Examining Crypto Volatility

Jul 7, 2020

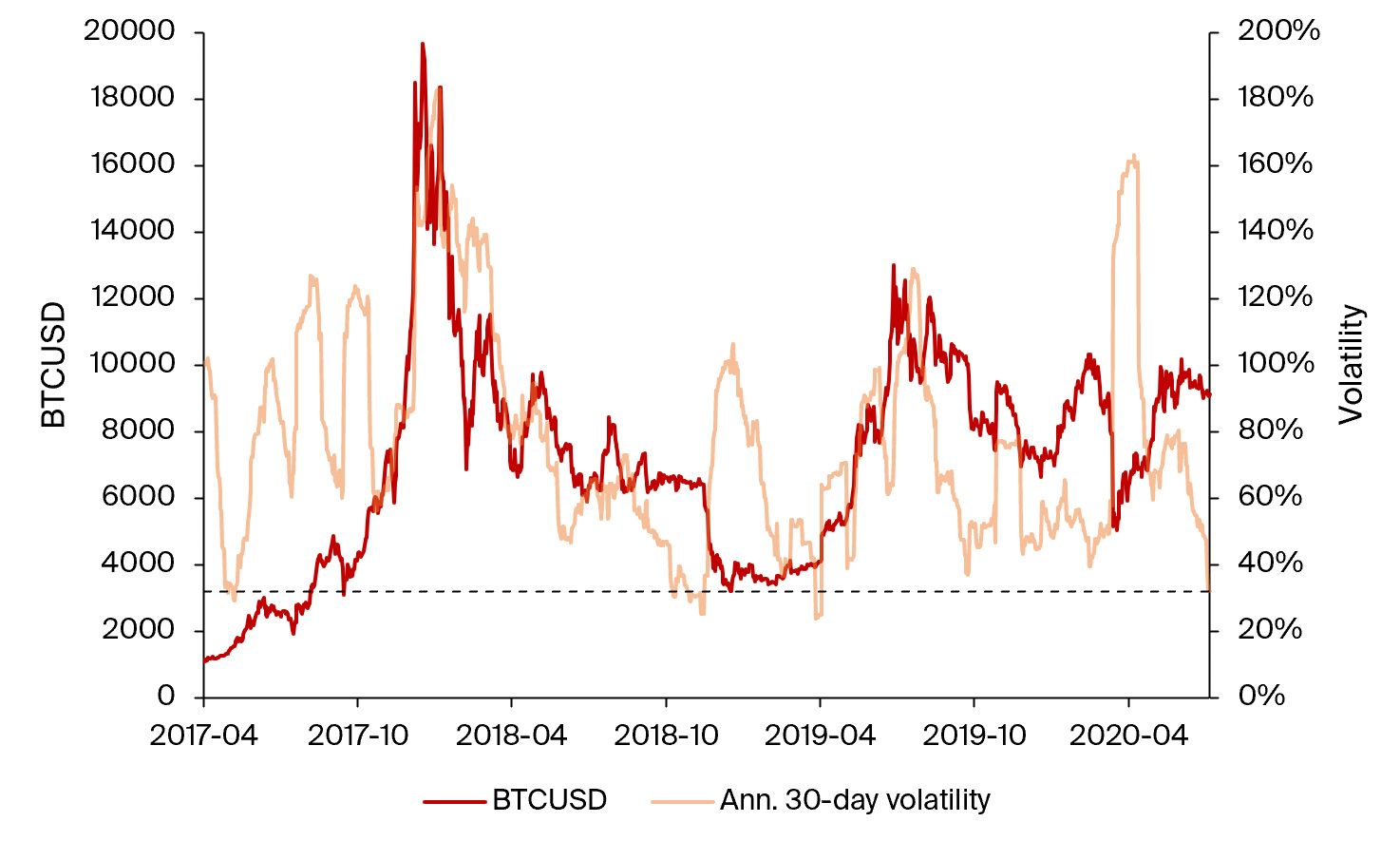

Crypto markets have been showing their calmer side over the past weeks. Both Bitcoin and Ether have recently shown low realized volatility in comparison to historical values. At the peak of the bull market in 2017 or during the large drop in March of this year, annualized volatilities of 150-200% (equating to 7-10% daily moves) were seen. Current 30-day volatility values of 39% for Bitcoin and 47% for Ether (annualized) reflect daily moves of 2-2.5%.

