Transaction Fees – Markets for Block Space

Oct 30, 2019

Nowadays, every transaction on most public blockchains contains a fee for miners to include it in a block. The fee is a bid by network users on block space, paid in the native currency of the network – the higher the bid, the more likely it is that miners will quickly include the transaction in a block to reap the fee. This was not always the case: In the early days of Bitcoin, it was possible to broadcast zero fee transactions that were still included in blocks.

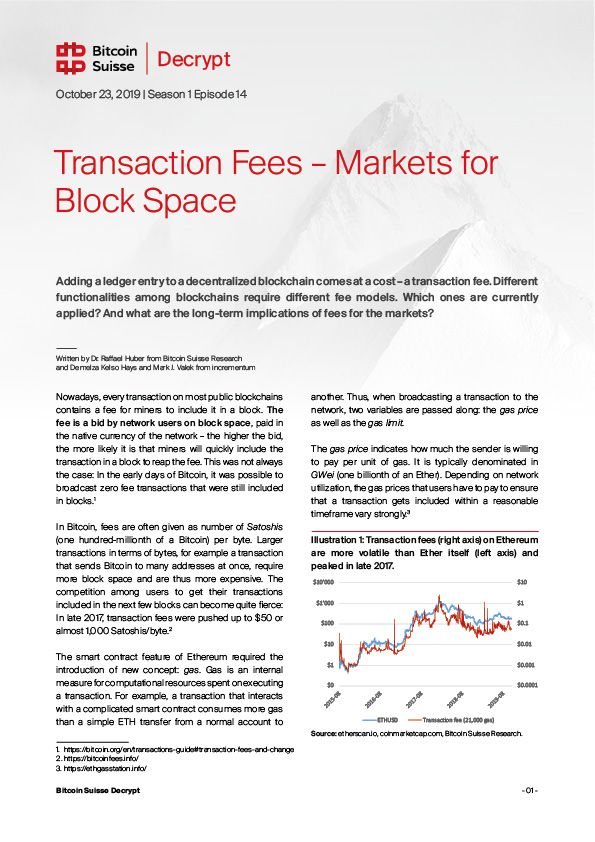

