Macro view - with an eye on Bitcoin

- Central banks cannot print energy or food. A war in Europe adds to the high-inflation environment and will cause supply shortages in 2023 and beyond that need time to solve. De-globalization in favor of national sovereignty is emerging.

- Central banks cannot ease and tighten simultaneously. All major economies fight with high debt levels in the face of interest rate hikes. Debt-based fiat currencies are getting under pressure, and de-dollarization has become a trend.

- Who needs central banks anyway? Despite a dim macro-outlook and too many CeFi shenanigans causing contagion well into 2023, Bitcoin adoption is increasing with nation states and institutions. Technical innovations on layers 2 and 3 bring new use cases to the Bitcoin/Lightning ecosystem.

Geopolitics hit everyone

In 2022, geopolitics hit hard in several aspects. Starting into 2022, the world was still trying to escape the lock- down-induced global supply chain interruptions from the previous year. The Federal Reserve (FED) and the European Central Bank (ECB) had already increased money supplies tremendously[1] when the 24 February 2022 came, and Europe had to witness Russia’s invasion of the Ukraine. What was planned to be a swift takeover has turned out to be an enduring stalemate that is ongoing at the time of writing.

The implications are still unfolding and will reach far into 2023 and beyond. According to geopolitical analyst Peter Zeihan, Russia, Belarus, and Ukraine combined form a dominant export region. Together, they rank global first in natural gas, uranium, neon (required for microchips), wheat, potash and fertilizer; global second in crude oil, oil products, steel, seed oil; and global third in coal, gas turbines, aluminum, and titanium[2]. Many countries in the world are depending on these commodities with interruptions having significant short- term consequences (e.g., wheat) as well as long-term (e.g, fertilizer, neon). Rectifying the shortage in certain commodities by building infrastructure in other countries may take years according to Zeihan. What has started as a local/regional conflict will have global impact in 2023 and beyond as other, remote countries will be affected.

Especially the interruption of the energy supply from Russia to Western Europe, caused by sanctions and pipe- line blowups, are not only causing human suffering and extraordinary measures by governments, but will have impacts on the economic outlook for Europe as a whole.

In addition to existing embargos, including disconnecting Russia from the Swift system and freezing its foreign currency reserves, the EU and G7 are imposing an import ban and price cap on Russian oil starting January 2023 with the aim to restrict Russian oil exports without increasing global oil prices[3]. The outcome will be determined by whether Russia will be able to circumvent the price cap, how strong its dependence on oil income is and how sensitive the EU and the G7 are to rising oil prices.

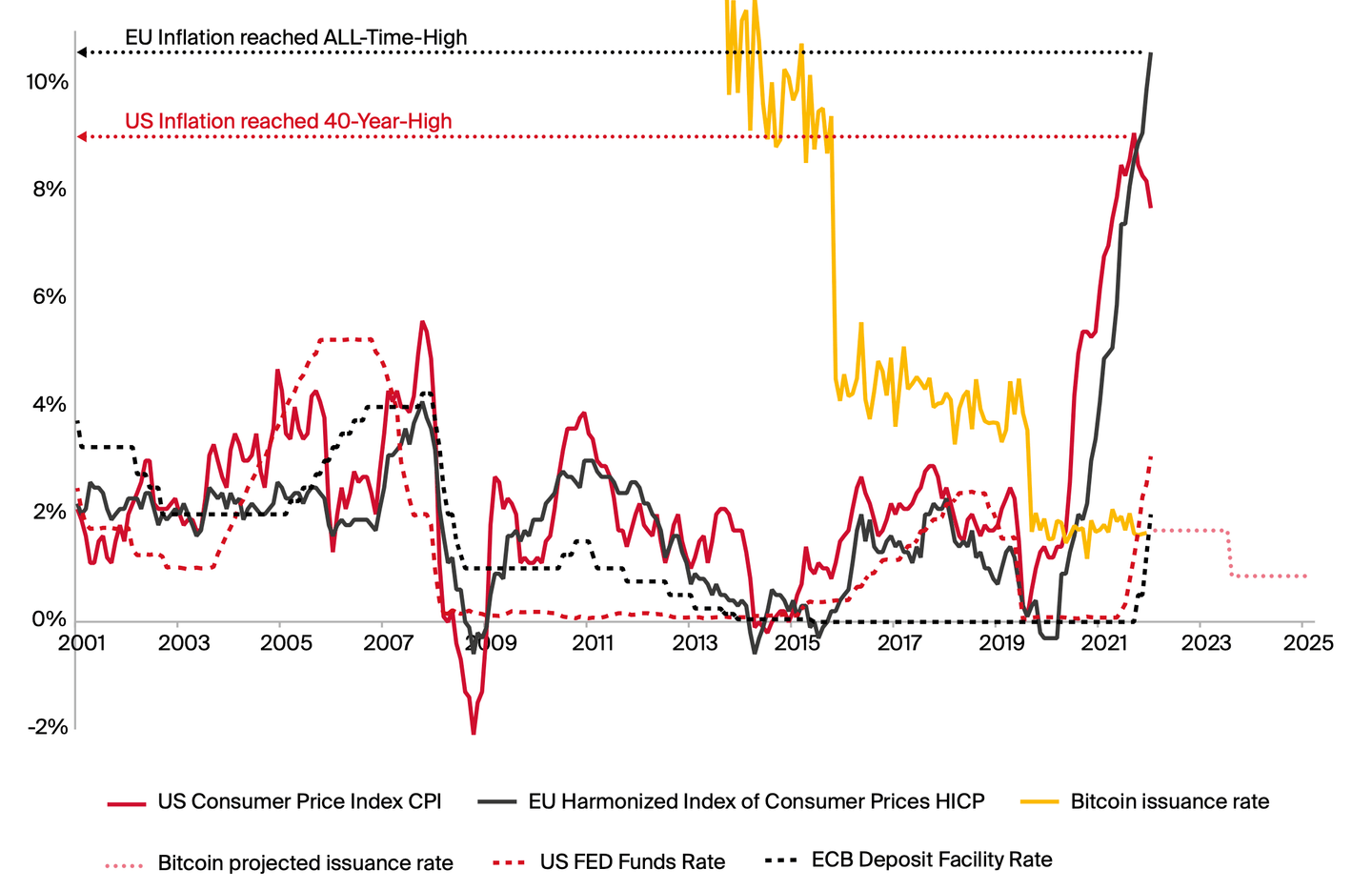

All these geopolitical factors only add to the inflationary pressure that was already reaching a new record before the invasion, indeed the highest for decades (illustration 1).

Artificially halting the economy through lockdowns and then balancing the impact through stimulus programs was possible through increasing money supply while accepting a “temporary” increased level of inflation. While stimulus checks could be printed, missing oil, gas, wheat, and fertilizer cannot be “printed” into existence. Deliberate fiscal and monetary action are helpless against the commodity crunch triggered by the Russo-Ukrainian war in 2022. Filling the supply gaps requires investments into reconstruction and infrastructure, which will take considerably more time than its destruction took. At the same time, record-high inflation has debased fiat currencies, making it less affordable to buy scarce commodities from foreign powers. What will happen to our money?

Zoltan Poszar argues for a new monetary era emerging4. The era of 1948-1971 (Bretton Woods I) was shaped by gold-backed currencies and the era from 1972 until today (Bretton Woods II) was shaped by treasury-backed currencies. He argues that due to the events in 2022, the new monetary era, which he calls “Bretton Woods III”, will be shaped by gold- and even commodities-backed currencies. In one sense, this will revert the monetary system to a pre-WW2 time, in which the potential of governments and (central) banks to increase the money supply was much more restricted. In the new era, he also sees a new digital commodity emerging and playing a role “if it survives until then”: Bitcoin.

Throughout 2022, the FED and the ECB were desperate to demonstrate that inflation was not an issue or “only temporary”, and that they are in control of the dynamics and on track to push it back to the long-term normal of around 2%, a coincidental and arbitrary number in case you did not know[5].