Illustration 1: Bitcoin and Ether 30-day volatility (annualized) is currently low in comparison to historical values.

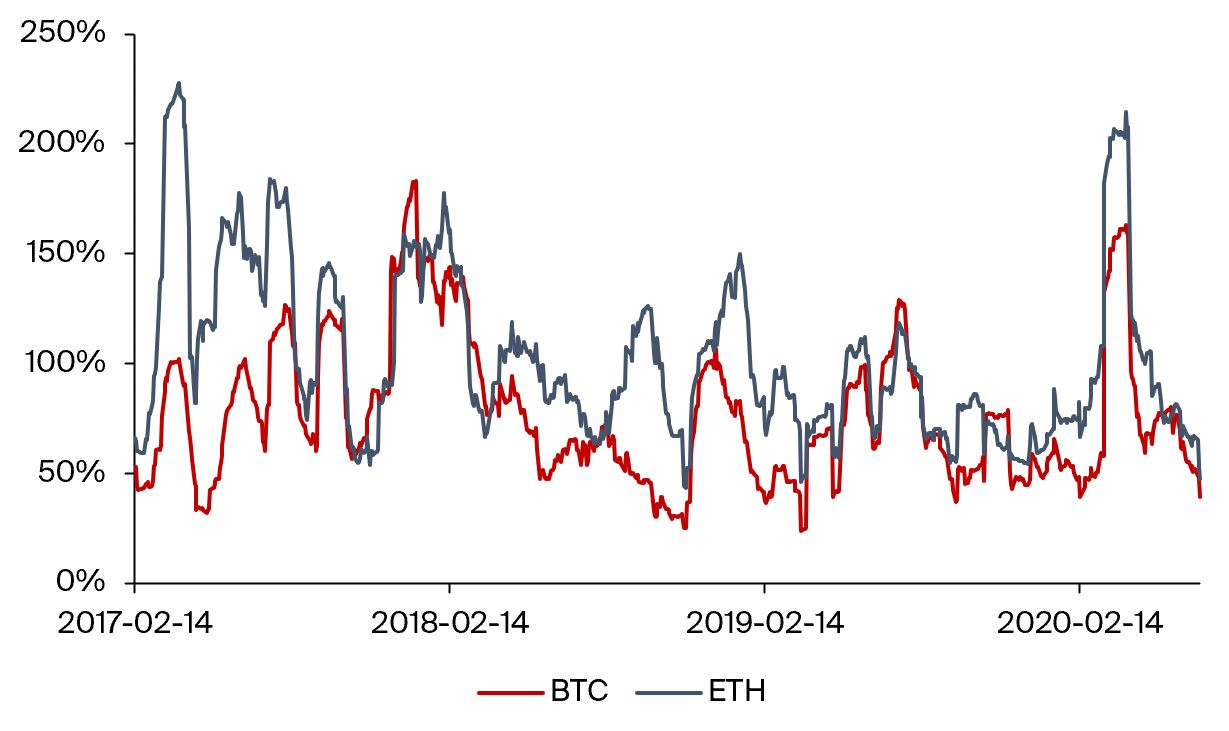

Periods of low volatility are preceded by periods of high volatility, and vice versa (by definition). Illustration 2 shows occurrences of similarly low volatility since 2017, for example in May 2017, October-November 2018, as well as April 2019. In each case, a large directional move (either bullish or bearish in nature) followed.

Illustration 2: Periods of low volatility have historically preceded strong moves, such as in November 2018 and April 2019. Current volatility level indicated by the black dashed line.

During times where Bitcoin price consolidates in a tight range, attention of traders often turns to altcoins. This is again highlighted during the current period, where much of the action is happening in the DeFi space and its related tokens.

