Crypto & Macro - Is the Bottom in? Version 2.0

Denis OevermannInvestment Analyst / Crypto Researcher

18 Apr 20238 Min

Just on the weekend amidst the “crypto bank crash”, more than one million new BTC wallets have been created, an attestation to an inevitable trend of adoption, which reflects the “case for crypto” outlined earlier, proving quantitatively, that it is irresponsible to not have any allocation to crypto in a diversified portfolio.

Executive Summary

- Long-term momentum indicators indicate that BTC visited its historical “bottom territory”, marking significantly undervalued prices are seen just 15% of the past trading days.

- Aggregated bear market regression channels imply that the S&P 500 is currently through less than half a historical downturn.

- Bitcoin is through three quarters of the historical downturns and priced at the lower end of historical downturns.

- BCI is weakened, whereas CCI has recovered somewhat, though the ISM is still turning downwards sharply, amongst tightened financial conditions (NFCI), implying economically tough times.

- Real inflation adjusted returns for the S&P 500 have been almost flat over the past two decades, while real wages did not increase in over half a century – BTC on the other hand significantly outperforms all of them, even on inflation adjusted returns.

- BTC visited its historically “undervalued” territory, with prices having declined significantly from one year ago, offering “undervalued price levels” that only occur 14% of the time.

1. Are we out of the woods?

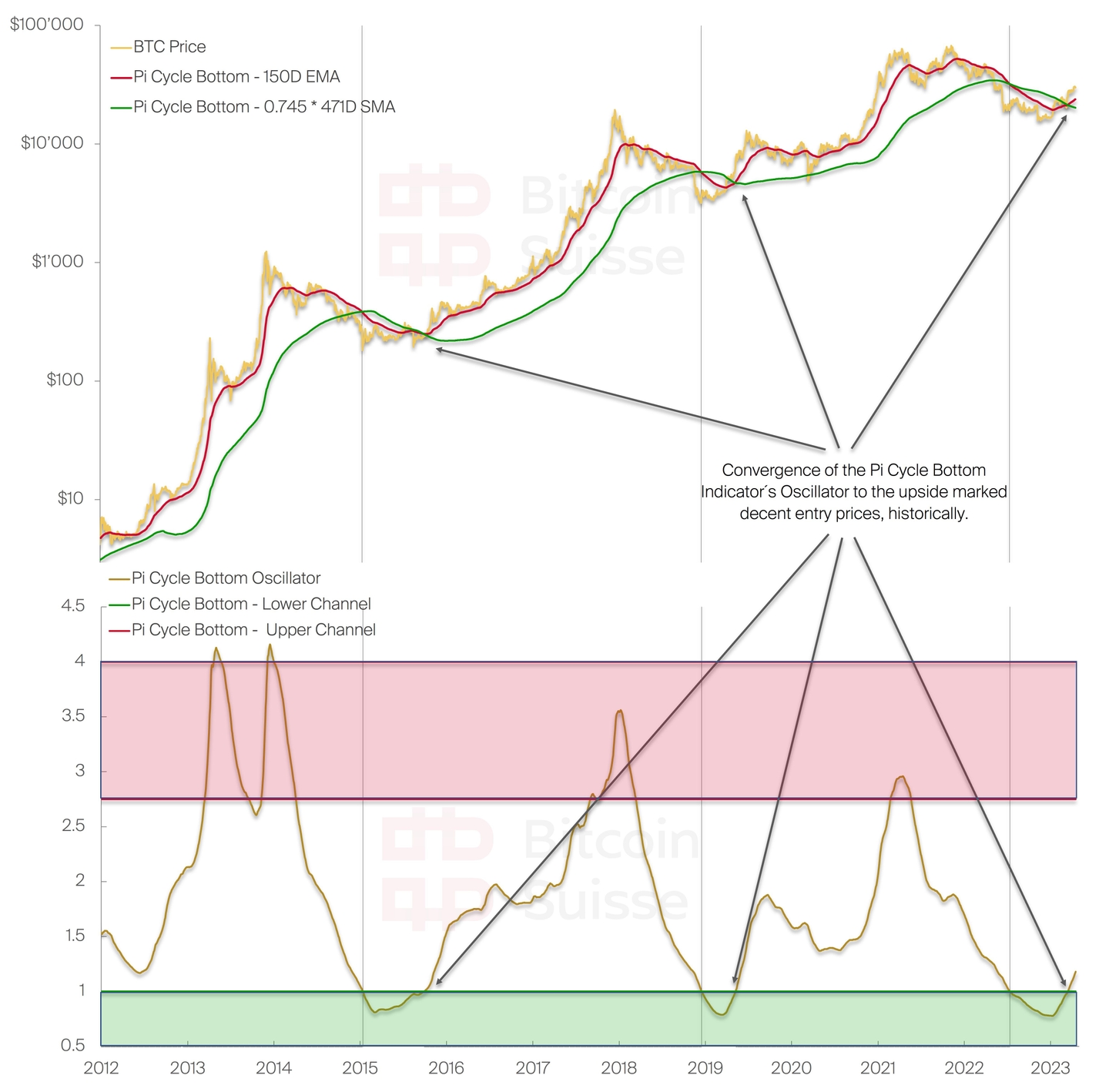

To determine the general market phase of the crypto market, we use BTC as a proxy and apply the Pi Cycle Bottom Indicator, which is a long-term momentum metric. Being composed of two long-term moving averages, the indicator is suited to determine likely bottom territories for BTC´s price. Interpreting the indicator becomes more insightful, after we derive an oscillator from the moving averages, bases on their convergence and divergence. The result is a homogenous picture of past BTC bottom prices, with the oscillator consistently revisiting similar “undervalued” price regions. Only 15% of the time Bitcoin was situated in the green “undervalued” price territory. With the oscillator converging to the upside, and out of the green “undervalued” price territory, past bottom prices have already occurred. This does not imply, that the bear market has been left behind, historically, but rather that the lows for the Bitcoin price have been seen already. Overall, the Pi Cycle momentum indicator and our oscillator indicate, that it is likely that BTC has seen its lowest price levels for this bear market cycle.

