Thinking Beyond 2022 – Macro Trends We See

Jan 31, 2022

- Inflation rates, though claimed to be “transitory”, are increasing to new record highs in the US and Europe. Bitcoin reaches new all-time highs against this background putting itself up as a hedge against inflation worries.

- Two major macro events in 2021 influence the development of Bitcoin in 2022 and beyond. The Great Mining Migration out of China shifted the geopolitical power structure for Bitcoin mining. The step to declare Bitcoin legal tender, catapulted El Salvador onto global Bitcoin scene and puts subtle pressure on other countries with heavy monetary dependence on the UD Dollar, to get clarity about their national Bitcoin strategy.

- More sense and sensibility will benefit Bitcoin’s sustainability debate greatly in 2022 and beyond. Free, instant, mining-free Bitcoin Lightning payments push the debate beyond energy and show the positive impacts, a publicly governed financial system like Bitcoin can have on financial inclusion.

Traditional finance and peak inflation

Fiat money. In 2021 the “Nixon Shock” had its inglorious 50th year anniversary. Half a century ago, on 15 August 1971, US President Nixon held a speech that ushered in a new monetary era – the era of fiat money. Nixon suspended the convertibility of the US dollar into gold, de facto ending the Bretton Woods agreement that had fixed international exchange rates against a gold-backed US dollar since World War II. With the suspension, Nixon decoupled the US dollar from the pressure to stick to the gold reserves and enabled the government to issue bonds against new currency from the Federal Reserve to address domestic issues like high unemployment. Since then, all major currencies have become free floating fiat currencies and all face similar problems: the amount of money supply is growing over time, leading to high GDP-to-debt ratios and inflated prices in many countries.

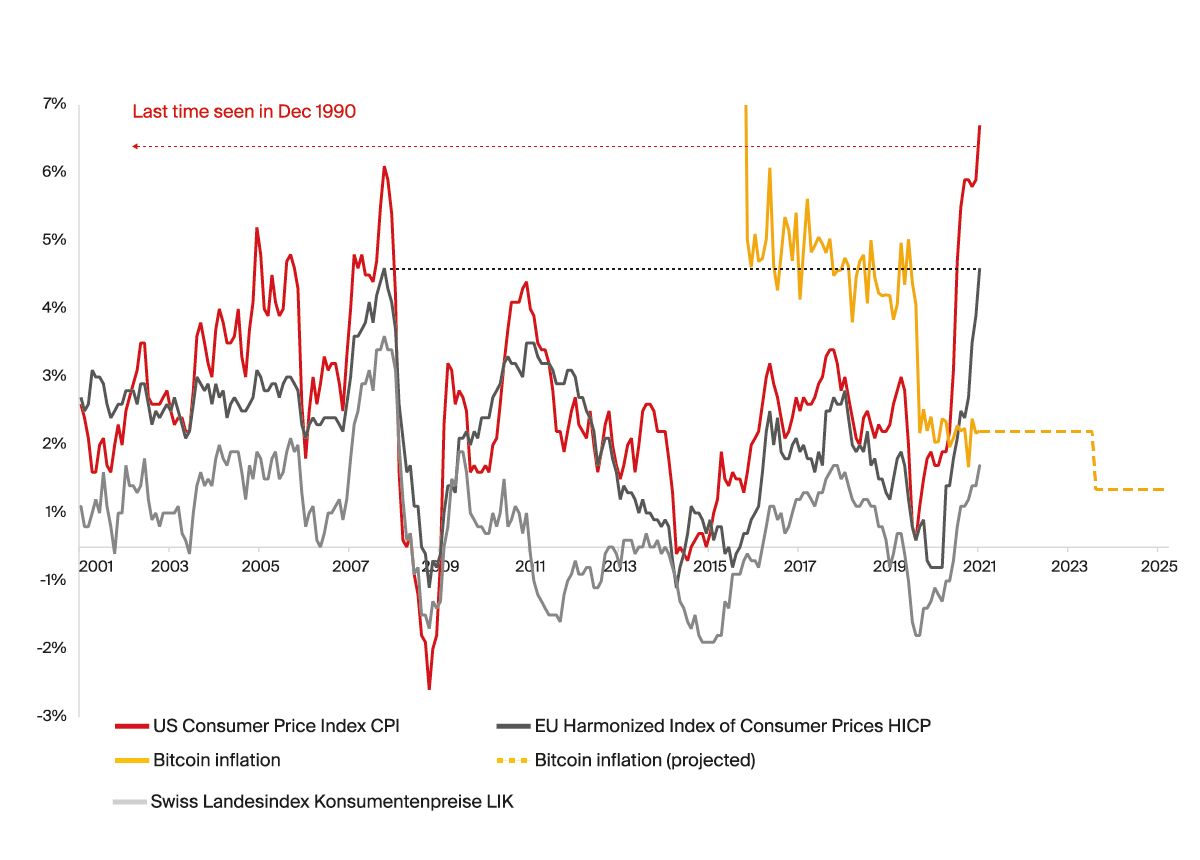

Inflation. In 2021, the numbers show that inflation rates are surpassing levels last seen at least a decade ago, right before the Great Financial Crisis 2008/2009, and hitting a 30-year peak in the US (illustration 1). The November Financial Stability Report of the Board of Governors of the Federal Reserve System therefore rightly lists “persistent inflation and monetary tightening” as risk #1.