However, how credible is this claim? If the governments of these central banks were financially sound and in good shape, one could think, okay, it is tough, but they might manage. But the governments are not in good financial shape at all.

Predictions

Inflation will not reach 2% again anytime soon, maybe never under this currency regime

The flight to safety will go to scarce commodities and even commodity-based currencies

At least one international trade between countries, most likely on an essential commodity, will be settled in Bitcoin

Fiat currency and national debt

Fiat currency is created either by a central bank printing it or by any bank, central or commercial, making a loan to somebody. None of these modes of creation are linked to actual economic activity, the generation of value through a product or a service. In other words: every dollar, euro, franc you have in your wallet is the debt of somebody else in the system. Therefore the tendency of having too much money compared to the economic output of a nation. This excess in money supply devalues the money, which we call inflation. However, the interest rates banks, central or commercial, demand from their creditors, have not been created. As every creditor must pay interest in addition to the principal of their loan, they inevitably take it from another creditor’s principal. Thus, the debt-based money system is under constant pressure because all creditors chase to repay their principals plus interest while only the money for the principals has been created in the first place... That is why fiat money systems over time tend to put all players, individuals, companies, and governments into debt.

The term “debt spiral” is quickly explained. Imagine, you are in debt and are unable to pay back. A creative solution is to just borrow more and use it to pay back. In other words: you repay short-term debt by accumulating more debt long-term. Once started, you can only escape if your income drastically increases, or your debt gets reduced. If not, the situation is just spiralling downwards from here...

Companies and governments can fall in a debt spiral in similar ways. Companies that are unable to cover their debts beyond interest costs with current operating profit over three consecutive years are called “zombies.” A recent Kearney[6] study estimates that nearly 5% of all listed companies around the world are zombies (+250% since 2010). Based on a sample of 70’000 companies, their projections yield that a 50% increase in interest rates would push that figure to 17%, and a doubling would result in 38% zombies – more than a third of all listed companies! The study estimates that nearly $0.5T of capital is misallocated this way and at a “significant risk of default.”

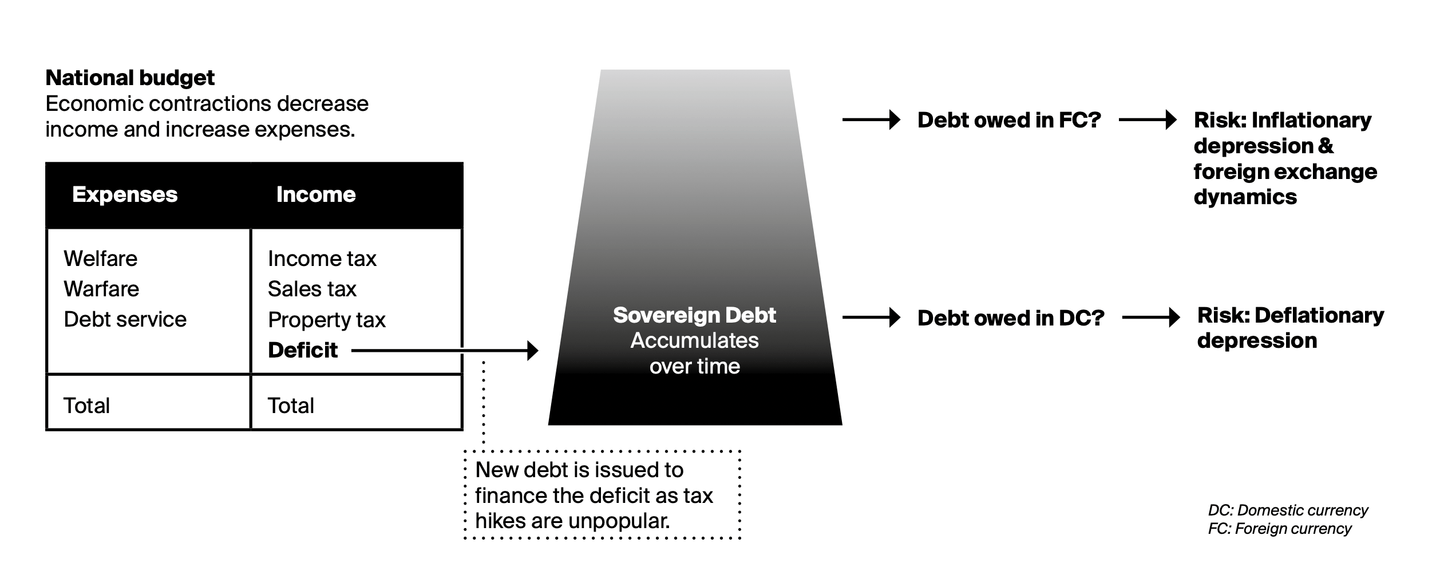

Governments create deficits if their expenses for welfare and warfare (and debt service) are higher than their income from taxes (Illustration 2). While overspending is the obvious cause for deficits, an economic contraction can impact the income side and create or exacerbate a deficit. As budget deficits accrue over time, sovereign debt is accumulated[7]. The crucial question for policy makers is whether the sovereign debt is predominantly owed in foreign (FC) or domestic currency (DC).

If owed in FC, the government finds itself in a tough spot because to repay it needs to buy FC using their own DC, which must be earned by the domestic economy first and be available in the form of tax money before it can be spent. As a result, the FC appreciates because of increasing demand and the DC depreciates in value. If the economy now contracts in that scenario, the FC inflows into the country slow and credits contract. That means liquidity and lending dry up while the DC depreciation produces inflation. This dynamic may lead to what Ray Dalio calls an inflationary depression[8].

If the sovereign debt is owed in DC, the government is in a somewhat easier situation as the central bank can monetize the government debt by paying with new currency. However, as there is no additional economic output backing the additional currency, the DC depre- ciates in value. If the economy now contracts in that scenario, the central bank can “stimulate the economy”, i.e., reduce interest rates to expand domestic credit. This effect dissolves when the interest rate reaches 0% - as was the case in the US and EU in 2019-2021 (c.f. illustration 2). Economic contraction then shrinks income and raises debt burden, eventually producing forced selling and defaults – but no currency issues. This dynamic may lead to what Ray Dalio calls a deflationary depression.

For those countries that have their debt denominated and owed in domestic currency, the matter is much simplified. The debt can be monetized: the government can issue debt instruments in domestic currency, which are bought by the central bank by increasing the domestic money supply. Thus, the governments do not need to raise taxes and the domestic economy does not need to earn the money first.

The United States has this “exorbitant privilege” (Charles de Gaulle) of hosting the global reserve currency, which is in almost constant demand by most other governments. They can “export” their inflation. There- fore, one could assume they would be the last nation to be overindebted.

Let’s look at some numbers. By 30 November 2022, total US sovereign debt[9] amounted to $31.4T. That is over 5 times the 2022 national budget of $6T, which already includes a deficit of $1.4T (~25% of budget)[10].

The US Congressional Budget Office revealed that interest payments alone (!) amounted to $0.4T (1.6% of GDP) in 2022 and projects a rise to $1.3T (3.3% of GDP) by 203211. Just to keep the debt level steady over the coming decade, US citizens and businesses face a total interest payment burden of $8.1T.

Illustration 3 shows the debt-to-GDP ratio for selected Western countries, which has been trending upwards in all, except Switzerland. The Great Financial Crisis[12] marks the pronounced increase in 2008 and the beginning of the Great Lockdown[13] the sudden spike in 2020. While, in 2008, government spending focused on bailing out failing banks, in 2020, it focused on stimulus programs for various businesses and citizens. In both cases, sovereign debt grew by increasing the money supply. The United States saw record-high domestic inflation in 2022 (c.f. illustration 1) following a record-high debt-to-GDP ratio of 137% in 2021 (c.f. illustration 3). A debt-to-GDP ratio above 100% means that a nation’s economy is not able to pay off its debt within one year if the entire GDP would be devoted to it.

