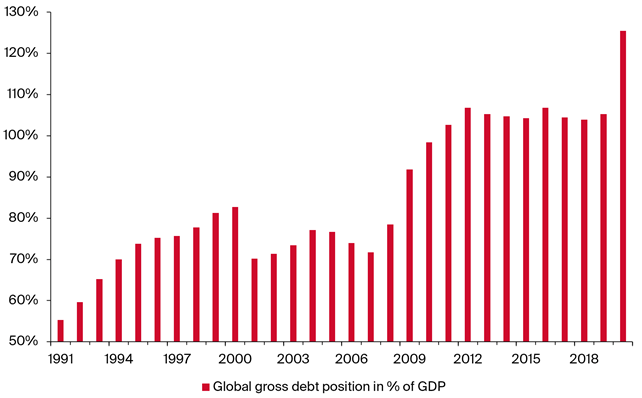

To give some historical context, the figure was 70% twelve years ago, just before the financial crisis, by the end of which it had lurched up to around 106%. After that, virtually no progress was made in reducing this debt burden, and so the effects of the Covid crisis and the financial crisis compound together.

The debt burden varies widely across countries, of course, with the US at 131% and Japan more than double that, while Germany is at 73% and Switzerland just below 50%. These figures would be lower, if government assets are netted off, and substantial portions of this debt is now held by central banks. Nevertheless, the big picture is clear: government debt was already very high before Covid, and it has soared as a result of the virus. The surge represents partly the lost tax revenue and increased benefits that operate automatically in a recession, and partly new measures to counter the economic weakness. There can be some improvement as the economy recovers, but it will be a grinding and slow process, and there are few signs of the political will to take the hard decisions needed to bring it down faster.

Yet, the risk that this extraordinary debt surge becomes dangerously unsustainable lies in the future; for now, it seems almost benign, and the reason is that the cost of debt service has barely risen or has even fallen, as a result of the parallel policy of ultra-easy money. Central banks around the world have abandoned the tentative steps towards tightening underway before the crisis and instead embarked on new rounds of easing. Zero or negative rates are now the global developed economy norm, and even many emerging countries have astonishingly low rates; quantitative easing has been expanded, not only in size but also in scope, with central banks buying assets that would have been unthinkable a few years ago, ranging from equities (Japan), to derestricted quantities of peripheral-economy bonds (Europe), and corporate and junk bonds (US).

These monetary measures have been highly successful in supporting asset prices, driving equity market multiples to high levels and compressing credit spreads. This has undoubtedly helped to minimise the depth of the Covid economic slump, but at the cost of over-valuing some assets in ways that inevitably distort resource allocation. For consumer good prices, it has probably helped to mitigate the risk of deflation, we don’t really know, but it clearly has not yet created an inflation.

And, this lack of inflation is just as well, for anything more than mild inflation could face central banks with an unpleasant dilemma: either they tighten policy (pushing rates up and ending asset purchases), which would trigger an economic downswing and raise the cost of servicing the debt mountain; or, they pretend the inflation isn’t happening, which works for a while until they lose credibility and bond yields then soar out of their control – unless they impose ‘financial repression’, with exchange controls and/or rules that force domestic investors to buy government bonds at low yields, effectively a confiscatory wealth tax.

So, how likely is the risk of such inflation? At present, not very likely, due to the slump in demand caused by Covid. And there is certainly a good chance that this slump will be followed by a gradual economic recovery, allowing central banks to start gently tightening policy over a period of several years, keeping inflation under control and avoiding the extreme scenarios just mentioned. But there are also darker scenarios. The “scarring” from Covid, with lower-skilled and older people driven out of the workforce and companies bankrupted, reduces economic capacity and may run the economy into the inflationary buffers much earlier than expected, unless countered by well-targeted re-training programmes. The move towards more nationalism in politics, and the new Cold War between the US and China, may encourage uncompetitive oligopolies that can push up prices easily – the recent antitrust action against the Google ad-monopoly appears to go against this, but has yet to be shown to have real teeth.

The bottom line is that we just don’t know how big is the risk of an inflation large enough to tip the debt mountain from benign to deadly – all we can say is that it’s a much bigger risk than it was before Covid.

Bitcoin in an era of debt and inflation

Bitcoin could have been designed as the perfect asset to protect investors from this debt-inflation spiral – and indeed, the need for such an asset does appear to have been one of its original inspirations. Because the supply of additional Bitcoin rises at a reducing rate and eventually stops, it is hard-wired to have a deflationary bias that no fiat currency could ever have. Provided there is ongoing demand to hold Bitcoin, as an investment and/or transactions asset, that has at least a loose positive correlation to overall nominal global GDP, then both real economic growth and inflation will, over time, create a tendency for its trend price to rise. And the risk of ‘financial repression’ mentioned above could add an extra impetus to this, for Bitcoin holdings, whether permitted or not permitted under dystopian future scenarios, could be difficult to detect.

Gold has traditionally been the asset held by investors concerned about runaway debt and inflation, but interestingly, it was the “dog that did not bark” in 2020, with its prices showing little strong uptrend in a year when cryptocurrency prices, though volatile, did trend upwards. One prosaic reason for that is that global jewellery demand has been weak, for a number of reasons, notably the decline in formal weddings in India and elsewhere; central bank demand has also been weak, for reasons that are not clear. But another key reason for the divergence between gold and cryptocurrency prices is that gold not only pays no interest, but actually costs money to hold. By contrast, cryptocurrency holdings can be used to generate substantial income, and we now turn to consider this.

Zero interest rates, the positive yield on cryptocurrency holdings, and the future of conventional banks

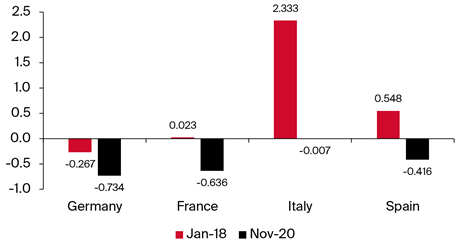

While near-zero or outright negative interest rates were already part of the ‘new normal’ when Covid struck, the monetary policy response to the virus has intensified their effect in a major way. In countries such as Switzerland, some banks have lowered the thresholds on which they charge depositors interest, but more profoundly, and globally, the action of the US Federal Reserve and others in buying investment grade and junk-rated bonds has compressed credit spreads. The result is that in many currencies, it is now barely possible to earn positive yields on fixed-income portfolios even by taking substantial credit and/or duration risk. Even emerging market debt portfolios now offer yields that would in the past have been associated with currencies such as the Euro or Swiss Franc (Illustration 2).