Striking the Right Balance in Regulating Crypto

23.02.2023 - 6 Minuten Lesedauer

by Dr. iur. Cansu Burkhalter, Dr. iur. Fabio Andreotti, Oliver Gehrig

Since the emergence of Bitcoin in 2009, the adoption of crypto assets has grown rapidly, and they have become an integral part of the global financial system. Rapid proliferation of such new assets has triggered repeated calls for regulation. Regulatory concerns to date have focused mostly on consumer protection, anti-money laundering, countering terrorist financing and potential transmission channels to financial stability risk.

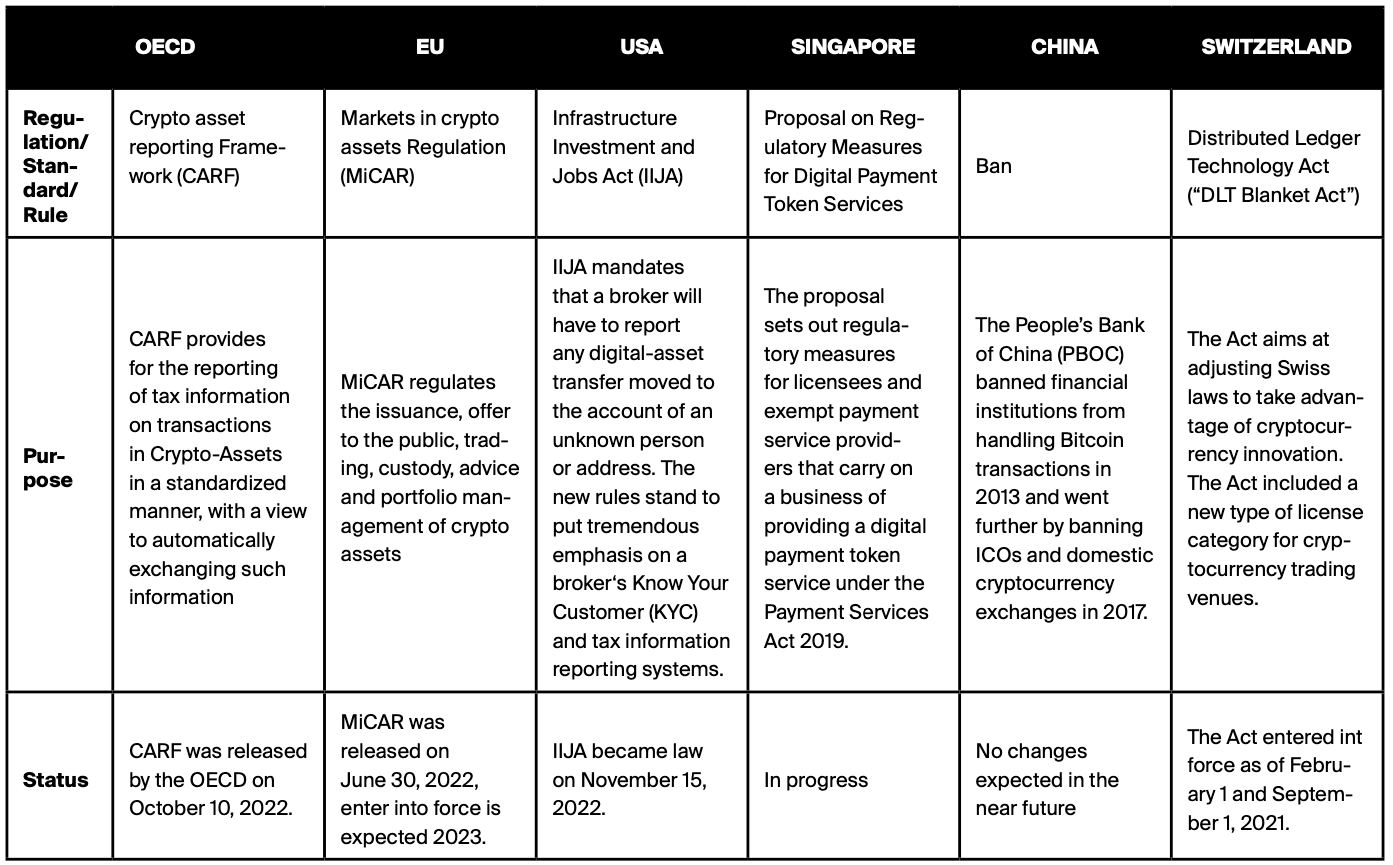

Policymakers worldwide struggle to monitor risks and implement consistent regulations in this rapidly evolving sector. Today, regulatory measures vary significantly by country: outright bans towards crypto exchanges in China or against privacy tokens in South Korea, consumer protection initiatives and certain regulatory guidance from US court rulings, a tax reporting standard from the Organisation for Economic Co-Operation and Development (OECD), anti-money laundering regulations from the EU, warnings about the risks of initial coin offerings (ICO) and regulatory approvals of crypto exchanges in Japan as well as adoption of Bitcoin futures contracts in the US.