While the Federal Reserve is assuring the public that the inflation rates are “transitory”, they are in fact in a difficult situation. The core of the problem is that fiat money creation is debt creation at the same time. The increase in money supply has also increased the debt of the US (and similar in other regions/nations) as asset purchase programs were paid by the central banks with newly created money. Now, the Fed needs to keep bond yields – the cost for debt – low to protect the government’s debt service. At the same time, the Fed should taper, i.e., reduce Quantitative Easing and maybe increase interest rates, to counter the price pressure coming from inflation.

The root problem with conventional currency is all the trust that's required to make it work. The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust.

— Satoshi Nakamoto (The Quotable Satoshi, NakamotoInstitue.org)

So, which forces will prevail for the 2021/2022 transition? The Fed’s intentions to taper, reduce of quantitative easing and possibly raise interest rates? Or the up-ward price pressure because of the extraordinary money supply increases caused by the Fed in the last 24 months, in addition to the interrupted supply chains and business shut-downs because of COVID restrictions?

Bitcoin: inflation hedge and payment solution for nations

Inflation hedge. Over 2021, major global stock indices moved moderately and performed through the first eleven months in the range 5%-22%, with the negative exceptions of China’s Hang Seng (-11%) and gold (-9%). You may wonder, what fuels this extraordinary market recovery from the 2020 crash and why the markets are chugging along in 2021 when, at the same time, supply chains are disrupted, businesses falter or close because they run out of either material, people, or both, and energy prices are tightening. With the fundamental outlook this weary, what is fueling these markets?

“Fed put” is the term for a range of monetary tools (i.a. repurchase agreements as indirect QE, large treasury bond purchases at high prices, lowered federal funds rate for cheap borrowing) exercised in one way or another by all recent Fed chairmen, beginning with Alan Greenspan’s policy response to the 1987 Black Monday crash. Over the decades, markets have learned that when a crisis arose with stock markets falling, the Fed would engage in ways that would cause the fall to reverse, leading to moral hazard: more and more speculative behavior by investment banks in markets perceived as “risk-free.” This behavior resulted in what was named the “Everything Bubble”: a situation where several asset classes show strong performance simultaneously. This is a phenomenon people see again this year.

High up on [Biden’s] list and sooner rather than later, we’ll be dealing with the consequences of the biggest financial bubble in U.S. history. Why the biggest? Because it encompasses not just stocks but pretty much every other financial asset too. And for that, you may thank the Federal Reserve.

— Richard Cookson, Bloomberg (4 February 2021)

With prices systematically distorted, investors find it harder and harder to make sense of market signals – and to trust them.

