Five Megatrends in 2021

Feb 5, 2021 - 10 min read

- Institutional adoption of cryptocurrencies as a component in a multi-asset portfolio is set to grow.

- Ethereum 2 is likely to become the largest staking market, with implications such as the development of an ETH2 futures and higher ETH borrowing and lending rates in DeFi.

- The stablecoin market has the potential to grow much larger but will have to comply with new regulations for the sector.

- The first Parachain Lease Offerings on Polkadot and Kusama will draw the attention of crypto investors and lead to interesting dynamics in the DOT markets.

- New decentralized finance protocols will further illustrate the power of composability and – if successful – grow the space by an order of magnitude.

The year 2020 has brought major progress to the crypto world. The market structure has seen further improvements in terms of capacity and liquidity. Fundamental breakthroughs in blockchain technology and cryptography have happened, such as with the launch of Ethereum 2 or Polkadot, and public blockchains have found their first real product-market fit in the form of decentralized finance (DeFi).

This article attempts to spot and outline the next big trends – what will drive crypto markets in 2021? What will the crypto landscape look like?

Trend 1: Institutional Adoption of Crypto

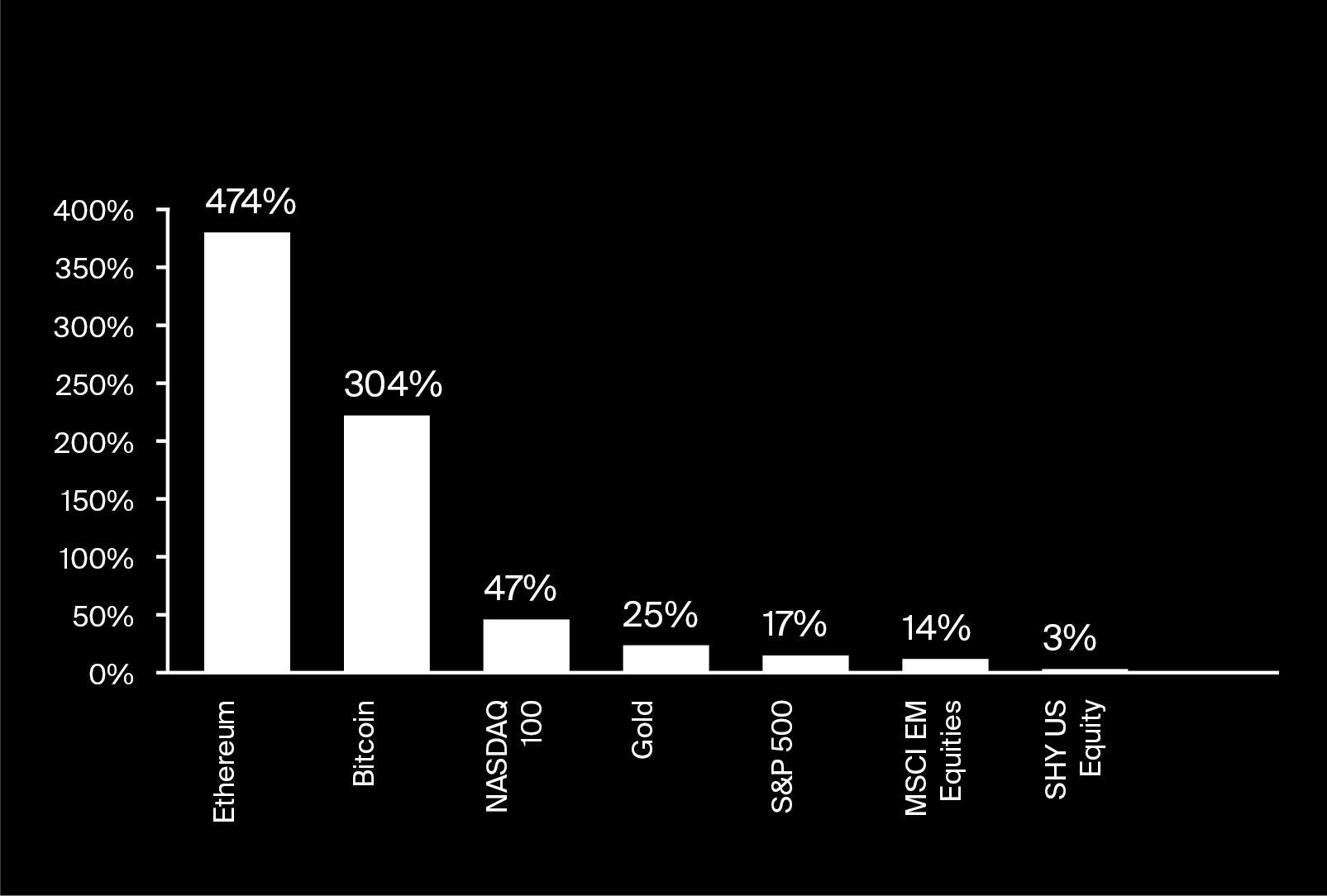

“Slowly at first, then all at once” – there is hardly a phrase that better describes the swift change of heart that many prominent investors had in 2020 towards cryptocurrencies. Bitcoin has become an investable asset, and cryptocurrencies as an asset class which outperformed other assets classes by a fair margin can no longer be ignored. The default question for portfolio managers seems to be switching from “Why should I invest in Bitcoin?” to “Why should I not invest in Bitcoin?”.

Among the first ones to make their investment public was Paul Tudor Jones, who wrote about it in his investor letter in May 2020 and allocated a low single-digit amount to Bitcoin as a hedge against inflation. Others, such as Stanley Druckenmiller or BlackRock’s Rick Rieder, followed later with positive statements or allocations towards Bitcoin. It is reasonable assume that this trend continues in 2021 and more investors decide to allocate to Bitcoin both strategically and tactically.

[Bitcoin] scores 66% of gold as a store of value [in our internal assessment], but has a market cap that is 1/60th of gold’s outstanding value. Something appears wrong here and my guess is it is the price of Bitcoin.