Looking at the developments domestically, Switzerland became a stronghold for the crypto industry due to the neutral stance adopted by Swiss regulators regarding new and emerging technologies. Switzerland was one of the first countries to enact legal regulations for blockchain technology. Moreover, the Swiss Federal Tax Administration has clarified the taxation of crypto- currencies through a working paper in 2019, generally subjecting them to wealth tax and in some instances

income tax in a fair and transparent manner, thereby removing any ambiguity concerning taxation of crypto assets. Such initiatives create reliable and clear rules- based frameworks.

Crypto has also been associated with fraud and undue exuberance since its emergence. The early days of crypto were marked by hype and speculation, which led to the ultimate failure of some projects, causing financial losses for investors due to the lack of clear regulations. How- ever, as the industry has matured, we have seen many new successful projects offering genuine technological innovation. Regulations that are not unduly biased by bad actors but maintain a constructive approach towards an orderly integration of crypto assets into the existing financial system are key to promote further growth of the crypto industry.

Proportionality and technology neutrality are the core tenets of crypto regulations. A technology-neutral approach should be pursued regarding the regulatory treatment of blockchain activities that is proportionate to the level of risk. Wherever possible, any differences in legal treatment should arise from (and be tailored to) material differences in the business or risks associated with the technology. Prematurely created regulations that are excessively broad and overly complex would stifle the further adoption of crypto assets as a key component of the financial services industry.

Meanwhile, it should take account of novel features of crypto assets and harness potential benefits of the underlying technology. Both traditional finance (TradFi) and crypto finance adhere to similar principles with respect to addressing anti-money laundering (AML) and countering the financing of terrorism - but not always through identical rules.

An effective regulatory framework should ensure that crypto asset activities posing similar risks as traditional financial activities are subject to the same regulatory outcomes.

International Regulatory Developments

Crypto Asset Reporting Framework (CARF)

Unlike traditional financial products, crypto assets can be transferred and held without the intervention of an established financial intermediary and without any central administrator having full visibility on either the transactions carried out or on the crypto asset holdings. Therefore, crypto assets can be perceived as undermin- ing existing international tax transparency initiatives, such as the Common Reporting Standard (CRS).

Many jurisdictions have already established reporting regimes requiring virtual asset service providers to report transactions to both the agencies in charge of combating money laundering and the financing of terrorism, as well as tax administrations. However, countries do not currently have information on operations carried out through crypto exchanges located abroad, since such exchanges are not obliged to share information with central banks, tax authorities or other public bodies.

In October 2022, the OECD released a stand-alone framework for the automatic exchange of information on crypto assets, the so-called Crypto Asset Reporting Framework (CARF), which ensures that crypto asset transactions are brought into information reporting rules. The CARF mirrors many of the reporting requirements of the CRS regime and introduces sweeping new third-party information reporting requirements for crypto assets that far exceed the CRS reporting obligations imposed on traditional financial assets and market participants.

The definition of crypto assets targets those assets that can be held and transferred in a decentralized manner, with- out the intervention of traditional financial intermediaries, including stablecoins, derivatives issued as crypto assets, and certain non-fungible tokens (NFT). The definition is meant to ensure that all assets covered under the new tax reporting framework also fall within the scope of the Financial Action Task Force (FATF) recommendations, ensuring intermediaries’ due diligence requirements can build on existing anti-money laundering (AML) and know- your-customer (KYC) obligations. The following four types of relevant transactions are reportable under CARF:

- Exchange from crypto assets to fiat currencies and vice versa

- Exchange from and to different forms of crypto assets

- Reportable retail payment transactions above USD 50’000; and

- Transfers of crypto assets.

The OECD will continue working with participant countries and industry stakeholders to ensure that CARF will be implemented consistently globally. It is expected that countries will start transposing CARF into national law as of January 1, 2026. The European Union has already released the proposal for the directive which will cap- ture the requirements brought by CARF.