What does the aggressive series of seven federal fund rate hikes[14] by the Federal Reserve in 2022 mean for US sovereign debt in 2023 and beyond? The dilemma is that to counter high inflation, higher fund rates are needed. However, higher fund rates will increase the burden of debt service even further.

Which of the three options will the US government choose to reduce sovereign debt (c.f. illustration 2): raise income through tax increases, reduce expenses through cutting welfare and/or military programs[15], or more deficit spending? While the first two options are very unpopular among voters and politicians (and strategically sensitive in the case of defense and current geopolitics), there is not much room left to maneuver: the series of rate hikes will have to come to an end and reverse as monetization of debt will have to continue. An aggravating factor is the fact that the real interest rate – the effective rate after deducting the inflation rate – is negative. Generally, investors buying sovereign debt through government bonds accept that a risk-free investment has only a low yield. But now it is negative and will remain so until the regime of high inflation and low interest rates changes.

Two final observations: first, in 2022 central banks around the world bought 400t of gold in Q3 alone (+340% YoY) and a total of 673t until 1st November – the highest annual total since 196716. Second, during the 14th BRICS Summit, Russia’s president announced that the BRICS nations (Brazil, Russia, India, China, and South Africa) intend to develop a “new global reserve currency” based on their sovereign currencies to “address the perceived US hegemony of the IMF”[17]. BRICS is currently representing 42% of global population and several nations are considering joining BRICS: Argentina, Iran, Saudi Arabia, Egypt, and Turkey are at different stages of the process[18].

We made this lengthy detour on inflation, debt, GDP, and fiat currency as we believe this extraordinary global situation will stay with us for 2023 and much beyond. What will this mean for the US economy and its trade partners? Which foreign countries have US Dollars as national reserves or directly depend on the USD because they are dollarized? Will more countries discover Bitcoin as “pristine collateral and reserve asset”[19] and even follow in the steps of El Salvador and make Bitcoin (secondary) legal tender in their country?[20]

In summary, highly indebted nations are between a rock and a hard place: they need to increase and sustain high interest rates to destroy demand so the inflation rates can decrease. However, the more they stick to this “hawkish” monetary policy, the more their own governments suffer from increased, unsustainable debt servicing cost with no easy solution in sight. Or is there?

Are CDBCs governments’ escape hatch?

Would it not be much easier to simply change an algorithm to adjust in real-time the money supply, funds rates, and optional stimulus packages, taxation, and other parameters for the whole economy at once? What sounds like a utopia for central bankers may come true with Central Bank Digital Currencies (CBDCs).

Activities around CBDCs have picked up pace during 2022. The CBDC tracker[21] of the Atlantic Council currently lists 119 projects, of which 11 are launched, 17 pilots, 33 in development, and 39 in research. A selection of countries to watch in 2023 is listed in Table 1 below, including recent updates that the tracker may not have yet picked up.

Interbank (type “wholesale”) CBDCs will deliver to central banks and governments the typical benefits of going digital, e.g., higher speed, lower cost, leaner processes, etc. without many down sides. Citizen-facing (type “retail”) CBDCs would give central banks for the first time a direct interaction channel to citizens and businesses, circumventing the banking system on which the central bank had to rely on for executing its policies.

Considering the precarious macro situation described above, it is important to understand what central banks and governments would be able to do with CBDCs. Above all else, digitizing a sovereign currency does not change the role of the issuing government and central bank in any way. Thus, the management of monetary supply and control over monetary policy will continue to rest with the central bank, no matter the jurisdiction. Implementations will almost certainly not put a focus on decentralization as this presents a conflict of interest with the requirement to stay in control. However, shaped by differing political views, the design of privacy protection may differ widely across jurisdictions. In fact, privacy preservation may turn out to be the key differentiator between competing CBDCs in the future.

The US OSTP feasibility study referenced in Table 1 expressly states that it does not give any recommendations on the pros and cons of technical designs. It reveals, however, that the US policy objectives that frame the design contain several profound conflicting goals. A few examples[29]:

- Preserving monetary policy-making and keep- ing control

- “Support US leadership in the global financial system, including the global role of the dollar”

- “Minimize energy use” and “improve relative to the traditional financial system”

- Promotion of AML compliance vs. protection of privacy and human rights.

The crucial insight for retail CBDCs is that a central bank could implement monetary policy directly. On the spending side, this may range from paying out stimulus checks, basic income, or other forms of “helicopter money” directly to citizens[30]. On the income side, taxation can be personalized and unpopular policies like, e.g., currency debasement, interest rates, expiration dates, etc. could be implemented at a much finer granularity than ever before[31].

The opportunity for central banks and governments and the danger for citizens and businesses lies in what I termed “surveillance monetarism[32].” While the term “surveillance capitalism” (Shoshana Zuboff) describes the mechanism by which big tech companies (“FAANG”) can extract value using surveillance methods based on large- scale data collection and analytics of users, “surveillance monetarism” will allow governments and central banks to micro-control citizens using surveillance methods based on complete financial data collection and analytics[33]. As the China Social Credit system exemplifies, governments differ from tech companies. By the powers vested in them and using the financial data history, they can directly punish or reward behavior: travel prospects, employment, access to funds and financial services, etc[34].

What prevents other governments from implementing similar systems? Hardly any government will come up with a proposal to monitor its citizens from day one, but enough arguments like anti-terrorism, illicit behavior, financial market stability, etc. will be available to justify technical designs that in principle allow surveillance – even if only in the future.

The answer from the DeFi space to CBDCs is stablecoins. Although their merits are undeniable – they offer “stability” in fiat terms plus all benefits of digital tokens like global transferability, speed, etc. – they have their downsides, too[35]. The major event in 2022, and the only major collapse of a DeFi protocol in 2022, was the collapse of the algorithmic stablecoin UST caused by the hyperinflation of Terra LUNA. The less-than-robust stablecoin algorithm proved vulnerable to arbitrage attacks as soon as the peg went too far off the equilibrium. The immutable algorithm was unable to detect and react adequately to the speculative attacks by humans that caused LUNA to hyperinflate... Algorithmic stablecoins are very hard to design in a robust way, the founder was overdoing the boasting of his project and the space will need deep introspection before investors fund the next algo-stablecoin experiment.

However, in general collateralized stablecoins performed quite decently in 2022: they turned out to be useful onramps to crypto in inflation-ridden countries like Argentina, Nigeria, Türkiye, and Venezuela[36]. While none of the reoccurring concerns about insufficient collaterals materialized for any of the major stablecoins, regulators remain on alert on this obvious competition to their fiat currencies[37].

Predictions

Macro/Debt situation may increase the pressure to speed up introduction of CBDCs.

So, governments keep pushing but central banks will not launch anything major in 2023.

All together now: CeFi is not DeFi!

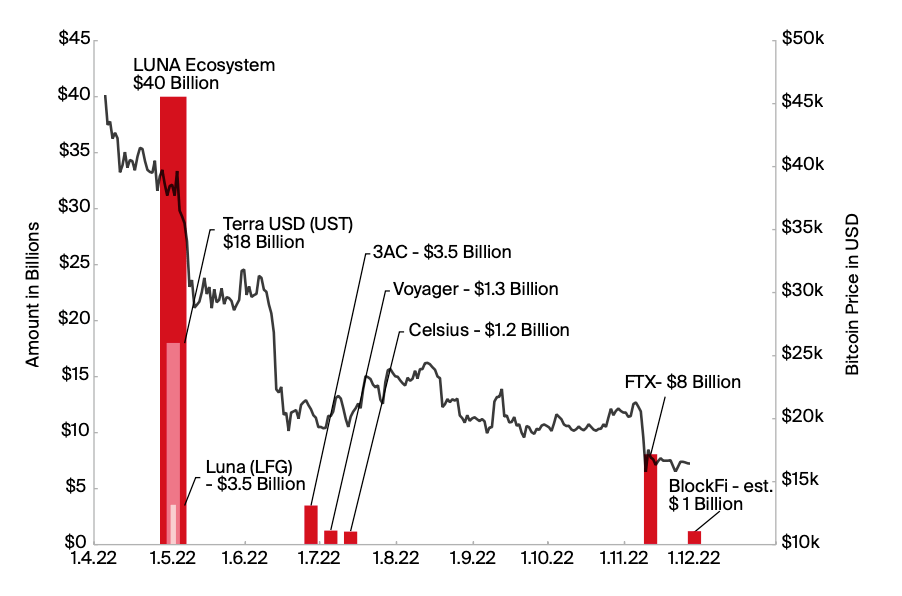

As if the macro situation and the LUNA collapse would not have been bad enough in 2022, the crypto space had to deal with a regrettably long series of collapses that made clients lose billions of funds and hurt the reputation of the entire industry. The too long series of CeFi shenanigans that followed in the months after LUNA caused contagion again and again until year end and into 2023. The first wave consisted of 3 Arrows Capital, Voyager, and Celsius and the final wave of 2022 were the revelations of FTX, which took scam, bankruptcy and fraud to a whole new level (illustration 4).

