The State of the Altcoin Market

Dec 3, 2019

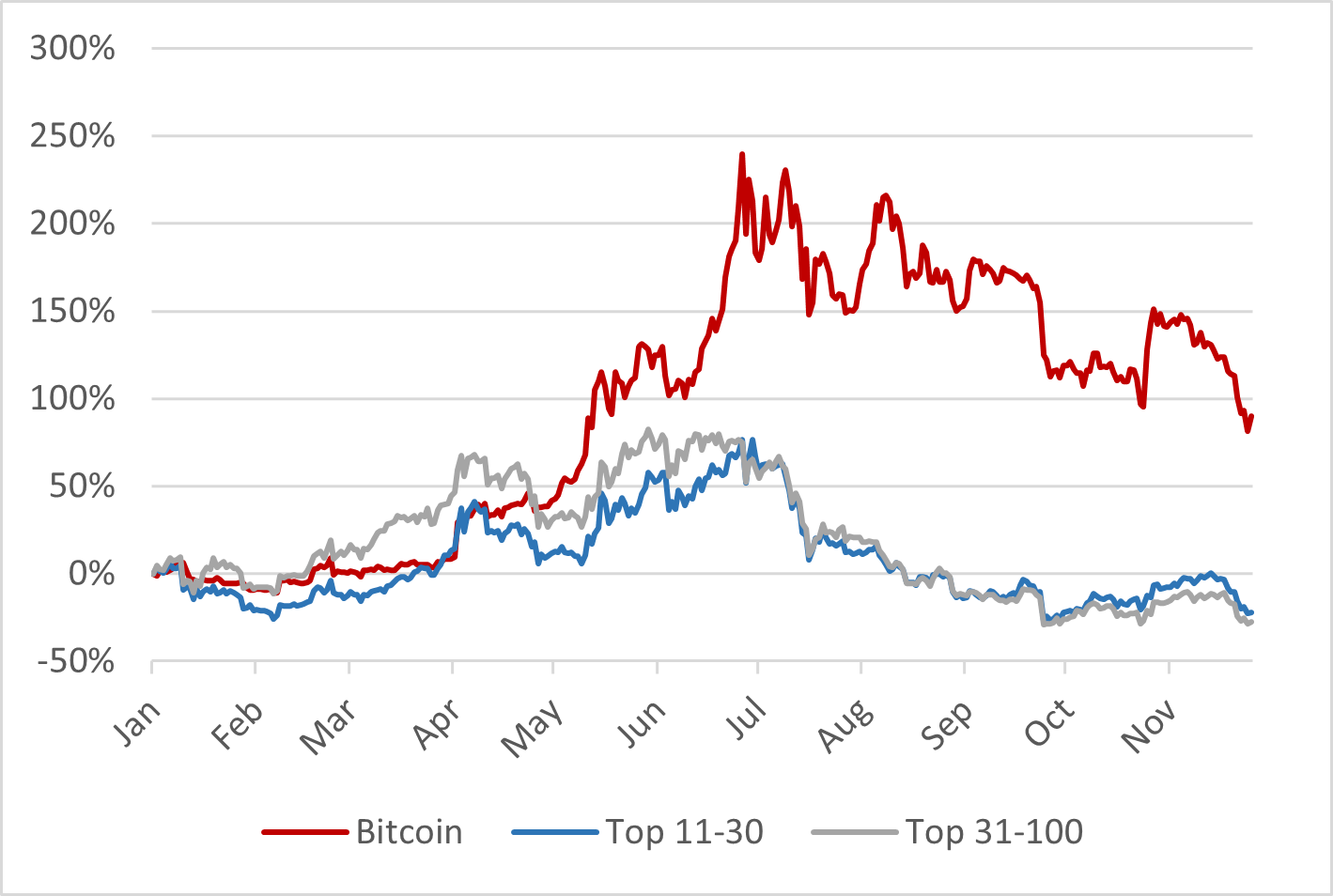

Bitcoin has performed well this year: On January 1, it traded around $3.8k. Through 2019, the price rallied to almost $14k and ended up at around $7.5k in late November – providing investors with a return of more than 90 %. For comparison: The S&P 500, which has been running hot this year, is up by about 25 % – strongly underperforming Bitcoin.