Paul Tudor Jones

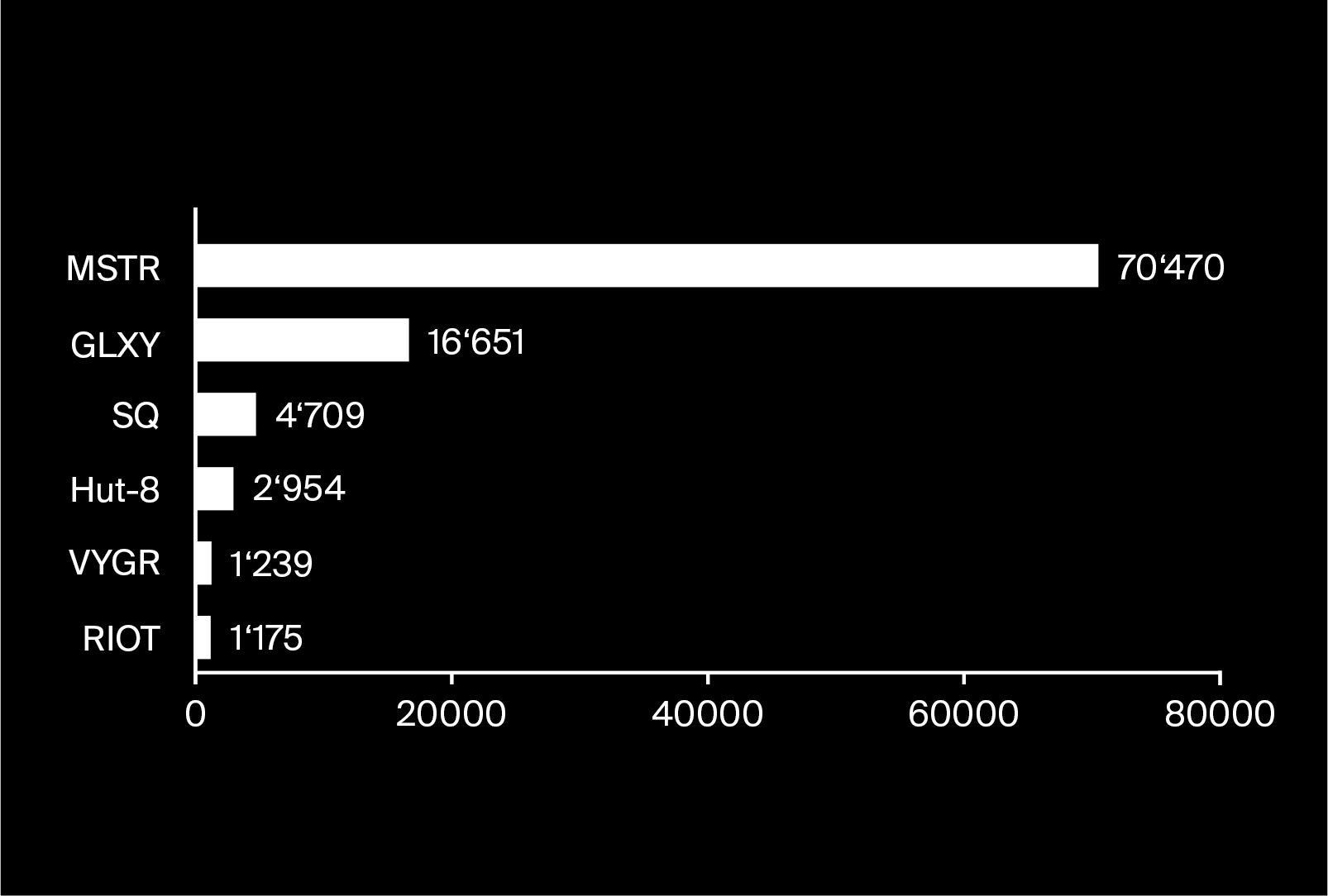

On top of that, a few companies started to use Bitcoin as a treasury reserve asset. At the time of writing, around 100’000 BTC (or about 0.5% of the supply) are held by publicly traded companies, such as MicroStrategy (70’470 BTC), Galaxy Digital (16’651 BTC) or Square (4’709 BTC). Another massive amount of BTC is held by the Grayscale Bitcoin Trust, which now owns close to 600’000 BTC (or about 2.7% of the supply) and has experienced rapid inflows in 2020, probably not least due to arbitrage between Bitcoin spot markets and the GBTC premium of up to 40% to its net asset value.

The reasons for an investment into Bitcoin and other cryptocurrencies vary. An often-cited reason is the current and future macroeconomic environment, in which cryptocurrencies are ideally placed, as outlined in the dedicated article on “Macroeconomics in Covid and after: the Perfect Storm for Cryptocurrencies” by Giles Keating in this report. Bitcoin is also seen as an alternative and challenger to gold, and cryptocurrencies in general as a bet on the future importance of blockchain technology in the world.

Do I think it will take the place of gold? Yes I do, because it’s so much more functional than passing a bar of gold around.

Rick Rieder

Additionally, the regulatory environment for cryptocurrencies is becoming clearer and provides the necessary legal certainty for investments into the asset class. Professional custody is largely a solved problem, and sophisticated trade execution techniques enable even larger investments. Following positive remarks from the CFTC Chairman Heath Tarbert about Ethereum, the CME will also launch ETH futures in February, which will further improve market access beyond Bitcoin.

Recently, S&P Dow Jones Indices also announced that they would create indices for various cryptocurrencies. This might lay the groundwork for a long-awaited Bitcoin ETF, applications for which have so far always been declined by the SEC, mainly due to price manipulation concerns. A trusted price source might alleviate these concerns.

Another implication of institutional adoption of Bitcoin and other cryptocurrencies is that correlations to other asset classes might increase in the future. The holder structure of cryptocurrencies currently still differs significantly from that of other asset classes, which likely plays a role in the uncorrelated nature of the asset class. As cryptocurrencies become a more regular inclusion in multi-asset portfolios, the correlation to other assets in such portfolios might increase due to rebalancing and more stringent risk management considerations.