investment strategies adhere to risk policies, and established management practices are applied to minimize risks. Traditional Finance (TradFi) and regulators had the opportunity to learn this over a century to amalgam- ate it into a set of useful financial regulations that are mostly adhered to, sometimes ignored and sometimes wilfully disregarded. CeFi is simply TradFi with digital assets and deserves similar regulation. In contrast, DeFi is transparent code that can be expected to remain unchanged during an investment.

The CeFi meltdown provides several learnings: investors should learn that CeFi reintroduces counterparty risks that DeFi protocols aim to remove in the first place: the risk that the other party in a deal may not fulfil its part and may default on their obligation. While DeFi carries risks around smart contracts and needs care because code has only limited flexibility to react to extraordinary market volatility, it offers much more transparency: smart contracts can be audited, transactions can be traced on the blockchain and thus the evaluation of exposure and leverage of oneself and potentially other players is much simpler.

Regulators do hopefully learn that focus is to be put on human behavior rather than technology. The reason is that “CeFi” implies an underlying company. With a company, investors need to trust the team to know what they are doing, and their honesty in all aspects of the business: funds are invested as advertised, not lent out in misleading terms – and not stolen (duh!). Furthermore, investors need to ensure risks are clearly communicated, investment strategies adhere to risk policies, and established management practices are applied to minimize risks. Traditional Finance (TradFi) and regulators had the opportunity to learn this over a century to amalgamate it into a set of useful financial regulations that are mostly adhered to, sometimes ignored and sometimes wilfully disregarded. CeFi is simply TradFi with digital assets and deserves similar regulation. In contrast, DeFi is transparent code that can be expected to remain unchanged during an investment.

The loss in trust caused by too many bad or naive actors who were trusted with too much client funds to literally gamble by rehypothecating tokens against other tokens to no end, is enormous and will set back the space for quarters if not years.

Code committed no crime. FTX and cryptocurrencies are not the same thing. FTX was opaque, centralized, and dishonest. Cryptocurrencies usually are open source, decentralized, and transparent.

US senator Patrick Toomey, during US Senate hearing on FTX collapse

Predictions

Contagion in CeFi is not over yet and many funds will not return to exchanges in 2023.

Move by US regulators to require large scale registration of tokens they deem “securities.”

Eye on Bitcoin

For the first time, Bitcoin has experienced a recession- ary macro environment in 2022. A dim macro-outlook and CeFi shenanigans presented the perfect storm to see how Bitcoin would react. Over 2022, the USD price of bitcoin dropped by 65.5%, but Bitcoin refused to die for the 467th time[38] with the latest obituary coming from the ECB in November 2022[39].

On a more serious note, it could have been much worse. Bitcoin dropped 65.4% in 2022, in line with the entire crypto market (65.7%) and remained in a stable range under $20’000 during the last months of 2022. A few comments to give a bit of context to these numbers:

First, drawdowns in this order or higher (80%-90%) are nothing new or uncommon for bitcoin[40]. That’s it. Even in the absence of all the macro pressures and the LUNA/CeFi shenanigans, Bitcoin could have been falling to a similar level just because it evolves in cycles, and it happened before. Our take: the world has yet to find the actual price, or better, value of Bitcoin, because, as we never had an asset like this before, we have no way of knowing in advance. The market figuring this out over time implies large volatility and only gradual price discovery. At one point we will know what affects the value of Bitcoin, but 2022 was not the year we figured it out for good.

Second, the lamentation about Bitcoin being correlated to (tech) stocks for three quarters in 2022 is short- sighted for similar reasons. 2022 was the first year that Bitcoin’s cyclical drawdown coincided with a drawdown across all markets, as the “everything bubble” we discussed in last year’s Outlook is morphing into an “every- thing burst” this year. The consequence? Everything is correlated because everything falls during such broad market downturns. The 2022 class of market entrants was hurt for sure, but long-term investors seem to just wait and hold out according to Glassnode analyses[41].

The extraordinary markets in 2022 caused US stocks and bonds both to turn negative within the same year! A situation that seems to contradict the established wisdom that both asset classes act as mutual counterweights and have therefore formed the basis of the famous balanced fund[42] portfolio (e.g., “60/40”). According to data from New York University[43], only four out of the last almost 100 years show this constellation: 1931 (S&P -44%, Bonds -3%), 1941 (-13%, -2%), 1969 (-8%, -5%), and 2022 (a double whammy: -18%, -18%). Dylan LeClair argues that within 2 years of each of the four, the “US defaulted on its debt[44]”, not explicitly but de-facto. We cannot go into deep analyses here, but let’s flag a few highlights to get a feeling of the circumstances of these times past:

- In 1933, President Roosevelt issued Executive Order 6102[45] confiscating private gold: citizens had to sell their gold at a price of $20.67 per ounce to the Federal Reserve. One year later, the Gold Reserve Act fixed the new gold price at $35 an ounce, effectively allowing the Federal Reserve to increase the money sup- ply without violating the Federal Reserve Act that required 40% gold backing, a limit nearly reached during the Great Depression.

- In 1941, the US entered WWII, which was financed by raising taxes and issuing war bonds. By 1943, two-thirds of the economy was integrated into war production[46].

- In 1971, the so-called Nixon shock, a series of measures in response to inflation, were initiated by President Nixon. The most consequential one was presented on a Sunday evening: Nixon declared to “suspend temporarily the convertibility of the dollar into gold or other reserve assets”. This statement unilaterally ended the post-war Bretton Woods Agreement of 1948 and ushered in the era of fiat currencies that are not backed by gold anymore[47].

- For 2024, ... we probably do good in preparing ourselves to expect extraordinary economic situations that we even may not have experienced in our lifetimes yet because the economic parameters of 2022 have been no smaller outliers than the ones described above.

Third, there is a less obvious connection between the LUNA/CeFi collapses and the Bitcoin price performance. To a significant extent, what was burned last year was “paper bitcoin”, IOU bitcoin, or “fake bitcoin.”

Bitcoin will not be a great store of value if most people are buying fake bitcoin.

Jameson Lopp on Twitter, 13 November 2022

What does Lopp mean by that? Paper bitcoin means bitcoin you own but are not under your control. The “not your keys, not your coins” mantra resurfaced when FTX, the Luna Foundation Guard and other “safe custodians” turned out to not be so safe after all. The core problem is that it requires trust, that your bitcoin is not repurposed for other investments while you entrust the custodian with them. As this repurposing is the source of any yield you could ever get on bitcoin, it is also attractive to entrust a third party with your bitcoin. Many bitcoin were involuntarily sold in 2022 because the DeFi institutions who custodied them (as reserves or as client funds), had to sell them to redeem collateral, other tokens, that their clients enquired to withdraw, or to cover for losses in other investments. These leverage dynamics created additional, and in a sense unnecessary, sell pressure on Bitcoin. Without the maniac search for yield on Bitcoin, much less of this pressure would have been generated during the market downturns.

Why? Because Bitcoin is “money” and money does not offer yield because its purpose is to store value in uncertain times and be a medium of exchange in better times. In addition, holding a bearer asset like Bitcoin does not have counterparty or other risks except price volatility measured in fiat currency.

