The Post-Merge Ethereum World

20.02.2023 - 10 Minuten Lesedauer

- Ethereum’s transition to Proof-of-Stake in September 2022 was arguably the most significant landmark event in blockchain technology since Satoshi bootstrapped Bitcoin’s genesis block almost 14 years back. A first of its kind, an open-heart surgery on a distributed ledger securing billions of dollars went through without any hiccups, a monumental achievement for consensus and coordination of like-minded individuals across independent researchers, client teams and infrastructure providers.

- The Merge brought a reduction in energy consumption in the range of 99.84 % to 99.99 % almost eliminating its carbon footprint, a significantly reduced net inflation and a lower barrier of entry for users aiming to secure the network. Despite MEV Boost, a first iteration of proposer-builder separation, being utilized to avoid economies of scale and protect decentralization, the transition to Proof-of-Stake and new regulatory scrutiny exposed looming censorship risks across Ethereum’s tech stack. Moving forward, solutions will not only rest on the shoulders of the social layer but also on the comprehensive roadmap. Being around 55% complete post-Merge, it will address issues including security, privacy, censorship-resistance and more.

- A significant part of the roadmap deals with scalability improvements that will unlock the full potential of rollups and streamline Ethereum to a lean protocol. As the Layer 1 narrative loses steam, activity is drifting towards scaling solutions such as Arbitrum, Optimism and Polygon. 2023 will be decisive for promising blockchain architecture paradigms as (multi-)monolithic and modular approaches line up to compete.

The Merge

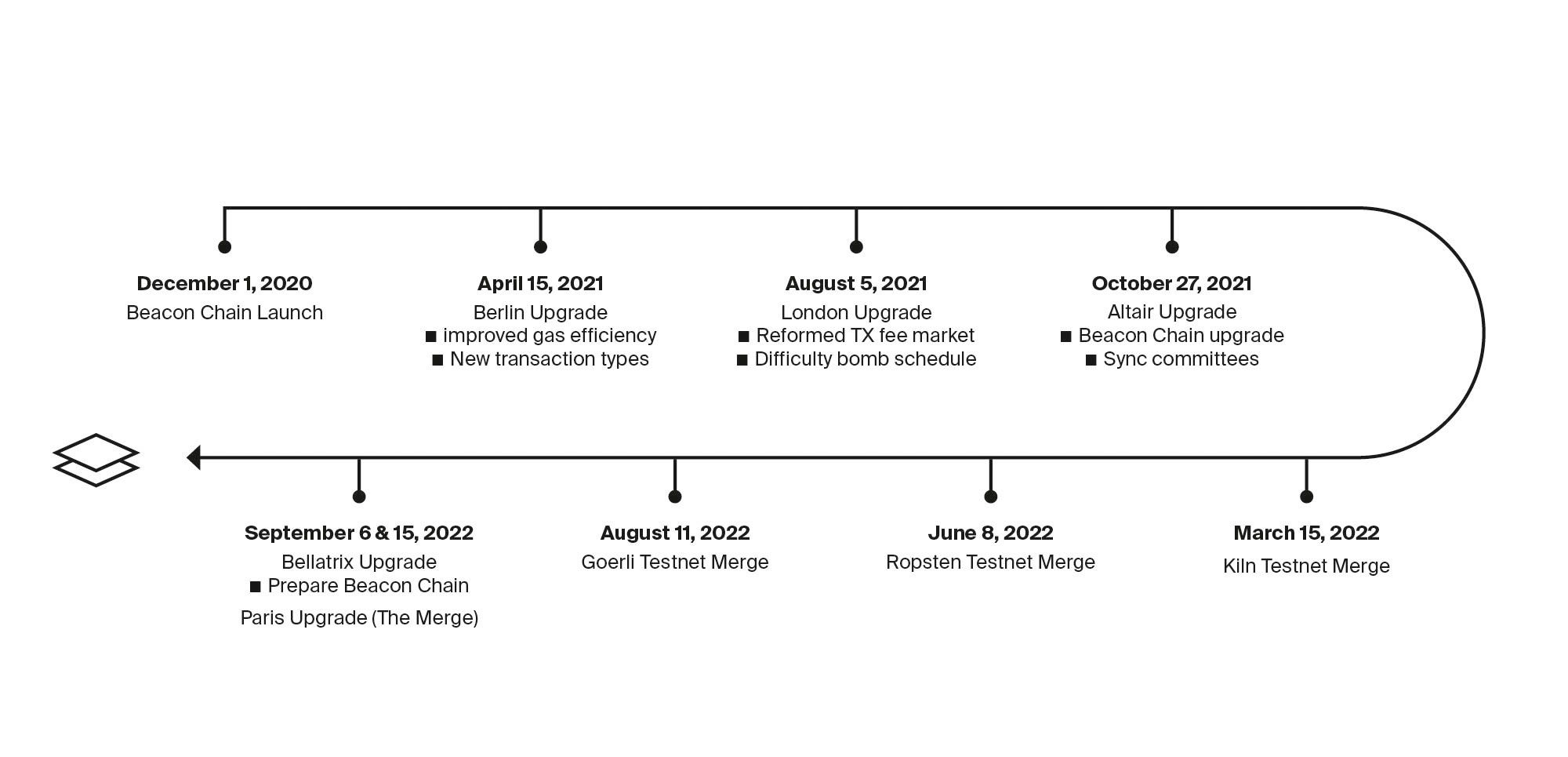

Some years down the road, 2022 will likely not be remembered as the year where flawed stablecoins and most of the CeFi industry blew up but as the defining moment in blockchain history where Ethereum successfully transitioned from Proof of Work (PoW) to Proof of Stake (PoS). With it, a tremendous effort finally culminated since its first proposal in 2017[1]. As the Merge block finalized in epoch 146’876 in September 2022, Ethereum managed to complete its mainnet transition to PoS in a flawless fashion. The Merge passed without any hiccups after a marathon of merged testnets and shadow forks, see Illustration 1, marking the conclusion of a multiyear effort that mitigated technical and operational risk of upgrading a ~$150b network in open-source development. Switching the core consensus mechanism of Ethereum without downtime was a spectacular technical feat that overall involved more than two years of testing and more than 100 bi-weekly calls[2]. Described as hot swapping airplane engines in-flight of a network that also secures >$163b in ERC20s and $22b in NFTs, the Merge upgrade was activated in two phases. “Bellatrix” activated on the consensus layer responsible for transaction validation and block production. It prepared the Beacon Chain to include user transactions from the execution engine and updated the fork choice rule to LMD-GHOST[3], that identifies the fork with the greatest accumulated weight of historical attestations. Consecutively, “Paris” triggered the actual merge on the execution layer that was previously tied to PoW and is responsible for transaction bundling, execution, and state management.

There's a much easier way to do the Merge: We shut down for three days, do the thing and flip the switch back on and it restarts. […] So getting this switch to happen, basically seamlessly in a way that was like incentive compatible with miners, was pretty wild.

Tim Beiko, protocol support lead since January 2021 at the Ethereum Foundation.

Proof-of-Stake

Transitioning to PoS completely changed the way of verifying transactions, securing the network, and issuing rewards as it relies on economic voting and slashing to keep validators in check. Introduced by Scott Nadal and Sunny King[4] in 2012, it was first adopted by the Peercoin blockchain in 2013 and now dominates the crypto industry since most of the protocols in recent years launched with PoS powering their blockchain.

By formally adopting the Beacon chain as the new consensus layer, validators instead of miners are now assigned to participate in consensus to secure Ethereum as they propose and attest blocks. Validators are specialized nodes that coordinate transaction processing and block creation by locking ETH. They are chosen at random by an algorithm rather than competing in mathematical puzzles with hash power. A validator either serves as single block proposer or as one of many block attesters within a committee[5].

During the Merge, a validator participation rate way above the mandatory 66% led to a quick justification of the first epoch. The network subsequently reached finality by hitting two justified consecutive epochs completing the Merge (an epoch consists of 32 slots that last 12 seconds each and offer the opportunity to propose a block to the canonical chain). Finality means that no changes afterwards are possible, except for a critical consensus failure. The PoS transition not only decreased block times from ~13.3 seconds (determined by mining difficulty) to 12 seconds but also introduced deterministic finality after 12.8 minutes (2 epochs) instead of probabilistic finality after around 1.5 minutes in PoW. While miners previously proved to have capital at risk by expending energy, validators risk capital by pledging native collateral to actively participate in securing the underlying blockchain. They get rewarded for doing so, or slashed (penalized) for inactivity or malicious behavior. Notably, PoS is only part of the consensus mechanism and functions as a Sybil attack protection, an attack vector which works by creating multiple identities. In PoS, votes are weighted by the amount of stake and thus, spinning up nodes is pointless without backing them with stake. As an attacker needs an overwhelming stake, it significantly increases the cost of attack and mitigates the risk of a Sybil attack. For instance, the cost and difficulty of an attack increased five-fold, and with the enhanced confidence induced by the Merge, it will grow higher as new validators join to protect the network.

As Vitalik Buterin states[6], PoS offers more crypto-economic security (disincentives for the same cost), enables easier recovery of attacks and offers lower barriers to entry because of reduced hardware requirements. PoS is also more resilient to force majeure, as a recent drop in BTC hashrate due to the ongoing blizzard in the U.S. showed[7]. Meanwhile, Ethereum was running at nearly 100% without any validators dropping off. On the flip side, PoS might lead to higher wealth concentration, being a closed system that requires weak subjectivity[8] (state root checkpoints implemented to undermine attack vectors such as long-range attacks). Moreover, PoS is less battle tested and brings increased implementation complexity.

Despite aiming for PoS since its genesis, Ethereum was initially forced to leverage PoW that was known for its robustness and security guarantees, while PoS took years of dedicated research and development. In hindsight, this hybrid approach was crucial to bootstrap the distribution of its native asset ETH and therefore enabled a higher degree of decentralization heading into PoS. As most networks that launched in the recent years utilized it as consensus mechanism, PoS can now also be considered to be more reliable. The Merge is one of the most significant catalysts in Ethereum history as it impacts the network on several fronts. As we outline, it came with various first and second order effects.