Trend 2: Ethereum 2 and Staking

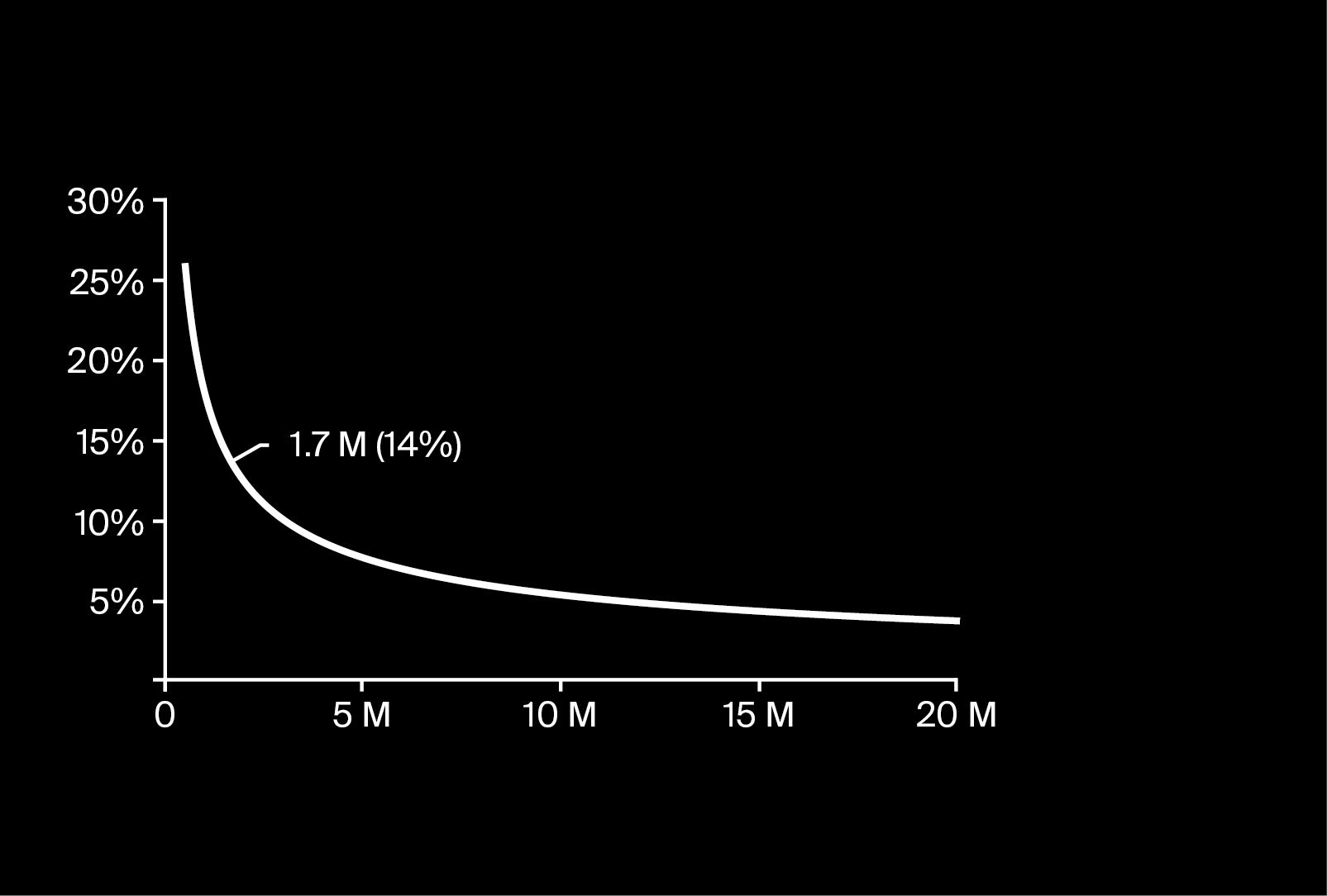

The Beacon chain of Ethereum 2 has finally launched on December 1 and represents a seminal achievement for blockchain technology. This is the first stage (or Phase 0) of a full deployment of Ethereum 2 and brings the possibility to stake ETH to earn staking rewards. These depend on the overall amount of staked ETH in the network (the formula can be found here); currently, around 1.7 million ETH were sent to the deposit contract for the beacon chain, resulting in an approximate staking reward of 13.6%. This reward is denominated in ETH, so any effective returns in USD (or EUR, CHF) highly depend on the ETHUSD price.

ETH is set to become a dominant player in the staking landscape – it will be by far the most valuable proof-of-stake blockchain, and staking returns compare well to other stakeable currencies.

At the moment, however, and until later phases of Ethereum 2 enable transfers of the cryptocurrency on the new blockchain, staking ETH represents a vote of confidence in the development of Ethereum and comes with an unknown lockup period. The Ethereum staking equilibrium will only fully establish, and the market grow to its real size, once full convertibility is enabled. Whether or not that happens in 2021 in yet unclear. An additional consequence of large ETH lockups might be increased volatility in all ETH markets, as liquid ETH gets deployed for staking instead.