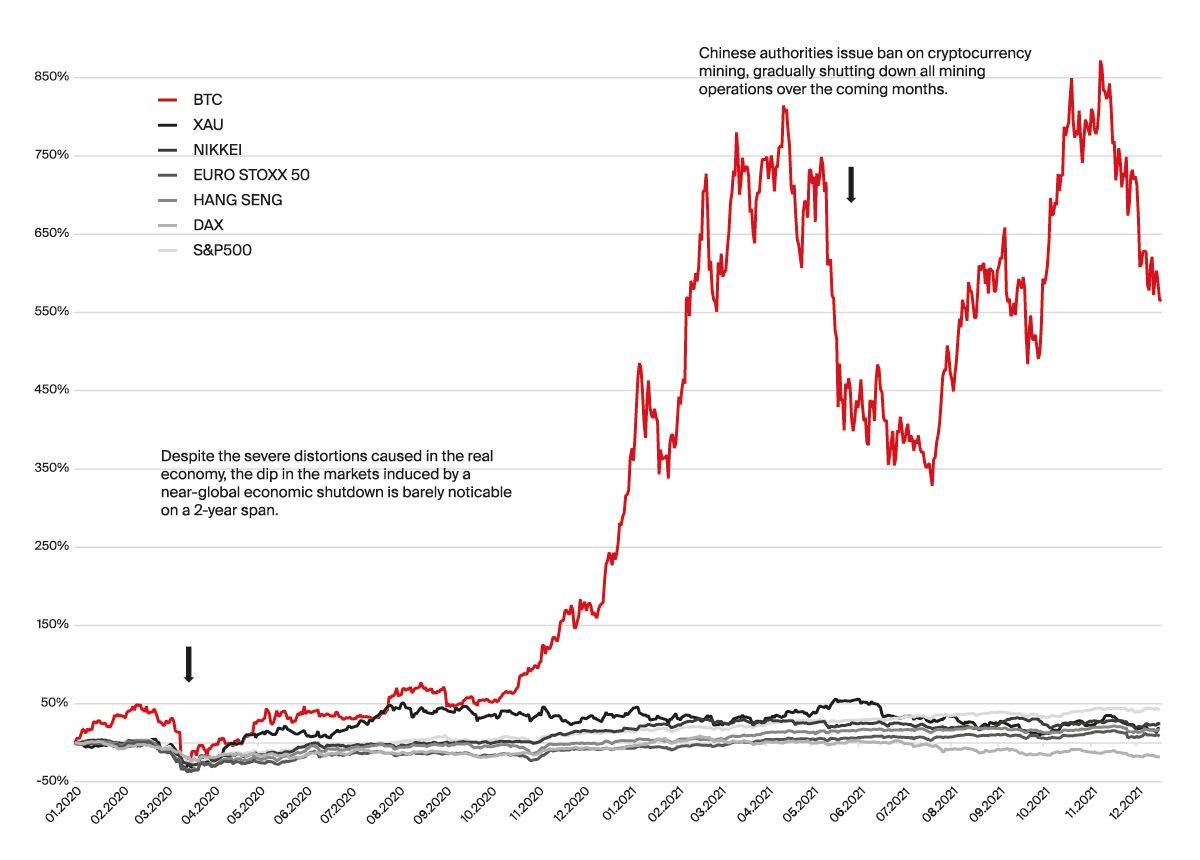

Bitcoin bull run. Against this precarious macroeconomic backdrop, Bitcoin passed a few new all-time highs and shot up 90% in 2021 YTD; and is up over 650% since January 2020 (illustration 2), while major indices moved in the lower two-digit range. Despite extreme volatility, investors seem to put increasing amounts of trust in Bitcoin’s monetary policy that is the literal opposite of central banks’ monetary policies: An absolute hard cap of 21m units and a self-reinforcing, cryptoeconomic assurance that the monetary policy will remain unaltered permanently seems to make for an attractive hedge against inflation worries.

The current Bitcoin bull run began after the 3rd Halving (11.05.2020), when markets also saw increasing adoption by institutional investors throughout that year. Today, public and private companies and trusts collectively own over 7% of the total supply of 21m bitcoin.

Another relevant milestone for Bitcoin investors was reached in 2021. One of the long-awaited traditional instruments that allows investors to get exposure to crypto assets are Exchange Traded Funds (ETF). On 19.10.2021 the first Bitcoin-linked ETF, ProShares Bitcoin Strategy ETF (BITO), launched one day after receiving SEC approval. The futures ETF broke several records on the spot: It was the second biggest ETF debut of all time, trading over $1 billion on the first day. In general, ETFs allow investors who are unable or unwilling to invest in the underlying crypto asset to invest using a traditional instrument that is known by market players and thus enable a new group of investors to get exposure.

Beyond investment circles, Bitcoin adoption among “ordinary people and use cases related to transactions and individual savings, not trading and speculation” also grew. The 2021 Global Crypto Adoption Index, a country-level metric based on on-chain value received, on-chain retail value received, and P2P exchange trade volume, jumped 880% in aggregate. It is interesting to see that the top 5 countries in this list mostly declared Bitcoin illegal (*): Vietnam*, India, Pakistan*, Ukraine, and Kenya*, while only one of the mostly Bitcoin-liberal Western countries made it into the top 20, the United States.

From a macro perspective, three events, one expected, two unexpected, have stood out in overlaying Bitcoin’s base dynamic in 2021. Two are of geopolitical significance, touching on the topic of national sovereignty, albeit having contributed to Bitcoin’s performance in opposite directions. The third is an obscure technical improvement that may show its profound impact only later.

