Distribution of Stores of Value

Oct 30, 2019

In the early days of Bitcoin, obtaining the cryptocurrency was relatively easy with sufficient technical knowledge. The mining difficulty was low enough that mining on standard home computers was possible, and the block reward was sitting at 50 BTC per block (compared to today’s 12.5 BTC/block). There was even a website called “The Bitcoin Faucet”, developed by Gavin Andresen, from which Bitcoin users could obtain 5 BTC per day – completely for free.

Hence, it would make sense that early investors or supporters of Bitcoin control a large amount of its coin supply. However, coins change hands during the boom and bust cycles of Bitcoin. As such, the distribution of the coin supply changes, and Bitcoin’s public ledger makes it possible to get an idea of the distribution shifts that take place. The conclusions drawn from such observations have to be taken with a grain of salt, however – addresses may contain pooled funds (such as cold storage wallets of exchanges), or one person may control multiple addresses. In fact, re-using Bitcoin addresses is discouraged for privacy and security reasons.

Nevertheless, some trends can be observed when examining blockchain data of Bitcoin addresses over time. To establish a reasonable measure of overall addresses in use, the number of addresses containing at least 0.01 BTC was collected.

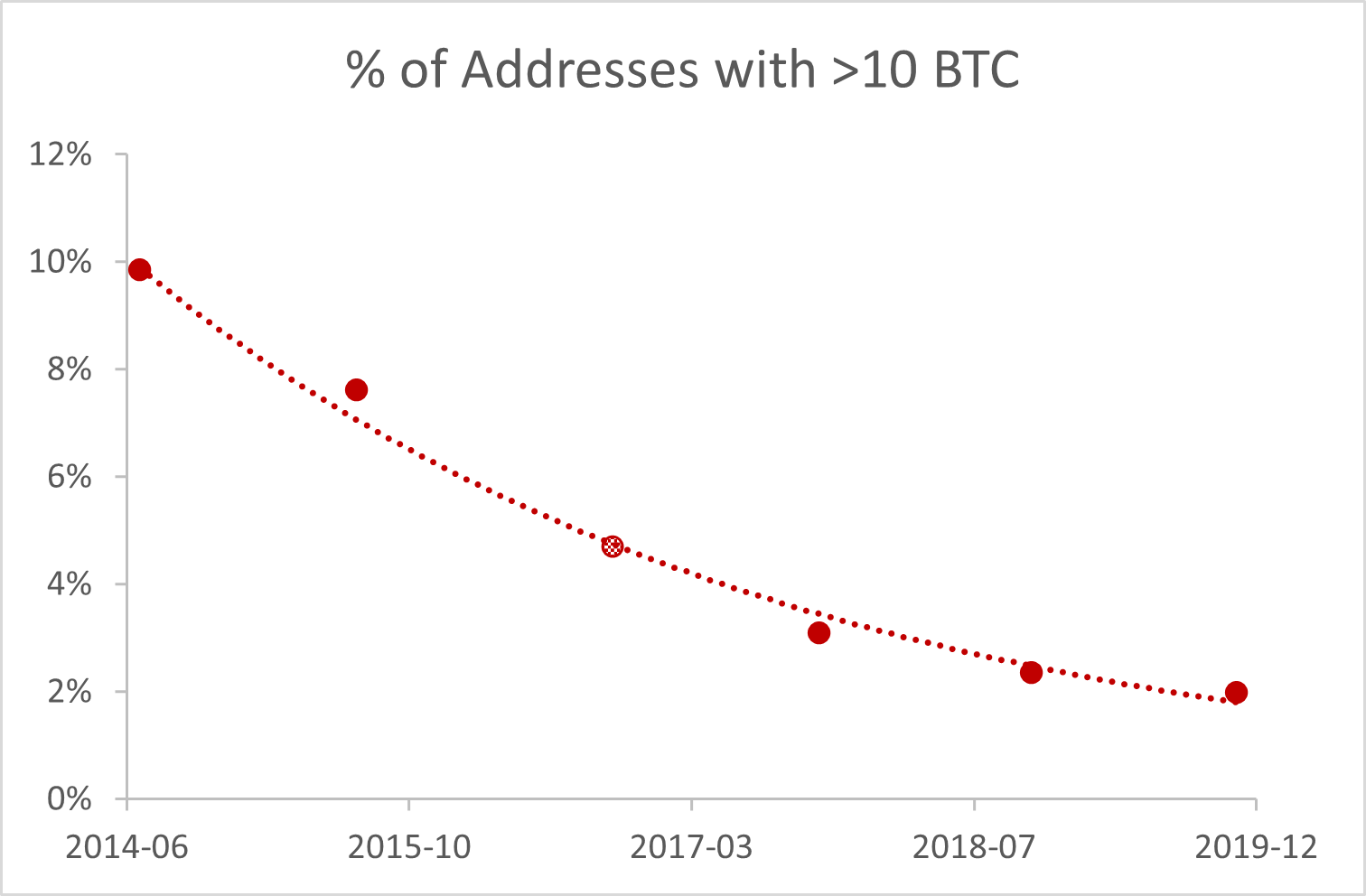

These numbers will be used as an approximation of the number of real Bitcoin addresses. Of these currently about 7.7 million addresses, only about 2% contain more than 10 BTC.