In the early stages of Ethereum 2 staking, an ETH2 futures market might also develop. Investors in this market will likely demand a liquidity premium, and ETH2 futures might trade at lower prices than ETH due to the lockup period. Additionally, markets for converting staked ETH to liquid ETH might develop both in centralized and decentralized manner – in this case, the conversion rate between the two variants does not need to remain at 1:1 (this rate is only ever guaranteed one-way for ETH to ETH2 through the deposit contract), and the degree to which de-pegging from 1:1 happens could serve as an indicator of perceived counterparty risk (either of a smart contract or a centralized service provider).

As more ETH gets staked and rates start to stabilize, this will also have an impact on yields on ETH in DeFi. Currently, the lending and borrowing rates for ETH stand at ca. 0.1% and 2% – over time, these should see a moderate increase towards the rate of staking rewards, or more precisely: towards the expected average staking rewards rate until transferability minus the costs of running an ETH2 validator (accounting for the tail risk of getting slashed). The presence of more tokenized Bitcoin on Ethereum (such as wBTC) could accelerate this process, as Bitcoin can serve as collateral in DeFi lending protocols to borrow ETH, stake it, and earn staking rewards. Similar mechanisms could unlock for other proof-of-stake chains should they either develop an own DeFi ecosystem or build a bridge to the existing one on Ethereum.