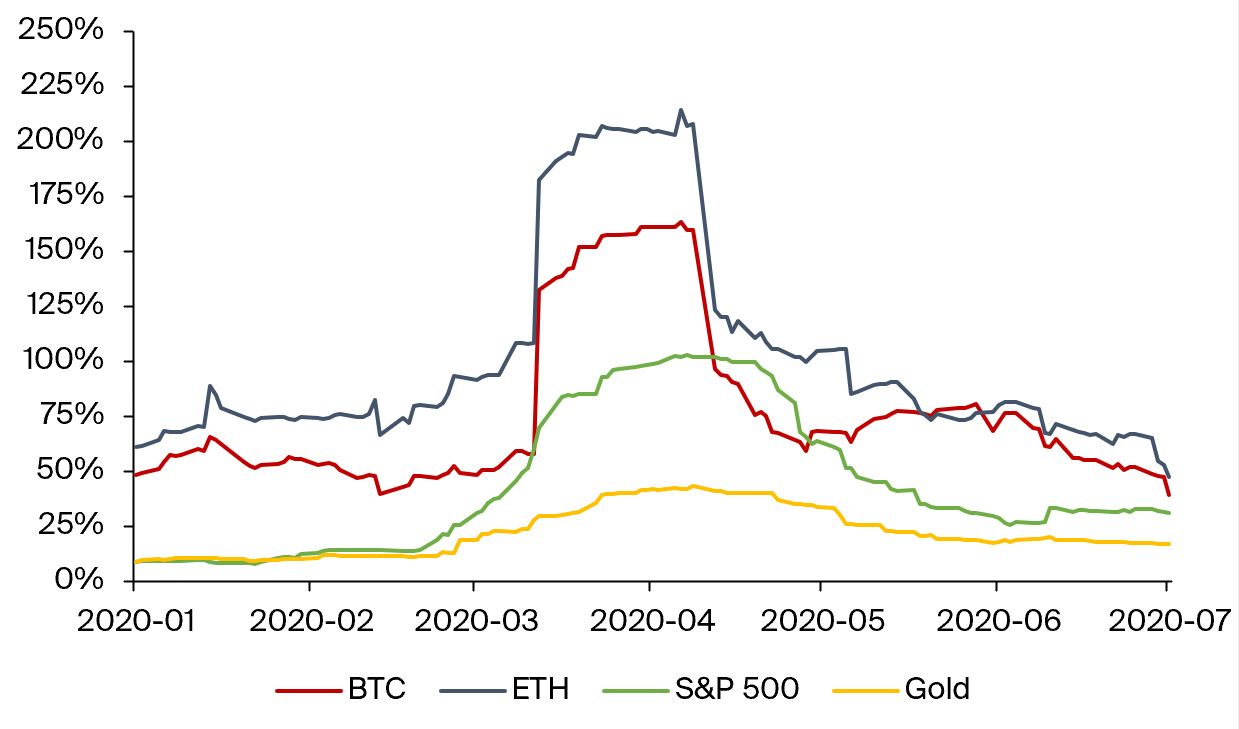

Zooming in on volatility for the period since the beginning of this year, the behavior of the two largest cryptocurrencies Bitcoin and Ether resembles that which can be seen in the stock markets, such as the S&P 500. At current levels, crypto markets are only slightly more volatile than equities. Gold, as the traditional safe haven asset, remained the least volatile throughout the year (currently standing at 16.7% annualized or daily moves of about 1%).

Illustration 3: The current 30-day volatility (annualized) of Bitcoin (39%) and Ether (47%) is close to readings on the S&P 500 (31%).