However, the picture is not so rosy for altcoins outside the top 10 by market capitalization: Mid- and small caps posted average returns of about -22 % and -27 %, respectively. As a result, the Bitcoin dominance has scratched 70 % in September – levels not seen since early 2017.

Several reasons might play into this underperformance. First, Bitcoin presents investors with the most liquid markets and is accessible through a variety of products – in addition to a liquid spot market, investable products include cash-settled and physical delivery futures as well as options, which are mostly unavailable for altcoins. Thus, it is the easiest market to enter with considerable capital. Additionally, Bitcoin still benefits from its first mover advantage – investors dipping their toes into the cryptocurrency markets will often choose Bitcoin due to its long history and battle-tested network security. The growing size of the derivatives markets, which offer leverage, also indicates that speculation might have been shifting away from altcoins and towards predicting Bitcoin’s next volatile moves.

From a more fundamental perspective, the token economic models of many altcoins also still have to prove themselves. Often enough, tokens in Initial Coin Offerings (ICOs) were issued with the primary goal of fundraising and establishing an initial userbase, and how the network value would affect the value of the tokens was an afterthought. As such, various utility tokens end up having a high velocity, meaning they only need to be held for short amounts of time. This is detrimental to the token’s price over the long run (as per the medium of exchange equation) without any counteracting token sinks such as burning mechanisms. On top of that, promises made by projects that raised funds through ICOs also take longer to materialize than expected, which may have driven out investors.