2. Historical duration of bear markets

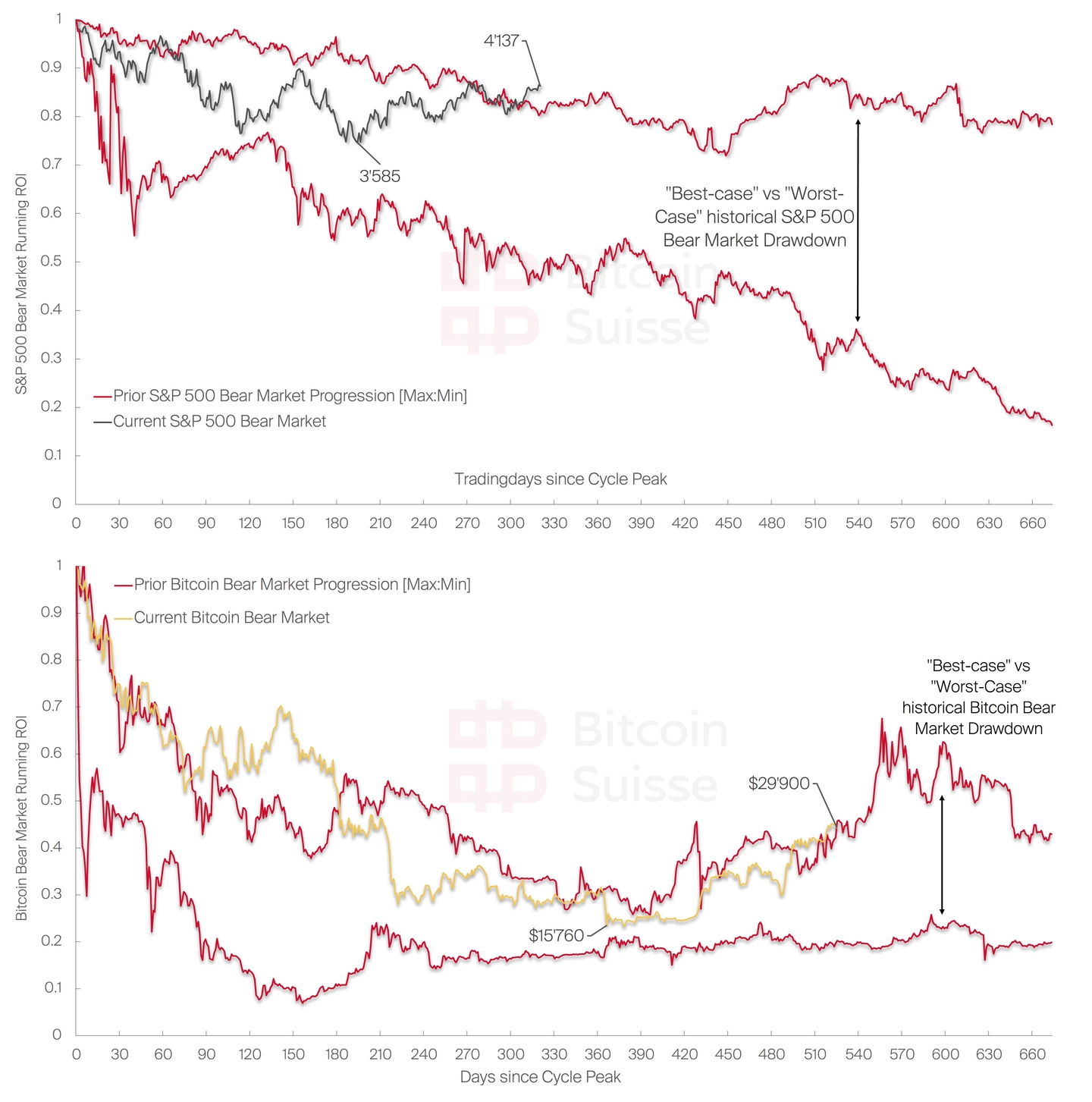

With prices having decreased quiet substantially over the past year, it appears reasonable to ask how long such market downturns tend to last. Figure 2 aggregates the entirety of past equity and crypto bear markets ad downturns, as represented by the S&P 500 and Bitcoin. The channels represent the “best case” and “worst case” scenario, being composed of the highest and lowest returns in the aggregate of all respective downturns. The channels are therefore not representative of a single bear market, but the aggregation of the respective highest and lowest returns within all past bear markets. A key characteristic of equity markets is that S&P 500 bear markets lasted 9 months, historically, whereas recessions lasted around 1.5 years for the S&P. Nevertheless, there are countless examples in the past, where recessions were drawn out for up to three years in total. Though the initial decline is more modest for equities than in crypto markets, there is a tendency for prices to dwindle down slowly and steadily in the long run.

In contrast, Bitcoin bear markets crash substantially harder, initially, while staying in a depressed price territory for an extended period. Generally speaking, BTC does not witness any short-term bear markets, which are a more regular occurrence in S&P bear markets but drawn-out periods of depressed prices. Nevertheless, an important distinction to make is that the S&P downturn is measured in trading days, Bitcoin’s in weekdays, which implies that equity downturns, denominated in normal weekday counts can last up to three years, compared to the longest Bitcoin bear markets of less than two years. Bitcoin’s downturn started earlier and is currently through three quarters of the past bear market channels, situated slightly above its upper center. Similarly, equities are sitting just above the upper band of the bear market progression channel, while being through less than half of it. Inferring from the progression channel, Bitcoin is almost at the end of the longest past bear markets, and further downturns from current prices are situated around the current lows of this downturn. Though lower prices are a possibility, past bear markets suggest that prices either fluctuate around the cycle lows previously seen or appreciate slightly to the upside. If we were to see new lows for BTC´s price, it would be the first, and the bear market progression channel of the next cycle would have to be adjusted to the downside, for the MAX drawdown channel band at the bottom. Due to the slight outperformance of both equities and BTC of past bear markets, the future MIN drawdown progression channels must be adjusted to the upside.