Markets in Crypto Assets Regulation (MiCAR)

Most crypto assets do not qualify as financial instru- ments within the definition of the respective European Union (EU) regulation, the Markets in Financial Instru- ments Directive (MiFID). For all crypto assets that are not considered financial instruments, there is no uni- fied European regulation so far. Therefore, there still exists market fragmentation within markets governed by national regimes, without the possibility of the free- dom of service by means of passporting crypto services throughout the European crypto space, as it is possible for TradFi institutions such as banks. This fragmentation also implicates the unintended consequences of regulatory arbitrage and uncovered risks. Addressing the above-mentioned shortcomings, the EU authorities are in the final stage of the legislative process to issue a landmark crypto asset regulation – the MiCAR.

MiCAR will bring uniform European requirements for crypto asset issuance. For instance, issuers must publish a white paper for investors containing specific information about the crypto assets to be issued. MiCAR also regulates the liability of issuers. It defines crypto assets as a digital representation of a value or right that can be traded via a distributed ledger (e.g., a blockchain). Crypto assets that are not redeemable and that represent a unique real asset – known as non-fungible tokens – fall outside the scope of MiCAR. The same applies to crypto assets with the same characteristics as existing financial products or instruments. This means that tokenized securities and other instruments are covered by existing MiFID rules. Stablecoins, however, do fall within the scope of MiCAR: Specific and additional rules will apply to issuers of stablecoins, especially regarding the assets that serve as reserves. MiCAR distinguishes between stablecoins whose value is linked to multiple fiat currencies, commodities, or crypto currencies (known as Asset-Referenced Tokens, ARTs) and stablecoins whose value is linked to the value of a single fiat currency (Electronic-Money Tokens, EMTs).

Alongside crypto assets and their issuance, MiCAR also regulates certain crypto services. These include operating trading platforms, exchange services (crypto to crypto or regular currency) and custody services for crypto assets. The professional provision of advice and portfolio management services for crypto assets are also considered crypto services by MiCAR. Providers of crypto services must obtain a license from a financial supervisor within the European Economic Area (EEA) or EU and comply with consumer protection as well as with disclosure requirements. Their governance struc- tures and information security systems must be in order, they must detect and respond appropriately to conflicts of interest, have a complaints procedure and provisions on outsourcing in place. Transaction service providers must also put in place effective systems and procedures to detect market manipulation.

Under MiCAR, issuers of stablecoins or anyone offering crypto services must obtain a license to do so from their domestic financial supervisor within the EEA or EU. This license allows MiCAR-regulated activities to be undertaken in all EEA countries. The MiCAR reg- ulations are currently being finalized and are expected to come into force in the coming months. MiCAR rules for issuing stablecoins are expected to come into force 12 months after publication, the other regulations after 18 months. In addition, European Supervisory Authorities (ESAs) are anticipated to soon start developing detailed technical standards for implementing the new rules. The new MiCAR rules are expected to take effect in 2024.

Regulatory Developments in Switzerland: Custody

Swiss lawmakers have been quick to recognize the new opportunities offered by blockchain and DLT technology. The way blockchains and cryptography work enables property-like legal implications as in the physical world. Clearly, the most important part of the so-called “DLT Blanket Act”, a new piece of legislation adopted in 2020, has been the clarification of what happens to crypto assets of clients in the event of bankruptcy of a Swiss crypto custodian. Extensive discussions paved the way for Bitcoin (BTC), Ether (ETH) and all the other crypto assets to now enjoy the same bankruptcy protection as physical objects.

When it comes to crypto custody from a legal perspective, we can distinguish three main cases:

In the first case, the client has exclusive control over his or her crypto assets. Even if the client relies on wallet software run by a third party, the client will not have to take legal action against that third party in the event of bankruptcy. In the second case, the custodian and the client have shared control over a crypto asset belonging to the client. The fact that the custodian also has a relevant cryptographic key to control the assets does not change the legal situation in the event of bankruptcy. Ownership of the assets firmly remains with the client even after the opening of the bankruptcy proceedings. Finally, in the third case, the custodian has sole control over a crypto asset belonging to the client. According to the recently revised Swiss Act on Debt Enforcement and Bankruptcy, if the custodian undertakes to always keep the crypto assets available for its clients and the crypto assets are individually assigned to them, their crypto assets are fully protected in the event of bankruptcy of the custodian. In such a case, clients would have a direct claim against the bankruptcy estate to hand over the crypto assets in kind. In other words, clients who held BTC before the opening of bankruptcy proceedings would eventually receive their exact BTC back. In addition, such custody works much like a segregated account at a traditional bank because company funds are not commingled with clients’ assets on the blockchain

At Bitcoin Suisse, we refer to the third case as Separated Custody. As described, this type of custody ensures that client assets are bankruptcy remote. We offer Separated Custody in two versions with different features: Clients with a Bitcoin Suisse Crypto Account generally have their assets stored on client-specific blockchain addresses; clients with a Bitcoin Suisse Vault Account have permanently assigned blockchain addresses and retain as much control as possible within a custodial environment. On the other hand, if client assets in the Bitcoin Suisse Crypto Account are held in Collective Custody, they are generally fully protected by a default guarantee from a Swiss bank as required by Swiss banking laws (certain groups of clients may be exempted according to current regulation – however, this does not affect their crypto assets held in Separated Custody).