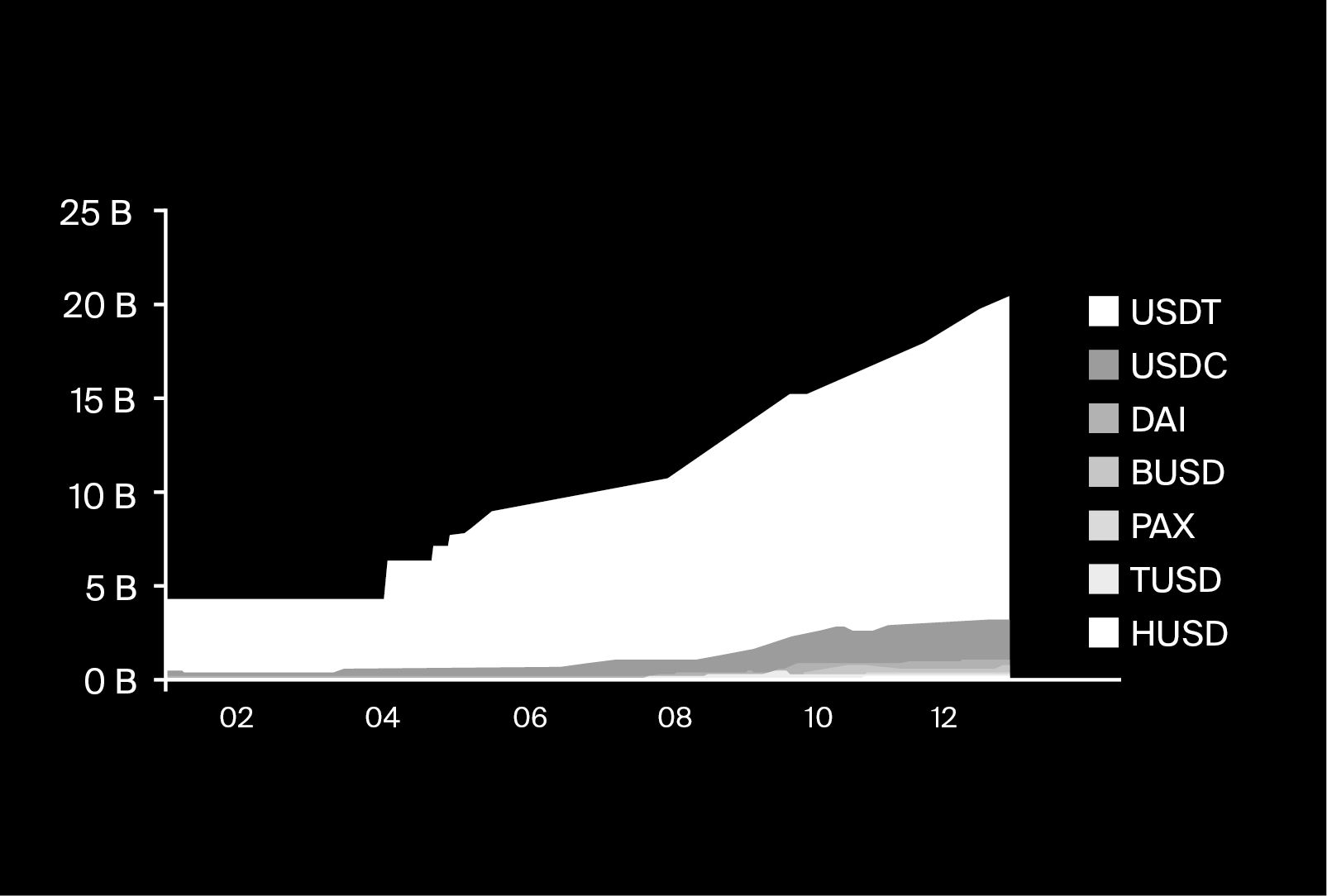

Trend 3: Stablecoins

Stablecoins have had a phenomenal year in 2020. The total stablecoin supply grew from ca. 5 billion to more than 25 billion, and they represent an important interface between the fiat currency world and the crypto ecosystem.

The majority of the stablecoin supply is on Ethereum. One catalyst for this increase has been the DeFi hype during the summer, where high yields, often >100% p.a., were available for providing USD stablecoin liquidity to protocols. This led to high demand and an inflow of capital to the space. Stablecoins pegged to the USD remain extremely dominant, and stablecoins pegged for example to the EUR have a negligible market cap. This may change in the future – in principle, the building blocks available in DeFi could be customized to allow for efficient forex trading. Demand might come, for example, from arbitrageurs that operate in the (fairly liquid) BTCEUR or ETHEUR pairs on centralized exchanges, or – in the long run and depending on the competitiveness of exchange rates – commercial and speculative forex traders. If such demand arises, so will the supply of non-USD-pegged stablecoins.