3. Financial conditions and sentiment

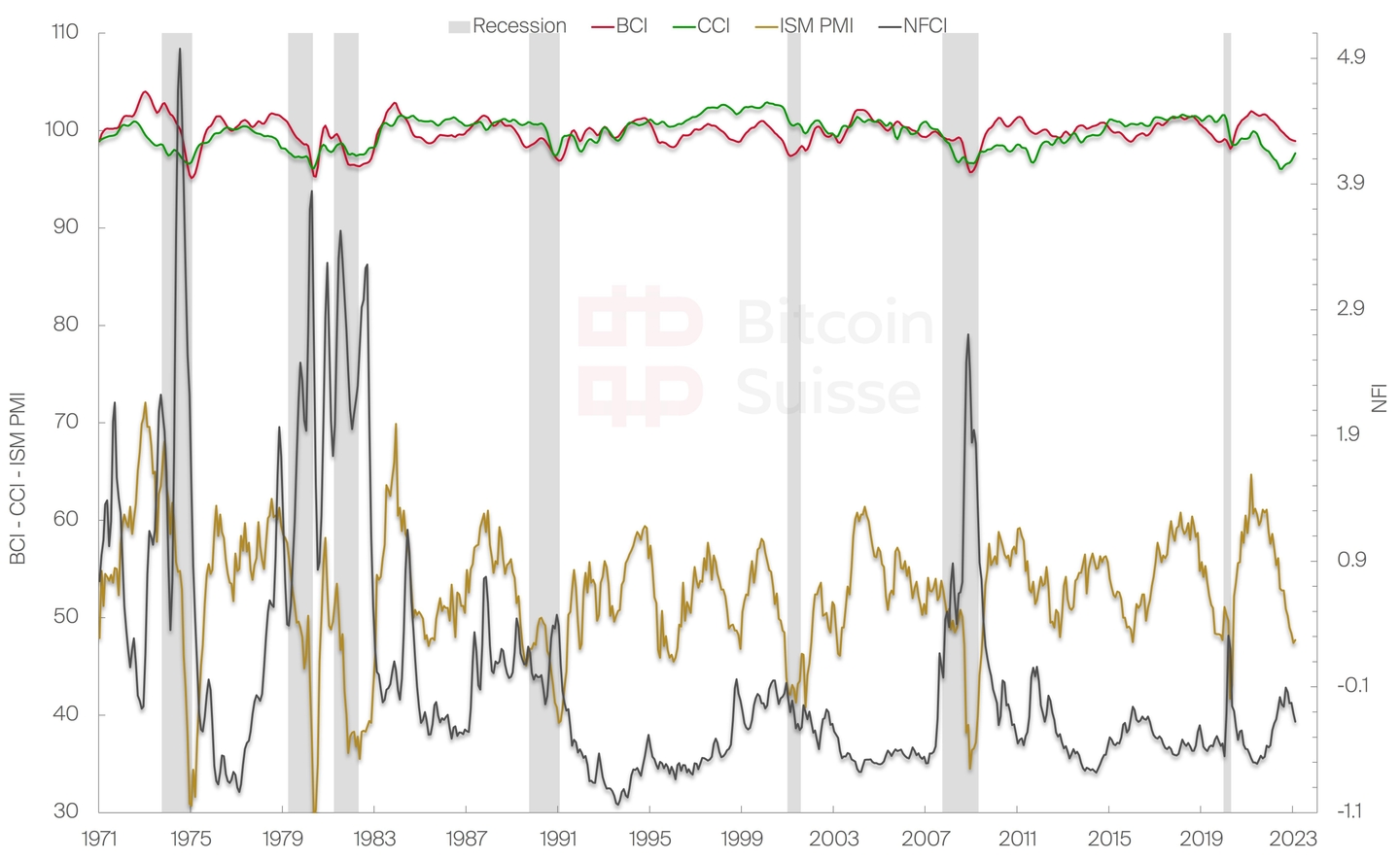

The long-term price progressions and momentum indicators have to be put in perspective with the current macroeconomic sentiment and financial conditions to judge the likelihood of the bottom being in. The Business Confidence Index (BCI) captures developments in production, orders and inventory in order to capture and anticipate future activity in output and economic activity. Similarly, the Consumer Confidence Index (CCI), measures the sentiment for consumers by aggregating unemployment, savings, or economic sentiment of consumers. The Institute for Supply Management’s (ISM) Purchasing Managers Index (PMI) measures the aggregate demand for products via orders, employment, prices, inventory etc. and indicates the overall sentiment and confidence among investors, consumers, and businesses. These three indices capture the aggregate sentiment of consumers, businesses and leading economic activity based upon the confidence of market participants. It will be combines with the National Financial Conditions Index (NFCI) which aggregates the financial conditions in equity, debt, and money markets, with an increasing index implying that financial conditions are tightening. We can observe that the CCI has been recovering slightly recently, but the BCI, however, is still on a rapid descent, which matches the ISM PMI declining in lockstep. An implication, going forward, is that businesses overall are still somewhat skeptical overall, whereas consumers regained their confidence and have a more optimistic outlook in the near-term. On the other hand, the financial conditions overall have eased somewhat, with the NFCI pulling back modestly. The reason for this is inflation cooling off moderately, while the future predicted interest rate hikes are milder than those in the past. Overall, the sentiment and financial conditions still suggest, that the economy will face headwinds in the near-term. This implies that a full market recovery cannot yet be expected with high confidence. In any case, the weakened sentiment, moderately tight financial conditions, and the overall beaten economic situation could be used as long-term entry position in generally weak markets, with current prices far from their all-time highs.