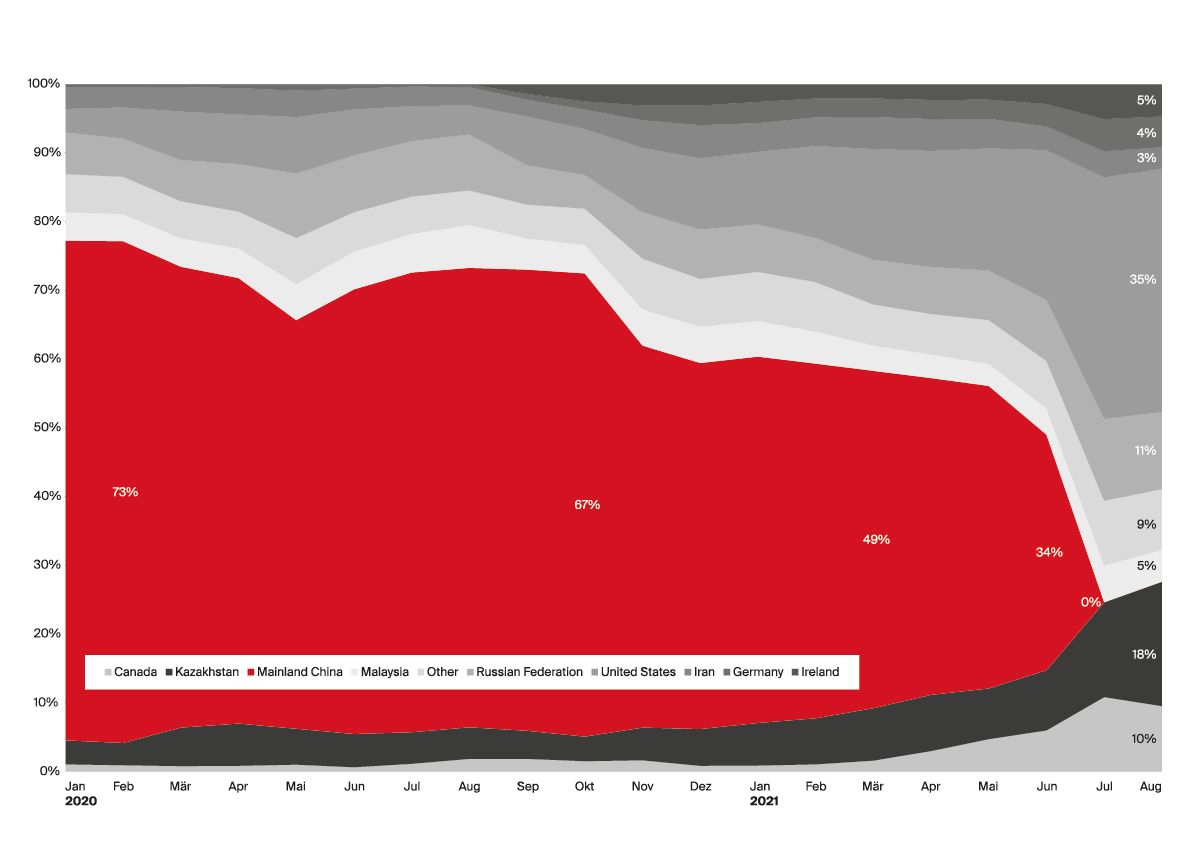

First, the “Great Mining Migration” from China. In June 2021, news broke that China issued a ban on cryptocurrency mining, ordering power companies to stop supplying electricity to miners within days. Unlike “bans” in the past, this time, authorities were serious and followed-up until all mining operations in the country stopped. This resulted in a very significant drop in hash-rate and the exodus of many mining operations to other countries, ranging from the United States to Kazakhstan, Russia, and Canada according to the Cambridge Center for Alternative Finance (illustration 3).

The geopolitical implications of this migration may be profound: (1) If reports (e.g., Reuters, Coindesk, etc.) are to be trusted, 2021 is the year China robbed itself of the possibility to exert any control over Bitcoin mining within its own borders. Should at any point in the future, Bitcoin gain more traction as a reserve currency, it will be very costly for China to get back into the game and impossible to ever regain a dominant position. (2) While the migration led to a more even distribution of hash power, it is less than perfect that the role of dominant host simply switched to the next country in line instead of dispersing among several countries: the US now harbors over a third (35%) of the world’s Bitcoin hash power, a strength we expect to attain geopolitical relevance in the long term. (3) Miners everywhere learned the lesson that a stable regulatory environment is very important for the mining business in which interruptions are very costly. In the future, they will probably be better prepared to move their operations even quicker to other jurisdictions and overall transform themselves into a “geo-neutral operation” (F2Pool). (4) On a positive note, it can be expected that the energy mix of Bitcoin mining is getting a boost towards “green” as the new locations outside of China, at least in the West, will demand renewable sources of energy for their mining operations and overall provide a more stable regulatory environment for Bitcoin.

Did the drop on hash rate hurt the Bitcoin network? Temporarily for sure. News of a government banning parts of Bitcoin’s modus operandi always create uncertainty. However, over time, markets realized that the hash rate was not lost but only reallocated to more welcoming spots, and that the switch took time. Within half a year, the network hash rate is back at pre-ban levels and bestowed the miners who stayed online during that period additional profits as the difficulty rate adjusted downwards.

Second, the first Bitcoin Nation is El Salvador. The other event of geopolitical significance is that a first nation state adopted Bitcoin as legal tender – an event that most observers expected to happen, if at all, only many years in the future. However, in short succession, the state of El Salvador in Central America, made several steps towards putting the relations of their nation state with Bitcoin on an entirely new footing.

While China decided fully against Bitcoin and with most states struggling with crypto currencies, El Salvador made several bold steps that amount to an “all-in” on Bitcoin:

– 8 June, Bitcoin Law passed by parliament

– 7 September, Bitcoin becomes legal tender besides the US Dollar

– September, with a $30 present in bitcoin, government onboards 3m citizens in one month

– Sep-Nov, government acquires a total of 1,120 bitcoin for a Bitcoin liquidity fund

– 23 November, government announces $1bn Bitcoin bond (10 years, 6.5% coupon) to buy bitcoin and build a tax-free “Bitcoin City”

This series of “Bitcoin firsts” for a nation state is staggering. It is very early and unknown territory, but let’s think about some of the potential ramifications of these steps:

(1) Against recommendations from the IMF and WB and their refusal to offer technical assistance in the introduction of Bitcoin, El Salvador went ahead, clearly signaling its intention to follow an independent, sovereign financial path. Irrespective of the outcome, this is remarkable for a dollarized country that is not even on the top 100 of the largest economies. Either the government and their advisors are complete fools gambling with their people’s financial resources – or they have a playbook only few outside the Bitcoin community really understand. It remains to be seen whether we will see other countries moving as boldly in 2022 or not (yet).

(2) Making Bitcoin legal tender is an aggressive way of making bitcoin available as a government. More than a few critics mocked this approach as non-liberal for a currency that is supposed to bring freedom and financial inclusion. On the other side, one can argue that very few countries are able to follow El Salvador’s Bitcoin playbook as very few companies can follow MicroStrategy’s Bitcoin playbook – the decision to go “all-in” on Bitcoin. It takes the riskiest strategy to enable the biggest rewards, not many can follow this strategy.

(3) Onboarding 3 million persons in one month also shows what is technically possible with Bitcoin Lightning in a population with more mobile phones than citizens. The side effect is that the 70% unbanked EL Salvadorans now have a safe, fast, and cheap means to receive remittances from their loved ones abroad. In the case of El Salvador, remittances make up 24% (!) of GDP or nearly $6bn in 2020. Looking at the big picture, what happens if more countries decide to solve their remittance problem using Bitcoin? The World Bank estimates the total of remittances flowing into Central and South America in 2020 to be $88.5bn. Plus, there is another continent suffering similar problems: Africa receives a similar amount in remittances from abroad, $83.4bn. To anyone living in any of the 77 countries, the idea of receiving financial support at home (safer) and digital (faster) and without remittance service providers (cheaper) will make immediate sense. Bitcoin being a permissionless technology, these people do not need to wait for their governments to act, they can simply switch.