Energy

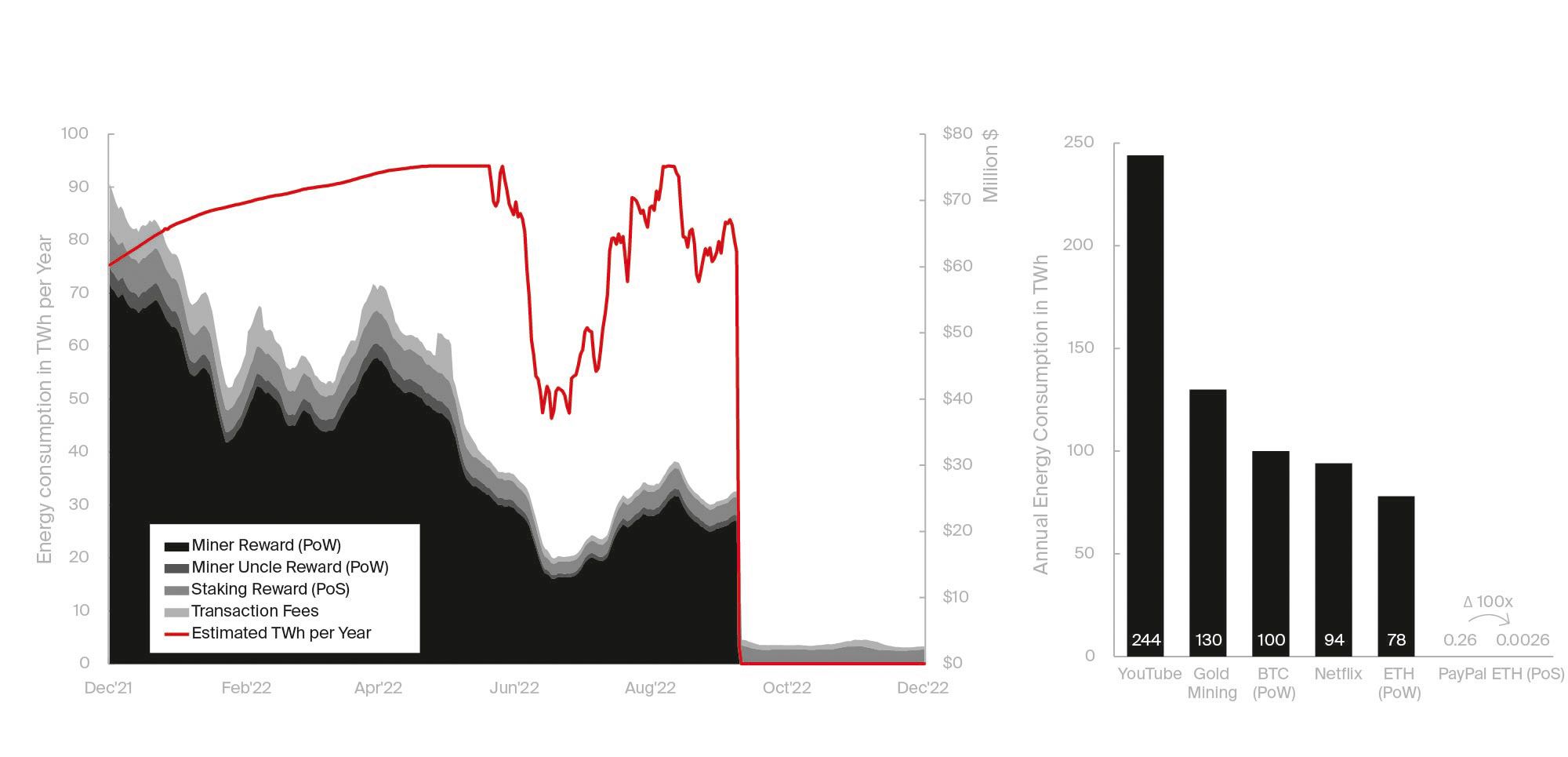

First order effects not only included a change in Ethereum’s security model and block confirmation times, but also massive changes in monetary policy and energy efficiency. Despite PoS having the same goal of achieving distributed consensus as PoW does, its lack of computational intensity leads to an impressive reduction of energy required. Neither expensive mining hardware nor operational cost of miners must be compensated any longer by protocol emissions. Therefore, PoS brings increased energy-efficiency and reduces its environmental footprint, by means of electricity consumption and carbon emissions, by 99.98% and 99.992%, respectively[9]. The Crypto Carbon Ratings Institute generated bottom-up estimates of the electricity consumption of various node hardware and client setups, yielding an estimate annual energy consumption of 0.0026 TWh and a reduction of carbon emissions from 11’000’000t CO2e pre-Merge to 870t CO2e post-Merge. For instance, PayPal consumes 100x more energy, see Illustration 2, where other ballpark estimates of industries are found for context (one should take these estimates with a grain of salt since they are subject to a broad range of assumptions). Other data suggests that the power consumption on the network fell from May’s high of 93.98 TWh, where we also saw a peak in hashpower, to around 0.01 TWh. Even with the most conservative estimates and comparing the new energy expenditure to the lowest energy consumption in 2019 at 4.75 TWh per year, the PoS transition still yields 99.8% energy reduction.

As Illustration 2 further indicates, Ethereum generated $19b in mining rewards, taking into account block subsidy and transaction fees, in 2021. Correlated to the drop in energy consumption, these block subsidies dropped to zero post-Merge. As a result, an estimated $5b of mining GPUs and ASICs[10] chased new purpose or were sold on secondary markets. One shelter was offered by the contentious PoW hard fork. However, the mean hash rate compared to pre-Merge Ethereum in September (~860 TH/s[11]) dropped to ~70 TH/s immediately after the fork. 100 days later, it is down to only 16 TH/ s[12] indicating a massive miner escape that matched the price decline of ETH PoW at around 80%. As Ethereum made up around 97% of the total daily miner revenue for GPUs, these miners struggled to find mineable coins within the crypto ecosystem and were partwise forced to pivot towards data-center oriented businesses.

As crypto starts to demonstrate real-world utility, we expect energy to be a key topic in the years ahead. Multiple headlines across the globe indicated in 2022 that PoW chains have come under more regulatory scrutiny due to their environmental impact. With ESG concerns rising, not only enterprises and governments will be under continued pressure to curb energy consumption, but PoW chains that fail to demonstrate utility will arguably see more criticism too. PoS blockchains on the other hand are more resilient to such criticism and therefore suited for ESG compliant institutional adoption.

Shifting consensus gears achieved improved sustainability for Ethereum. One could consider it as one of history’s largest decarbonization events. According to Ethereum researcher Justin Drake, the PoS transition reduced global electricity consumption by 0.2%[13]. The significance is further amplified by both an acceleration in climate change[14] and a looming energy crisis induced by the Russo-Ukrainian War. Yet, one might also argue that Bitcoin mining in the context of geopolitical tensions alongside a deglobalization trend could serve as a catalyst towards clean energy and simultaneously balance the electrical grid.

To avoid greenwashing, it is important to note that Ethereum itself added the previously mentioned 0.2% in the first place and switching consensus does not address the substantial carbon debt accrued since Ethereum’s genesis block. To repay Ethereum’s carbon debt however, there is a nascent movement known as ReFi (Regenerative Finance). ReFi builds tools to make Ethereum carbon negative via incentives for land generation, carbon capture through regenerative agriculture and other strategies. DeSci135 (Decentralized Science) might become another major innovation and momentum catalyst in 2023, fostering open, decentralized markets for research and academia via e.g. biotech DAOs or IP-NFTs enabled by blockchain technology. As such, significant improvements in publishing, reproducibility, replicability, funding, IP, data storage and access are enabled.

Issuance & Burning

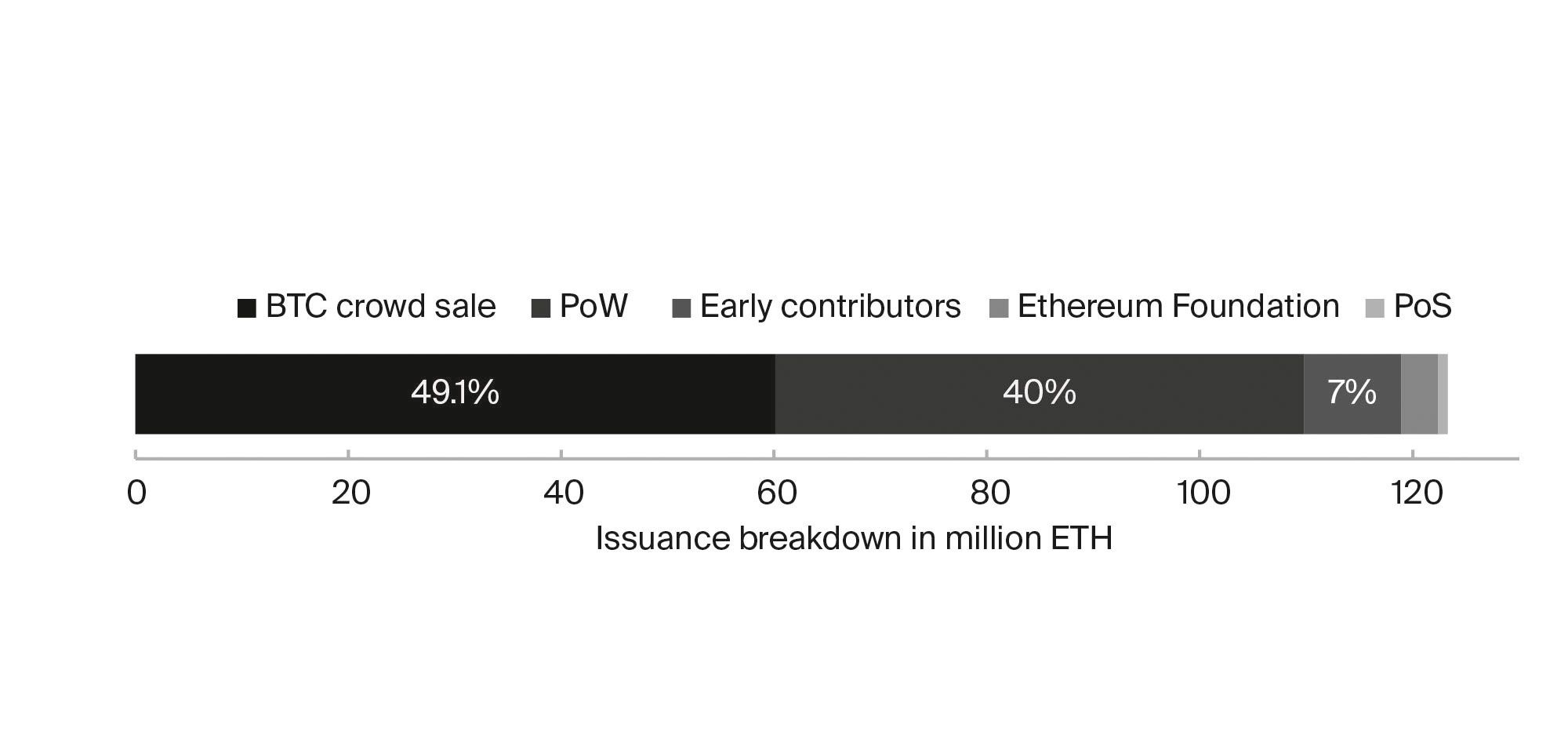

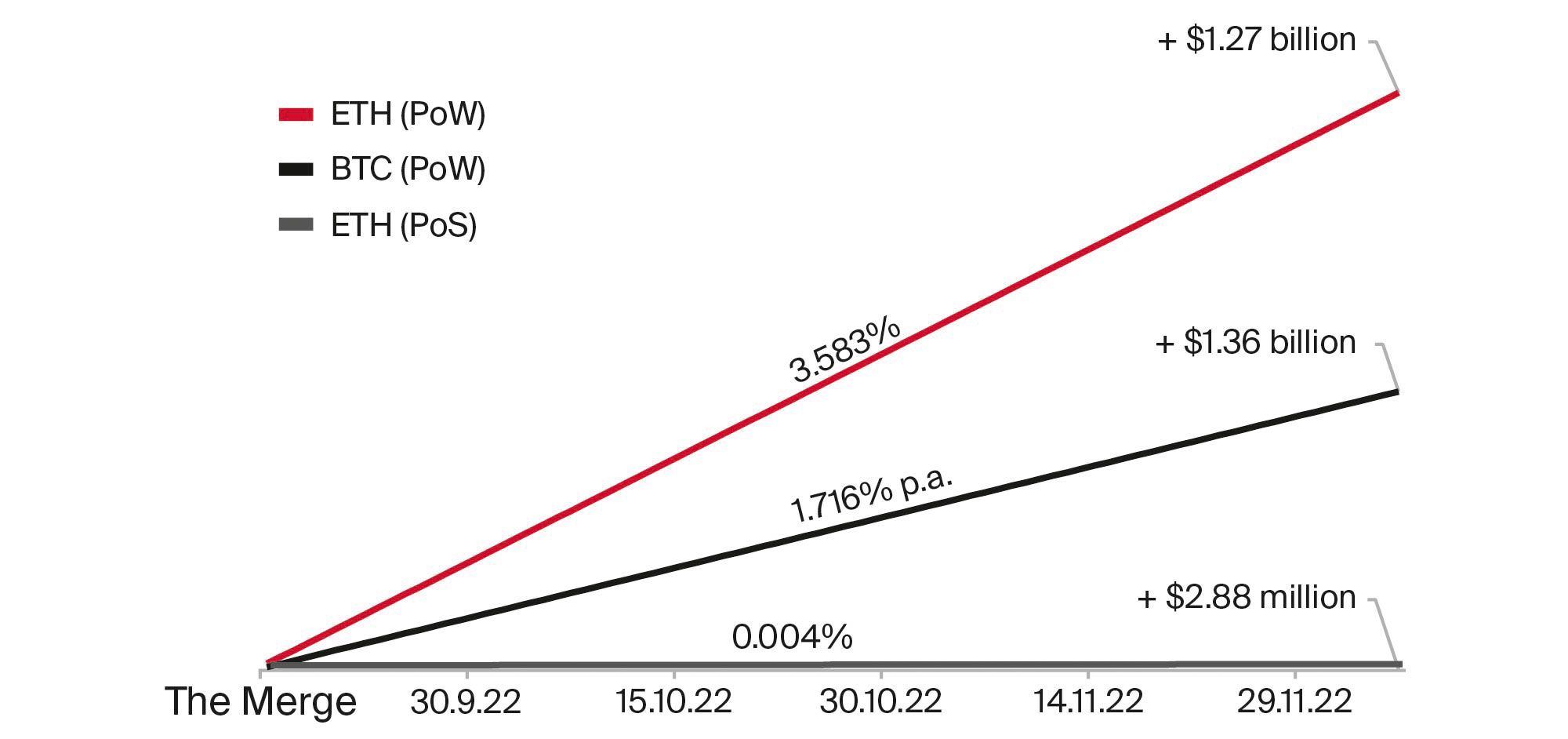

The next major first order effect is the network’s updated gross inflation. The Merge represented a major revamp of Ethereum’s monetary policy. Miner subsidies were eliminated in one swoop and drastically reduced the daily ETH issuance, since validator rewards are only a fraction compared to the compensation required for energy expenditures of miners. It brought Ethereum’s daily network issuance, that started back in 2015, at 26k ETH under PoW, down to 1.7k ETH post-Merge. On an annual basis, the issuance dropped down to 0.62m ETH postMerge from 4.9m ETH pre-Merge, thus by ~87%. Illustration 3 shows Ethereum’s supply distribution to date. Notably, the PoS issuance only accounts for less than 1% of Ethereum’s circulating supply, despite the Beacon Chain launching two years ago in December 2020. To catch up with historical PoW rewards, PoS would have to run for approximately 110 years.