4. The Case for Crypto

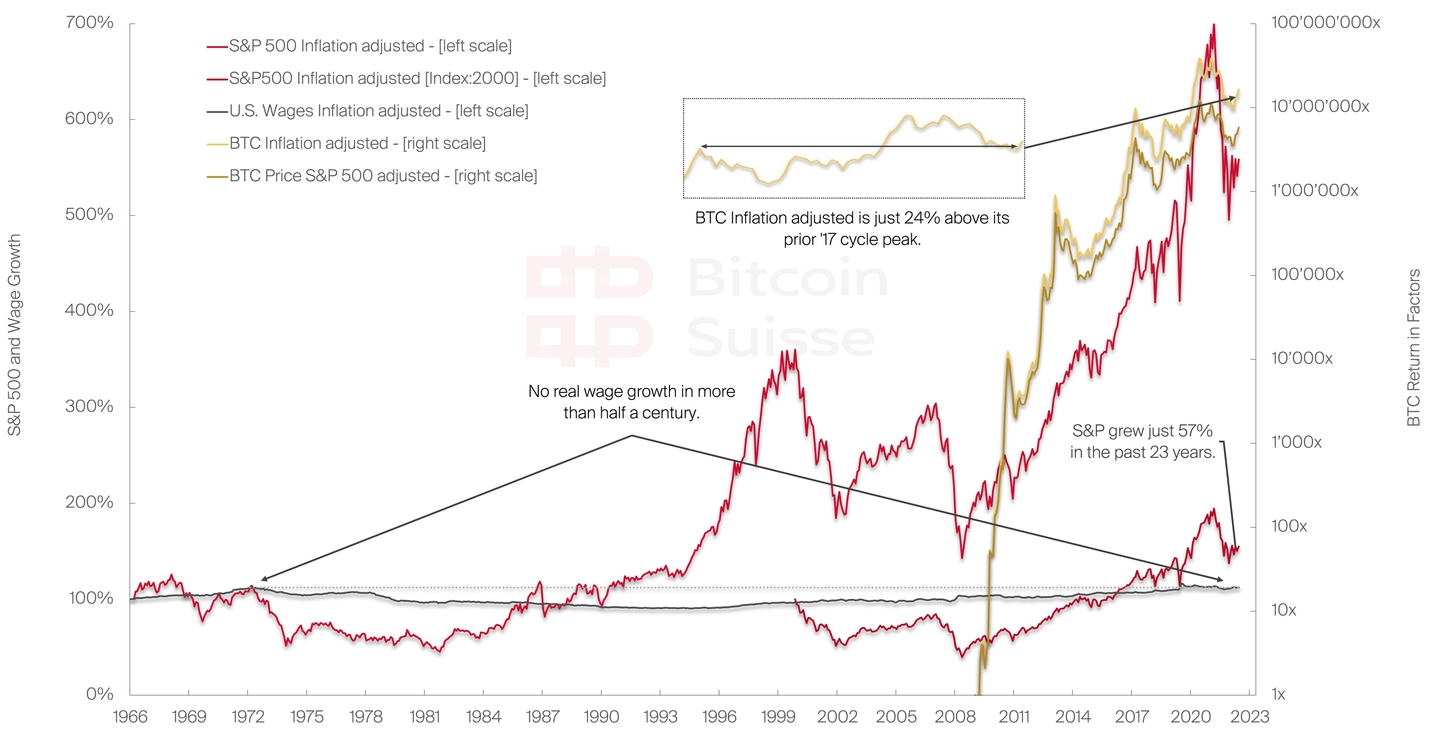

The growth and price appreciation of crypto and Bitcoin is tremendous, when considering the percentage growth in isolation. It becomes even more significant, however, when comparing how other assets, or everyone’s personal income has been growing over the years. Real Wages, i.e., wages adjusted for inflation, did not grow in more than half a century. Since 1966 wages grew just 12 % in real terms, implying that roughly two generations later, despite tremendous productivity increases, the respective pay did not reflect these improvements in any form. Moving towards the investigation of the adjusted equity returns, it turns out that the S&P 500 only grew by 57% since 2000, over more than 20 years. Therefore, the S&P 500, inflation adjusted, returned less than 2% p.a. (1.98%), and can almost be considered an inflation benchmark with higher volatility.

In contrast, Bitcoin’s performance does not deteriorate to any notable extent, when adjusting for inflation. Even adjusting BTC’s performance to the performance of the S&P, the performance does not get lowered considerably. Bitcoin´s performance is indicated in billion percent on the right y-axis, on a logarithmic scale, in order to fit on the chart. Even if BTC´s performance was to be re-indexed over the past years, its performance leaves all other asset classes behind by multiple orders of magnitude. Given the tremendous growth and substantial outpacing of the best performing equity indices, it can be considered irresponsible to not have a reasonable allocation and exposure to crypto in a properly diversified portfolio.

The most significant part is that BTC, inflation adjusted, is trading just 24% above its 2017 cycle peak. BTC’s adoption has improved substantially, and its fundamentals are more solidified, yet its price is currently sitting at inflation adjusted price levels last seen more than 5 years ago.