(4) Owning bitcoin offers the El Salvadoran government an inflation-resistant diversification to the national reserve that is a bearer instrument, not a debt-based fiat currency. Gold would fulfill the same purpose but is more expensive to hold, much more cumbersome to make available in small quantities and impossible to use online. Given that bitcoin can be used in tiny quantities (“satoshis”, see below), let’s make a quick speculative calculation for the scenario that the country would abandon the US Dollar and switch to bitcoin entirely. Assuming that the government would not buy additional bitcoin, how much value would one bitcoin need to represent in order for 1,120 bitcoin to represent the $26bn GDP sometime in the future? The price per 1 bitcoin would need to be reflective of $23m worth of economic activity. Under such a scenario 1 sat would represent a quarter dollar, a useful size that is already transactable today using the Bitcoin Lightning network.

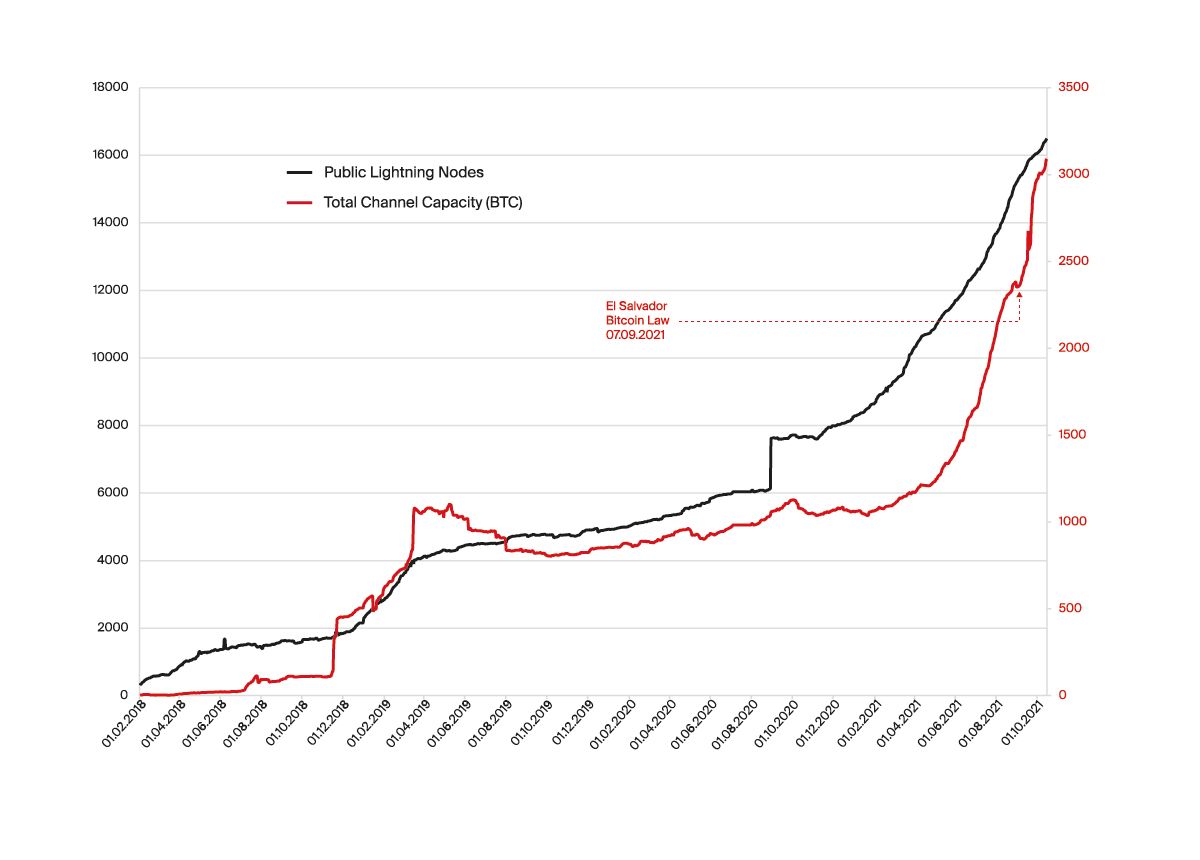

Onboarding millions of people in a short time put the Bitcoin Lightning network – the scalable payment layer built on top of the Bitcoin network – into the spotlight in 2021. Compared to base-layer Bitcoin transactions, the Lightning network offers instant and free payments that do not require mining and scale without clogging up the base network. The number of nodes powering the Lightning network doubled while channel capacity tripled in 2021 alone, as illustration 4 shows.

Third, “Taproot” was activated. At block height #709632 on 14 November 2021, Taproot became active. While the previous two developments even made it to the mainstream news, the activation of Taproot made much less headline, maybe unjustly, because the soft fork named “Taproot” is considered the most significant upgrade to the Bitcoin protocol since SegWit in 2017.

Taproot introduces Schnorr signatures (BIP-340). They make multi-sig transactions smaller by allowing signature aggregation and they increase privacy as TR transactions will look the same, be they Lightning channel transactions, multi-sigs, or simple standard transactions. Taproot expands smart contract functionality by introducing a new transaction output type, SegWit v1 (BIP-341), and increases privacy by enabling different spending paths of which all are hidden except the one executed. Finally, Taproot upgrades Bitcoin’s script language to ‘Tapscript’, which allows more complex, contract-like control over spending coins. It also introduces upgradeability for the script language itself.