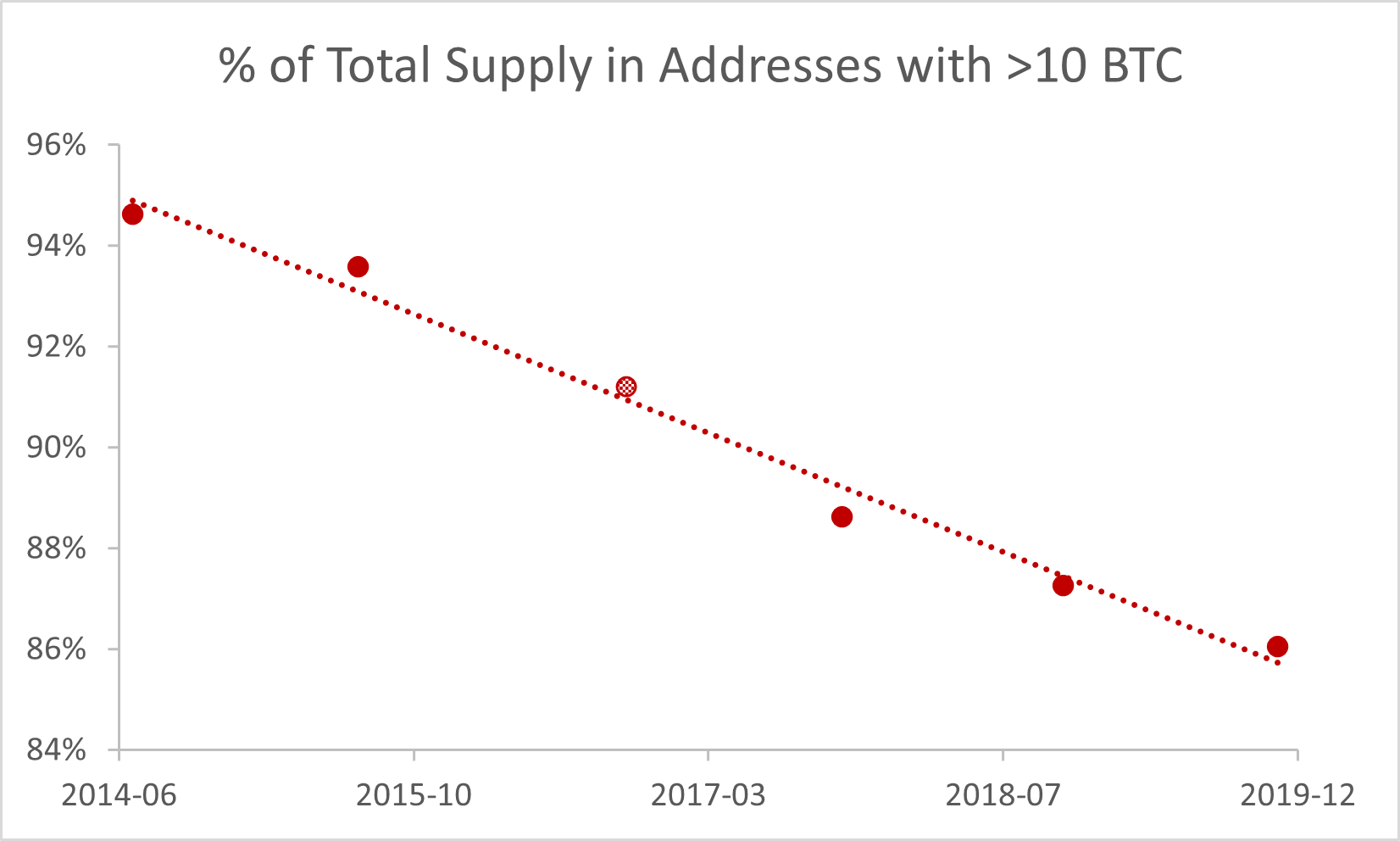

Looking more closely at the percentage of total supply that these addresses hold reveals that the amount of Bitcoin held in large chunks above 10 BTC has also decreased. In July 2014, almost 95% of coins were associated with addresses containing more than 10 BTC. Today, this amount has decreased to about 86%.

