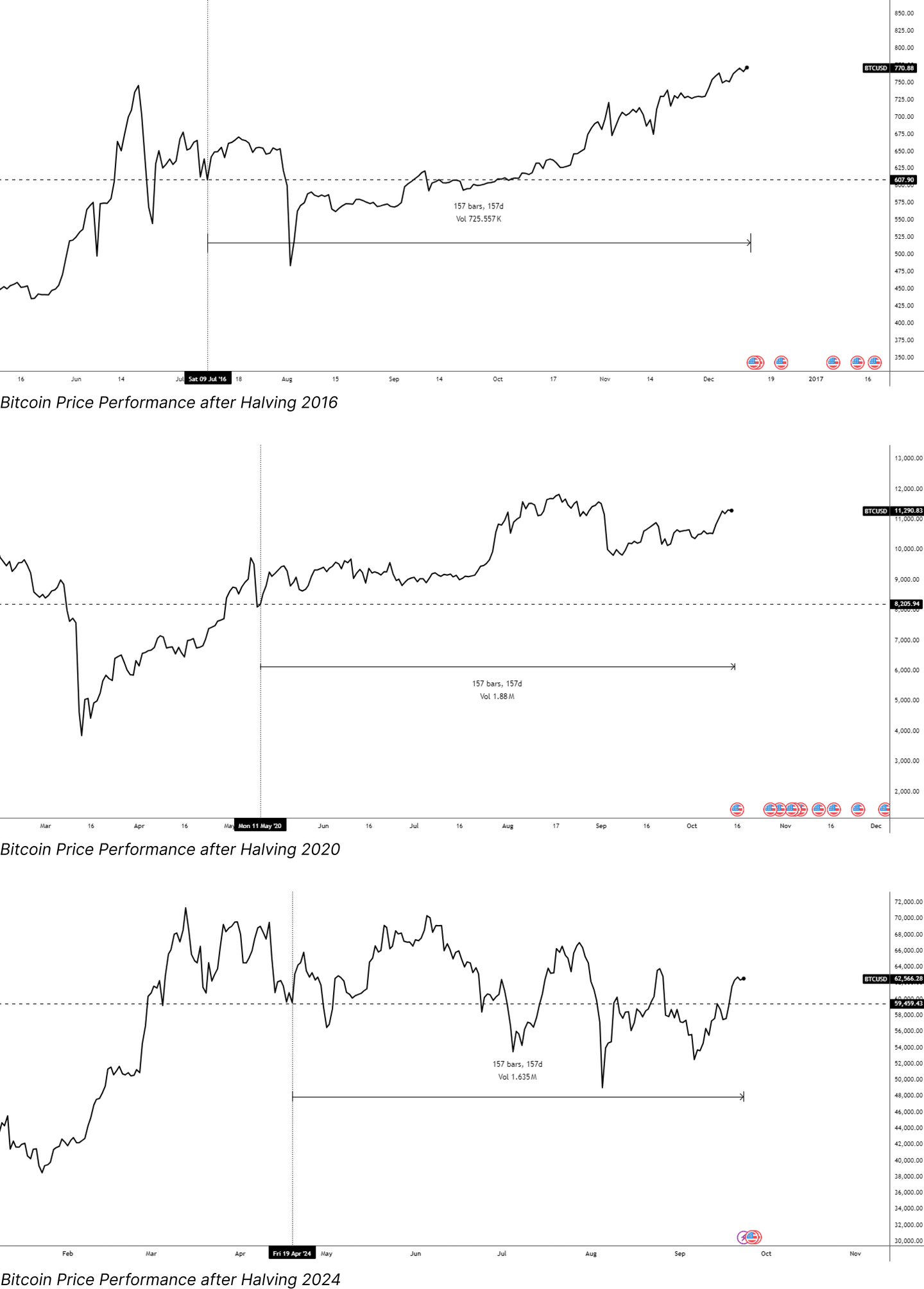

But that’s not all—2024 is also pivotal for bitcoin, as the fourth halving event occurred on April 19. Let’s delve deeper into how these developments might influence the price movements of risk assets like bitcoin and the S&P 500.

The bitcoin halving

On April 19, 2024, the fourth bitcoin halving took place. We have previously published several articles on this topic, which you can revisit for more context. In this section, we will compare bitcoin's price performance following previous halvings with its current performance in 2024, after the fourth halving. As mentioned earlier, seasonality plays a minor role in price movements; significant events and news—such as economic data and policy decisions—also exert considerable influence. The chart below illustrates bitcoin’s price performance following the halvings in 2016, 2020, and 2024.