There might be regulatory headwinds coming for stablecoins, though. As governments and central banks around the world gear up for the launch of their own central bank digital currencies (CBDCs) in the wake of the inefficiencies in the current financial infrastructure exposed by the pandemic, privately issued stablecoins will receive more regulatory attention. As a first mover in the CBDC space, China has already banned private stablecoins backed by the Renminbi. The EU has proposed regulations that would also affect stablecoins, while the U.S. is exploring digital currency as well, but no clear direction for private stablecoins was given so far. How large the initial backlash can be was demonstrated by Libra (now Diem), who will launch in the first half of next year with a minimal version and a simple USD-pegged stablecoin. Over the next decade, however, privately issued stablecoins that are convertible to CBDCs through intermediaries might still become the go-to interface between CBDC ledgers and public blockchains.

Trend 4: Parachain Lease Offerings on Polkadot and Kusama

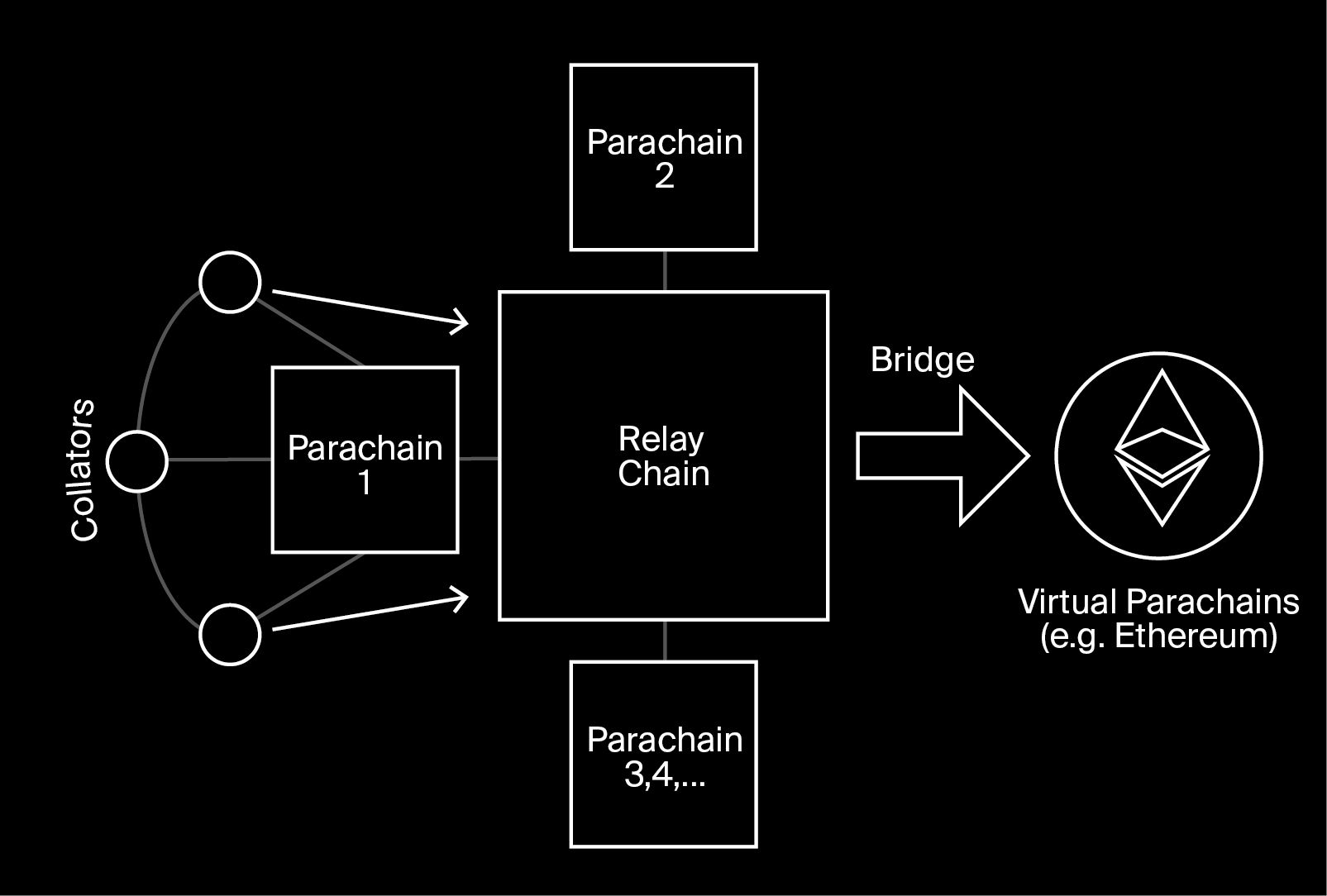

Polkadot launched its long-awaited mainnet in May 2020, and slightly after that handed over governance of the protocol to the community. Polkadot is set to become an important player for blockchain interoperability – a topic more closely described in the dedicated article “Interoperability: Where are we now and what can we expect for 2021” by Fatemeh Shirazi in this report.

Polkadot’s architecture (and that of its “canary network” Kusama) includes a relay chain and parachains. Parachains are customizable blockchains for each use case, such as high transaction throughput or strong privacy. The relay chain enables pooled security guarantees: Instead of securing each parachain individually, this duty can be outsourced to the relay chain, which improves the capital efficiency and likely reduces the overall required security budget.