From a user perspective, the benefits of Taproot are increased scalability through smaller transactions, improved privacy for transactions, and a future-proof upgrade to scripting. Taken together, the soft fork lays the necessary groundwork for “Bitcoin DeFi (BiFi)” in the future. It may not be as powerful as Ethereum’s Virtual Machine, however, it achieves smart contract functionality with a much less complex technical architecture than Ethereum, especially considering the migration to Proof-of-Stake and sharding.

– We invite you to read our in-depth article about Ethereum’s Long Chain of Forks towards “The Merge” in this Outlook edition!

Sense and sensibility in the sustainability debate

The unobjective ESG debate. The China ban and ensuing “great mining migration” as well as the idea of “volcano mining” in El Salvador, have both rekindled the debate about Bitcoin’s energy consumption. Due to increased institutional adoption of Bitcoin and crypto, the debate was further extended into the larger ESG context, which refers to the “environmental, social, and governance” aspects of due diligence screenings for investment allocations and company ratings.

The ESG debate in Bitcoin is cumbersome for several reasons. First, the inner workings of Bitcoin, where and how energy is used and what second order effects result from that, are inherently complicated, multi-disciplinary, and hard to grasp for many people. Second, Bitcoin’s transparency makes it compelling to abstract away the complexity and pick easy-to-measure metrics for comparisons. The case in point is the practice of comparing Bitcoin’s electricity consumption with that of countries. The most cited country in 2021 was Argentina, with 122 TWh electricity consumption in 2019 according to the US Energy Information Administration, which is the same data source used by the Cambridge Center for Alternative Finance for their meaningless country comparison. Why meaningless? First, Bitcoin is not a country. Second, countries are very different. Which of the following countries uses the most electricity: Ukraine, Norway, United Arab Emirates, or Argentina? Answer: they all consume a similar amount of electricity (1.1% deviation, US EIA data), although they are vastly different in almost all other aspects: population, area, human development, gross domestic product, etc. Electricity use alone says nothing when comparing countries and it says even less if you compare with non-country entities.

Energy. Several sources provided quantitative data on Bitcoin’s electricity use in 2021. The Bitcoin Mining Council (BMC) uses a self-reporting survey whose respondents cover 33% of global mining hash rate. According to their Q3 data report, Bitcoin uses 188 TWh per year. This is 0.12% of global energy production or 0.38% of energy wasted as 1/3 (!) of all energy generated worldwide is lost due to inefficiencies. Compared with other industries, Bitcoin mining is below gold mining (571 TWh), computer games (214 TWh), and the use of holiday lights (201 TWh). Based on the past, the BMC predicts a 24x efficiency improvement in Bitcoin mining over the next eight years.