Despite all these pressures – from war, inflation, rate hikes, DeFi mistakes in large stablecoins, CeFi shenanigans – the Bitcoin network just kept chugging along: no bridges hacked, nobody had to put the “blockchain into maintenance mode”, transactions were processed every ten minutes on average and fees were bearable throughout the year. In fact, security of the network in the form of hashrate hit five all-time highs in 2022 and the number of nodes as an indicator of decentralization remained stable around 15’000 public nodes (and an unknown number of private nodes on the TOR network).

Short-term investors or recent entrants (since “peak bull” in 2021) have experienced quite a bit of pain – like everybody who joined just before a “-80%” period in the history of Bitcoin. If you think the fundamentals of Bitcoin are intact, and we think they are, then a long-term perspective does this “money experiment” more justice. For such a perspective and in such volatile times, qualitative information about ecosystem developments is more telling for the future than historical charts. So, let’s see...

To watch: nation-state adoption. While user adoption of Bitcoin has slowed in the 2022 bear market, it remains above pre-bull market levels with the top 20 adoption countries covering all continents[48].

After El Salvador in Central America (06.09.2021), the Central African Republic (CAR) is the first country on the African continent that introduced Bitcoin as legal tender on 23.04.2022. Both countries depend on a for- eign currency: while El Salvador is dollarized[49], the CAR is using one of the two CFA franc (Franc of the French Colonies in Africa) currencies that are in use in 14 former French colonies in Western and Central Africa[50]. As the CFA franc is pegged to the Euro, these countries struggle with economic planning as the monetary policy for them is made in Brussels and the Euro peg makes exports more expensive as they cannot actively manage adequate exchange rates. No wonder, the Machankura project enables Bitcoin Lightning transfers via SMS across eight African countries to counter the lack of internet connectivity[51].

Despite the bear market, El Salvador is continuing its Bitcoin journey and holds 2480 bitcoin at time of writing[52]. On November 17, 2022, the president announced that the country is buying one bitcoin every day. Addressing the primary criticism that citizens have been hit unprepared by the legal tender law in 2021, the NGO ‘Mi Primer Bitcoin’ has started to educate 11’000 students on Bitcoin in 2022, with plans to extend the offering to 250’000 in 2023. They also created a school curriculum in which students can receive a “Bitcoin diploma” in several public schools, with the aim to reach all schools in the country.[53]

In May 2022, El Salvador hosted the annual meeting of the Alliance for Financial Inclusion to discuss Bitcoin for nations with 32 central banks and 12 financial authorities in attendance from a range of countries: Paraguay, Haiti, Honduras, Costa Rica, and Ecuador in Latin America, Angola, Ghana, Namibia, and Uganda in Africa, and Bangladesh, Palestine, and Pakistan in Asia[54].

Since December 2022, Bitcoin is recognized as a means of payment and investment asset in Brazil, with the law going into effect in summer 2023[55]. While the law does not render Bitcoin or other cryptocurrencies legal tender, the greater regulatory clarity may encourage businesses to explore it more closely – Brazil is currently the top 7 country in crypto adoption[56].

A second aspect of nation state adoption would be to adopt Bitcoin as a part of the national currency reserve strategy. No country has yet publicly spoken about using or considering the use of Bitcoin in that way – although you could argue El Salvador’s Bitcoin stack is more of a reserve than investment money for the time being. In a working paper from Harvard, Matthew Ferranti explores the potential of Bitcoin to serve as an alternative hedging asset compared to gold, which was bought 2016-2021 by countries who faced a higher risk of US sanctions[57]. Coming from a student of Kenneth Rogoff, Harvard economist and Bitcoin critique, it was a bit of a sensation. A group of shareholders of Swiss National Bank also suggested in the 2022 general assembly that the SNB prepares for taking on bitcoin as part of its reserves. Reserves in bitcoin could not be confiscated nor otherwise tampered with as is possible with fiat currencies. For example, Russia’s foreign currency reserves including gold were frozen, i.e., not accepted anymore for debt payments after Russia was also disconnected from SWIFT[58].

To watch: green energy contribution. Energy grids pose delicate management challenges. Energy supply must follow demand changes as instant as possible to prevent blackouts or waste of excess energy. The grid is therefore composed of a range of energy producers: from slow reacting but large base load providers up to very fast, but usually small peak load providers. For the same reasons, the same flexibility is desired on the demand side. In tight situations, grid operators ask large industrial consumers to switch parts of their machines off. Again, the larger the machines, the slower they are in reacting.

This is where Bitcoin mining comes in. In the words of the Bitcoin Policy Institute[59]: “Proof-of-work mining has complex and dynamic effects on global energy systems. While mining uses substantial amounts of electricity — currently 0.18% of global energy — it is price-sensitive, interruptible, adjustable, and location-agnostic, which pairs well with intermittent renewable energy sources like wind and solar, as well as stranded sources of energy like waste methane.”

The electricity consumption of Bitcoin is substantial, however, considerably less than of those industries relevant to the fiat monetary system: military-industrial complex[60] (30-60x of Bitcoin), banking/finance (22-50x of Bitcoin), and gold mining (2-5x)[61].

The properties of Bitcoin mining make it uniquely qualified as a location-agnostic, very fast-reacting and yet large energy consumer to support the stabilization of energy grids. Mining can be leveraged in three ways to help decrease emissions of existing fossil sources of energy and increase the fraction of renewable sources of energy.

- First, to prevent blackouts, energy grids tend to overproduce. In the case of fossil sources of energy, this not only leads to energy waste but also unnecessary additional emissions. Bitcoin mining can help to reduce emissions by mitigating methane and CO2 emissions from landfills and flaring/venting of excess gas at refineries. Instead of emitting into the atmosphere, they are used to generate power to run a mining operation. Bitcoin mining helps reducing emis- sions and supports the financing of such oper- ations[62].

- Second, grids are increasing the fraction of renewable sources[63]. As renewables are inter- mittent sources (sun does not shine always, wind does not blow always), they contribute to grid volatility, thus making it harder to keep grids stable compared to fossil power plants that provide stable base load. In such situations, Bitcoin mining can help finance the increase of renewables, location-agnostic, while decreasing volatility and preventing blackouts[64].

- Another large source of clean energy that deserves a bigger role in the energy transition according to the International Energy Agency is hydropower[65]. Bitcoin mining can support the financing of more hydropower operations[66].

In one sentence: Bitcoin mining is evolving as a self-financing global search mechanism for the cheapest sources of energy. Since mid-2021, most new renewables undercut cheapest fossil fuel on cost[67]. Hence, we can expect an increasing contribution of Bitcoin mining to a global path of a renewable energy future.

So, although the energy debate on Bitcoin in 2022 has been dominated by energy shortages because of inflation in TradFi and Ethereum’s switch to Proof- of-Stake in crypto and the EC contemplating a ban on proof-of-work, regulators and activists need to learn to understand and appreciate Bitcoin’s unique potential to contribute to a green energy future. If you hear ‘Bitcoin steals energy from poor citizens and boils the planet’ you may respond that lazy research or wilful spread of misinformation are detrimental to crucial progress, we all need to mitigate climate change – and to fix our broken monetary system.

A closing remark on the “ESG” narrative. While the core idea of caring about the planet is in the utmost interest of humans, the way ESG in TradFi has been implemented does not bring us there. The twisted narrative got a deserved backlash in 2022 as widely reported in TradFi news media[68]. Rather than changing business operations, “ESG” is facing blame as a misused instrument for gatekeeping companies in (or out) of indices to become investable (or not) for institutional investors by introducing criteria that sound noble but have nothing to do with a company’s performance (e.g., Tesla being kicked from the DJ Sustainability index).

