The Bitcoin Halving: Supply and Demand

Luca Gnos

15 Feb 20244 Min

_Digital assets are the most vibrant, most disruptive, most dynamic, most performant, and most transformative asset class available to mankind. We enter an era where digital asset exposure becomes the norm, where a lack of exposure equates to risk._

Supply and Demand

In his article “13 Digital Asset Predictions” in the Crypto Outlook 2024, Dominic Weibel looked at the law of supply and demand and outlined arguments on why the price equilibrium of BTC should be substantially higher some months down the line.

Demand

We will briefly summarize some of the key demand drivers stemming from macro, institutions, demographics, risk mitigation and adoption.

From a macro perspective Dominic mentions that the rate cycle likely peaked, possible QE measures upon yield curve un-inversion become more likely, global liquidity is transitioning into an uptrend, expansionary fiscal policies are at play, election year with multiple pro crypto candidates is upon us and that an overall risk-on setup seems to be looming.

He then weighed on the boost in acceptance, legitimacy, and regulatory clarity of digital assets induced by the approval of the first spot ETFs in the U.S and that gaming, betting, social applications, DeFi and RWAs will likely attract millions of new users in 2024.

Combined with the fact that the digital asset adoption rate of millennials is factors higher than that of baby boomers, it is reasonable to assume that a fair share of the demographic wealth flows towards millennials end up in digital assets (Galaxy estimates a daily flow of $20M-$28M across the next 20 years).

Supply

On the supply side, the hardcoded Bitcoin Halving estimated for April 2024 limits the structural supply available to the demand sources outline above. Post-halving, there is $8.5B less potential sell pressure hitting the orderbooks (calculated based on BTC at $52'000). Moreover, Bitcoin historically yielded strong gains in the year that followed the halving and early trends of this 4 years cycle echo past patterns.

To add some context, the amount at which the Bitcoin price was stable decreases by half, from at least 328’500 BTC per year before the halving to only 164’200 BTC per year after the halving. If we now multiply these 164’200 BTC with the current Bitcoin price, we get the above-mentioned amount in USD, which equals the new supply hitting the market in a year. This leads to the fact that for the Bitcoin price to depreciate, the demand for Bitcoin would have to fall by 50% after the upcoming halving in April. Yet, we expect demand to increase.