Unlike cases like Mt. Gox where former clients are still waiting for their payouts and will likely only get an equivalent amount in fiat, clients holding their assets in Separated Custody with a Swiss custodian must not fear that their crypto assets fall into the bankruptcy estate or are converted into fiat claims against their will. We can therefore conclude that Swiss lawmakers have solved a crucial matter of the crypto industry in a very efficient and customer-friendly way. At Bitcoin Suisse, we have worked hard to take advantage of the new rules for the benefit of our clients.

Application of Existing Regulatory Standard to Crypto: BEX/FIDLEG

Legal and Regulatory Basis

The duty of Best Execution derives from both private and supervisory law. Under private law, the Best Execution principle is based on contract law. Service providers who execute orders on behalf of their clients typically have a legal relationship with their clients that is governed directly or by analogy by agency contract law or the like. Accordingly, the service provider owes the client loyalty and care when executing transactions assigned to him. For financial service providers to which the Swiss Financial Services Act (FinSA) applies, this principle is further specified in art. 18 FinSA. Thus, financial service providers subject to the FinSA must ensure that the best possible result is achieved in terms of cost, time and quality in the execution of their client orders.

Even though Bitcoin Suisse is currently not subject to the FinSA, we are committed to adhering to Best Execution industry standards known from traditional finance to achieve the best possible outcome for our clients.

Best Execution in TradFi vs. Crypto

To ensure a proper trading process and investor protection, end clients and certain service providers representing such end clients do not have direct access to the markets on which specific products are traded. Consequently, these market participants must rely on the services of third parties. Client orders shall be executed in such a way that the best possible result for the client is achieved. In particular, the third-party provider shall promptly conclude client orders at the best possible market price at a generally recognized, suitable execution venue that guarantees the orderly execution of the transaction, considering the limits, conditions and restrictions set by the client. When executing the order, the service provider shall strive to achieve the best possible overall result for the order in question.

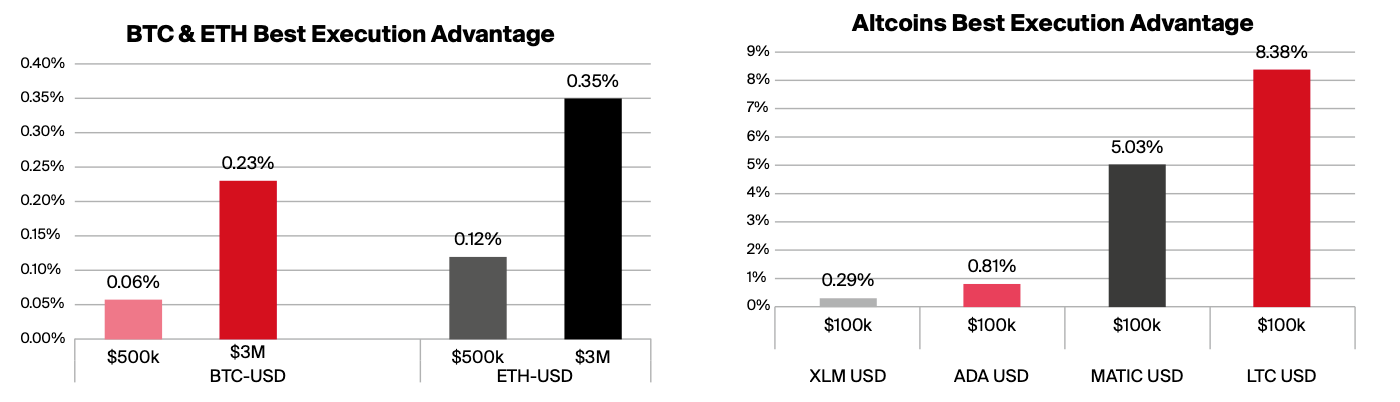

In both TradFi and crypto, Best Execution refers to the practice of executing transactions at the best possi- ble price, considering factors such as speed, cost, and likelihood of execution. This is typically accomplished using advanced trading tools and algorithms that provide access to a wide range of liquidity sources. Achieving Best Execution in crypto can be difficult due to its complex landscape of centralized exchanges, decentralized marketplaces, and the corresponding counterparty and protocol exposure. While the principles of Best Execution are similar in both TradFi and crypto, the approaches and strategies for achieving it can differ significantly. To successfully achieve Best Execution in this environment, it is necessary to have a deep understanding of the underlying markets and the industry.