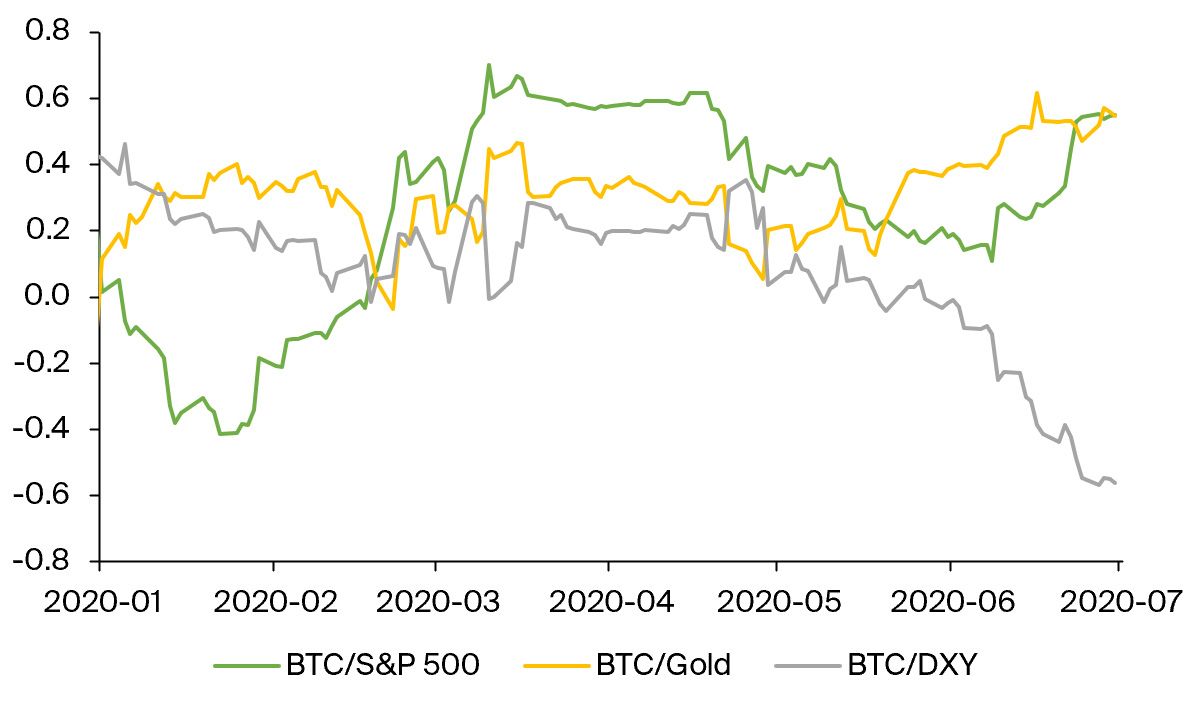

Short-term 30-day rolling correlations of daily returns between Bitcoin and both the S&P 500 and gold started increasing again after reaching record highs during the market wide sell-off in March. Perhaps even more interestingly, a negative correlation to the dollar index (DXY) started to emerge since May. The dollar index is a measure of the value of the U.S. dollar in comparison to other currencies, specifically against the euro (57.6% index basket weight), the Japanese yen (13.6%), the British pound sterling (11.9%), the Canadian dollar (9.1%), the Swedish krona (4.2%) and the Swiss franc (3.6%).

Illustration 4: The 30-day rolling correlation of daily returns of Bitcoin and the dollar index (DXY) has started to drift into negative territory since May.

A negative correlation means that when the dollar strengthens (DXY rises), Bitcoin drops in value and when the dollar weakens, Bitcoin increases in value as measured in USD. While this intuitively makes sense, historically Bitcoin and the dollar index have been largely uncorrelated. The emergence of a short-term correlation may indicate that recent market movements have been driven by dollar strength and weakness. This might also be an interesting metric to watch in the future, as central banks around the world still continue printing money in large amounts in an attempt to offset economic consequences of the coronavirus lockdowns and to stabilize the flow of credit within the economy through liquidity injections.

A Hedge Against Inflation? Bitcoin was created in the aftermath of the Great Financial Crisis of 2008, and its creator Satoshi Nakamoto envisioned it to act as an “insurance policy” against mismanagement of government-issued currencies. The first block ever mined references a headline in the Times: “Chancellor on Brink of Second Bailout for Banks”.

The recent economic crisis and associated fiscal and monetary policy measures bring up similar topics as in 2008 for example the risk of inflation and currency devaluations due to money printing presses going into overdrive. As such, an emotional moment for many Bitcoin advocates happened during this year’s block reward halving. An inscription in block no. 629’999, mined by F2Pool, read: “NYTimes 09/Apr/2020 With $2.3T Injection, Fed’s Plan Far Exceeds 2008 Rescue”.