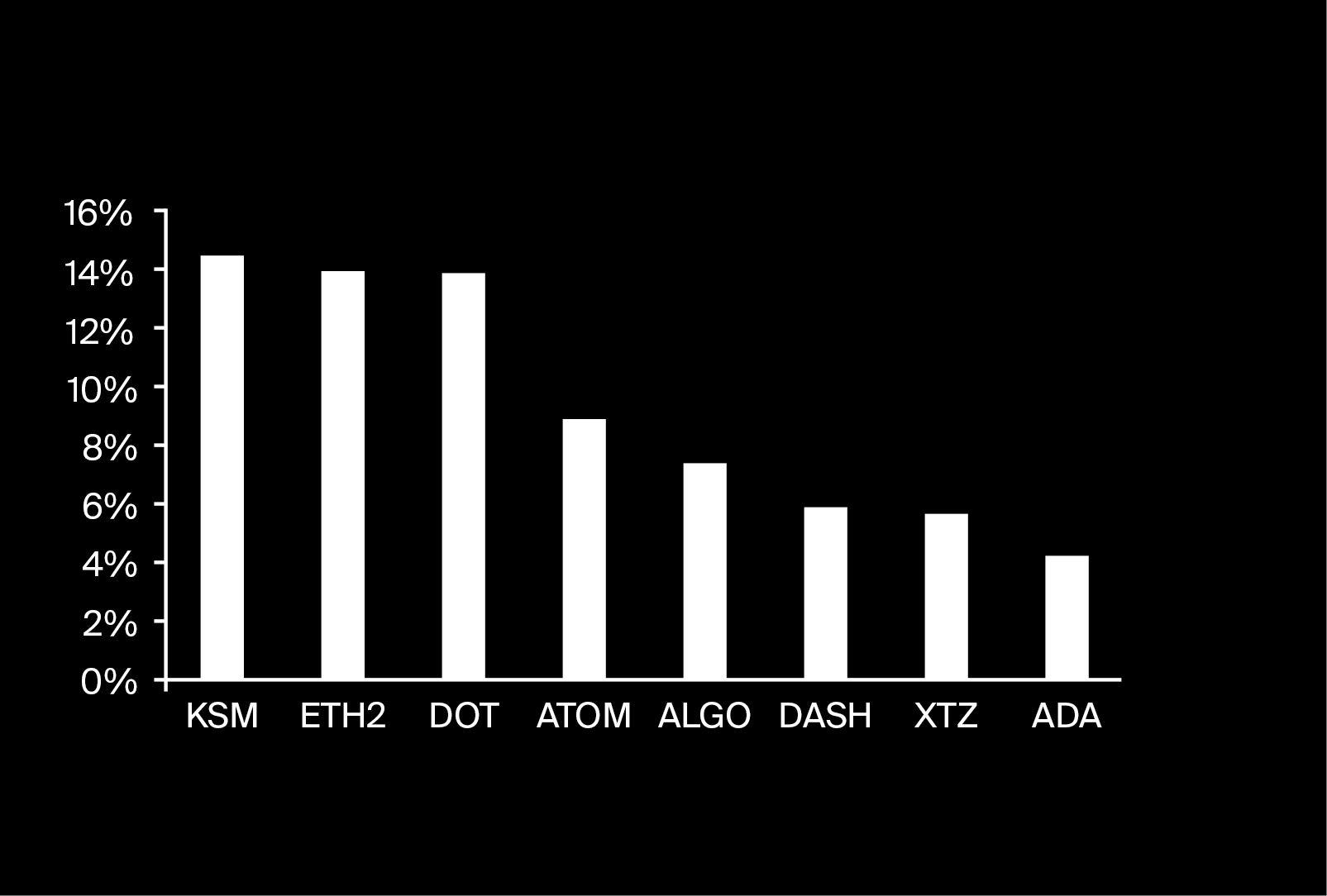

Projects looking to become a parachain of Polkadot will need to lock up DOTs, Polkadot’s native coin, for 6 to 24 months. This lock-up is in direct competition to the staking of DOTs, which currently yields around 13.5% annually (denominated in DOT). However, the economics of staking in Polkadot are designed in a way to encourage – as soon as parachains go live – a 50% staking rate of the total DOT supply, such that up to 50% of DOTs are available for parachain lock-ups.

Parachain slots are assigned in candle auctions, where interested parties can bid on the slot; in the medium term, there will likely be up to 100 slots available. Since projects looking to become a parachain will often lack the required DOTs, they can look to crowdsource these from other DOT holders and conduct a Parachain Lease Offering (PLO). This will require incentivization, for example in the form of tokens, that can make up for the forgone staking rewards.

PLOs will likely receive a lot of attention in 2021, both on Polkadot and Kusama. The returns that participants in the first few PLOs obtain might help in the economic incentive design for later offerings and will serve as an indication how they relate to the staking rewards rate. In principle, the game theoretical equilibrium for returns (in DOT) should lie slightly above the staking rewards rate, accounting for the longer lock-up period (at least 6 months in PLOs, 28 days for staking), project-specific execution risks, and the absence of slashing risk.

Trend 5: Growth of Decentralized Finance

2020 was the year of DeFi – many projects that were quietly building over the past three years have exploded in popularity, which was best seen in the skyrocketing total value locked (TVL) in various DeFi protocols.

This trend is likely to continue in 2021 – however, as mentioned above under Trend 2, DeFi protocols will have to compete with ETH staking for liquid ETH. Still, expansion of the DeFi universe through introduction of new projects happens quickly and will continue to attract liquidity for as long as yields remain high, or whenever composability between protocols opens up new possibilities.

One area that seems underexplored so far is DeFi derivatives. There are early examples of interest rate swaps that would allow to trade floating rates (which are the norm in DeFi) for fixed ones – which is currently only possible through centralized platforms that offer both perpetual swaps (which come with a variable funding rate) and futures contracts (with a fixed annualized premium or discount upon opening a position). Similarly, various protocols aim to capture the on-chain options market. Such upcoming derivatives platforms will likely battle for liquidity through governance tokens and liquidity mining.