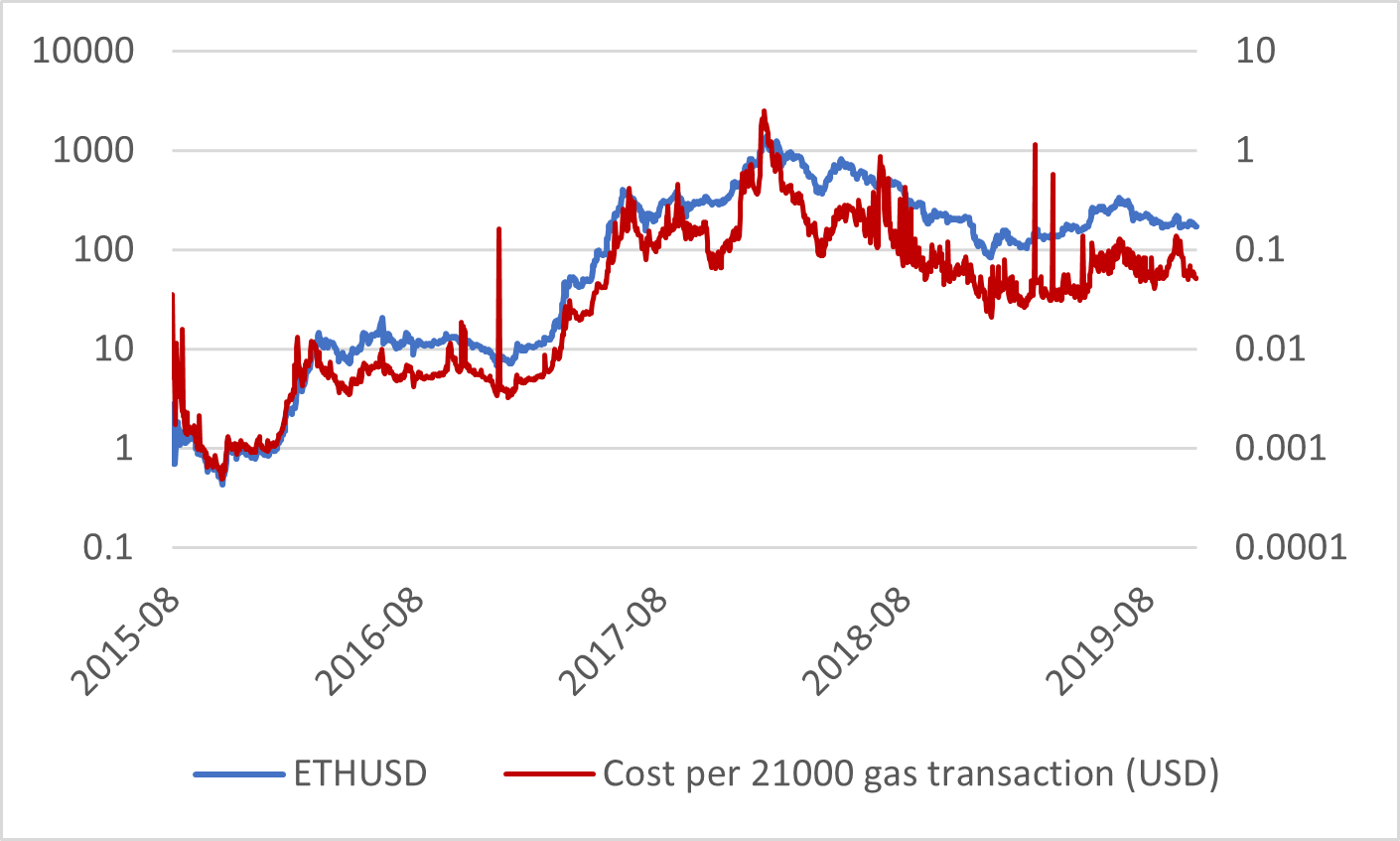

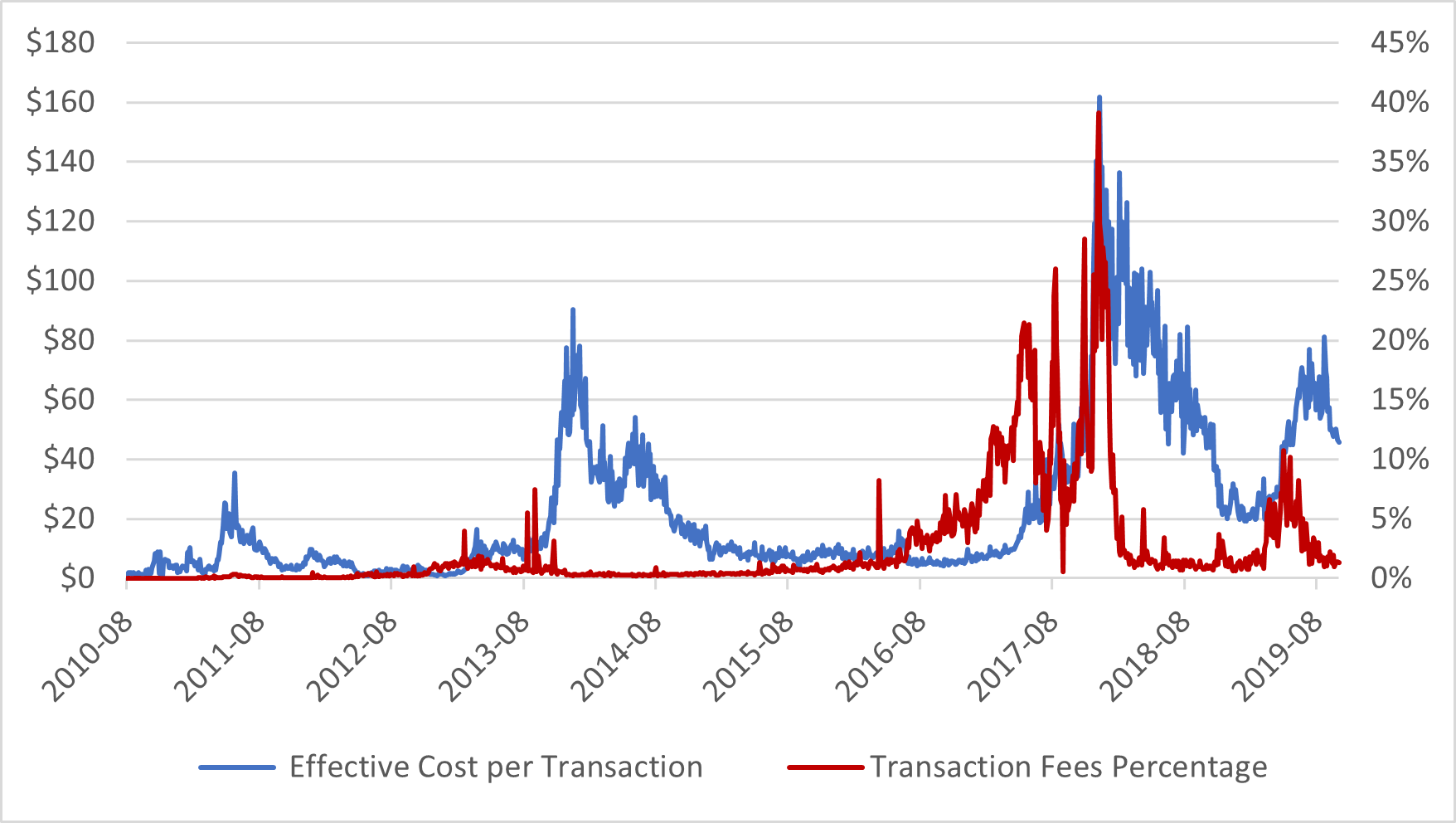

In Bitcoin, fees are often given as number of Satoshis (one hundred-millionth of a Bitcoin) per byte. Larger transactions in terms of bytes, for example a transaction that sends Bitcoin to many addresses at once, require more block space and are thus more expensive. The competition among users to get their transactions included in the next few blocks can become quite fierce: In late 2017, transaction fees were pushed up to $50 or almost 1,000 Satoshi/byte.