Best Execution. Applying Best Execution does come with many considerations, simply hitting the best price on the market does not guarantee Best Execution. The likelihood and speed of execution are also crucial factors to be considered. Looking at order book depths, identifying the best trading venue(s) to execute while maintaining a sound and tight counterparty exposure is key for being able to deliver Best Execution. The following paragraphs focus on selected practical aspects of how to ensure that our clients get the best possible results when trading with Bitcoin Suisse.

Liquidity. There are two types of liquidity most rel- evant to executing trades: market liquidity (how much can you trade at a given price x?) and funding liquidity, which is required by the trade venue to allow trading and settlement.

Market liquidity varies heavily depending on the token to be traded. Large trades, if not executed in a smart way, potentially cause material price changes. A diversified network of crypto trading venues (exchanges, brokers) does not only help increase the available liquidity on which can be traded but also allows to trade tokens that are not extensively listed across crypto markets. The most liquid order book does not help if there are no funds available on the account to trade with. Managing funding liquidity is a key feature of our Best Execution approach. But how much should one hold on to a single trading venue anyway?

Trading Venue. To select a trade venue and determine a prudent counterparty risk limit for it, Bitcoin Suisse applies its proprietary counterparty risk methodology. In simple terms, that means qualitative and quantitative factors are assessed and added up and the result is being assigned to a risk tier.

All our trading venues must fulfill certain minimum criteria to be onboarded as eligible trading counterparty. Since we are taking over the counterparty risk for our clients, we put our own capital at risk to protect our customers. Our various order types allow Best Execution trading for customers considering their preferences on how to execute. A principal order is a trade versus Bitcoin Suisse’s own books. At the time of the trade, we scan available liquidity across the different order books from our trade venues and compile the best bid/ask price for the asset in the form of a snapshot. If the customer decides to trade, the compiled price is locked in, and the trade is instantly settled. This form of order is best suited for immediate trades as execution is instant. The client has funds available in the account directly after trading, as Bitcoin Suisse is taking care of pre-funding and consequent hedging of the trade at its own risk.

For larger trades with lower time constraint, agency orders are normally the preferred choice. Under our agency model, we still protect the customer against coun- terparty risks and are able to execute the order in a way that minimizes market impact, hence achieving a better price on the order at the expense of longer execution time. Upon completion of the desired order amount, our clients get the actual traded price – which is most often better than a direct market order.

Best Execution Outlook 2023

Best Execution is an integral part of the TradFi sector. With MiFID in the European Union and FinSA in Switzerland, a lot has been done on the regulatory side to protect customers the best way possible. We strive to make this happen in the crypto space, too. If we want our markets to be competitive with traditional financial markets, we need to apply comparable standards, offer comparable client protection, and serve our customers with a high level of quality and security. Therefore, we are looking into upgrading our current Best Execution Policy to a standard comparable to MiFID/FinSA in 2023. With this step we mark our commitment towards meaningful regulation of crypto markets which profits all; the clients, the crypto space and all its participants.

Conclusion

The regulatory developments described signal that there is a clear desire to provide legal clarity. However, regulation of crypto markets is still at an early stage and there has been a lack of consistent regulation in this rapidly evolving sector across different countries, with some implementing outright bans and others adopting more supportive measures. Highly heterogeneous international regulatory requirements and uncertainties regarding the evolution of regulation can make it difficult to operate a crypto financial services provider. In addition, crypto markets are currently going through turbulent times.

Crypto markets are going through very similar if not the same events as TradFi, however with a speed factor of 10x. It is key to review the lessons learned from TradFi and apply the good parts for crypto, too.

Lothar Cerjak, Chief Trading & Brokerage Officer

To promote the growth of the crypto industry, it is important to implement globally harmonized regulations and regulatory frameworks to be proportionate and technology neutral, considering the risks and benefits of crypto assets, and applying similar regulations to activities with similar risks as traditional financial activities. Switzerland has taken a neutral stance towards crypto assets and has implemented clear regulations for blockchain technology and the domestic taxation of cryptocurrencies, which has made it a hub for the industry.

At Bitcoin Suisse, we see our role not only in adhering to existing rules, but also in pioneering regulation and helping the industry to find standards that enhance customer protection and mature the crypto market. We believe that prudent and sensible regulation is paramount to the sustainable growth of crypto.

The authors would like to thank Julien Binder, Markus Perdrizat and Ronnie Studer for their contribution to the research and writing of this article.

Bitcoin Suisse