Since the Merge went live around four months ago, PoS issued 4.8k ETH instead of 1.2m ETH running on PoW. At current valuations, that is $2.88m compared to $1.27b, see Illustration 4, or equal to eliminating $120m of potential monthly selling pressure. While Ethereum lowered its annual net inflation from 3.5% to 0.004%, Bitcoin currently inflates only 1.72% annually, but issued $1.36b in dollar terms, more than Ethereum PoW since the Merge. With the current block rewards, Bitcoin’s inflation is 430 times higher than PoS powered Ethereum. Looking at gold, around 3’000t of gold are estimated to be mined per year. That supply expansion brings around $192b of new annual supply to the market at an annual inflation of around 1.6%.

Not only did PoS substantially reduce Ethereum’s gross inflation, but it did also change Ethereum’s supply dynamics. By design, it lowered the sell pressure on its native asset ETH as validators are not forced to cover capital expenditure and operational expenditure. For instance, 50’000 BTC was sold in 2022 by Bitcoin miners. Projecting that to the current market cycle, ETH prices might have dropped much deeper in a low liquidity environment with an additional 1.2m ETH in circulation. Ethereum’s issuance is designed to attract more validators if the staking ratio is low. The network issuance, therefore, varies based on the amount staked and follows a root function (maximum annual issuance equals 940.87 times square root of N, where N is the number of validators)[16]. It closely interacts with Ethereum’s base fee burn feature that depends on blockspace demand and removes ETH from circulating supply. Since validators took over, two deflationary periods, one closely after the Merge and one with activity picking up related to the downfall of FTX, were present to date. Ethereum’s net inflation (gross inflation – burned supply) becomes deflationary if burnt transactions implemented with EIP-1559 exceed the network’s staking issuance rate. Since EIP-1559 went live last summer, Ethereum burned about 85% of all transaction fees. With EIP-1559, Ethereum turned a major flaw, being high gas fees, into a mechanism that benefits holders of the underlying base asset ETH.

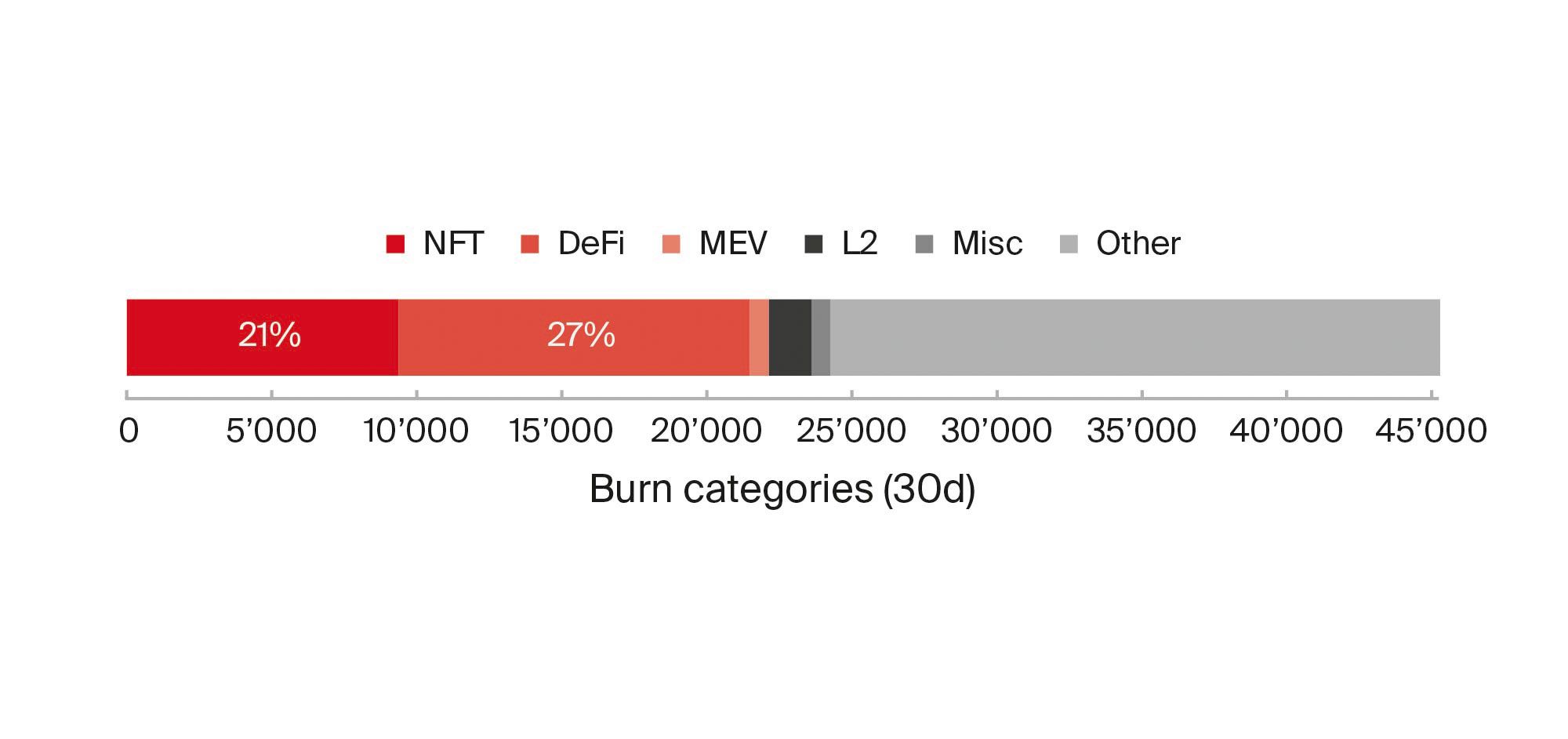

Overall, 2.8m in ETH, at an average burn rate of 3.8 ETH/min, or $8.77b has been burned[17] within the 510 days since EIP-1559 was activated. That’s on average 3.22x more than Ethereum’s post-Merge issuance of around 1.18 ETH/min. Substantial demand that drives burning is induced by NFTs and especially DeFi, see Illustration 5.

One crucial part for burn activity is MEV (Maximal Extractable Value), that the block proposing validator can extract in PoS. Instead of miner subsidies, validators are now eligible to gain the execution layer rewards aside from the protocol issued consensus layer rewards. Execution layer rewards are directly proportional to the transaction activity and can be referred to as a combination of rewards consisting of tips and rewards generated through MEV (primarily available to validators who run MEV Boost). Technically, validators receive execution layer rewards as additional tips for prioritizing, including, excluding, or reordering transactions.

Consensus layer rewards on the other hand are inversely proportional to the amount of ETH staked and refer to the rewards from the issuance of new ETH. Validators receive these rewards, also considered inflation rewards, for participating in the security of the Ethereum blockchain either as block proposers, attesters, or members in sync committees[18]. The largest part of the consensus layer rewards for validators, making up for 84.4%[19], are attester rewards that validating nodes receive for correct and timely votes on the source checkpoint, target checkpoint and chain head block. Additionally, validators are eligible for rewards participating in sync committees in varying proportions.

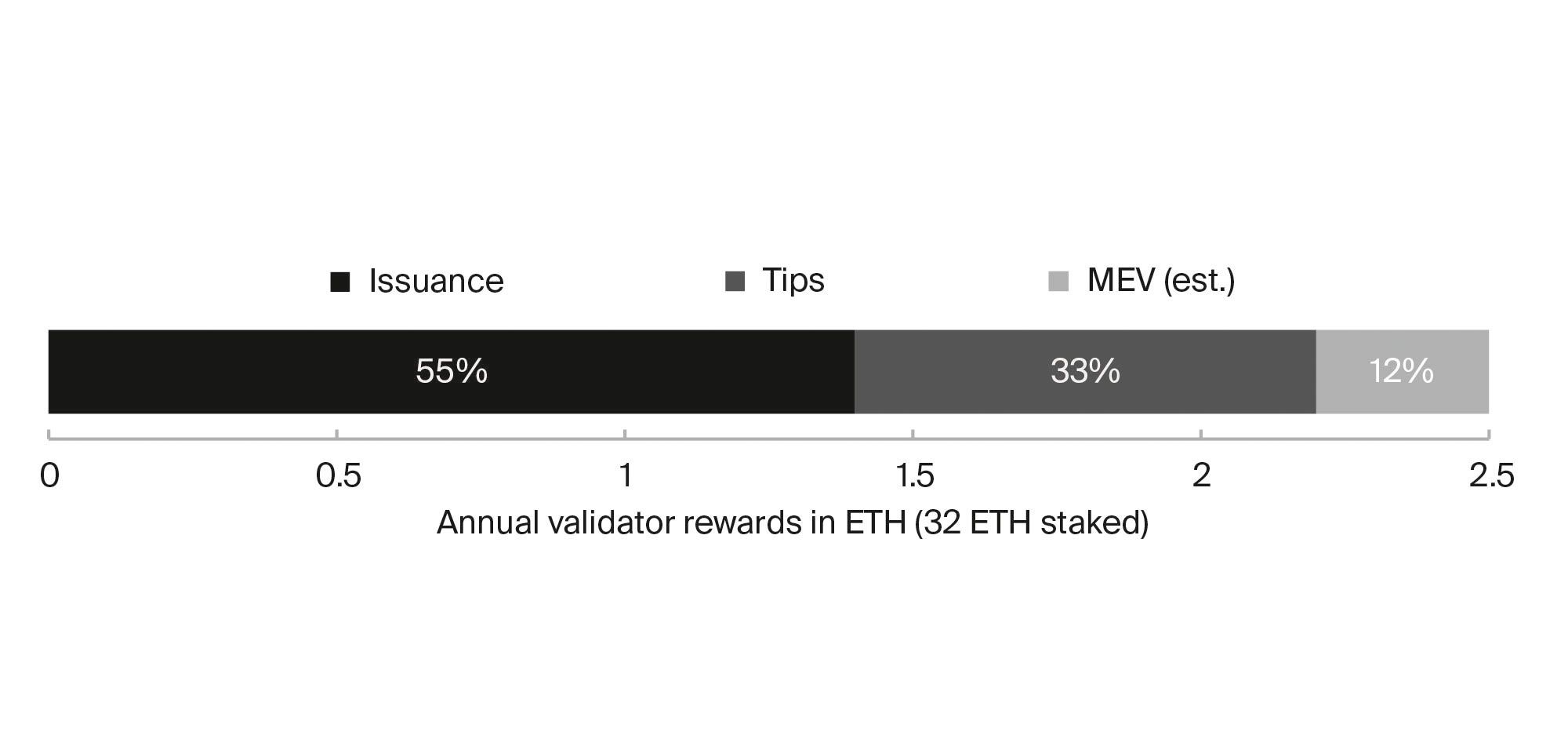

An average validator is currently able to yield 7.8% annually, composed of 55% issuance, 33% tips and 12% sourced from MEV, see Illustration 6 where the average annual rewards are broken down for a validator staking 32 ETH.