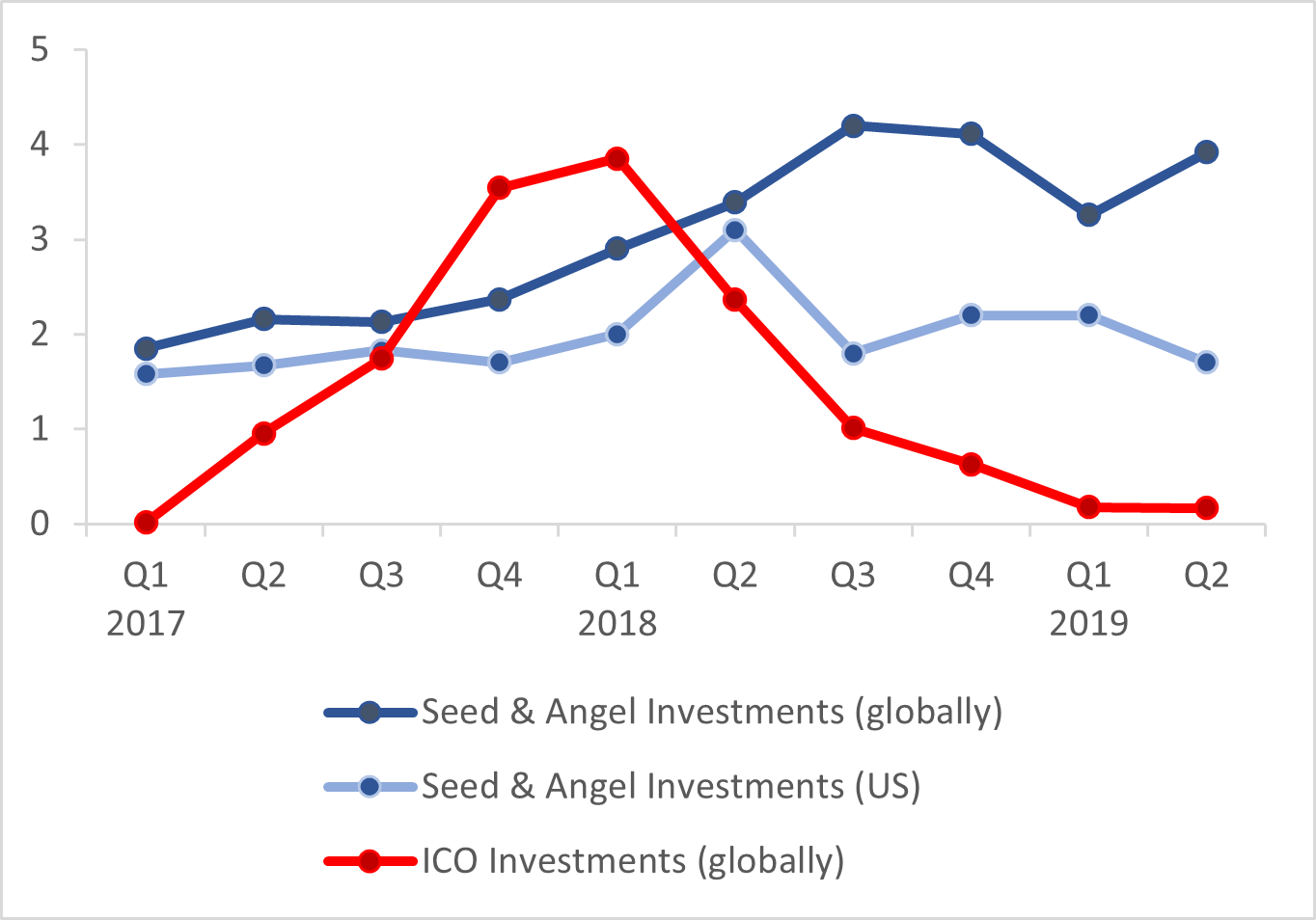

Nevertheless, open crowdfunding in the earliest stages of a project through ICOs was arguably the first use-case of cryptocurrencies that truly was a mass phenomenon and a major factor in the 2017 bull run. The total investments made in late 2017 even exceeded those made through traditional venture capital seed and angel investments.

The hype has since died down, with increasing regulatory scrutiny and downwards pressure on cryptocurrency markets in 2018 as major contributing factors. It is hard to estimate whether such a heated phase for ICOs as in 2017 will return – however, decentralized fundraising as a use-case for cryptocurrencies is most likely here to stay, be it in the form of ICOs, Initial Exchange Offerings (IEOs) or Security Token Offerings (STOs).

Overall, despite the sluggish performance of altcoins this year, coins and tokens of projects that have solid economic models and manage to drive adoption of their cryptocurrency might emerge as long-term winners – and provide outsized returns to investors that correctly spot them through fundamental research.

