Token Burning Mechanisms

Nov 19, 2019

At the beginning of November, the Stellar Development Foundation announced that they had burned 55 billion Stellar (XLM) tokens, or about half the total supply. This led to a short-lived price increase by about 30 %, which has relatively quickly retraced to the original price levels. Token burns are not uncommon in the cryptocurrency world – major tokens such as MakerDAO’s MKR, Binance’s BNB and Bitfinex’s LEO are regularly burned.

There are various ways to burn tokens. One of the two major methods is sending the tokens to an address for which nobody possesses the private key. For example, the Ethereum address 0x0 (a common burn address) contains more than $900M worth of ERC-20 tokens. Another – possibly superior – method is to include a “burn” function in the smart contract or protocol that issues the token. The advantage of this is that the burnt amount can be deducted from the total supply and thus is more transparent at reflecting the actual burn events.

The reasoning behind token burns is usually that a reduction in total supply should lead to a higher token price. However, the market still has to actively adjust to the reduced supply – as the example of Stellar’s large burn shows, a correlation between sustainable price increases and burn events is far from certain. This is in contrast to direct revenue sharing tokens: A simple example for one of the oldest tokens with such a mechanism would be DICE, the token for an online dice rolling gambling game, which directly pays out dividends to token holders based on house profits.

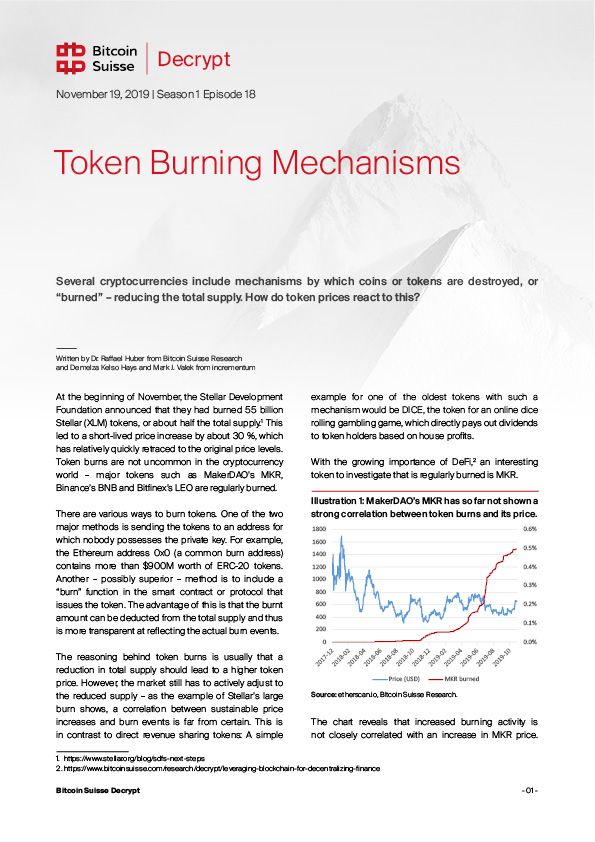

With the growing importance of DeFi, an interesting token to investigate that is regularly burned is MKR.

The chart reveals that increased burning activity is not closely correlated with an increase in MKR price. So far, only about 0.5 % of the total MKR supply has been burned as stability fees for open CDPs (or to embrace new terminology suggested by Maker, “Vaults”). However, since stability fees only need to be paid when closing the CDP, another 8’400 MKR tokens (0.84 % of total supply) will be burned in the future from currently accrued fees. The migration to multi-collateral DAI that started on November 18 might lead to increased burning activity, since CDPs will be forced to close, pay the stability fee and reopen under the new protocol.

Another prominent class of tokens that often feature burning mechanisms are exchange tokens such as KNC (from the decentralized exchange Kyber) or BNB (Binance’s token).

Illustration 2: KNC price (top) has barely reacted to continuous token burning, whereas BNB (bottom) has strongly outperformed most other cryptocurrencies.

Source: etherscan.io, Binance, Bitcoin Suisse Research

Whereas Kyber’s KNC price has barely reacted to continuous burning up to currently 1.32 % of the total supply, BNB has strongly outperformed most other cryptocurrency. This may be due to the high percentage of 7.26 % of the total supply that has been burned so far; Binance will continue to burn tokens based on their profit until the supply hits 100 million tokens.