For the time being, we expect the new supply dynamics to shape a range between a slightly deflationary and slightly inflationary environment. As blockspace demand is comparably low in prolonged downtrends, we observe that Ethereum’s burning feature is nonetheless balancing out the inflation rewards for validators. Hence, it is bringing the net inflation close to 0% despite being in a sustained period of low average transaction cost, with $5/ transaction[20]. In 2021, the average transaction cost was mostly above $20. Long-term, Layer 2 (L2) momentum along with a change in the Layer 1 (L1) narrative, and an uptick in activity might bring the issuance into a deflationary environment. Especially when headed into an uptrend again, that is known for stimulating on-chain activity. Like a Bitcoin halving on steroids, the Merge reduces the overall network inflation, and with that, sell pressure linked to network issuance decreases on the supply side. As with Bitcoin halvings, we expect to see the new supply dynamics heavily in play as soon as demand hits the industry again. Ethereum’s inflation adjusted staking APR is already best in class and will likely have material impact across multiple industries. Introducing yields to the largest smart contract platform might also induce institutional interest. Yet, transforming ETH into a yield-bearing financial instrument comes with regulatory risk. As such, SEC’s Chairman Gary Gensler did not hesitate to signal that Ethereum’s new PoS mechanism might draw attention of the SEC, as staking could trigger securities laws[21].

Looming censorship

On August 8, the U.S. Department of the Treasury’s Office of Foreign Assets Control (OFAC) sanctioned the privacy protecting crypto mixer Tornado Cash and 44 smart contract addresses associated with it[22] for aiding thieves in laundering stolen money from exploits. These sanctions fueled controversies around Ethereum’s censorship resistance and exposed substantial attack surface. It also sparked the question why a single jurisdictional entity should have cross-jurisdictional sovereignty on a neutral, permissionless and decentralized network. In crypto, censorship is a spectrum that can range from weak to strong censorship and often derives from centralized points in the tech stack. Weak censorship usually occurs above the validator level and refers to a mild form of transaction censorship. It happens via frontends, via centralized infrastructure providers such as Infura or Alchemy that are capable of restricting transactions flowing through their nodes, or within the block production pipeline that results in an on-chain inclusion delay of transactions subject to censorship. In this block production pipeline, we face builder centralization and centralization of trusted MEV relays that represent another layer of possible censorship. It can also happen on the validator level if a fraction of validators actively participates in block censorship. Yet, if the fraction is insignificant, other validators will eventually pick up the transaction. Same applies to block producers as non-censoring block producers ultimately pick up non-compliant transactions. As of writing, there is a 99.99% chance to have a OFAC non-compliant transaction included within 5 minutes instead of 12 seconds. Strong censorship, however, happens on the validator level rooted in block proposer attestations[23] and means that censored transactions never get included in any block. Strong censorship is possible if a certain entity controls the machine layer consensus by hitting an aggregate of 51% consensus threshold. If this ever happens, the only way out is via social slashing and a minority fork, viable means as validator level censorship-resistance is mandatory in order to protect and maintain Ethereum’s integrity as well as its core value proposition offering equal access to anybody.

My personal opinion is if we allow censorship of user transactions on the network, then we basically failed, and this is the hill I’m willing to die on. If we start allowing users to be censored on Ethereum then this whole thing doesn’t make sense. […] I think censorship resistance is the highest goal of Ethereum and of the blockchain space in general so if we compromise on that there’s not much else to do in my opinion.

Marius van der Wijden, developer from the Geth client team, on protocol level censorship resistance

As Ethereum successfully transitioned to PoS, all eyes are now on potentially centralizing forces within the upgraded network and the threat of censorship looming alongside. Ethereum faces points of centralization almost across the entire tech stack. However, there is a plethora of strategies to mitigate potential risks moving forward that rely on not only the protocol layer but also the social layer.

Remote Procedure Calls (RPC) and Frontends

Many dApps have centralized frontends that allow censoring access as seen multiple times in 2022. More importantly, these dApps usually leverage RPC nodes in the background to communicate user intends. Infura and MetaMask for example blocked wallets trying to interact with Tornado Cash. Recently, ConsenSys also announced an update to its privacy policy affecting wallet provider MetaMask and its default RPC Infura[24].

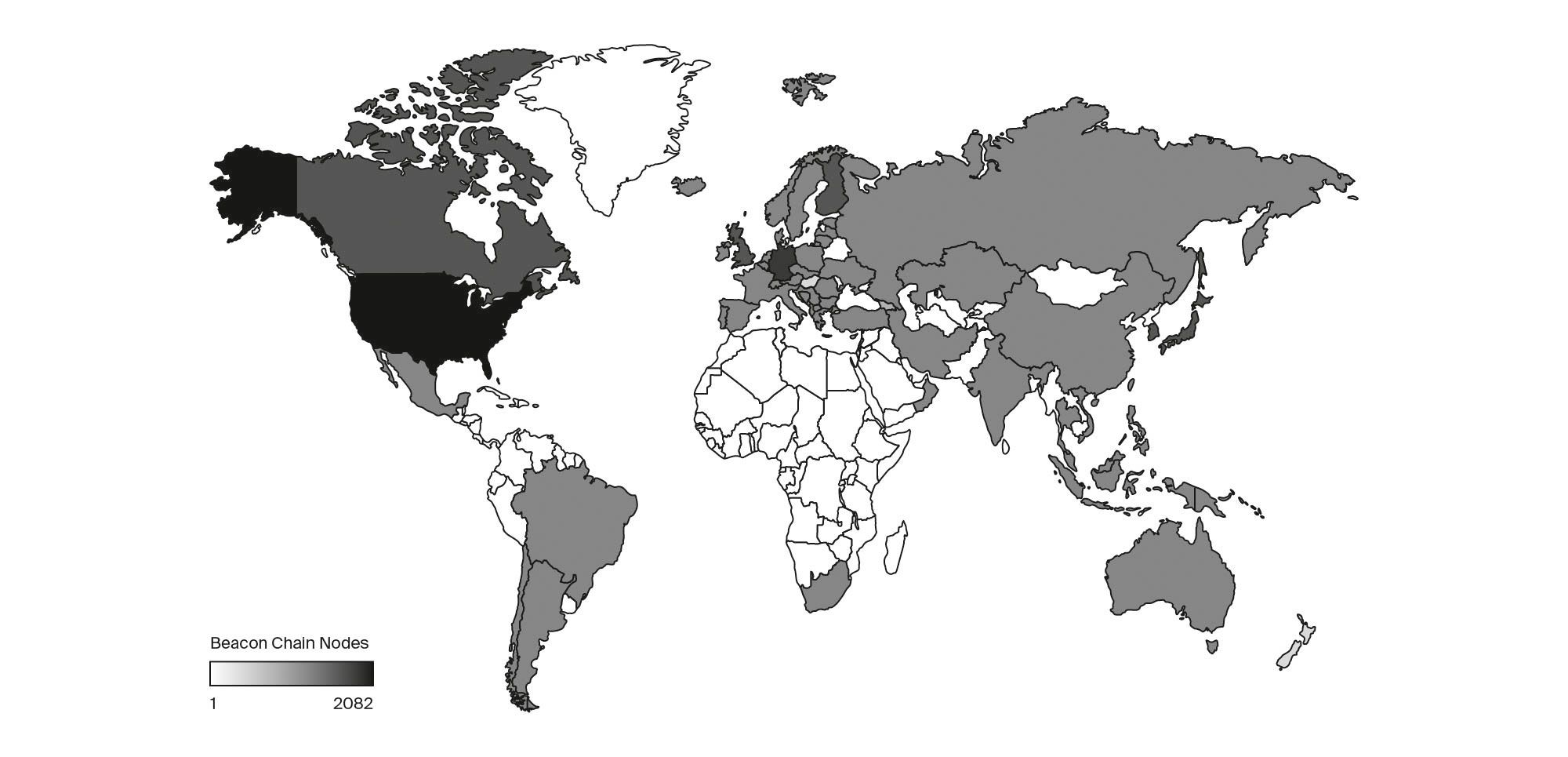

To fight weak censorship above the validator level, there is a clear roadmap to decentralize infrastructure via in-browser light clients instead of going through RPC endpoints. In PoS, light clients that figure out the tip of the chain via sync committees are way easier to build and it’s reasonable to expect that even MetaMask will move to light clients post-Merge, therefore enabling users to route around and avoid endpoint censorship. A viable short-term workaround is switching the wallet provider (e.g. XDEFI wallet, Rainbow, BlockWallet or Frame instead of MM), the RPC (e.g. SecureRPC by Manifold, Pocket Network, Alchemy) or a combination of both. Some RPCs also offer additional features such as private transactions, censorship resistance and to some degree front-running protection. However, the best solution by far is running a node to guarantee direct blockchain access instead of relying on a centralized API and node infrastructure providers such as Infura or Alchemy. Anyone is free to sync their own, self-verified copy of Ethereum by running a node. Despite no staking capital required, nodes serve a critical role in securing the network by holding all block proposers accountable and offer additional benefits such as improved security, privacy and censorship resistance. It also counters risk associated with node hosting, which represents another point of centralization and attack vector, not only regarding operator diversity, but also jurisdictional diversity. Illustration 7 for instance shows the global distribution of Beacon chain nodes. These entities reside in jurisdictions that underly various regulatory risk.

Dependencies on centralized frontends, such as Uniswap’s, can be avoided by having multi-jurisdictional decentralized frontends, IPFS/ENS frontends, running local UIs or by engaging directly with the smart contract and therefore going around all checks and friction. Aside from the frontends and RPCs, oracles, stablecoins, source code hosting services or upgradeable smart contracts offer more attack surface.