The Impact of ICOs on the Markets

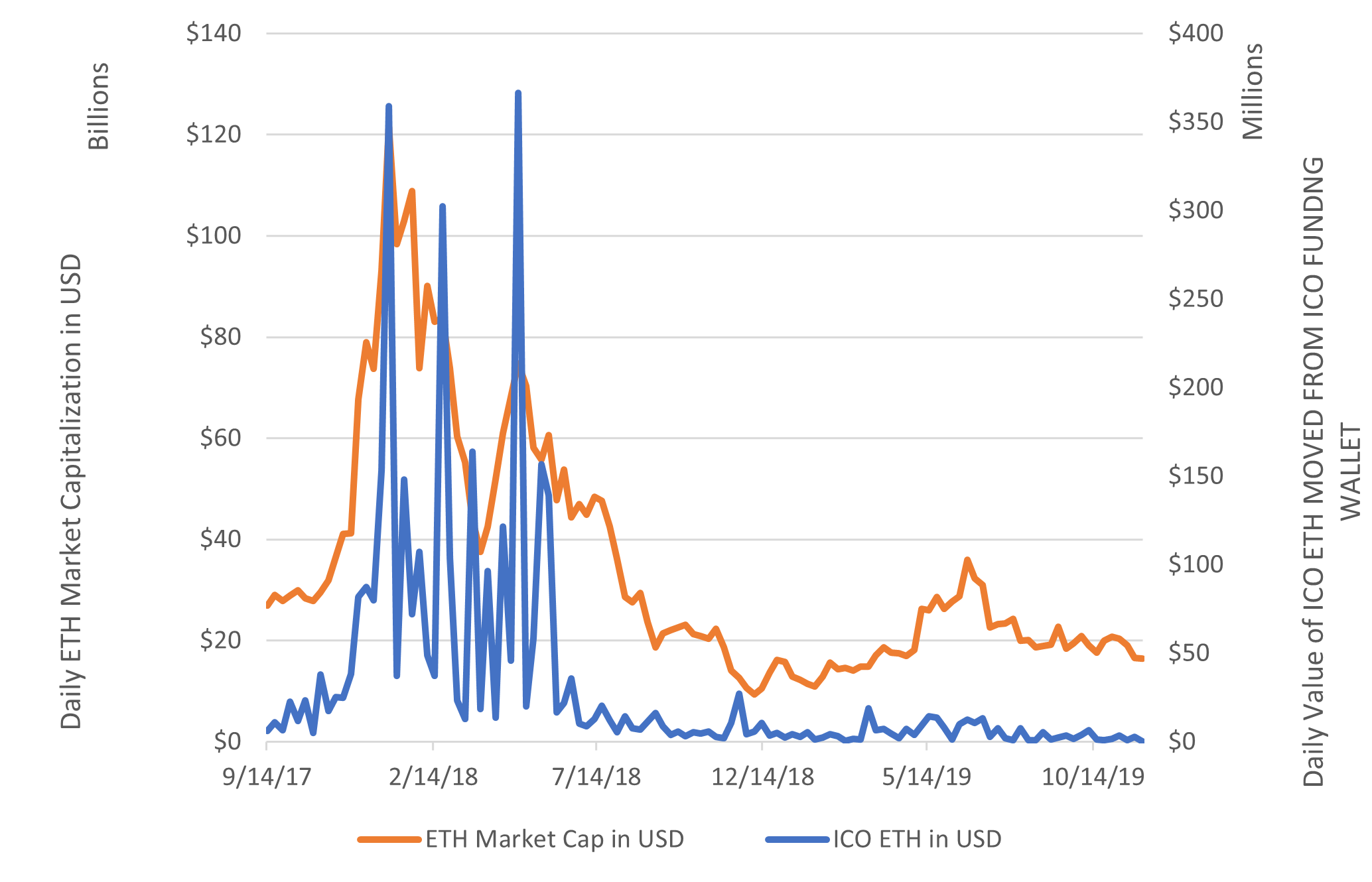

Some analysts argue that ICOs are the cause of the bear market in ETH. Development teams that raised ETH during ICOs between 2017-2018 have slowly been selling it to the market. The increased supply arguably outpaces demand leading to a downward pressure on the price. The data does support this argument to some degree. The value of ETH in USD moved out of ICO wallets has a high and positive correlation coefficient of 0.68 with Ethereum’s market capitalization in USD.