However, this most likely was not the only reason for BNB’s outperformance. BNB’s utility aspects also include a 25 % discount on trading fees, or a higher chance to participate in IEOs run on the exchange based on the amount of BNB held in a trader’s account. As such, an analysis of token burns versus price in a vacuum misses the whole picture of what drives the value of a utility token.

A Token Burn Is Not a Stock Buyback

A token burn cannot be compared to a stock buyback for two reasons. First, a buyback is when a company purchases its own shares that are trading in the open market. For example, when Stellar burned 55 billion coins, they did not buy the coins off of the open market that were part of Stellar’s float. Instead, they burned tokens that were held by the development team and were not trading in the open market. Second, the majority of tokens that do burns do not represent equity in a company, and therefore, coin or token investors do not enjoy an increased share of ownership in a company and that company’s future cash flows. When a company does a buyback, the size of the shareholder’s equity liability decreases, and the company’s cash assets decrease. However, when a cryptocurrency company does a token burn of coins that they are withholding from the market, this represents a decrease in the asset side and no subsequent offsetting transaction from the liabilities side, because payment coins do not represent liabilities for issuers according to FINMA.

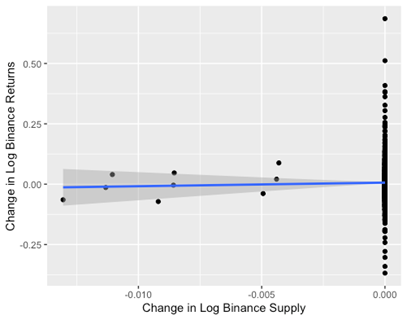

Out of the many token burn mechanisms, some are more effective than others at increasing the price of a coin. The four main burning methods are: ICO burns, Circulation (VeChain, Tron), Out of Circulation (EOS, Stellar), and Burning During Each Transaction (XRP, ETH with EIP-1559). Binance’s quarterly token burns do not have a significant impact on the Binance Coin (BNB) price, but they do affect positively the rate of change/growth rate in BNB’s price. Two separate models were used to study the price: In the first model, the log of BNB’s price was regressed on the log of BNB’s supply with a dummy variable representing the days that Binance did a coin burn and control variables for trading volume, market cap, and volatility. The dummy variable was assigned to “0” when a token burn occurred on that day and “1” when a token burn did not occur on that day.

The results were insignificant for the first model. The second model was a difference and difference model to capture endogenous independent variables that the model did not account for directly. On days when a buyback occurred, the growth rate of Binance’s price was 0.02 higher than on days when a burn did not occur. The results were significant at the 10% significance level. This means that the probability of rejecting the null hypothesis when it is true is 10% or in other words that 10% of the time, the study sample would find that Binance’s burns have a positive impact on the growth rate, when in actuality, no impact exists. Illustration 3 shows that on most days, the growth rate in supply was zero, and on the days when the burns occurred, the supply shock ranged from negative 0.004 to 0.013, and on some burns the price rose and on other burns the price sank.

The duration of the positive growth rate was analyzed with lagged variables (1 week, 2 weeks, and 1 month), and none of the buyback lags (1 week, 2-week, 1 month) had a significant influence on the price. This suggests that the effect is only contemporaneous and lasts less than a week. The caveat to this analysis, the results are based on a small sample of data, and therefore, the results may change as more Binance does more burns in the future.

Holding all else equal, a coin burn that decreases a token’s circulating supply on the open market by 50% should lead to a doubling or 100% increase in that coin’s price. However, this gain may be short lived, because this can signal to investors that the company did not have a better investment opportunity available such as developing new features for the coin that can boost user adoption and organic growth.

Furthermore, the real world rarely behaves like an economic model, because not all variables can be held constant. For example, even if a company buys back tokens from the secondary market, this could be offset with new coins coming to the market from investors, stakers, or miners that want to sell. Also, investors learn over time. If investors expected the price of a token to respond positively to a future token burn, then investors could invest in the coin prior to the token burn in anticipation of a capital gain.

Bitcoin Suisse