Validator level

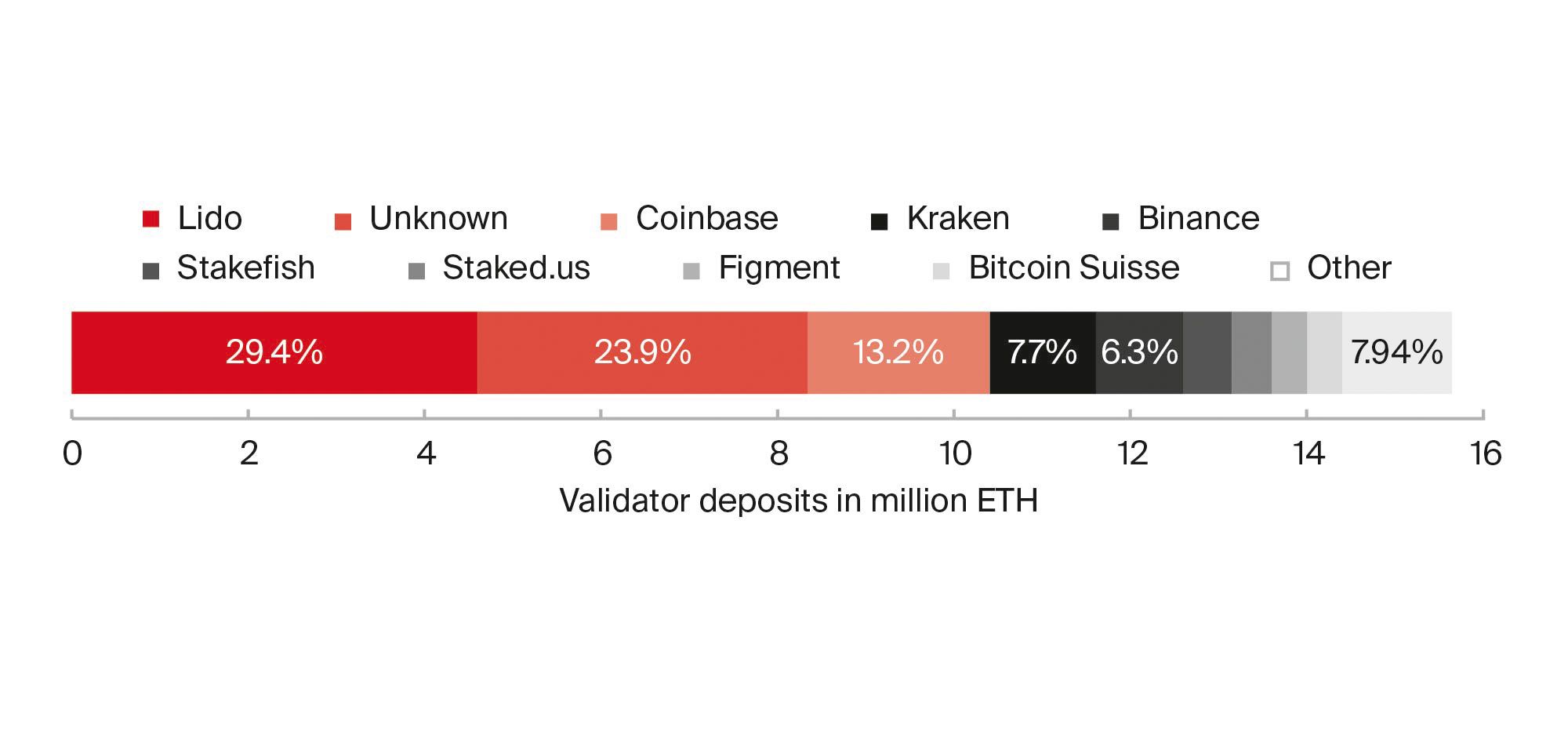

One of the Merge’s second order effects was boosting user confidence towards staking. As liquid staking derivatives recovered from significant depegs, while staking deposits accelerated, concerns about validator centralization grew quickly. Validator deposits printed new ATHs with 487’656 validators now staking 15’659’191 ETH[25] within the deposit contract, thus removing 13% of the overall circulating supply. 44.8% of that stake, however, is controlled by only three entities, Lido, Coinbase and Kraken (note that Lido is a DAO and consists of 30 independent operators[26]), see Illustration 8. These entities provide staking services and are either centralized exchanges or staking pool services with a varying degree of decentralization. With liquid staking derivatives, users can take advantage of yield prospects in DeFi without compromising network security. While liquid staking offers PoS networks the chance to increase their meager security, it has the potential to become a centralizing factor over time. Validator centralization does also have second order effects as it contributes to client homogeneity. A lack of client diversity[27] poses a risk of network outages if for example there is a client error, or a client is under attack. Slashing penalties in PoS help to encourage operators to adopt a diverse stack of clients to ensure uptime and network liveness.

As the overall integrity and security of Ethereum’s PoS can only be guaranteed with no one entity surpassing crucial consensus thresholds, an excessively concentrated stake can call into question the decentralization and neutrality of the network. One entity holding a third of the stake can already cause concerns, as it breaks Byzantine fault-tolerance, a crucial characteristic of the consensus protocol that enables resilience against dishonest players. Staking via a centralized entity is convenient, requires almost zero know-how and often allows staking with less than the minimum 32 ETH required for solo staking. Even if PoS was designed to lower the entry level complexity for validators, independent staking still comes with significant friction regarding risk tolerance (slashing), technical know-how (setup and operation) and investment size (32 ETH to spin up an individual validator). Thus, small holders and anybody with less technical expertise are almost forced to use some form of staking service with a ranging degree of trade-offs. Aside from staking with centralized exchanges, liquid staking solutions such as Lido, Rocketpool or Stakewise are popular. Rocketpool, is noteworthy as it offers additional permissionless node operation, enabling greater decentralization and less capital requirement (16 ETH +16 ETH delegated from retail stakers) as anyone can operate a node, known as Minipools. Moreover, Lido takes a 10% cut of the rewards (5% treasury, 5% node operators) while Rocketpool takes a 15% cut from retail stakers of which 100% goes to node operators. Stakewise is another interesting project offering modular staking and distributed validator technology (DVT) support. Notably, Stakewise is the only one aiming to pay out 80%-100% of fees earned to SWISE token holders. Solo staking and fully decentralized services like Rocketpool’s have the biggest impact on decentralization and resilience of the network. Solo staking also allows to actually propose self-build blocks. An average solo staker proposes 5.36 blocks per year earning 1.27 ETH at 0.237 ETH per proposed block to date. Running a validator node moreover guarantees direct access to the network without dependencies on RPCs that might track one’s data.

Improving validator centralization heavily relies on the social layer. Any user staking ETH can actively choose how and where he aims to stake and hereby contribute to improving jurisdictional and operator diversity[28]. If there is ever a threat of strong censorship on the validator level, there is a multitude of solutions in the pipeline that aim to prevent said threat: Enshrined proposer-builder separation (PBS) that removes the requirement for validators to trust relays, MEV smoothing that removes variance of MEV and MEV burning[29], single slot finality[30] to speed up deposits and withdrawals, statelessness[31], DA sampling and zero-knowledge (zk) EVMs that will significantly reduce hardware cost, a reduction in necessary stake size, privacy preserving deposits and staking, anti-slashing hardware and finally, encrypted mempools that will help both against censoring builders and proposers (validators).

We expect that not only liquid staking solutions will gain more momentum in 2023 but also staking innovations such as Obol[32] or SSV[33]. Obol provides DVT (Distributed Validator Technology), also known as secretly shared validator technology, a middleware solution alike MEV-Boost, that can enhance the operation of an Ethereum validator by allowing multiple non-trusting operators to run distributed validators. Applying DVT will lead to improved resilience, greater stake decentralization and reduced slashing risk. In combination with the reduced sell pressure from a lower gross inflation in PoS, increased staking activity triggered by the Shanghai upgrade will likely remove more liquid supply from the market.

Block production pipeline

Economies of scale was considered to be a huge threat heading into PoS. Economies of scale of validator entities could have potentially triggered MEV (changing the transaction order to build blocks with the highest possible economic value) flywheel effects by having substantial amounts of staked ETH. To avoid centralizing forces within the validator set, Flashbots preemptively introduced MEV-Boost, a middleware that validators can adopt to capture MEV-rewards. It enabled a fairly even distribution of MEV across the entire validator set. So far, MEV-Boost succeeded in preserving validator level decentralization in that it allows any validator to plug into sophisticated MEV extraction techniques. Therefore, it democratized access to MEV as validators are not forced to redelegate their stake, yet still mine profitable. MEV-Boost also lowered gas cost as block auctions were put off-chain. However, it introduced other centralizing forces within the block production pipeline like relay and builder centralization. The block production pipeline consists of searchers and their own private order flow, that leverage certain strategies. These include front-, back-running, arbitrage, sandwich attacks and liquidations to find MEV-opportunities. They then bundle up these transactions and forward it to builders. Builders aggregate transactions to craft the most economically sound blocks. Finally, proposers (validators) receive the blocks (execution payload) via relays. Extracting MEV is highly profitable. Since January 2020 a total of $686m was extracted, while $1.49m was wasted on failed MEV-transaction fees[34].

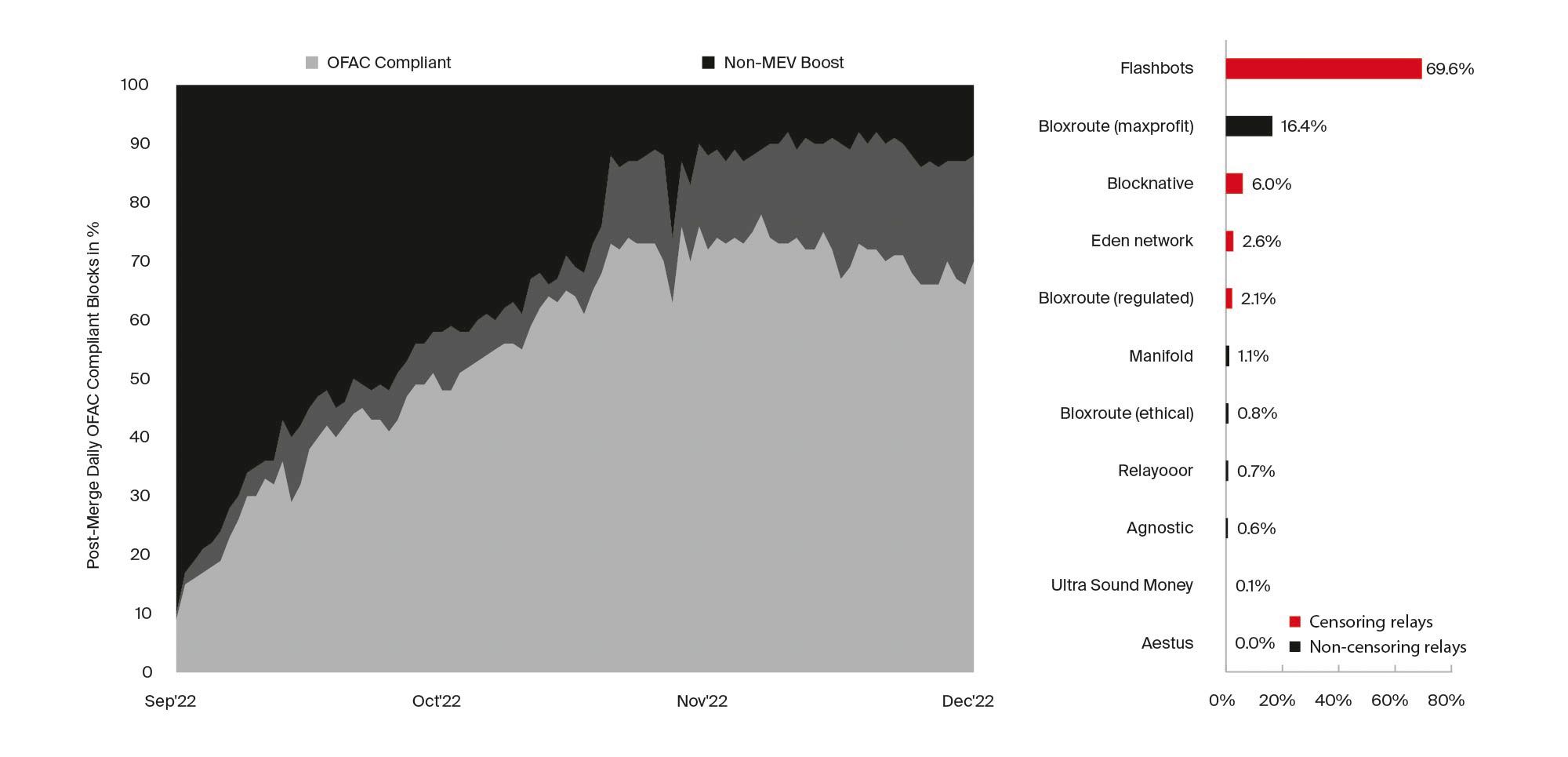

As MEV-Boost provides a substantial financial advantage to validators who use the software to sell blockspace to block builders, its adoption propelled to 90.79% of network adoption[35]. While builder centralization seems to be a non-issue as of writing (Flashbots builder’s market share fell from ~80% in September to ~25% in December), relay centralization is a real threat. Illustration 9 depicts the percentage of OFAC compliant blocks funneled through MEV-Boost. Censoring relays being most adopted, with Flashbot’s relay dominating the landscape at almost 70%.

OFAC compliant in that context means that relays won’t include transactions that interact with Tornado Cash or other sanctioned wallet addresses, as outlined by the OFAC. There are currently 11 relays competing in MEV-Boost, with four of them censoring. Unfortunately, these four currently make up around 80% of all blocks added to the chain. Across 30 days, the ratio of OFAC compliant block has been at almost 70%. The fact that most blocks routed through MEV Boost are OFAC compliant raises concerns. It creates the impression to financial authorities, that they can enforce compliance requirements by applying pressure to large custodians. The prevalent dominance of censoring relays is a patronizing obstacle, that at its core represents a dangerous and regressive development.

In 2023, centralizing forces within MEV are likely to be one of the key topics. Recent shifts in the relay landscape give reason for hope. Not only did more non-censoring relays recently join the battlefield, but the dominance of OFAC compliant blocks seems to have peaked in late November, indicating a trend shift towards more diversity and competition. More entities will likely be brave enough to choose a relay diversity approach to boost non-dominant relays. With the threats being exposed and more awareness due to CeFi blowups, we expect this trend to be sustained in 2023. Moreover, an interim solution in 2023 is arguably provided by Flashbots, that is building an open-sourced upgrade to MEV-Boost known as the Single Unifying Auction for Value Expression (SUAVE). SUAVE is a MEV-aware and privacy-first encrypted mempool which provides transaction opacity and eliminates any central points of control, including Flashbots itself. Notably, Flashbots also open sourced its relay in August, and its builder in November, thereby reducing the risk of builder centralization. Medium-term solutions include encrypted mempools, enshrined PBS and inclusion lists.