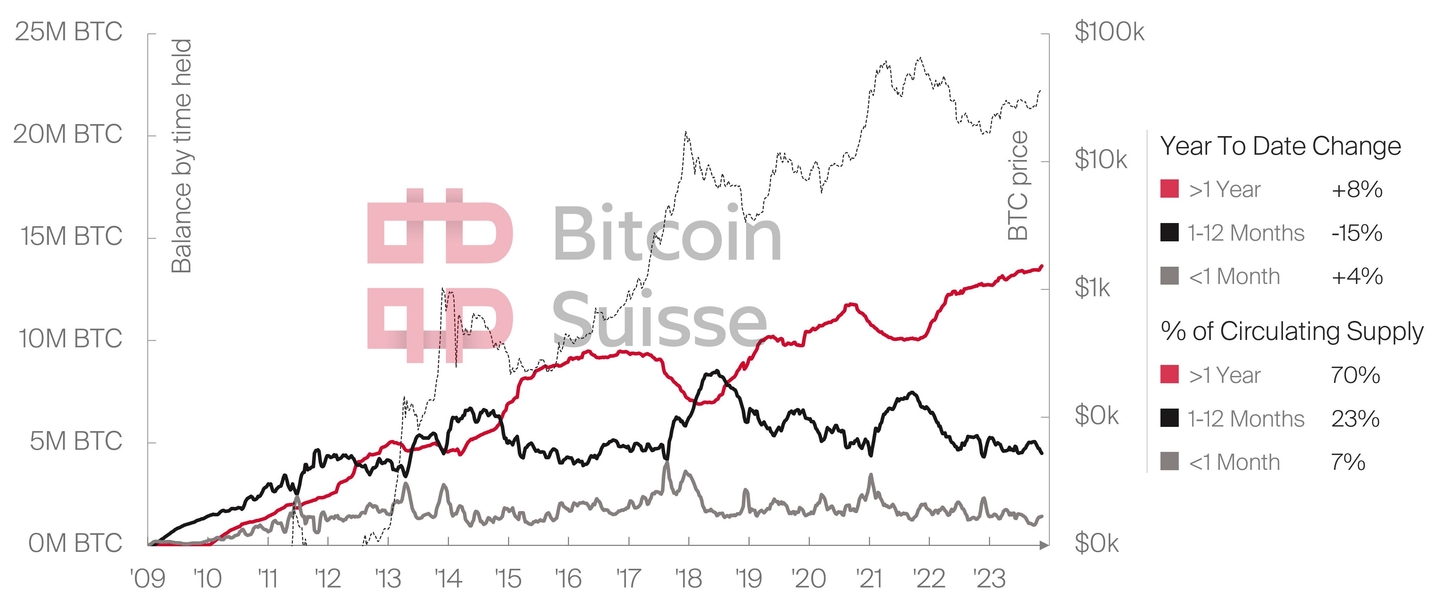

The supply dynamics are indicating that long-term holder supply is on a sustained upward trajectory, while the short-term holder supply flashes exhaustion and mid-term holder supply is ranging at multi-year lows. We derive strong signs of holder conviction, leaving ample room for growth as increasing supply age is a proxy for illiquidity. Exchange reserves are also showing a sustained multi-year decline, recently hitting an all-time-low of 2M BTC. This suggests that BTC is migrating towards more illiquid and less speculative venues that puts the available supply at historical lows, another strong signal of elevated long-term positioning and accumulation. Note that supply leaving exchanges is also subject to institutional and TradFi vehicles like custody.

Conclusion

Combining the above, there is a major supply crisis assembling. For a fair number of holders, Bitcoin is a one-way street, a buy and never sell asset held by a community of believers with high conviction. Meanwhile, regulatory derisking and major streams of adoption start to materialize, bringing multiple demand verticals that stumble into the halving event and historically low supply dynamics. Never in digital asset history did we have such a textbook setup for price discovery.

To sum up, we project that liquidity will chase strong narratives and the strongest narrative is anchored within the digital asset class. Since these are a very rhythmic and reflexive asset class, we might face the culmination of catalysts engineered for more than a decade. This could result in an endless twap into digital assets with ever reinforcing feedback loops while price agnostic flows from institutions run into major supply constraints. Digital assets are ready for prime time. In our view, the supercycle is closer than ever.

Related Articles

Education

EducationThe Open Network: Global Payments for 950 Million Telegram Users

Telegram brings various applications of blockchain technology to many of its users, enabling them to make free peer-to-peer payments, use mini-apps and play games, among other things. Telegram also offers monetization opportunities for developers and content creators.

3 Mar 20256 Min Education

EducationA Day In The Life Of A Crypto Scammer

As part of International Fraud Awareness Week, we take a closer look at the daily life of a crypto scammer. We'll highlight some common fraud tactics by sharing the stories of two scammers, Jordan and Marco, who try to steal people’s cryptocurrencies every day – using a variety of methods.

21 Nov 20247 Min Education

EducationSeasonality, the bitcoin halving, US elections and the FED rate cuts

You’re likely familiar with the famous song by the American rock band Green Day, "Wake Me Up When September Ends." In the world of investing, particularly when it comes to U.S. stocks, this phrase holds meaning beyond just the song title. In recent weeks, much has been said about the seasonality of both equities and bitcoin, and for good reason: August and September have historically been the worst-performing months for U.S. stocks and bitcoin.

3 Oct 20248 Min

Personal Support, Every Step

Our team of native experts are here to provide you with the tools, insights and support you need.

Opening hours

24/7 online

Monday to Friday: 7am to 7pm

Call us toll-free from Switzerland

Call us from abroad