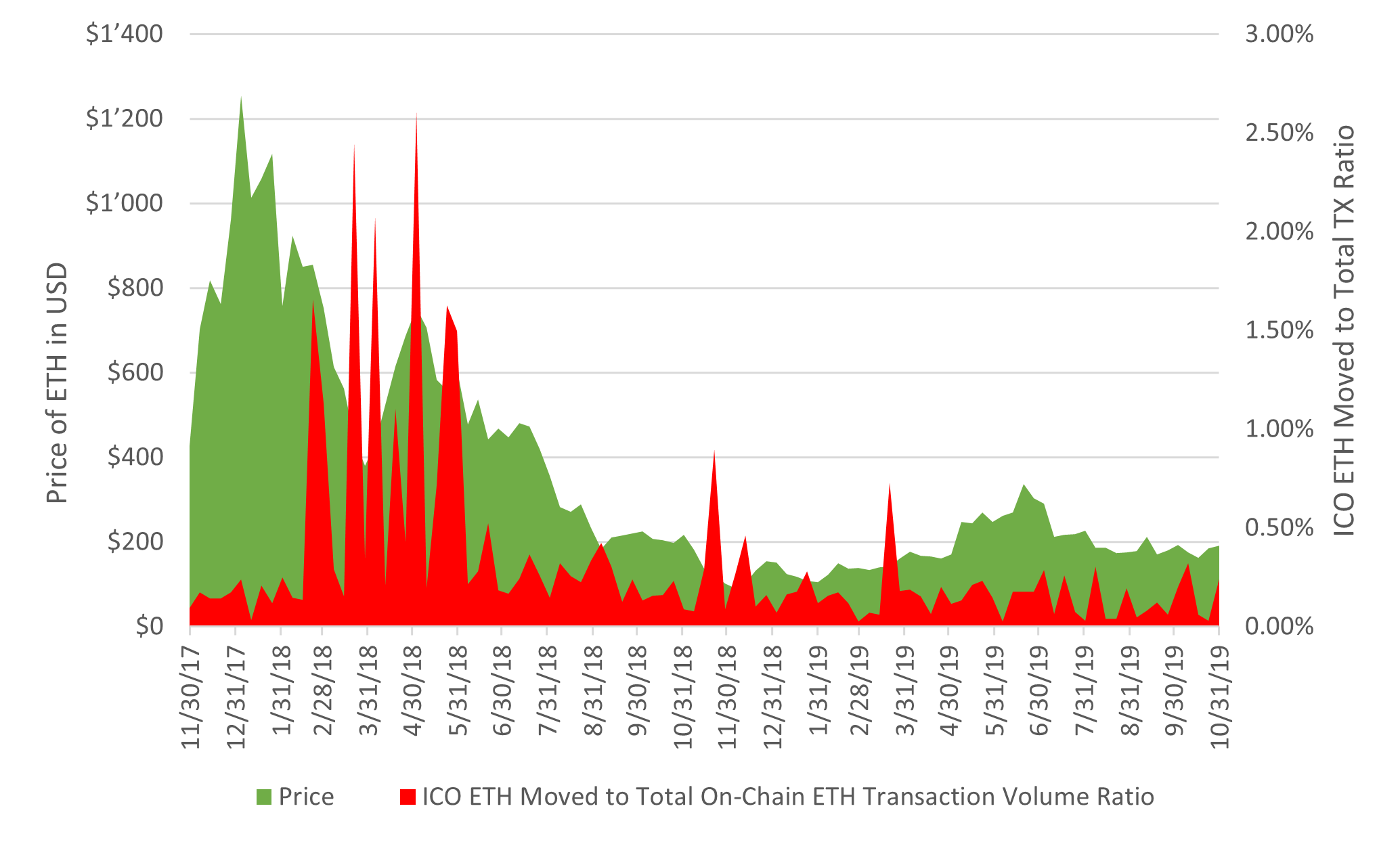

However, the strong visual relationship breaks down when analyzing the ratio of the amount of ETH moved out of wallets controlled by ICO companies compared to the total amount of on-chain Ethereum activity. As Illustration 4 shows, the 2018 sell-off of ETH collected by ICO teams did not begin until after Ethereum’s price started to decline. The amount of ETH moved from wallets controlled by ICO development teams averaged 63’754 per day between November 30, 2017 and October 31, 2019, which was on average 0.32% of Ethereum’s on-chain transaction volume. Similar numbers are present when comparing the USD volume of ETH moved out of ICO funding wallets to USD volume of ETH trading on exchanges. This provides evidence that the performance of ETH cannot be completely explained by ICO companies selling it.