Censorship-resistance is a mandatory feature for future proof blockchains. If Ethereum wants to be a self-sovereign public good with secure blockspace and equal access for everybody, it must have immunity from nation states. It is important to understand that censorship-resistance will, to a significant extend, be up to the conscious end users and the community actively choosing and supporting permissionless applications and services built atop Ethereum.

Roadmap

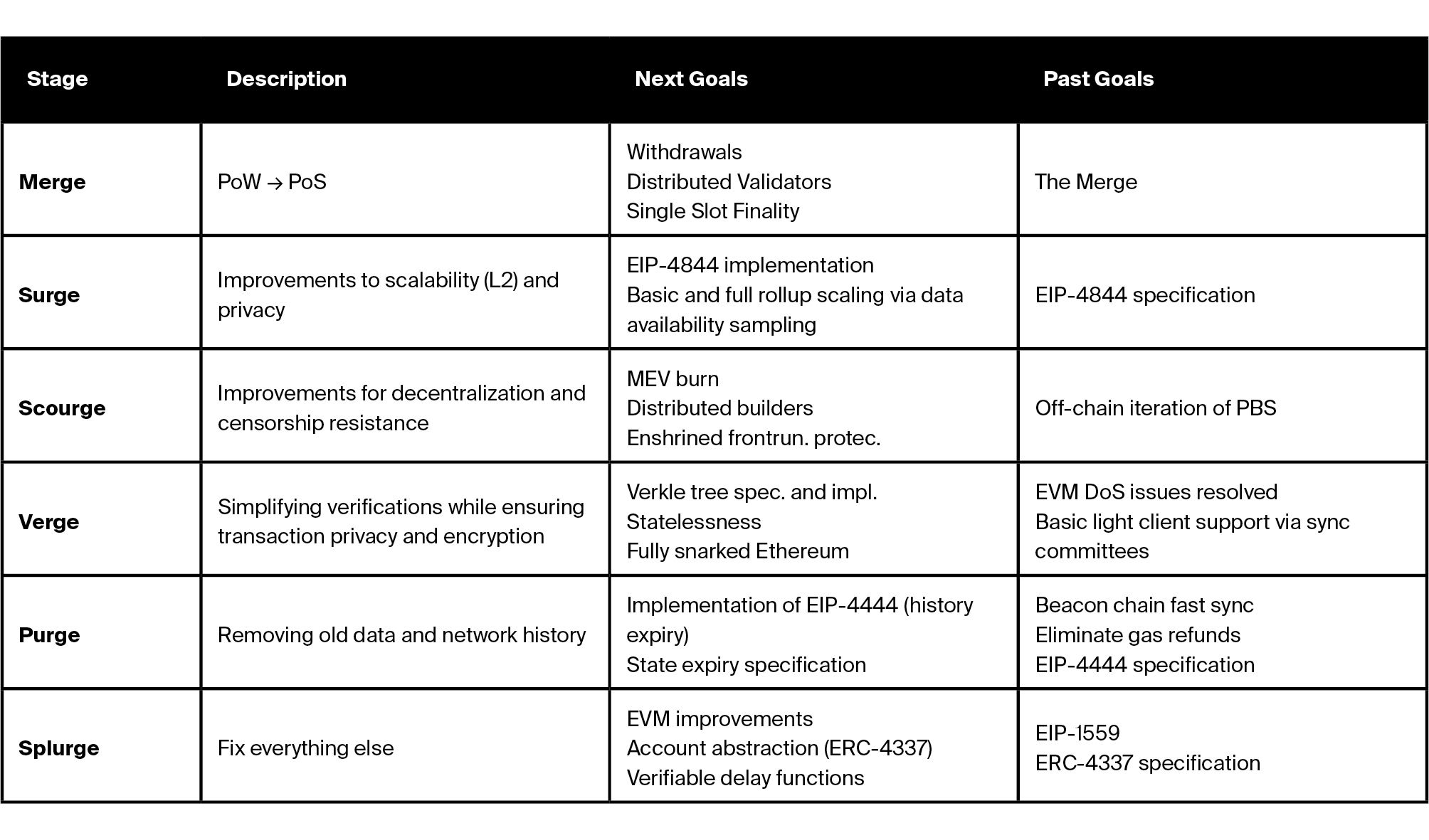

Despite the Merge being one of the most significant structural shifts of any large-scale crypto asset to date, it was only one part of Ethereum’s comprehensive roadmap that aims to improve the network around scalability, decentralization, security, hard disk requirements and elimination of tech debt. Just two months after the Merge, Vitalik Buterin revealed a new roadmap organized in six categories, see Illustration 10: The Merge, The Surge, The Scourge, The Verge, The Purge, and The Splurge. With the recent roadmap update[36], not only more precise milestones were added in each category, but also a new item, The Scourge. It aims to ensure reliable and credibly neutral transaction inclusion as it deals with MEV-challenges and forces of centralization.

Scheduled for March 2023, the next highly anticipated Ethereum upgrade after the Merge is the Shanghai and parallel Capella upgrade. As interest of financial authorities is rising with the mess caused by FTX, it’s important to have withdrawals enabled as soon as possible to avoid regulatory tail risk of potential censorship-enforcing jurisdictional actions. Capella will upgrade the Beacon chain (consensus layer) and Shanghai targets the execution layer, formerly tied to PoW. Enabling withdrawals is crucial. Since the launch of the Beacon chain, all staked ETH plus the consensus layer rewards remain locked, while execution layer rewards like Tips and MEV are distributed concurrently. Aside from EIP-4895 (withdrawals), EIPs that are prioritized in Shanghai are EIP-3860 (initcode), EIP-3651 (coinbase address) and EIP-3855 (new instruction called “PUSH0”). Instead of Proto-Danksharding, developers recently agreed to include EIPs related to EOF implementation. EOF implementation is the first major code change since its inception targeting the EVM, Ethereum’s execution environment.

Beyond the activation of withdrawals, the next major upgrade for Ethereum will be centered around activating the Surge related Proto-Danksharding (EIP-4844). Initially planned for implementation with Shanghai, it was recently shifted to the next upgrade in favor of avoiding any delay for withdrawals and potential tension induced by the complexity of the upgrade. EIP-4844 will introduce a new transaction type that allows “blob” carrying (instead of calldata) for L2 batch settlement in a specific blockspace allocation that is expected to massively boost L2 scalability. Consider Danksharding to be an afterburner to rollups making them more efficient and cheaper. For Proto-Danksharding, there is no fundamental change to how the underlying blockchain technically works. It’s also a precursor for full Danksharding, a design that uses a merged market fee where shards share the same block proposer for different blocks. According to Dankrad Feist, responsible for the technical lift, Danksharding brings Ethereum from being capable of serving one million people to one billion people. Notably, the introduction of PoS is an enabler for sharding. While it’s not preventable that PoW miners collude their hashpower on a single shard to take over control, PoS randomly assigns validators to a shard preventing from choosing the shard they want to participate in. The initial execution sharding approach is currently skipped for Ethereum’s rollup-centric roadmap[37], which prioritizes modularity and Data Availability for rollups. Other EIPs of importance are EIP-4488, complementing Proto-Danksharding by reducing calldata cost, EIP-4337, introducing Account Abstraction[38] enabling users to employ smart contract wallets instead of an externally owned account (EOA), and EIP-1135 which should reduce gas costs for the Layer 1 and is heavily lobbied by the Uniswap team who is building their V4 product with that upgrade in mind.

While the Merge kept us on tenterhooks for years, we expect subsequent upgrades from Ethereum’s well-defined roadmap to take shape at a considerably higher pace in 2023. The Shanghai hard fork enabling withdrawals already sets the tone and is a legitimate proof that the core developers have the user’s best interest in mind. Active withdrawals might induce a sustained period of increased yet limited liquid supply entering the market. Validators will need to enter an exit queue with limited batchwise unstaking per epoch (50k ETH are allowed to exit the active validator set per day). The unlocking of staked funds will arguably go hand in hand with a substantial confidence boost and hence attract new (solo) stake that was hesitant previously. This caution is very much indicated by a comparably low staking ratio in Ethereum. We expect that deposits outpace withdrawals even in the short- to medium-term. A higher staking ratio would result in improved network security along with a reduction in staking pool and liquid staking reliance. Withdrawals will moreover allow activist staking again, where stakers are free to actively reshuffle their funds to achieve more distributed validator pools. This will also avoid validators being trapped in regulatory crossfire. In 2023, Proto-Danksharding will unlock a plethora of new financial and non-financial use cases including social media, gaming, and metaverses that rely on more scalability. It will also reinforce Ethereum’s approach to modularity by outsourcing execution to rollups. Yet, “blobs” will arguably not solely solve rollup scalability as it brings a massive demand of on-chain data, state bloat and technical complexity.

Ready, Layer 2

To date, the most sophisticated and promising L2 scaling technology that supports general purpose EVM-code are rollups. A rollup off-chain bundles transactions which reduces transaction fees and network congestion. This transaction bundle is senttowards an Ethereum smart contract, inheriting Ethereum’s security guarantees, settling on the L1 and enabling anyone to reconstruct the correct state. The data is handled by sequencers and validators.