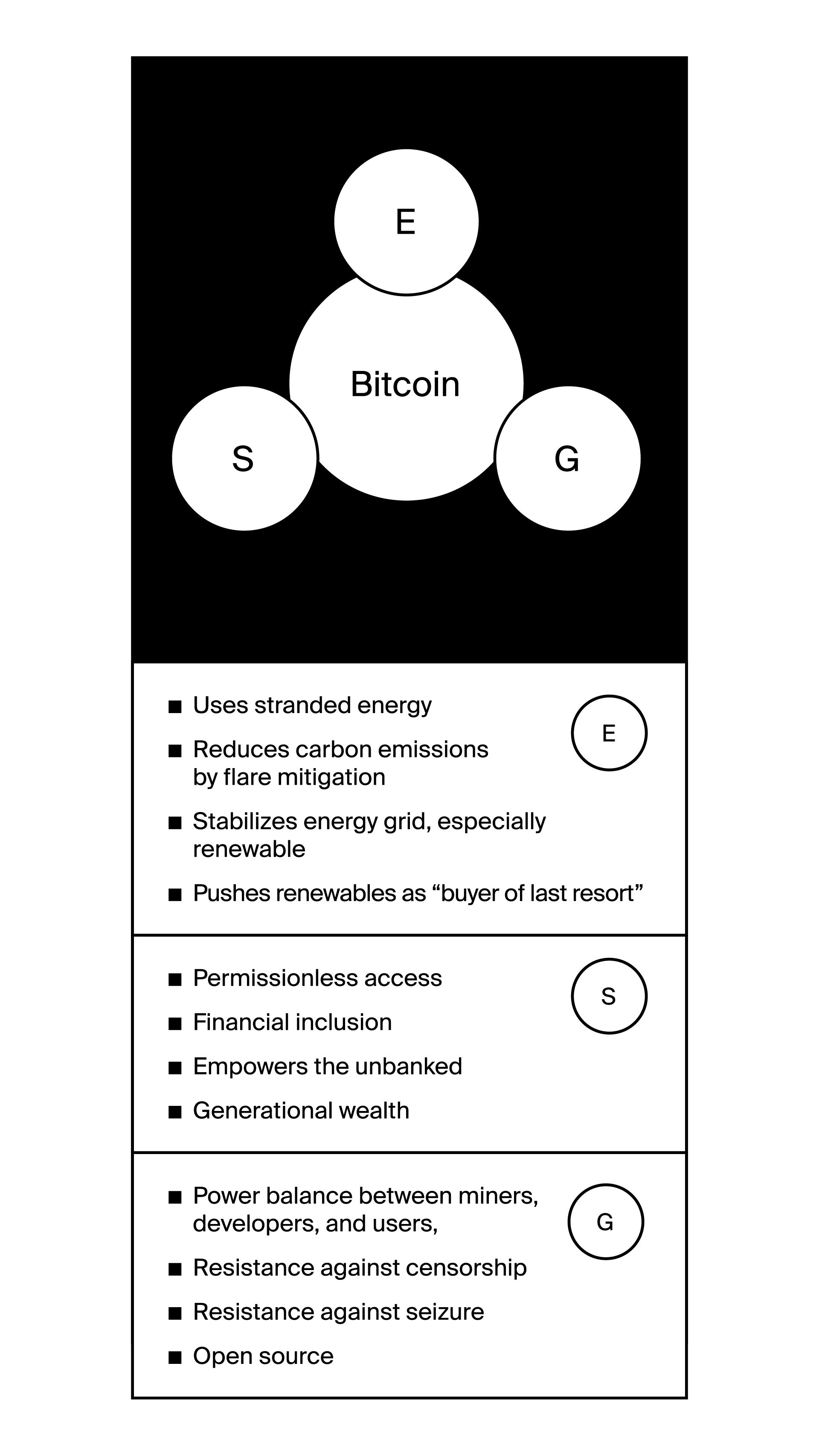

With the energy discussion being center stage, the social impact and governance aspects of Bitcoin gets much less attention. We provide a qualitative overview on these two dimensions (illustration 5).

The positive social impact of Bitcoin stems primarily from its permissionless design: anywhere in the world, anyone can at any time enjoy the financial services Bitcoin offers – send and receive any amount to/from anyone else directly. The only requirement is an internet-connected device. This potential for independent self-empowerment might not be appreciated much in countries with a functioning digital banking system like Switzerland or Western Europe. However, for the 1.7 billion “unbanked” on the planet (31%) this low entry barrier may be life changing. Therefore, 8 of the 17 SDG have financial inclusion as one of their targets. If Bitcoin payments prove successful in El Salvador, knowledge and software tools may spread like wildfire across the Americas and Africa.

From a governance perspective, Bitcoin is still often portrayed– also by the media – as an anarchist, opaque, inner circle favoring those who got in early and an overall unfair environment for everyone else (if not taken as an outright “scam”). This portrayal usually stems from a lack of understanding about the way Bitcoin is governed as an open-source project with economic incentives. Power over Bitcoin’s monetary policy is indeed balanced across three powers: developers decide which software rules to “code”/legislate, miners decide which rules to execute, and users (besides being the citizens) judge which software rules they consider legitimate. The current rule set is designed for Bitcoin to be censorship-resistant as well as seizure-resistant, two properties no other form of money currently fulfills.

– We invite you to read our in-depth interview with Alex Gladstein on “Bitcoin, human rights, and the ESG Debate” in this Outlook edition!