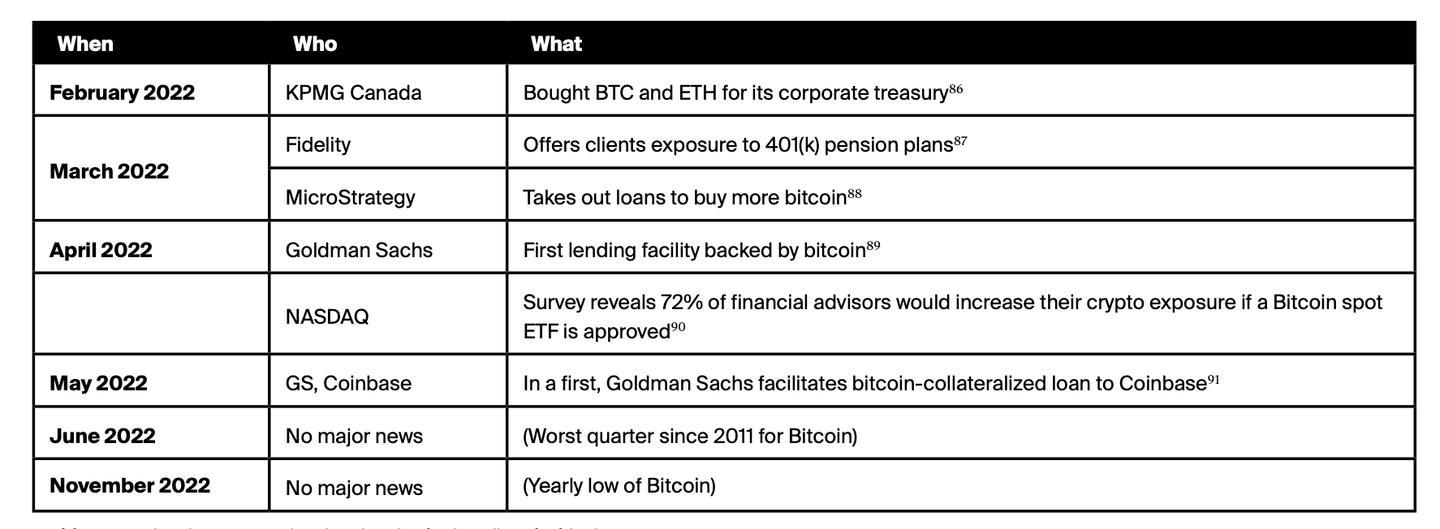

To watch: institutional adoption. Although crypto news in 2022 was dominated by noises of the now dis- solved band “LUNA & the CeFi Collapses feat. FTX”, professional institutions continued to seriously engage with Bitcoin and the crypto space. Throughout 2022, the overall amount of Bitcoin in corporate treasuries (plus a few government treasuries) remained stable above 500’000 BTC[69].

At least during the first half of 2022, some institutions showed their continued engagement publicly. Some examples are in Table 2. In December 2022, MicroStrategy announced Lightning-based products and services in 2023[70]. While most companies in the Lightning space focus on technical improvements or individual solutions, MicroStrategy’s integration offering to get Lightning infrastructure ready “in an afternoon” for companies may find a largely untapped market given how early Lightning payments still are.

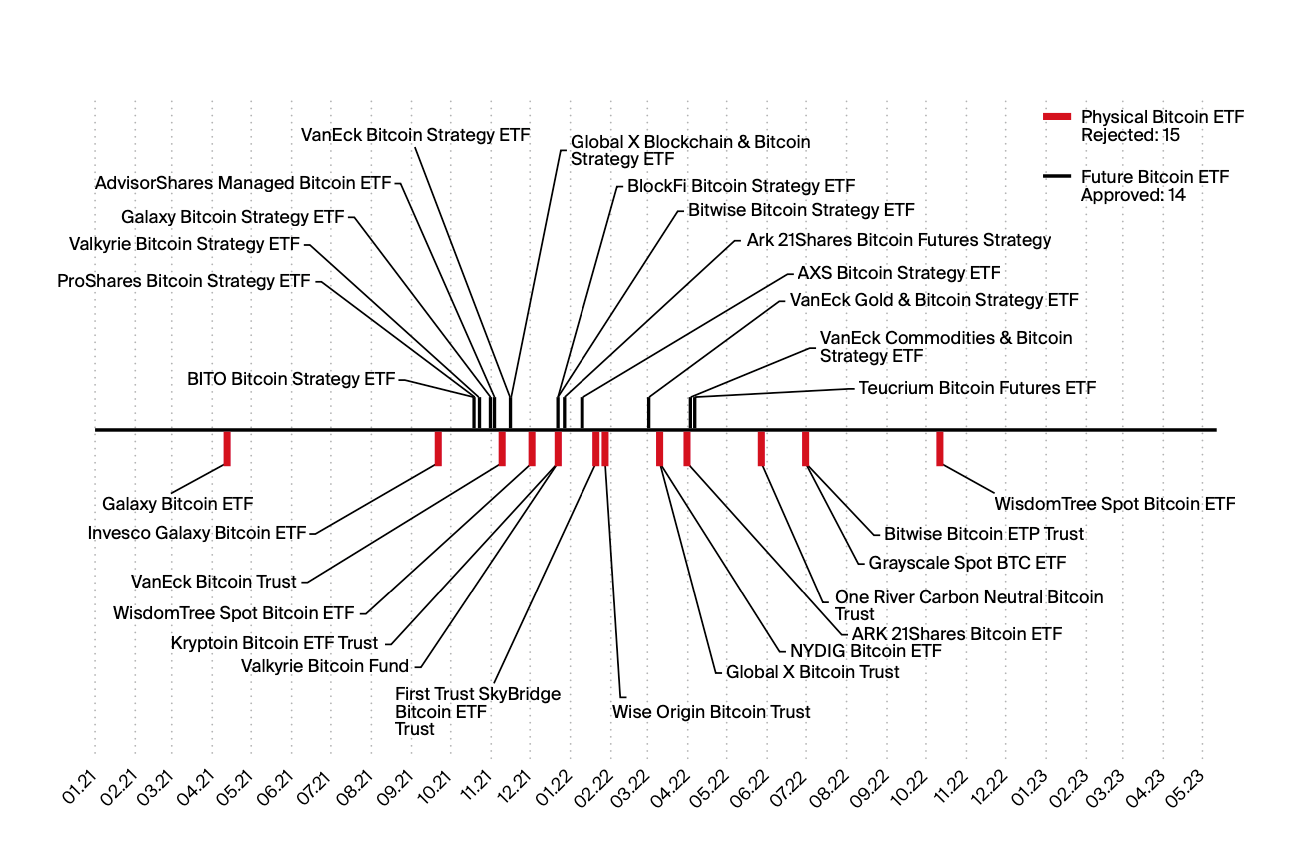

Creating bankable products within the confines of TradFi like ETFs, ETPs, etc. has been one strategy for financial service providers to offer clients exposure to crypto. The regulatory situation with Bitcoin in the US – the largest financial market – is curious in that regard. While 14 futures-based Bitcoin ETFs (including one to short Bitcoin) have been approved by the SEC since beginning of 2021, yet not a single of the 15 applications for a physical Bitcoin ETF have been approved (illustration 5). Honi soit qui mal y pense[71].

The question is: Why is that? The main argument given by the SEC is that the Bitcoin markets can be easily manipulated. If that is the case, then it is not quite clear why that is different to future-based ETFs. Why allow one and not the other? One could even make the argument that a spot ETF is less risky and volatile than one based on futures. Plus, futures are fully dependent and correlated with the physical underlying, contrary to cash-settled derivatives.

Let’s assume for a moment that Bitcoin would become this “superior form of money”, as the maximalists propose, that would compete with fiat currencies and thus be perceived as dangerous by issuers, i.e., governments and (central) banks. What subtle, non-obvious ways would exist to discourage the use of Bitcoin aside official bans, withdrawal limits at ATMs, transaction limits, registration of wallets, and similar ideas for explicit regulation? Having seen the measures taken about gold in 1933, 1943, and 1971 (see above), the idea that counter measures would be taken against a competing form of money is not entirely outlandish.