The smart contract feature of Ethereum required the introduction of new concept: gas. Gas is an internal measure for computational resources spent on executing a transaction. For example, a transaction that interacts with a complicated smart contract consumes more gas than a simple ETH transfer from a normal account to another. Thus, when broadcasting a transaction to the network, two variables are passed along: the gas price as well as the gas limit.

The gas price indicates how much the sender is willing to pay per unit of gas. It is typically denominated in GWei (one billionth of an Ether). Depending on network utilization, the gas prices that users have to pay to ensure that a transaction gets included within a reasonable timeframe vary strongly.

The gas limit defines how much computational effort the user is willing to pay for. There is an underlying reason why a gas limit is necessary: Without it, a smart contract could be programmed to run forever (e.g. by including an infinite loop). This would not only crash the nodes executing the transaction that calls this smart contract, but also ensure that consensus about the state of the blockchain is never found. With a gas limit, the transaction will simply run out of gas and terminate the calculation.

Currently, the bidding on block space through transaction fees follows a first price auction model. This means that everyone simply submits their bids without knowing what others plan to pay – which typically leads to users overpaying (to the benefit of the miners). While most modern cryptocurrency wallets include algorithms to estimate transaction fees, this is still far from optimal from the point of view of user experience.

A more sophisticated transaction fee model has been proposed for Ethereum in EIP-1559. The protocol change would introduce a standard fee amount, which would then be adjusted up or down by a known amount based on network congestion. This standard fee would be burned instead of going to the miners – leading to a reduction of ETH supply based on transaction volume. The miners would only receive a tip from the sender instead of the whole transaction fee. Since the fee adjustments in the new model are predictable, this would enable wallet software to more reliably set fees. The details of the proposal are currently still under debate.

In the future, the discussion about fees might become less relevant in Ethereum. Since all fee markets are simply proxies for the value of block space, it can be expected that scalability solutions which increase the available throughput alleviate the upwards pressure on fees in growing networks.

The Long-Term Role of Transaction Fees in Bitcoin

To pay for network security, Bitcoin currently hands out 1,800 BTC per day on average to miners as block rewards. At a price of $8,200, this equals an annual budget of around $5.4 billion for security. At the moment, transaction fees only account for a small percentage of miner revenues – currently around 2%.

Bitcoin’s economic model has been designed from the start to include block reward halvings every 210,000 blocks (approximately every four years). With each “halvening” event, the security budget coming from block rewards drops by 50%. However, block reward halvings also strongly reduce the supply side of Bitcoin’s supply and demand equilibrium. In the past, this has led to significant price rallies – which meant that miner revenues did not drop in USD terms, but even increased, as evidenced by the hashrate chasing all-time high after all-time high.

“In a few decades when the reward gets too small, the transaction fee will become the main compensation for [mining] nodes.” – Satoshi Nakamoto

The issuance of Bitcoin through block rewards is an implicit way for Bitcoin holders to pay for operational costs of the network. In the future however, when block rewards converge towards zero, the cost for maintaining the network will have to be borne entirely by users of the network through transaction fees. These transaction fees will become Bitcoin’s security budget. Lowering it would lead to lower network security, since unprofitable miners would shut off their machines and hashrate would drop. Assuming that security stays at least at current levels, there are two possible scenarios: Either, we will see large transaction volume on Bitcoin with comparatively low fees; or transaction volume will be low with high transaction fees. Which approach is viable in the long run? How do scaling solutions impact this?

These questions are at the heart of the debate between Bitcoin, Bitcoin Cash and Bitcoin SV supporters. Bitcoin developers bet on the Lightning Network, a second-layer scaling solution, to provide a sufficiently scalable system. Additionally, another off-chain scaling approach would be Bitcoin-backed banks as originally proposed by Hal Finney. Block space on the main chain would require high fees and thus be reserved for few high-value transactions. Proponents of Bitcoin Cash and Bitcoin SV aim to achieve scalability fully on-chain through increasing the block size from Bitcoin’s current 1 MB limit. This would ultimately lead to the second scenario of high on-chain transaction volume and low fees.

Only time will tell which transaction model for Bitcoin will be stable. The transition phase from the current block reward security model to one that is largely based on transaction fees will be gradual and continue at least through the upcoming halvings in 2020 and 2024. How the markets respond to this transition will be an important indicator for investors to monitor.