Ethereum: Cambrian explosion in the smart contract universe

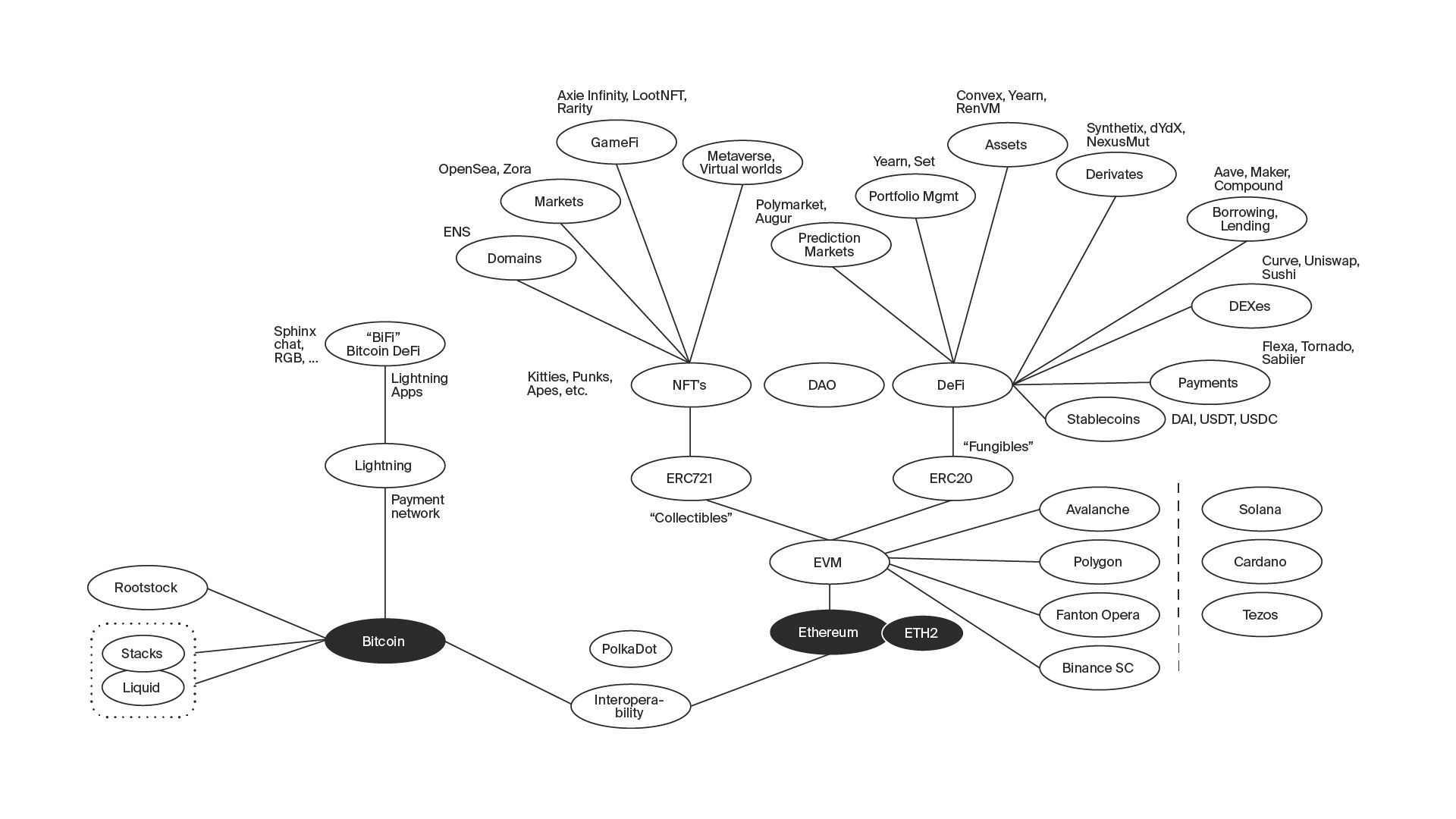

Whether building on the success of Ethereum during “DeFi Summer 2020” or whether losing patience with the slow development of the platform in terms of performance and consensus, the Ethereum universe experienced a Cambrian explosion in all directions over the last 1.5 years (illustration 6).

What started with new protocols on top of Ethereum extended sidewards into new, independent smart contract platforms – some EVM-compatible, some entirely new; some symbiotic, some competitive; but all stirring up the space and unleashing innovative forces in all directions.

The other direction was upward: The DeFi space in the narrow sense powered by Liquidity Pools, Automated Market Makers that enabled borrowing/Lending, Decentralized Exchanges, stablecoins, derivatives, prediction markets, and more got new neighbors. Non-fungible tokens (NFTs) conquered a space of their own: starting with artwork and animals of various kinds, marketplaces developed, play-to-earn models created GameFi, and most recently people have started to talk about the metaverse, which was there all the time as virtual worlds.

No wonder, the Ethereum developers put all their focus on making Ethereum fit for the next level, cutting the Gordian Knot of blockchain-inherent limitations. Work on Layer-2 scaling solutions exploded in all directions as well: state channels, different types of rollups, side chains, plasma chains, etc.

– We invite you to read our in-depth article on “Ethereum 2.0” in this Outlook edition!

Decentralized Finance: “The Road ahead”

From a quantitative view, the DeFi market exploded in 2021. Total Value Locked (TVL) of all DeFi chains (not only Ethereum) surged from $21.5b to $255.1b YTD, which is a factor of nearly twelve. Despite growing competition, Ethereum still dominates the DeFi space with a TVL of $166b (65%).

In this Outlook edition, Prof. Fabian Schär (University of Basel) highlights several trends in Decentralized Finance (DeFi) he sees unfolding in the next year. We just list them and invite you to read his article on page XXX: (1) regulators handling of “decentralization theater”, (2) the market for institutions also in decentralized protocols, (3) improvements of governance beyond governance tokens, (4) the growing malpractice of “Maximal Extractable Value (MEV)” by miners/validators, and (5) scalability and developments on Layer-2.

- We invite you to read the contribution by Prof. Schär on “Decentralized Finance” in this Outlook edition!

One of the hippest corners in DeFi have been Non-Fungible Tokens or NFTs. An NFT is most akin to a piece of art as it represents a single digital, collectable object. The numbers? Total NFT sales in 2021 YTD were $300m across $79,100 sales transactions resulting in a NFT being valued at $3,780 on average. With popular series issuing 10’000 more or less varied versions of pixelated Bored Apes or CryptoPunks, Sotheby’s herald NFTs as the “future of art”, while a former Christie’s auctioneer thinks the concept makes “no sense.”

While the value of art lies in the eyes of the beholder, NFT use cases can also carry utility: be it in virtual worlds like in DecentraLand or Axie Infinity; in new science funding models like STEM-Genesis; or in a dozen other use cases.

Conclusion

2021 has been an intense year, not only for the crypto markets. The economic after-effects of various COVID measures weigh heavy on some parts of our societies. While all major stock market indices point upwards over 2021, the increase in inflation takes away some of the conviction about the reliability of these figures.

Against this backdrop, or because of it, Bitcoin has shown an impressive positive performance, hitting more than one new all-time highs in 2021. Three events stood out: The Great Mining Migration out of China had no lasting negative impact on the overall market outlook. Positive impulses from El Salvador’s move to accept Bitcoin as legal tender pushed Lightning technology in the limelight and let Bitcoin use for small payments surge. Finally, the Taproot upgrade paved the way for “Bitcoin DeFi”.

Bitcoin’s energy debate has been growing into a full-fledged sustainability debate, which will bring social and governance aspects into the discourse as well.

Ethereum and DeFi are experiencing a Cambrian explosion of protocols, projects, and platforms – with NFTs only being the latest iteration of exploration.

The crypto space is expanding in all directions at an incredible pace. While some developments seem like crazy, exaggerated hype with not much real-life foundation, some others are underestimated and may indeed change the world. Therefore, thinking crypto always demands thinking beyond.

Marcus Dapp

Head of Research