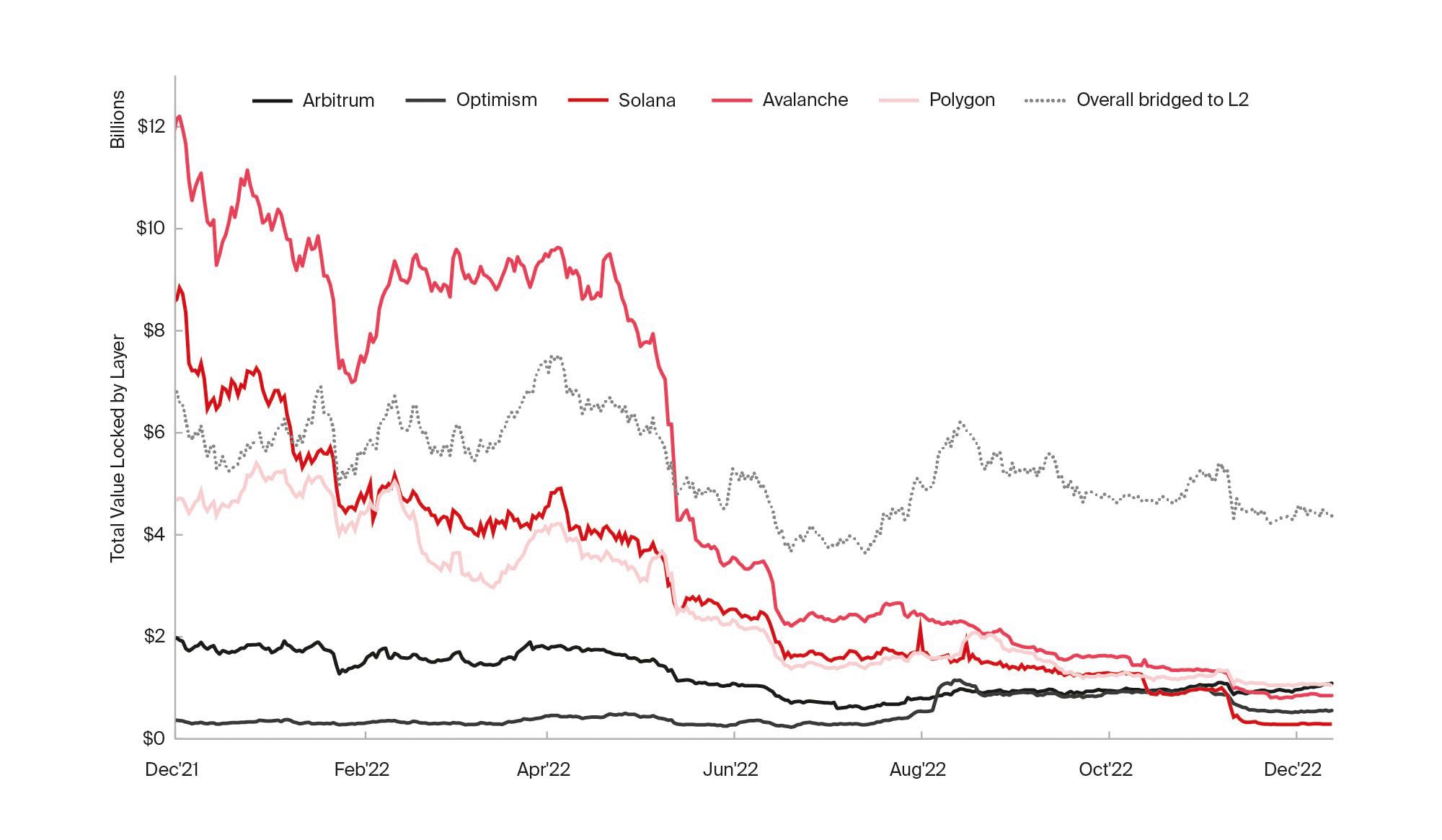

Within recent years, unsustainably high transaction costs on Ethereum haunted users and induced a wave of alternative L1 smart contract platforms alongside L2 scaling solutions atop Ethereum. While the expanding set of protocols with varying design tradeoffs created viable alternatives for developers and investors alike, 2022 revealed substantial interest in rollups. Underpinned by low transaction cost, Ethereum’s rollup-centric roadmap began to materialize in ’22 while alternative L1s such as Avalanche, or Solana dropped massively across most relevant metrics. Even Ethereum suffered declines across the board, as for instance, its total value locked (TVL) shrank from the peak in November ’21 at $110.28b (22.9m ETH) to $22.9b (1.06m ETH) in December ‘22. The best relative performance in TVL, despite declining, was seen in both Arbitrum and Optimism (Illustration 11), where optimistic rollups are indicated in yellow and alternative L1s in red. In fact, Arbitrum and Optimism steadily climbed up the TVL leaderboard and are now the 4th and 7th largest chains by TVL, respectively. Arbitrum managed to take over former giants such as Avalanche (TVL peaked at $12.21b, now at $0.77b) and Solana (TVL peaked at $10.17b, now at $0.21b). Solana’s drop was remarkable as its ecosystem was closely linked to FTX and its downfall. Solana is now trading at single digits, down from the November ’21 peak of $259.96 and hence wiped out more than 96% of its value. Overall, scaling solutions have largely been dominated by Arbitrum, Optimism, and dYdX, which currently account for over 90% of the TVL across all Ethereum-based rollups[39].

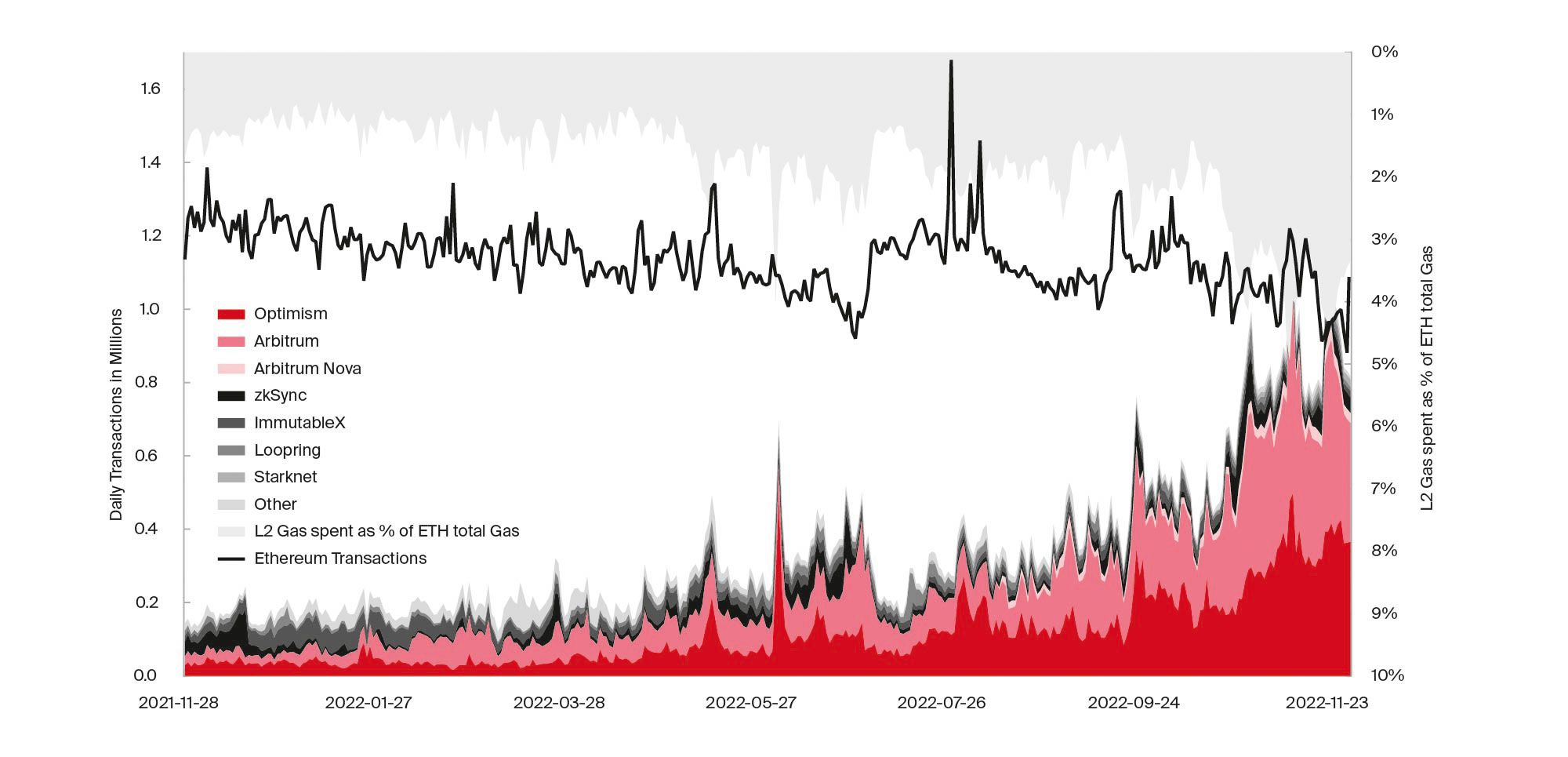

The momentum of rollups was also reflected by a huge uptick in transactions. As of writing, they increased scalability of the underlying base layer by 2.44 times (7d average)[40]. It takes into account how many more transactions are settled on Ethereum on top of its native base layer transactions. For a one-month duration, the scaling factor currently lies at 1.84, including non-general purpose L2s[41] with Ethereum at 12.27 transactions per second (TPS), Arbitrum at 3.49 TPS and Optimism at 4.96 TPS. As a result, the L2 transaction count caught up with Ethereum’s and even outmatches it occasionally, see Illustration 12.

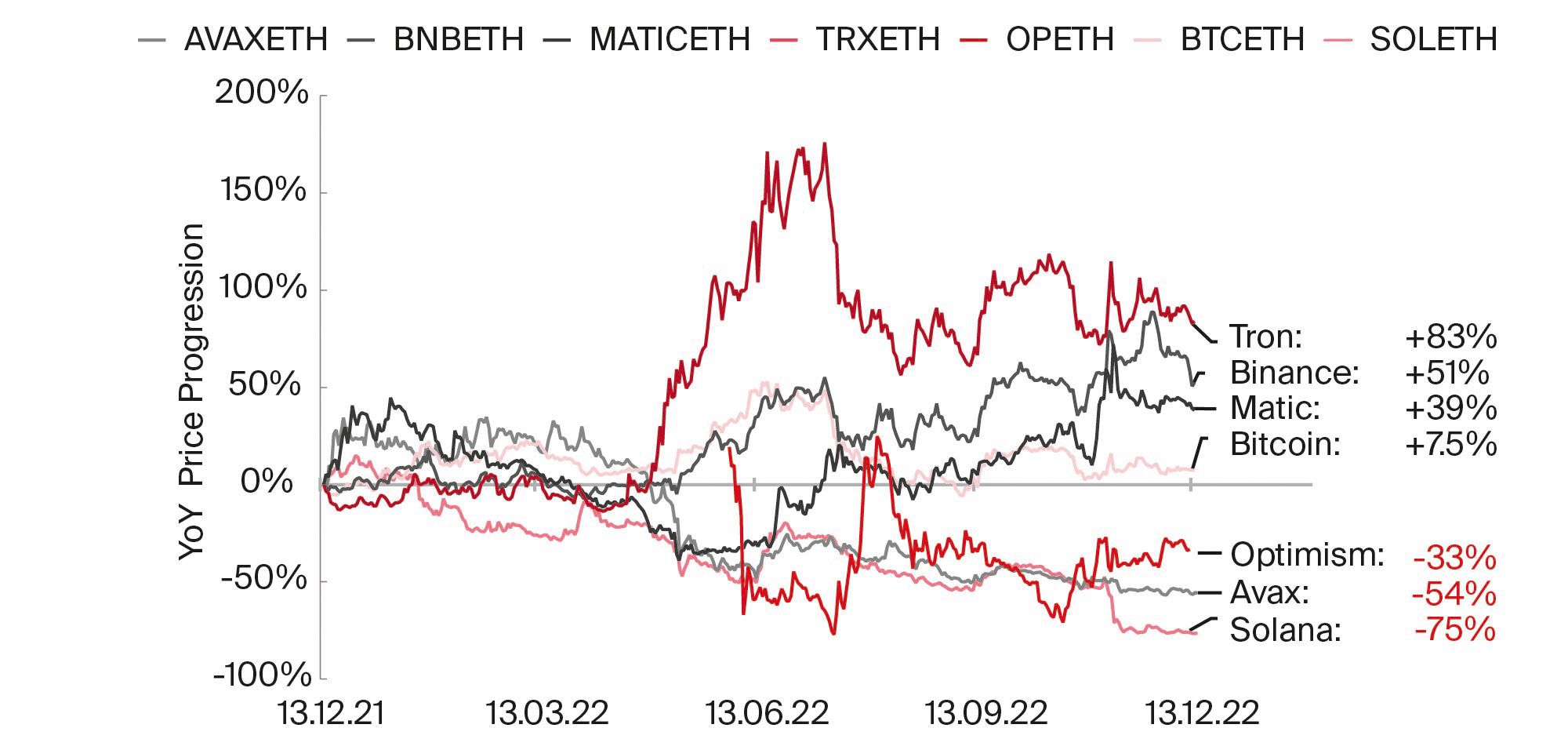

While transactions on Ethereum where mostly rangebound this year, L2 transactions, especially those executed on Optimism and Arbitrum, grew substantially. Optimism grew in weekly transactions from around 0.3m in January to 3m in December while Arbitrum grew from 0.25m to around 2m. With increasing adoption, rollups also start to account for a significant percentage of gas spent on Ethereum. It’s no outlier anymore that rollups range above 4% of the overall gas spent on Ethereum. For instance, the Arbitrum sequencer is constantly among the top gas spender on Ethereum. Given further adoption of L2s, sequencers of different rollups might soon be the tenants paying the highest rent to get their data stored on the L1 and to benefit from Ethereum’s security. However, these tenants also extract value from the base layer since the rollup’s sequencer is responsible for adding and ordering transactions and hence captures the majority of the MEV. This revenue can either accrue to the L2 token, to potential L2 validators or fund public goods within the rollup’s ecosystem. Heavy, Layer 1 In 2022, L1 ecosystems across the board suffered from CeFi blowups and heavy macro conditions. Ethereum showcased good resilience among smart contract platforms. Bitcoin, Tron, Binance and Matic even outperformed ETH by a good margin year-over-year (YoY), see Illustration 13.

From 159 blockchains that offer smart contract functionality, Ethereum accumulates 59.7% of the total TVL and accounts for around 47.6% of the volume on decentralized exchanges (excluding L2)[42]. Notably, 2022 saw a trend shift coinciding with the collapse of Terra Classic. While 2021 was characterized by an ever-declining Ethereum TVL dominance as more L1s and L2s emerged, 2022 marked a bottom in May at 49.8% indicating a saturation of blockspace. Since then, Ethereum’s TVL dominance consistently climbed back up to ~58%.