Let’s start with a news piece crypto people may have overlooked as it sounds like some unrelated, obscure TradFi problem: in August 2022, gold traders by JPMorgan and other banks were found guilty of “gold spoofing”. During an 8-year-period(!), they made use of the “power to move the market, the power to manipulate the world- wide price of gold.” That is after JPMorgan, the largest US bank, was fined to pay $920m to settle spoofing allegations in 2020 – the largest fine for any financial institution since the Great Financial Crisis 2008[72]. All in all, ten traders from different banks were convicted – one of the biggest cases of the Justice Department.

Gold spoofing is the manipulation of the gold futures market by creating a false impression of demand, as measured by trading volume. It is done by submitting fake transactions and withdrawing them nanoseconds before an actual transaction can occur, to move the price in the desired direction. What sounds like manipulation was legal until and during the Great Financial Crisis 2008 and only became illegal with the Dodd-Frank Act in 2010[73].

Financial institutions engaging in spoofing just aim for profit without much concern in which direction the gold price moves. Governments, however, have a clear interest that the gold price remains low to protect their fiat currency from (perceived) competition.

So, what if the gold price were suppressed by governments to keep “competition” at arm’s length? That sounds a bit like a conspiracy question, however news outlets like Forbes74 report on it and NGOs like GATA75 have been research- ing this question for decades. More recently, thanks to Wikileaks we know of a diplomatic cable that was sent from the UK Treasury to the US Secretary of State on 10 December 1974. It is one of the only official documents giving merit to this suspicion[76]. The cable was sent a few weeks before the US government allowed citizens to hold gold again – 40 years after Executive Order 6102 banned the private ownership of gold. The cable is important as it suggests that the governments well understood that promoting a (not yet existing) futures market for gold would create price volatility and thus reduce the desire to hold gold in physical form for the long term.

Today, the ratio between physical gold and “paper gold” (futures, options, ETF, gold contracts, etc.) is estimated to be around 1:200 to 1:250[77]. For every ounce of physical gold there are 200+ ounces documented on paper. A dollar-based estimate says some $11T physical gold (of which central banks hold approx. $1T) stand against approx. $200-$300 trillion paper gold[78].

What are the reasons again, why we see so many future ETFs for Bitcoin, but no spot ETF approved in the US? With a Bitcoin futures ETF, the holder is not in possession of “physical” bitcoin but is exposed to an ETF that holds Bitcoin futures. According to Willy Woo and Seb Bunney, “the futures market dictates 90% of bitcoin’s price[79].” While acknowledging the problem, Arman gives two reasons why this dynamic cannot be sustained with Bitcoin versus gold[80]. First, bitcoin is much easier to custody and spend than gold, making it much more likely that investors will physically hold bitcoin. Second, arbitrageurs who sold bitcoin against a contract will eventually want to build up their bitcoin stack again and thus close/sell the contract.

In summary, while the price suppression problem exists, bitcoin holders have more options than gold holders to mitigate it. In the span from 5 November to 26 December 2022, a total of nearly $20B left exchanges: $6B in BTC, $5B in ETH, and $7B in stablecoins[81].

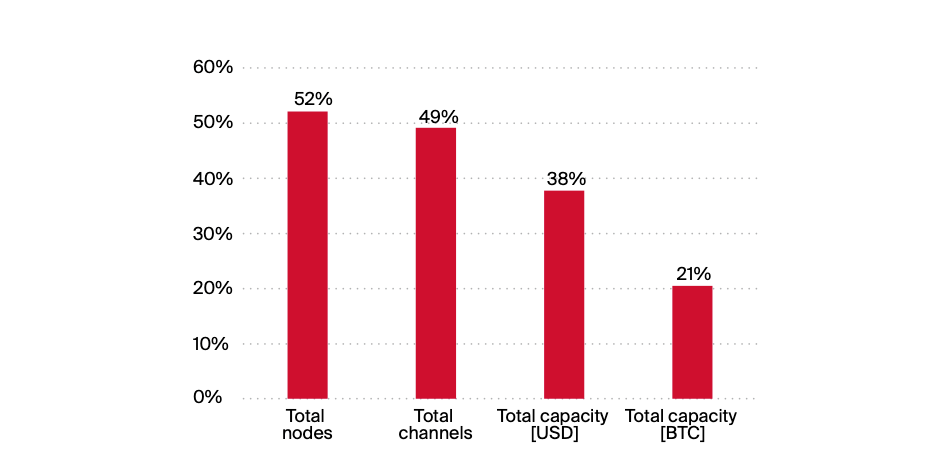

To watch: Bitcoin for payments. Despite the current crypto winter that also affects Bitcoin, the actual growth of the Lightning network has continued as can be seen in Illustration 6. Both the number of nodes and channels rose by approx. 50%. As channels need capacity to run, the overall channel capacity also rose by nearly 40% in BTC terms and 20% in USD terms, indicating an uptake in network usage. Lightning is well suited for small payments because it enables global, instant, extremely cheap transactions without mining and waiting 10 minutes for a block. That is one of the key reasons its uptake across countries in Latin America, Africa and the Middle East is so compelling according to Alex Gladstein[82].

To watch: Bitcoin stablecoins. Lightning Labs, the company behind the leading Lightning client in the market, raised $70M in a series B to develop Taro. Leveraging the Taproot[83] upgrade, which is active since November 2021, Taro will enable application developers to integrate digital assets (aka tokens) alongside BTC in applications both on-chain and via Lightning. Specifically, the company sees Taro as an “important step to bitcoinizing the dollar” by issuing assets like stablecoins. The initiative is addressing feedback from several countries with strong Lightning uptake across Latin America and West Africa that says adding stablecoin assets would expand financial access for many communities[84].

To watch: Bitcoin smart contracts. Based on technical ideas by former Bitcoin core developer Peter Todd in 2016, the company Pandora Core maintains the open- source project “RGB.” With a somewhat broader vision than Taro, the RGB project aims for a generic smart contract system for Bitcoin and Lightning. While not a token protocol, RGB also enables the issuance of programmable digital assets (aka tokens). The key difference to systems like Ethereum is that smart contracts and their data are managed off-chain using “client-side validation[85].”

Both initiatives, Taro and RGB, are raising the bar for what it technically possible on top of the Bitcoin base layer and the Lightning Layer-2, respectively. Such developments will not only further strengthen the use case of Bitcoin as a payment system but put the idea of “Bitcoin DeFi” into the spotlight by enabling a next level of programmability of the Bitcoin/Lightning tech stack.

Predictions

A third nation, most likely from Latin America, will declare Bitcoin (second) legal tender in 2023

A first stablecoin on the Bitcoin/Lightning network will be issued in 2023

A first non-crypto company will start using Lightning for payments in 2023

Final thought

Fiat currencies are in a crisis, the biggest the most. Nations are trying to reduce their dependency on the US Dollar. Expect more volatility as we go through this process of deleverage and unwind in the years to come. This base dynamic will affect all assets classes, TradFi and crypto alike.

Bitcoin, the decentralized peer-to-peer network to store and transfer value in digital form, is working and is as unstoppable as anything else in crypto. How its price in fiat terms will evolve depends on how the growing group of holders perceive it. Given all its properties, for investors with low time preference the trade is asymmetric with upside potential in the long run. You can also just save it, because in past times, money was meant to be a safe haven, particularly for uncertain times.

The author thanks Denis Oevermann for creating all the charts.

Disclosure: at time of writing, the author holds BTC.