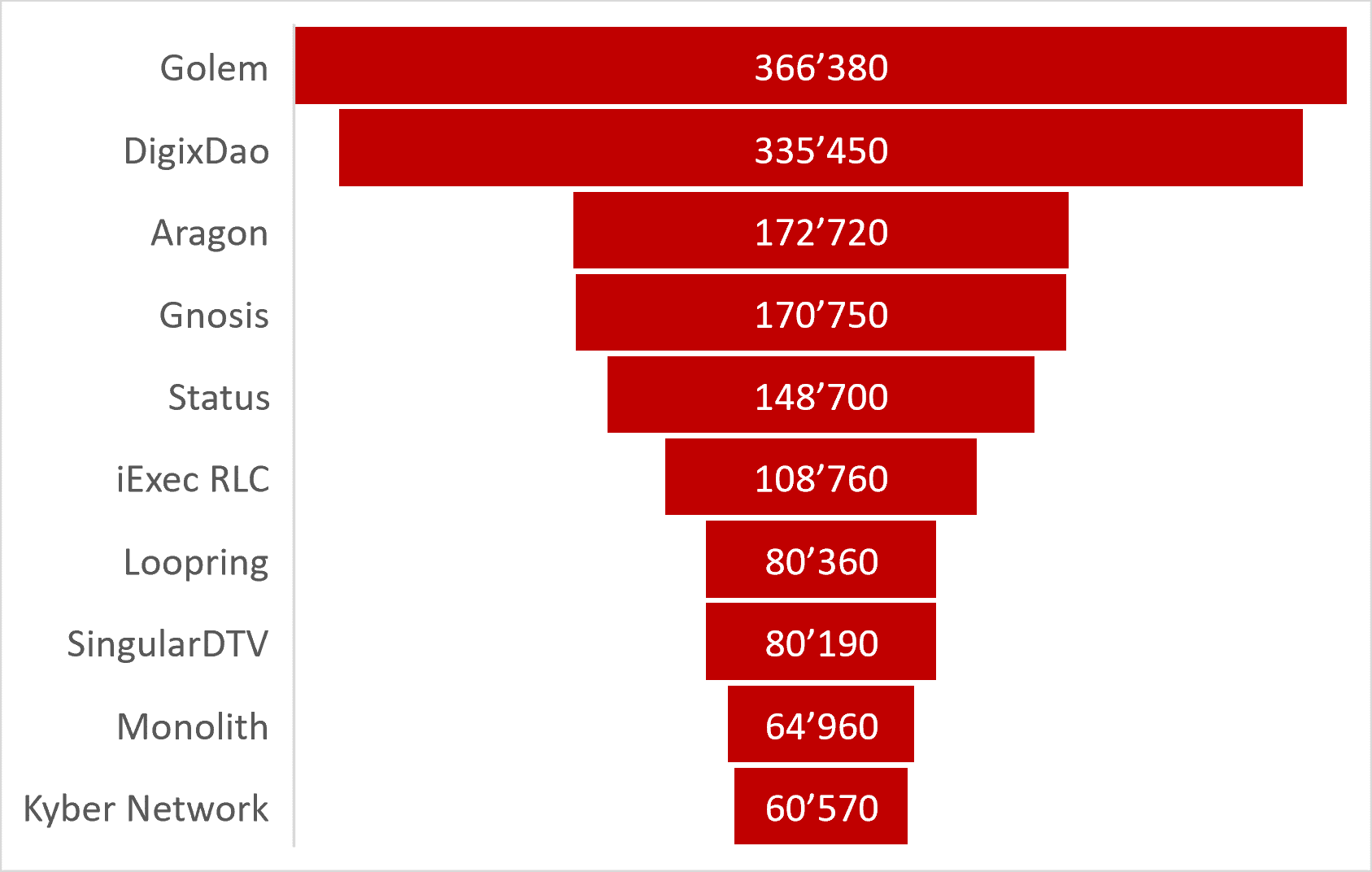

Even if ICO teams selling ETH does not explain its decline, the ICO craze did heavily contribute to ETH volatility. First, investors pushed up the price of ETH by demanding ETH needed in order to invest in ICOs. Then ICO teams are still gradually selling their ETH to the market. The top 10 ICOs that hold the highest amount of ETH from their original fund raise still control over $230 million worth of ETH. Overall, this trend is not likely to continue with IEOs and STOs because IEOs and STOs give investors the ability to invest with other currencies instead of only ETH.