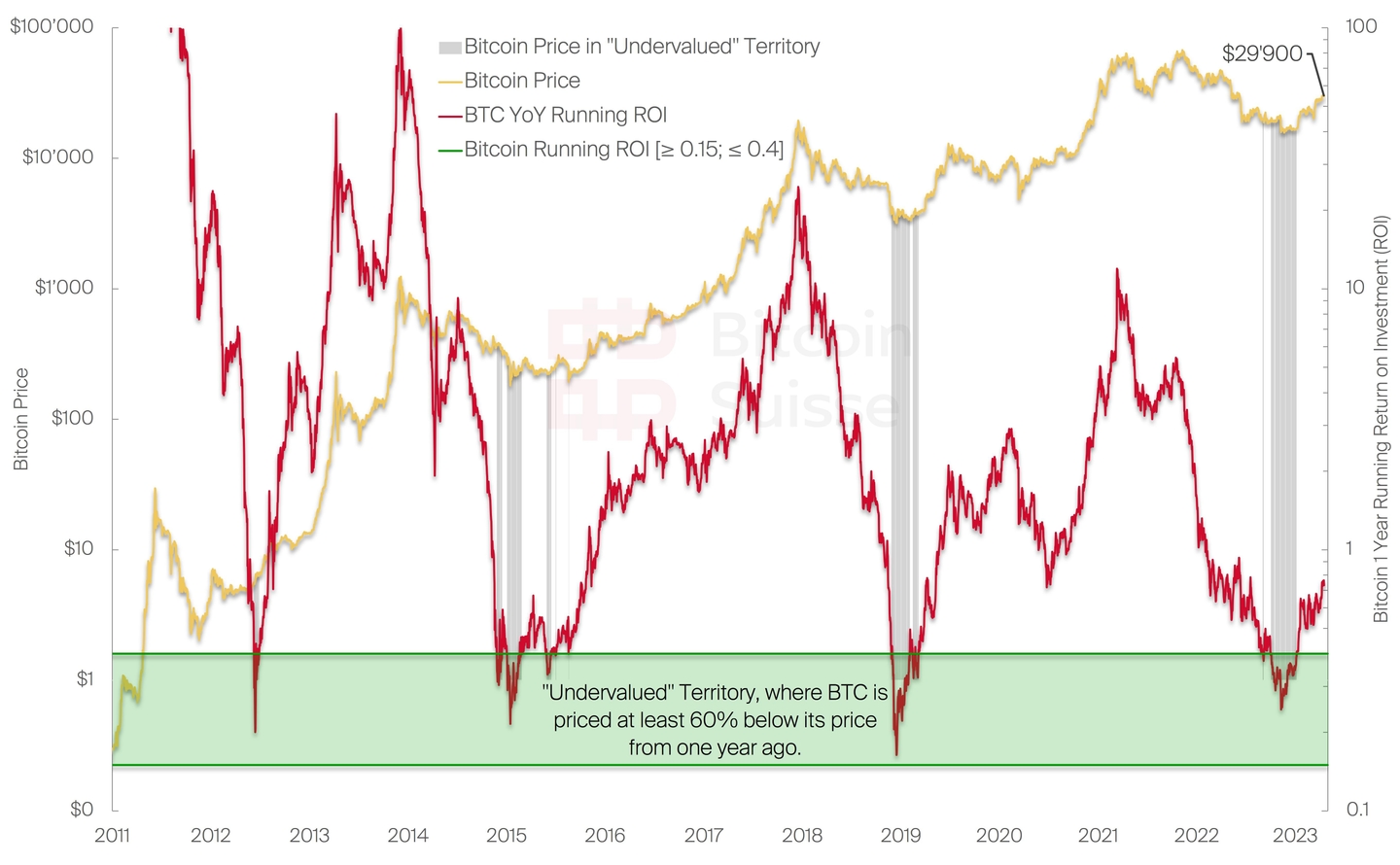

5. Bitcoin price drawdowns

The relative underpricing of BTC becomes most pronounced and can be judged easily once the one year running return on investment (ROI) gets plotted. The one year running ROI compares BTC’s current prices to its prices from 365 days ago and determines the respective out- or underperformance of its price over the past year. Overall, a very homogenous picture can be observed. Bitcoin’s peak overvaluation in hype cycles follows a downwards trend, which is consistent with its logarithmic price progression we observed in the last edition. On the contrast, the bottom bear market undervaluations tend to visit the same price drawdown region, market as the green “undervalued territory”. Prices in the undervalued territory are at least 60% below the price from one year ago, and indicate, that there was a steep decline in price due to a change in the market cycle. Exactly 683 out of 4845 days so far BTC has been trading in the “undervalued” territory, priced at least 60% below its price from one year ago. Bitcoin’s running ROI is only this low 14% of the time, offering rarely seen entry prices. If the prices converge back into the $20-25’000 region, the running ROI will move closer towards the “undervalued” territory again.

6. How does it fit into the current situation?

Given the current troubles surrounding the macroeconomic situation and the resulting financial system it is reasonable to ask the question “what will happen with the crypto industry going forward?”. The simple answer is: “Crypto will survive”. We will briefly assess the overall situation and piece together the facts to back the case for crypto going forward.

It is undeniable, that there are overall stringent macroeconomic and monetary conditions, including tight liquidity, high interest rates and sustainably elevated inflation levels. Following years of zero interest rate policies, substantial quantitative easing (QE), effectively flooding the financial system and the