But whether Bitcoin can truly serve as a hedge against inflation is still unproven. Most major developed economies experienced mild to no inflation over the past years. This is not the case, however, for some emerging economies and their currencies. For example, Turkey experienced an inflation of 15.2% in 2019, and Argentina even more at 53.6%.

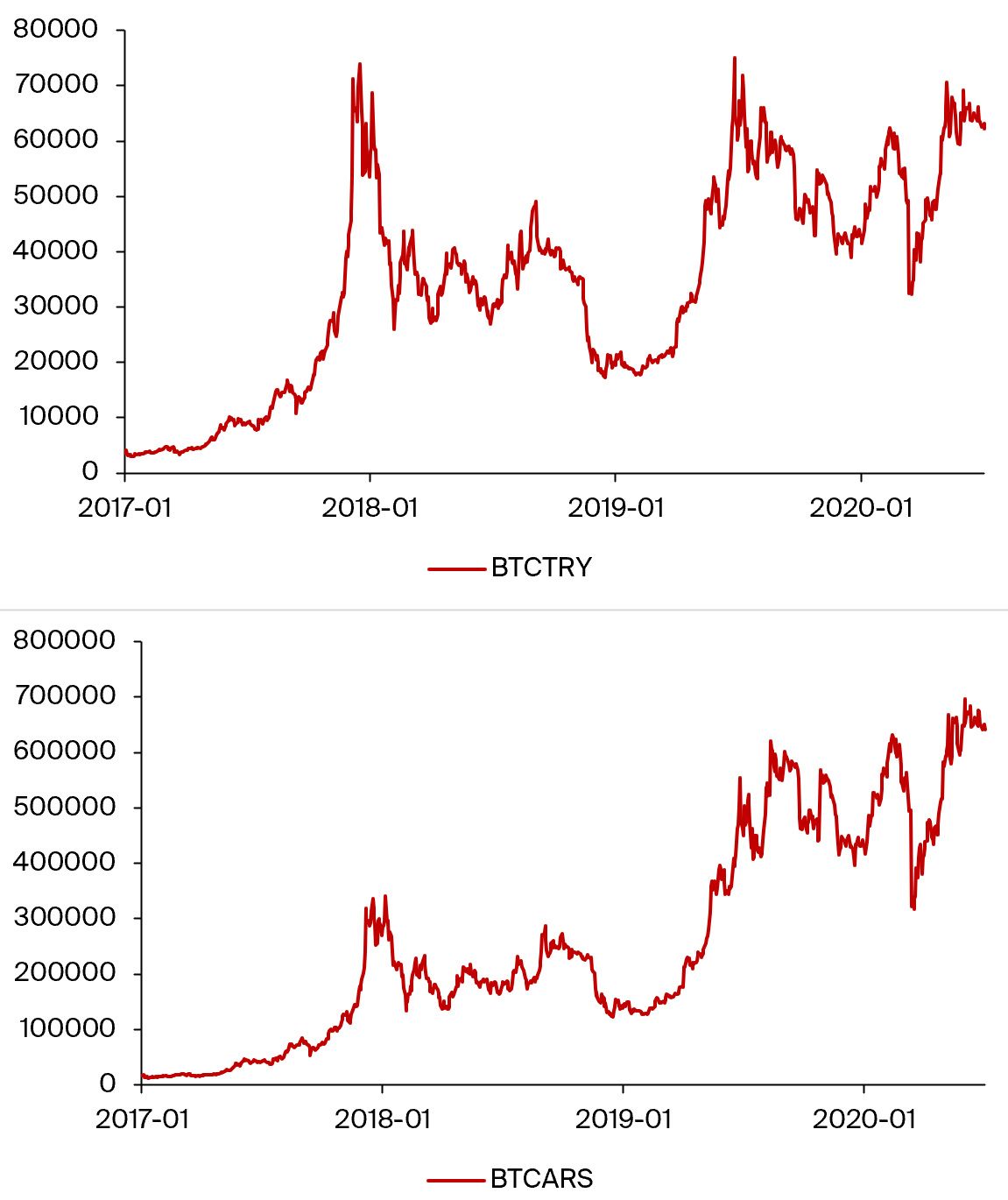

While usually, Bitcoin is charted against the USD or EUR, the occasional glance at other currencies can reveal vastly different patterns. As shown in Illustration 5, BTC valued in the Turkish Lira is close to its 2017 all-time high, and it has long breached the 2017 peaks when valued against the Argentine Peso.