- https://www.tradingview.com/symbols/ECONOMICS-EUM2/

- Peter Zeihan, Keynote ECC 2022, https://www.youtube.com/watch?v=UA-jOLF2T4c

- https://www.bruegel.org/blog-post/will-european-union-price-cap-russian-oil-work

- https://www.credit-suisse.com/about-us-news/en/articles/news-and-expertise/we-are-witnessing-the-birth-of-a-new-world-monetary-order-202203.html

- https://www.nytimes.com/2014/12/21/upshot/of-kiwis-and-currencies-how-a-2-inflation-target-became-global-economic-gospel.html

- https://www.kearney.com/financial-services/article/-/insights/the-walking-debt

- https://www.investopedia.com/terms/s/sovereign-debt.asp

- https://www.bridgewater.com/big-debt-crises/principles-for-navigating-big-debt-crises-by-ray-dalio.pdf

- https://fiscaldata.treasury.gov/datasets/debt-to-the-penny/debt-to-the-penny

- https://www.govinfo.gov/content/pkg/BUDGET-2022-BUD/pdf/BUDGET-2022-BUD.pdf

- https://www.pgpf.org/blog/2022/06/what-is-the-national-debt-costing-us

- https://fred.stlouisfed.org/series/DFEDTARU

- https://www.defense.gov/News/News-Stories/Article/Article/3252968/biden-signs-national-defense-authorization-act-into-law/

- https://www.gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-q3-2022/central-banks

- https://economictimes.indiatimes.com/news/economy/policy/brics-explores-creating-new-reserve-currency/articleshow/94628034.cms

- https://www.arabnews.com/node/2127586

- https://www.atlanticcouncil.org/cbdctracker/

- https://www.scmp.com/tech/policy/article/3195744/china-digital-currency-transactions-total-100-billion-yuan-end-august

- https://www.ecb.europa.eu/paym/intro/news/html/ecb.mipnews220916.en.html

- https://www.bitkom.org/EN/Digital-Euro-Summit/

- https://www.coindesk.com/policy/2022/11/29/india-to-start-retail-cbdc-pilot-in-four-cities-with-four-banks/

- https://www.nfcw.com/2022/12/08/380838/central-bank-of-nigeria-limits-cash-withdrawals-to-drive-cbdc-and-digital-payments-adoption/

- https://www.snb.ch/en/iabout/internat/multilateral/id/internat_multilateral_bisih

- https://www.whitehouse.gov/wp-content/uploads/2022/09/09-2022-Technical-Evaluation-US-CBDC-System.pdf

- https://www.whitehouse.gov/wp-content/uploads/2022/09/09-2022-Policy-Objectives-US-CBDC-System.pdf

- https://www.atlanticcouncil.org/cbdctracker/

- https://www.bitcoinsuisse.com/research/theme/privacy-in-the-era-of-cryptocurrencies

- https://link.springer.com/chapter/10.1007/978-3-030-71400-0_1

- https://www.btcpolicy.org/articles/why-the-u-s-should-reject-central-bank-digital-currencies

- https://www.bertelsmann-stiftung.de/fileadmin/files/aam/Asia-Book_A_03_China_Social_Credit_System.pdf

- https://www.bitcoinsuisse.com/research/decrypt/season-2022/un-stablecoins

- https://cointelegraph.com/news/global-inflation-mounts-how-stablecoins-are-helping-protect-savings

- https://www.rba.gov.au/publications/bulletin/2022/dec/stablecoins-market-developments-risks-and-regulation.html

- https://99bitcoins.com/bitcoin-obituaries/, performance figures from TradingView.com

- https://www.ecb.europa.eu/press/blog/date/2022/html/ecb.blog221130~5301eecd19.en.html

- https://www.tradingview.com/chart/JvEkI6g5/

- https://newsbtc.com/news/bitcoin/glassnode-bitcoin-long-term-holder-conviction-not-lost/

- https://www.investopedia.com/terms/b/balancedfund.asp

- https://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html

- https://youtu.be/uBMUGChTp4w?t=604 (5 mins)

- https://en.wikipedia.org/wiki/Executive_Order_6102

- https://en.wikipedia.org/wiki/War_economy#World_War_II

- https://link.springer.com/chapter/10.1007/978-3-030-71400-0_1

- https://blog.chainalysis.com/reports/2022-global-crypto-adoption-index/#top-20

- https://en.wikipedia.org/wiki/Currency_substitution

- https://en.wikipedia.org/wiki/CFA_franc

- https://machankura.com/. A short documentary highlights this and other Bitcoin projects across Africa: https://www.youtube.com/watch?v=d5AvBsxRMYk

- https://nayibtracker.com/

- https://miprimerbitcoin.medium.com/un-a%C3%B1o-incre%C3%ADble-logros-de-mi-primer-bitcoin-en-2022-55d9395ecab8

- https://bitcoinmagazine.com/markets/el-salvador-president-nayib-bukele-announces-countries-to-discuss-bitcoin

- https://bitcoinmagazine.com/legal/brazil-enacts-bitcoin-payments-bill

- https://blog.chainalysis.com/reports/2022-global-crypto-adoption-index/#top-20

- http://med.a51.nl/sites/default/files/pdf/Cryptocurrency_in_Central_Bank_Reserves.pdf

- https://www.bbc.com/news/business-60521822, https://finance.yahoo.com/news/g-7-frozen-russia-assets-222049235.html, https://www.aljazeera.com/news/2022/3/25/gold-russia-ukraine-war.

- https://www.btcpolicy.org/research-categories/mining-energy

- https://bitcoinminingcouncil.com/wp-content/uploads/2022/01/2022.01.18-BMC-Q4-2021.pdf. Factors are calculated lower and upper bounds of 100-200 TWh/year energy use for Bitcoin. See chart "Total Bitcoin electricity consumption at: https://ccaf.io/cbeci/index

- https://www.iea.org/news/renewable-power-s-growth-is-being-turbocharged-as-countries-seek-to-strengthen-energy-security

- https://www.iea.org/reports/hydropower-special-market-report

- https://www.irena.org/news/pressreleases/2021/Jun/Majority-of-New-Renewables-Undercut-Cheapest-Fossil-Fuel-on-Cost

- https://bitcointreasuries.net/

- https://www.bloomberg.com/news/articles/2022-02-07/kpmg-canada-adds-bitcoin-ethereum-to-corporate-balance-sheet

- https://edition.cnn.com/2022/04/26/success/fidelity-bitcoin-401k/index.html

- https://decrypt.co/96313/microstrategy-takes-out-205m-bitcoin-backed-loan-buy-more-bitcoin

- https://www.bloomberg.com/news/articles/2022-04-28/goldman-offers-its-first-bitcoin-backed-loan-in-crypto-push

- https://www.nasdaq.com/articles/majority-of-financial-advisors-want-to-increase-bitcoin-exposure%3A-nasdaq-survey

- https://bitcoinmagazine.com/business/goldman-sachs-partners-with-coinbase-for-banks-first-bitcoin-backed-loan

- https://cointelegraph.com/news/microstrategy-to-offer-bitcoin-lightning-solutions-in-2023

- https://www.bloomberg.com/news/articles/2022-08-10/jpmorgan-precious-metals-traders-found-guilty-in-spoofing-trial

- https://en.wikipedia.org/wiki/Dodd%E2%80%93Frank_Wall_Street_Reform_and_Consumer_Protection_Act

- https://www.forbes.com/sites/greatspeculations/2019/05/20/yes-gold-is-being-manipulated-but-to-what-extent/, also https://www.fool.com/investing/general/2011/09/13/is-gold-being-suppressed.aspx

- https://gata.org/about

- https://wikileaks.org/plusd/cables/1974LONDON16154_b.html

- https://www.usmoneyreserve.com/news/executive-insights/paper-gold/

- https://europhoenix.com/blog/an-upcoming-paper-gold-crisis-by-les-nemethy-and-alberto-scalabrini/

- https://lookingglasseducation.com/what-the-us-government-doesnt-want-you-to-know/

- https://bitcoinmagazine.com/markets/bitcoin-futures-market-explained-price-manipulation

- https://news.bitcoin.com/more-than-19-billion-in-btc-eth-stablecoins-left-exchanges-since-the-onset-of-ftxs-collapse/

- Alex Gladstein, Check your Financial Privilege, BTC Media LLC, 2022.

- https://www.coindesk.com/tech/2021/11/13/taproot-bitcoins-long-anticipated-upgrade-activates-this-weekend/

- https://lightning.engineering/posts/2022-4-5-taro-launch/

- https://www.rgbfaq.com/what-is-rgb