What really sets DeFi apart from traditional financial infrastructure, though, are the immediate composability benefits that new projects gain. In DeFi, a structured product might be just a “zap” that, for example, simultaneously trades various options and futures in a single transaction using multiple protocols. A layered infrastructure is forming, with lending and borrowing platforms (such as Maker, Compound or Aave) and decentralized spot exchanges (such as Uniswap) as the base layer upon which others can build and innovate in a permissionless fashion.

The yields in DeFi on USD stablecoins can be thought of as the value of the dollar in the crypto ecosystem (plus smart contract risk, especially for the newer projects). An indication for that has existed long before DeFi took off, in the form of centralized USD borrowing and lending markets, as well as in the futures contango or backwardation, which enables yield generation from cash and carry trades. Historically and perhaps naturally, these yields increased during bull markets and decreased during bear markets. In the long run, however, as capital flow to crypto becomes even easier, the trend for those yields should be downwards and closer to traditional USD interest rates.

Last, but not least, as limited transactions throughput on the Ethereum chain imposes some restrictions on the use of DeFi due to high gas fees and hence transaction costs, a migration to layer 2 solutions might happen – Synthetix is an early adopter in the space and will use the layer 2 solution Optimism in the future. As a partial migration of some protocols might fracture the ecosystem and reduce composability, it is likely that this migration takes longer than expected as layer 2 solutions prove themselves stable and secure, but then happens quite rapidly once it starts.

Conclusion

The year 2021 is set to be exciting on all fronts – from broader recognition of cryptocurrencies as an asset class to fundamental advances for blockchain technology. New components of the ecosystem, such as Ethereum 2 and staking or Polkadot’s Parachain Lease Offerings, will allow to observe the game theory behind them unfold in real time in the markets. The “crypto experiment” is slowly maturing and transforming into a powerful ecosystem that can disrupt what is viewed as a store of value, how the financial infrastructure is constructed and how efficient and elegant business processes could be in the digital age.