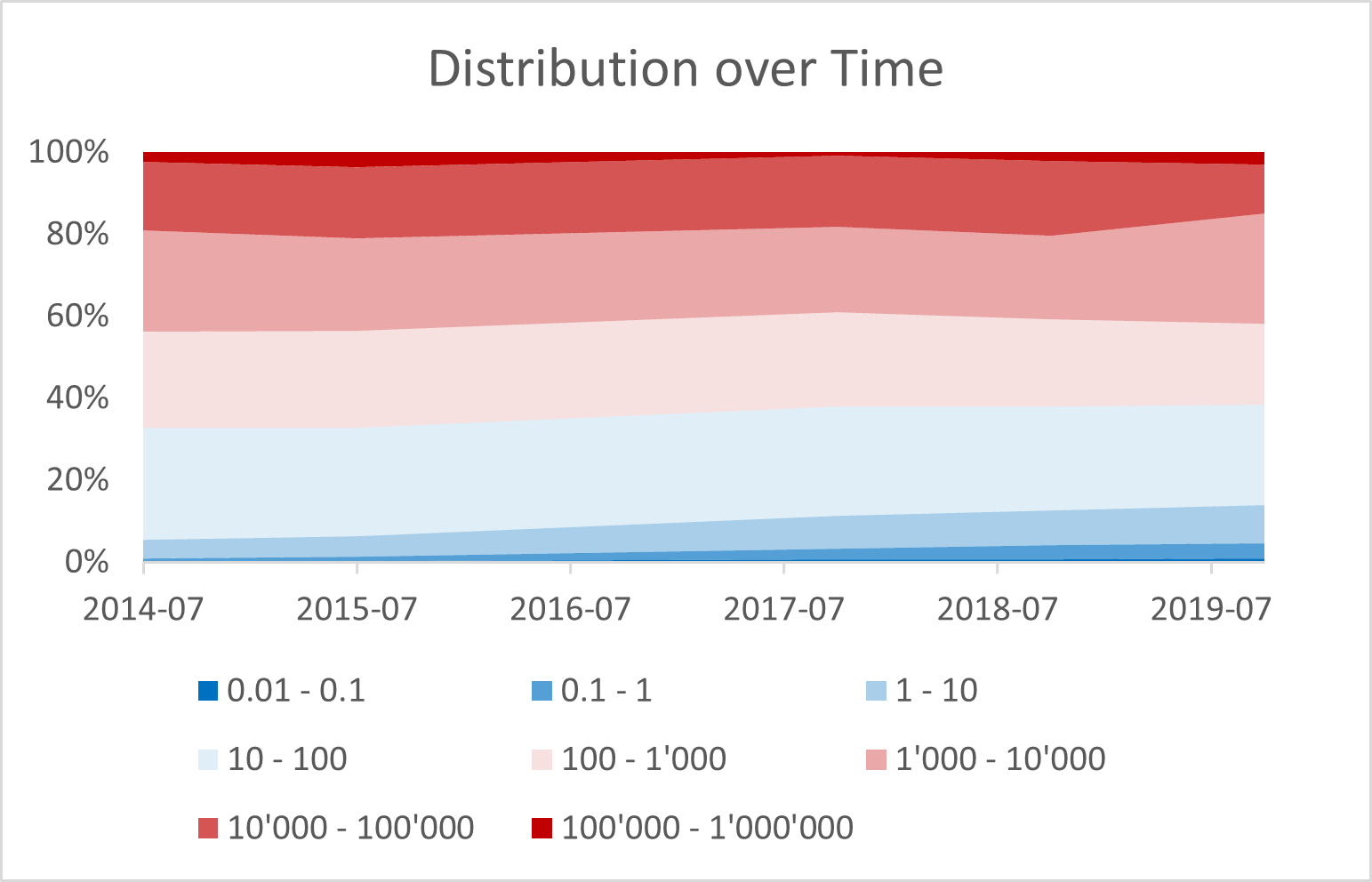

The overall picture of Bitcoin’s Unspent Transaction Output (UTXO) set is shown in Illustration 4. While the distribution over time has remained relatively similar, two observations can be made. First, the number of addresses containing relatively small amounts of Bitcoin (less than 10) has been constantly increasing. Secondly, the amount of addresses containing more than 10’000 BTC has recently been decreasing, flowing to smaller addresses.

What conclusions can be drawn from these observations? While Bitcoin’s distribution still appears to be relatively concentrated among big holders, a slight shift over time towards storing smaller amounts per address can be observed. This may be indicative of a slow distribution from early investors who are taking profit to new investors and users that are getting involved in the cryptocurrency space. Overall though, the distribution still has not changed too much. One contributing factor might be lost coins – i.e. coins that are no longer accessible because the original owner has lost the corresponding private key. More than 3.8M coins have not moved for more than 5 years – at least part of them are most likely lost forever.

How Does Gold’s Distribution Compare to This?

Wealth inequality has become an important topic the last few years. A recent paper by economists at the Netherlands Central Bank called, “Central bank policies and income and wealth inequality: A survey,” found that inflation of the money supply increases wealth inequality because distribution of newly printed money is not uniform.

However, Bitcoin was not designed after the fiat monetary system. Instead, Bitcoin’s current design resembles that of gold, and gold’s distribution of ownership is meritocratic and more evenly distributed than fiat ownership. Two main factors contribute to gold’s ownership being decentralized. First, the largest deposits and mining companies are not concentrated geographically. Instead, they can be found all over the world, including Indonesia, America, Uzbekistan, Russia, Papau New Guinea, Dominican Republic, and Congo. Second, the long-historical track of gold has led to a more equal or bell-shaped distribution because gold miners must sell a certain amount of gold to the market every month in order to cover overhead costs. As the price of gold increases, gold investors also have a financial incentive to sell gold to the market in order to realize gains and rebalance their portfolio. These two relatively constant supplies of gold to the market enable newcomers to join the network, leading to a lower level of wealth inequality.

