Regulations and Innovations

Sep 15, 2020

15 September 2020

Regulatory Advances The regulatory landscape for crypto assets continues to become more well-defined. Recently, both the European Union as well as Switzerland have made progress towards establishing a legal framework for the issuance and handling of crypto assets.

Perhaps spurred by projects with potentially immediate and global reach, such as Libra, finance ministers of Germany, France, Italy, Spain and the Netherlands jointly stated that stablecoins should only be allowed to operate within the EU once regulatory frameworks have been established.

Meanwhile, a draft of the proposal by the European Commission has surfaced. The draft claims to aim at achieving four objectives:

- to provide legal clarity and certainty for the use of DLT in financial services;

- to support innovation and fair competition;

- to protect consumers and investors;

- to address financial stability and monetary policy risks.

The proposal outlines that regulation should be harmonized within all EU member states. More concretely, guidelines for the issuance of crypto assets are proposed. According to these guidelines, each issuer of crypto assets must publish a whitepaper (that describes, for example, the rights of token holders) – similar to traditional documentation requirements for financial products, such as key investor information documents or a prospectus. The practice of publishing whitepapers is already customary within the crypto sphere, even though the quality of whitepapers varies. Furthermore, and specifically for asset-backed tokens such as stablecoins or “e-money tokens”, issuers must register as a credit institution or an electronic money institution. Both new harmonized licenses and mandatory use of existing ones will enable what is currently lacking: Passporting from one EU member state to the whole market.

On the topic of stablecoins, one distinction is made: Algorithmic stablecoins that attempt to stabilize the price of the token by controlling supply and demand and without referencing a fiat currency are treated separately, but marketing them as “stable” would be prohibited under the proposal. It is unclear if an algorithmic “stablecoin” that references, for example, inflation metrics like CPI would fall under these regulations.

The proposal also exempts central banks from these regulations, simplifying the issuance of potential central bank digital currencies (CBDCs), which is an area that the ECB and other central banks have been actively exploring.

Swiss DLT Law Passed Last week, the Swiss Parliament has accepted – without opposition – adjustments to Swiss law that would incorporate and regulate the use of distributed ledger technology (DLT). The law was originally filed in November 2019 for discussion in parliament. Its aim is to embrace the opportunities presented by DLT and to improve legal certainty for businesses that incorporate the technology into their processes. It also addresses what happens with crypto assets in the case of bankruptcy. This act also incorporates current practices and interpretations into formal law. Amendments to both civil law and financial markets law will be made; these legally enable a new financial markets infrastructure using DLT-based trading systems, amongst other innovations.

Bitcoin and Schnorr Signatures Meanwhile, in the crypto space, Bitcoin core developers have gotten one step closer to integrating support for Schnorr signatures in Bitcoin by integrating the relevant Bitcoin Improvement Proposal (BIP-340) into the secp256k1 library. The proposal was originally written in 2018.

Schnorr signatures are potentially superior to elliptic curve signatures (ECDSA, the current signature algorithm of Bitcoin). They allow multi-signature transactions to be indistinguishable in terms of signature size from “normal”, single-signature transactions, which enhances Bitcoin’s pseudonymity features. Theoretically, they would also help to improve the scalability of Bitcoin, since the signature size from transactions with multiple unspent transaction outputs (UTXOs) as inputs could be reduced.

Another feature is that transactions that open and close channels on the Lightning Network, a second layer scaling technology for Bitcoin, would look equal to and be just as expensive as regular transactions.

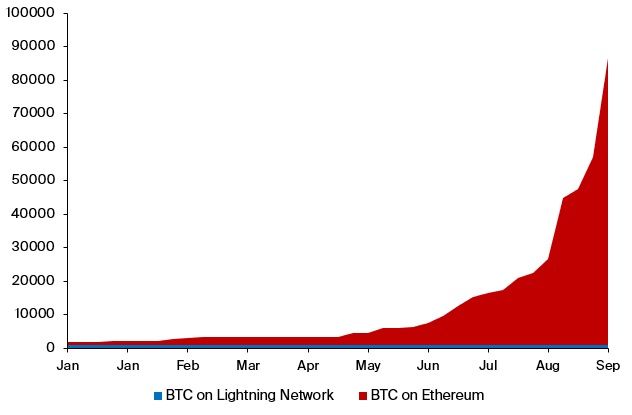

Bitcoin on Ethereum Grows The Lightning Network, however, still struggles to get significant traction. It appears that for now, Ethereum de facto acts as “Bitcoin’s Layer 2” – the amount of Bitcoin that is now present on Ethereum in tokenized form has exploded over the past months, alongside the general hype for decentralized finance (DeFi).