economy with cheap liquidity, last year marked the beginning of the steepest interest hike ever, raising interest rates by roughly 60x from their lows in less than a year (0.08% to 4.58%), combined with quantitative tightening (QT), effectively removing liquidity from the system. Going forward, the issues surrounding the financial system are unlikely to be stopped at any point soon, unless the current interest rate will be cut, and inflation will decline further, which will ease the overall stress on the economy. Though it would be favorable to see the financial conditions ease, it seems unlikely that a potential rate cut and liquidity injection, and or potential overall QE, will not cause inflation to pick up again, reigniting the vicious spiral our economy finds itself in. Furthermore, the “reversion” of the inverted yield curve never happens without further economic difficulties.

Going forward the implications for crypto in the interim might appear unfavorable. However, due to “foot voting”, which is the economic concept of businesses, capital and individuals are going to move where the ease of business is highest, which is especially the case for the dynamic crypto industry, enabling it to easily adapt to a changing economic and business environment relatively easy.

The crypto industry will continue to innovate and develop, and short-term headwinds usually back this trend, contrary to what one would expect. Just on the weekend amidst the “crypto bank crash”, more than one million new BTC wallets have been created, an attestation to an inevitable trend of adoption, which reflects the “case for crypto” outlined earlier, proving quantitatively, that it is irresponsible to not have any allocation to crypto in a diversified portfolio. Lastly, financial crises and times of economic turmoil in the past have offered extremely attractive investment opportunities and “cheap” prices, historically, which is why the current situation should counterintuitively be seen as a chance, not as a crisis.