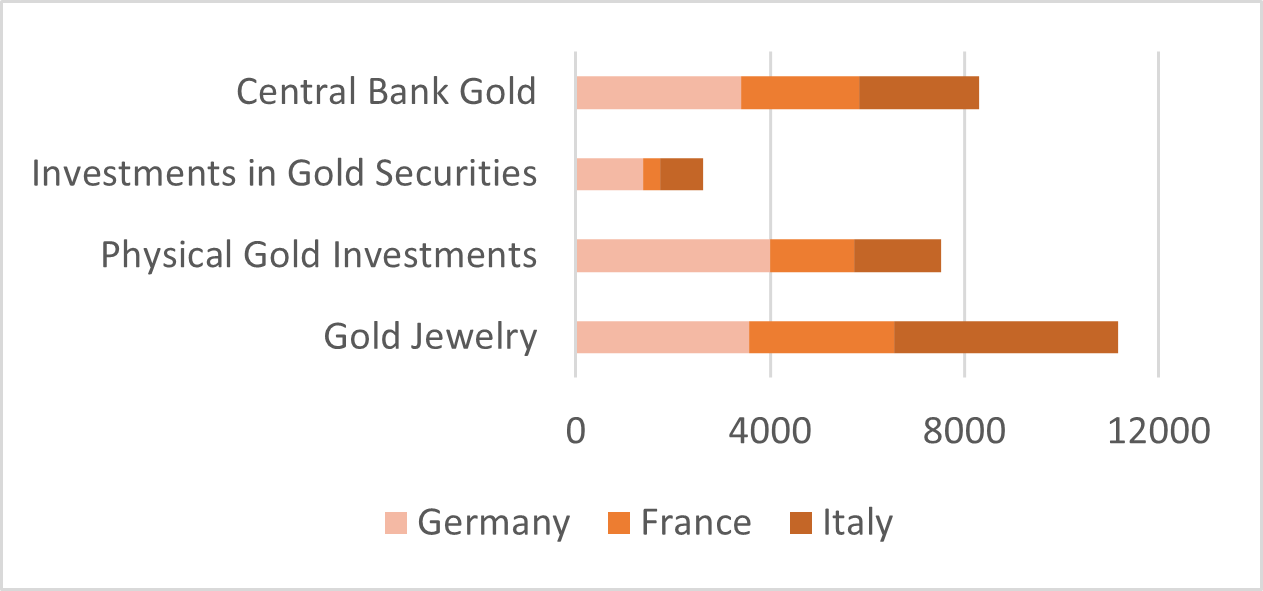

The world’s ownership distribution of gold is approximately 50 % in jewelry, 14 % industry, 18 % central banks, and 17 % private investment in physical gold. In 2010, the Steinbeis University in Berlin [studied ](http://www.steinbeis-research.de/images/pdf-documents/KLEINE Financial Study - Gold Ownership by Private Individuals in Germany.pdf)the ownership distribution of gold in Germany and found that the country holds approximately 8 % or 12,000 tons of gold out of the 163,000 tons globally available. The study further broke down the distribution of gold into private households and government. Of the

8 %, German households hold 6 % and the Bundesbank 2 %. In Germany, one in every four people hold physical gold as an investment.

A survey of 3,248 gold owners in Germany found that private investors with less than €25,000 in wealth own on average 15 grams of physical gold. Individuals with €150,000 in wealth own on average 277 grams. This shows that people in Germany hold more of their wealth in gold as they become wealthier.

Unlike in Germany, in Italy and France the central banks hold more gold than private households. Central bank gold holdings per capita clearly puts Switzerland in the lead with 128 grams of central bank gold per person. Germany comes in at 42, France at 38, and Italy at 40. Although the Swiss National Bank’s 1,040 tons of gold holdings are reported, estimates of the total amount of gold held privately in Switzerland are unavailable.

The wealth inequality in Bitcoin has decreased over the past decade and is expected to continue to decrease. Although, the current ownership distribution of cryptocurrencies appears to follow a power-law distribution with few accounts holding most of the cryptocurrencies, the distribution may approach a bell curve distribution similar to gold’s, because Bitcoin miners must also sell a portion of their proceeds in order to pay monthly costs, such as electricity. Also similar to gold, Bitcoin investors sell small portions of their holdings as the price increases in order to rebalance their portfolios. The economics of validators in proof of stake are different, because stakers do not have a strong incentive to sell a certain portion of their coins every month in order to pay for the costs of staking. Instead, they hoard coins to maintain or increase their staking power in the network. With limited supply of new coins to the market, this may put upwards pressure on the price, but slows down the coin distribution to new networks joiners. Overall, the ownership distribution of fiat is expected to become increasingly centralized and concentrated, while Bitcoin’s ownership distribution is expected to follow gold’s.