Illustration 5: BTC valued in Turkish Lira (TRY) is close to its all-time high, while BTC versus the Argentine Peso (ARS) has surpassed its 2017 high by more than 2x.

Arguably, using the USD as a store of value in these countries would have offered similar benefits to protect against inflation. Ultimately, accessibility is a deciding factor for the choice of store of value in such cases. Capital controls often restrict the ability to obtain USD – therefore, it may be easier to purchase Bitcoin. Localbitcoins (a peer-to-peer trading platform) volumes in high-inflation countries soared at the end of last year. Once a buyer has entered the crypto markets, access to USD is often easier than through traditional capital markets. Demand for USD-denominated stablecoins has risen rapidly in this year, and the largest one, Tether, is closing in on a $10 billion market capitalization. This may contribute to a (covert) dollarization of such countries.

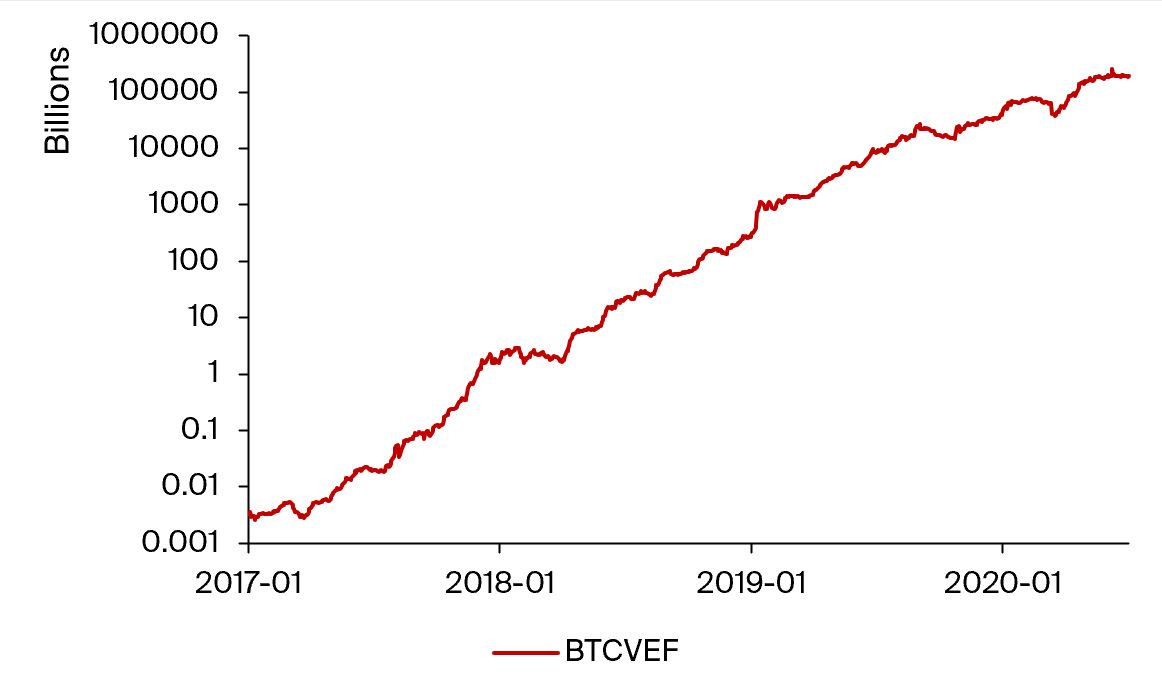

However, when push comes to shove, any potential store of value is better than a hyperinflationary currency. Bitcoin’s “volatility” is barely noticeable when quoted against the Venezuelan bolivar, and one BTC costs around 191’000’000’000’000 VEF (or 1’910’000’000 VES) at the time of writing, give or take a few thousand billion. Under such extreme circumstances, Bitcoin can indeed provide an excellent hedge against inflation.