Illustration 1: Currently, close to 90’000 BTC (around $900M) are on Ethereum in tokenized form, whereas the Lightning Network has a capacity of around 1’100 BTC.

As seen in Illustration 1, the amount of Bitcoin tokenized on Ethereum far eclipses the amount that is locked in the Lightning Network. This is perhaps mostly attributable to the ability to collateralize Bitcoin and “yield farm” with it, achieving high yields on BTC that would otherwise sit idle in cold storage (albeit with a very different risk profile of the returns).

This synergistic interaction between the two largest blockchains (by market capitalization) enhances the value proposition of both chains – Bitcoin can now easily be collateralized using DeFi on Ethereum. If trustless bridges between the two chains (as pursued, for example, by the RenVM) can be established, the whole process becomes permission- and trustless. Especially the permissionless nature would be an advantage of the “digital gold” over normal gold. In the longer term, however, moving Bitcoin off its native chain might also cut into miner revenues coming from transaction fees if it happens in large amounts. This becomes increasingly relevant as the block subsidies are reduced through reward halvings.

ERC-721: Non-Fungible Tokens Besides the growth of the amount of BTC on Ethereum, another class of tokens is starting to complement the DeFi space: ERC-721 tokens, or non-fungible tokens (NFTs). These tokens are each unique and distinguishable from each other, as opposed to “regular” (ERC-20), fungible tokens.

Illustration 2: Transfer volumes of non-fungible tokens over the past 7 days in various sectors, such as domain names (Unstoppable Domains, Ethereum Name Service), digital collectibles (Sorare, CryptoKitties, Rarible), and insurance (yInsureNFT).

Since inception of the NFT markets, over $100M in value has been transferred. Much of this was during the CryptoKitties hype in 2017 and from the decentralized virtual world Decentraland. But other sectors, such as digital collectibles, have also been growing, as shown in Illustration 2.

Digital collectibles are ideally represented by ERC-721 tokens, since each item is unique. These collectibles can, for example, be digital-first art or digitized art, with provable ownership represented on the blockchain.

Another use case comes from the gaming industry, which has shown strong growth over the past decade. Games often offer purchasable in-game items, but true ownership of the item is not achieved since it lies with the issuing company. Transforming such items into NFTs could change that. One blockchain-native example is the trading card game Gods Unchained, where each card is represented by a token.

Beyond these two applications, NFTs also open up the door to integrating more financial products in the DeFi space. One example is insurance – as, for example, yinsure.finance insurance covers that can be traded on the secondary markets. The NFT specifies the insured amount as well as the duration of the cover. While the initial cost of the insurance is set by the NFT issuer (the underwriter, in this case, is Nexus Mutual, a decentralized insurance protocol), the NFT representing the insurance contract can afterwards be freely traded on a secondary market (such as Rarible, in this case).

This allows the market to continuously assign a fair rate for the insurance contract. The major use case for insurance, currently, is within the crypto space – DeFi users take out insurance on the protocols they use (such as Compound, Aave or Balancer). In this case, a new audit of such a protocol by a reputable auditor would likely impact the fair market price of such an insurance cover.

It is also conceivable that NFT markets can be extended to other products with fixed, unique terms – perhaps with a more direct link to the real world, such as mortgages.

Conclusion

Over the past weeks, regulatory uncertainty for the crypto space has been reduced. It remains to be seen if the newly developed regulations achieve their goals of providing a proper legal framework without stifling innovation.

For now, innovation in crypto continues at a rapid pace, and specifically in DeFi. Big opportunities have already been seized, and more may lie ahead in the form of non-fungible tokens. However, the exponential growth that is currently seen is a result of the building blocks that were developed not over the past two months, but through the entirety of 2018 and 2019.