7. Table of figures

Figure 1: (Chart) Bitcoin Suisse (Data) BTC Index – TradingView

Figure 2: (Chart) Bitcoin Suisse (Data) SP Global, BTC Index – TradingView

Figure 3: (Chart) Bitcoin Suisse (Data) OECD, Intitute for Supply Management, Chicago FED – TradingView

Figure 4: (Chart) Bitcoin Suisse (Data) SP Global, Bureau of Labor Statistics, BTC Index – TradingView

Figure 5: (Chart) Bitcoin Suisse (Data) BTC Index – TradingView

8. Disclaimer

The information provided in this document pertaining to Bitcoin Suisse AG and its Group Companies (together "Bitcoin Suisse") is for general informational purposes only. The information represents the opinion of Bitcoin Suisse at the date of issue. It should not be considered exhaustive and does not imply any elements of a precontractual or contractual relationship nor any offering or advice of any kind. Bitcoin Suisse does not provide tax, legal, or investment advice, and the information contained in this document do not take into account the specific investment objectives or financial situation of any individual person. While the information is believed to be accurate and reliable, Bitcoin Suisse and its agents, advisors, directors, officers, employees, and shareholders make no representation or warranties, expressed or implied, as to the accuracy or completeness of the information contained in this document. Bitcoin Suisse reserves the right to amend or replace the information contained herein, in part or entirely, at any time without notice and undertakes no obligation to provide the recipient with access to the amended information or to notify the recipient hereof. Investing in crypto assets or any other investment may entail certain risks, including market, liquidity, credit, technical and operational, as well as legal and regulatory risks and may be subject to other relevant factors. Bitcoin Suisse does not guarantee the performance of any investment, and past performance is not a guarantee of future prices. Investment decisions should be made solely based on a thorough evaluation of the specific investment objectives and financial situation of the individual person concerned. Therefore, Bitcoin Suisse expressly disclaims any and all liability that may arise from decisions based on this document. The information provided is not intended for use by or distribution to any individual or legal entity in any jurisdiction or country where such distribution, publication, or use would be contrary to the law or regulatory provisions or in which Bitcoin Suisse does not hold the necessary registration, approval, authorization, or license, in particular in the United States of America including its territories and possessions. In particular, Bitcoin Suisse is not registered with the U.S. Securities and Exchange Commission as a broker-dealer under the U.S. Securities Exchange Act of 1934, as an investment adviser under the U.S. Investment Advisers Act of 1940, or with any other competent authority under any applicable federal or state laws in the United States of America. Therefore, Bitcoin Suisse does not offer any services to “U.S. Persons”, as defined under applicable U.S. laws. This material is not intended for U.S. Persons and does not constitute a solicitation of any offer to U.S. Persons. Except as otherwise provided by Bitcoin Suisse, it is not allowed to modify, copy, distribute, transmit, display, reproduce, publish, license, or otherwise use any content for resale, distribution, marketing of products or services, or other commercial uses. Bitcoin Suisse 2023.

Related Articles

Tech Insights

Tech InsightsMidnight: Verifiable Yet Private, the Fourth Generation of Blockchain

For more than a decade, blockchain developers and enthusiasts have promoted state integrity as their core unique selling proposition, emphasizing that transactions on public blockchains are accessible and visible to everyone.

12 Mar 20265 Min Tech Insights

Tech InsightsBitcoin ETF Decision: Examining the Landscape Leading to the Potential Green Light

In the dynamic world of cryptocurrency, the spotlight is currently fixated on a historic event—the potential approval of a U.S. Spot Bitcoin ETF. As we approach the final deadline for ARK on January 10th, Bitcoin Suisse delves into the unprecedented developments that have set the stage for what could be a transformative moment in the industry.

9 Jan 20247 Min Tech Insights

Tech InsightsExploring Supply Transparency

A joint research report by Coinmetrics and Bitcoin Suisse Research.

17 Oct 202312 Min

Personal Support, Every Step

Our team of native experts are here to provide you with the tools, insights and support you need.

Opening hours

24/7 online

Monday to Friday: 7am to 7pm

Call us toll-free from Switzerland

Call us from abroad