As blockspace scarcity dwindles with more L1s and L2s on the battlefield, most monolithic and multi-monolithic chains suffered from a lack in revenue and blockspace demand. As of writing Polkadot, Ripple, Stellar, EOS, Ethereum Classic, Litecoin and Monero have a combined market cap of almost $40b, yet only processed daily transactions worth $4’000 while Ethereum did more than $2’900’000. For instance, Polkadot also saw a steep drop-off in winning bids for parachain slots, down to an average bid of $0.69m in Q4 2022 from average bids of up to $109m in November 21[43]. Illustration 14 provides key metrics for selected protocols ranging from monetary policy, revenue, and decentralization.

As shown in Illustration 14, Ethereum’s post-Merge inflation adjusted yield (nominal staking yield - inflation rate) is among the highest of all leading smart contract platforms. These yields will also influence the floor for DeFi lending rates due to arbitrage. The tokenomics of Avalanche, Solana, and Ethereum differ, but the underlying model shared by each of these networks has a burn mechanism to validate transactions and thus impact the net inflation. The rather high staking yields of Polkadot, Near, and Cosmos indicate a high inflationary monetary policy that dilutes users that don’t opt to stake. The adjusted yields are outlined for the lowest barrier of entry staking solutions such as delegating to staking pools. That’s how delegating stake in Cardano even yields negative returns if adjusted for inflation.

We expect that adjusted yields on Ethereum face headwinds in ‘23 as withdrawals get enabled in March. Notably, the staking ratio of Ethereum still ranges lowest by a significant margin compared to other PoS platforms. Among the smart contract platforms, Ethereum remains the central hub for novel applications and disruptive technology. To date, it’s the blockchain with the most weekly active developers (2’199)[44], measured in number of distinct developers tagged to open-source repositories with at least one repository commits per week, ahead of Polkadot (1’074) and Cosmos (656). It also has almost 70x more validators than all outlined PoS protocols in Illustration 14 combined. Blockspace demand driving revenue is a reliable sign of a robust and healthy network. On a smart contract platform, the cumulated transaction fees and network revenue are therefore directly correlated. The lower the Price-toSales (P/S) ratio value, the better. Ethereum yields the lowest and Polkadot the highest P/S value. As rollups offer unique benefits while sourcing the full security of Ethereum’s decentralized trust pool, we expect sustained rollup adoption that becomes a new breeding ground for both DeFi and NFT innovation alike. Not only looming rollup airdrops but also the launch of a multitude of zk-rollups forged by Polygon, Scroll, Starkware or Matter Labs will heat up the rollup race in ’23 and boost EVM dominance. They will enable a new level of data privacy,, efficiency, identity use cases, social networks, voting and games. Their complexity and maturity could leave them more vulnerable to centralization and security vectors in the short-term, however. While the EVM continued to dominate among smart contract platforms (83% of overall TVL), a growing number of alternative execution environments and appchains was present as well. We expect that 2023 will bring more clarity around the most permeating blockchain design. While the L1 narrative loses steam, promising blockchain architecture paradigms such as multi-monolithic and modular approaches like Celestia line up to compete. Cosmos and Polkadot allow liquidity from appchains to flow between previously siloed ecosystems while L3s allow application specific execution layers on top of L2s that can provide the base layer security of Ethereum. The era of Ethereum killers seem to fossilize and alternative L1s will rather compete with L2s.

Continued momentum of L2s and the synergy emerging with Ethereum’s roadmap towards modularity will likely reinforce its position as the dominant smart contract platform. While we might see a giant blend condensed in a multi-modular blockchain future, its most important modular component, being its substantial pool of decentralized trust, will be leveraged via restaking primitives such as EigenLayer, Therefore, Ethereum will maintain its gravitational pull towards users, developers, and innovation going forward. As rollup technology is still immature, it usually comes with a basket of risks[45]. It is tainted with security and trust assumption such as upgradeability, sequencer or validator failure, mechanisms available to force an exit, multisigs or a varying reliance on the fraud or validity proofs. We expect to see substantial progress on that front indicated by e.g. Arbitrum decentralization upgrades or external sequencers like Stackr Network[46] or Espresso, a middleware[47] that is able to replace an internal, centralized sequencer. Eventually, they will close the gap and achieve to inherit the full security guarantees of Ethereum. Rollups currently also lack cross-L2 interoperability that we consider to be of major importance. Composability and liquidity fragmentation will be major challenges as we face adoption. Regarding scalability, the data availability (DA) bottleneck is being targeted by the upcoming Proto-Danksharding that will unlock a part of the peak theoretical performance of rollups. Heading into the next cycle, we consider rollups to be key infrastructure as they significantly enhance speed and cost without sacrificing security and decentralization – a true contender for solving the blockchain trilemma.

Fat ecosystem

In the last two years, we saw a drift from fat protocol to fat application. The fat application thesis argues that value tends to primarily accrue to the protocol instead of the application layer. In contrast, web2 represents fat application where most value accrues to applications built on top of web2 infrastructure. Taking the Ethereum ecosystem as a proxy, we observe that the fat application thesis took over with the rise of DeFi and NFTs, as Illustration 15 indicates. Overall, $330b in asset value lives on Ethereum. Only 44.5% is made up of Ethereum’s native asset ETH while the majority resides in ERC20s, making up 49% of the total value secured. Notably, all this value is currently secured by 15.9m ETH or $19.3b, leading to a security ratio of 17.1 times.

The Outlook

The negative effects of various CeFi collapses hit hard in ’22 while a hazard around other major players is still looming. Yet, crypto is a tough cookie and we are cautiously optimistic about 2023 being a decisive year for the industry. While Ethereum pulled off a seminal moment in blockchain history with the Merge, it elevated its sustainability objectives, amplified its supply dynamics towards negligible issuance and redesigned its security model along a major efficiency improvement. Shipping the Merge heavily fed into Ethereum’s value proposition and will act as a confidence catalyst for further implementations of its ambitious roadmap. In 2023, we expect a vortex of upgrades that will initially enable withdrawals via the Shanghai and Capella upgrade. Following up, none other than Proto-Danksharding will hit Ethereum’s mainnet, that in a first iteration will optimize Ethereum’s blockspace into a data availability engine. This paves the way for full-fledged outsourced execution via Ethereum’s rollup centric roadmap and bulletproofs the network for the modular blockchain age. We expect more awareness and progress towards censorship-resistance and a flight to self-custody. Likewise, we will see a continued battle, be it via internal or external infrastructure, towards optimizing MEV that is considered to be the Millenium Prize Problem of the industry. As Ethereum strives towards long-term protocol ossification, restaking primitives will unlock synergy effects enabling the fat ecosystem and further underpin Ethereum’s widely developed and capital heavy base layer. As multiple narratives converge to shape the future of blockchain architecture, anyone following the industry has all the reasons to be excited.

The author thanks Denis Oevermann for the important and valuable support creating the charts.

Disclosure: at time of writing, the author holds ETH, NEAR, XTZ, SWISE, RPL, MATIC, AVAX and ATOM.

Sources

[1] [https://arxiv.org/ abs/1710.09437](https://arxiv.org/ abs/1710.09437)

[2] [https://www.galaxy.com/ research/insights/tags/ ethereum](https://www.galaxy.com/ research/insights/tags/ ethereum)

[3] [https://arxiv.org/ pdf/2003.03052.pdf](https://arxiv.org/ pdf/2003.03052.pdf )

[4] [https://whitepaper.io/ document/139/peercoinwhitepaper](https://whitepaper.io/ document/139/peercoinwhitepaper)

[5] [https://kb.beaconcha.in/ glossary](https://kb.beaconcha.in/ glossary)

[6] [https://vitalik.ca/general/2020/11/06/pos2020. html](https://vitalik.ca/general/2020/11/06/pos2020. html)

[7] [https://www.theblock.co](https://www.theblock.co/ post/197861/bitcoin-mining-hashrate-declines-more-than-30-amid-americasbig-winter-storm)

[8] [https://ethereum.org/en/ developers/docs/consensus-mechanisms/pos/weaksubjectivity/](https://ethereum.org/en/ developers/docs/consensus-mechanisms/pos/weaksubjectivity/)

[9] [https://carbon-ratings.com/ dl/eth-report-2022](https://carbon-ratings.com/ dl/eth-report-2022)

[10] [https://twitter.com/ WuBlockchain/status/1552837630278385664](https://twitter.com/ WuBlockchain/status/1552837630278385664)

[11] [https://charts.coinmetrics.io/ network-data/](https://charts.coinmetrics.io/ network-data/)

[12] [https://2miners.com/ ethw-network-hashrate](https://2miners.com/ ethw-network-hashrate#:~:text=Ethereum%20 PoW%20network%20hashrate%20reflects,505%20 813%20633%20h%2Fs)

[13] [https://twitter.com/ VitalikButerin/status/](https://twitter.com/ VitalikButerin/status/ 1570299062800510976?s =20&t=a-zD5hbswn_xSXgYYksvzg)

[14] [https://public.wmo.int/ en/media/press-release](https://public.wmo.int/ en/media/press-release/ eight-warmest-years-record-witness-upsurge-climate-change-impacts)

[15] [https://ethereum.org/en/ desci/](https://ethereum.org/en/ desci/)

[16] [https://eth2book.info/altair/ part2/incentives/issuance](https://eth2book.info/altair/ part2/incentives/issuance)

[17] [https://www.theblock.co/ data/on-chain-metrics/ ethereum](https://www.theblock.co/ data/on-chain-metrics/ ethereum/cumulative-value-of-burned-eth-aftereip-1559)

[18] [https://coinshares.com/ research/ethereum-stakingyields](https://coinshares.com/ research/ethereum-stakingyields)

[19] [https://eth2book.info/altair/ part2/incentives/rewards](https://eth2book.info/altair/ part2/incentives/rewards)

[20] https://messari.io/asset/ethereum/chart/txn-fee-avg

[21] [https://www.wsj.com/ articles](https://www.wsj.com/ articles/ethers-new-staking-model-could-drawsec-attention-11663266224)

[22] [https://home.treasury. gov/policy-issues](https://home.treasury. gov/policy-issues/financial-sanctions/recent-actions/20220808 )

[23] [https://ethereum.org/en/ developers/docs/consensus-mechanisms/pos/attestations](https://ethereum.org/en/ developers/docs/consensus-mechanisms/pos/attestations/)

[24] [https://twitter.com/ethereumJoseph/status]( https://twitter.com/ethereumJoseph/status/1596198 718339948552?s=20&t=d eigZW4AUrFsowqTXPQJig)

[26] https://operators.lido.fi/

[27] https://clientdiversity.org/

[28] [https://www.rated. network/?network=mainnet&view=pool](https://www.rated. network/?network=mainnet&view=pool)

[29] https://ethresear.ch/t/burning-mev-through-blockproposer-auctions/14029

[30] https://members.delphidigital.io/reports/the-hitchhikers-guide-to-ethereum

[31] [https://twitter.com/peter_szilagyi/status](https://twitter.com/peter_szilagyi/status/156305160384 6115328?s=20&t=3Au0sHQ9o98TpSKH2pWmdQ)

[32] https://obol.tech

[33] https://ssv.network

[34] https://explore.flashbots.net

[36] [https://twitter.com/VitalikButerin/status](https://twitter.com/VitalikButerin/status/1588669782 471368704?s=20&t=7dNB kxuW7iP4k20_HDqEug)

[37] [https://ethereum-magicians. org](https://ethereum-magicians. org/t/a-rollup-centric-ethereum-roadmap/4698)

[38] [https://eips.ethereum.org/ EIPS/eip-4337](https://eips.ethereum.org/ EIPS/eip-4337)

[39] [https://l2beat.com/scaling/ tvl/](https://l2beat.com/scaling/ tvl/)

[40] https://l2beat.com/scaling/activity

[41] https://ethtps.info/

[42] https://defillama.com/chains

[43] https://parachains.info/auctions

[44] https://www.gokustats.xyz/developers

[45] https://l2beat.com/scaling/risk

[46] [https://mobile.twitter. com/0xstacked](https://mobile.twitter. com/0xstacked)

[47] [https://www.espressosys. com/blog](https://www.espressosys. com/blog/decentralizingrollups-announcing-theespresso-sequencer)

[48] [https://messari.io/report](https://messari.io/report/ eigenlayer-to-stake-and-restake-again)