Listen to the Weekly Wrap on Spotify and Apple Podcasts. It is a summary with the help of AI-voices.

This Week’s Top Stories

“Trump announces Powell’s successor, Kevin Warsh.” – Friday, 30 January 2026

- Last Friday afternoon, US President Donald J. Trump announced he is nominating Kevin Warsh as Chairman of the Federal Reserve Board.

- During his previous five-year term as a Fed governor, Warsh earned a reputation as an inflation hawk and a critic of the Fed's large-scale bond holdings, used to help lower mortgage and other long-term interest rates as a permanent tool of monetary policy.

- In recent months, Warsh has advocated for lower rates, arguing that an AI induced GDP boom is setting the stage for speedy growth without troublesome inflation, publicly agreeing with Trump that the Fed should sharply lower interest rates.

“Due to the House being in recess, the US government entered a technical, partial shutdown last Saturday.” – Saturday, 31 January 2026

- The US government went into a technical, partial shutdown on Saturday evening after a funding bill failed to pass in time. While the Senate approved a $1.2 trillion appropriations package, the House was in recess and did not vote on it until early this week, passing the package on Tuesday and ending the shutdown after just two days.

- Trump and Democrats now have two weeks to strike an agreement on how to rein in federal law enforcement, specifically Immigration and Customs Enforcement, or face another shutdown for the department, which includes agencies from TSA to FEMA.

A Quick Crypto Overview: The worst BTC daily candle since FTX

The crypto market continued to trade to the downside last weekend, with Bitcoin losing more than 5 percent on a low volume Saturday evening, after already trading to the downside during the previous week. Saturday’s downturn shook up the markets quite a bit, and while there was a period of sideways price action at the beginning of the week, many market participants already feared the worst.

As we mentioned in last week’s Wrap, a sustained move below the $80’000 level was the signal for another acceleration to the downside, and the correction continued yesterday, Thursday, with Bitcoin closing the day with a 14 percent loss, the highest daily loss since the FTX collapse back in November 2022.

At the time of writing, Bitcoin is down 15 percent on the week, Ethereum is down 16 percent since Sunday, and Solana has a weekly loss of 21 percent. Let’s look at some of the possible catalysts behind this recent correction.

The last few weeks were packed with new developments in various areas, be it geopolitical, macroeconomic, or crypto-specific. Recent months have seen significant selling pressure from long-term BTC holders, accompanied by the drying up of ETF and DAT flows, all while the crypto market still seems to suffer from the consequences of the 10/10 crash. Let’s dive into some of the most recent headlines below.

Trump announces Powell’s successor Kevin Warsh

While we expect Warsh to be stimulative for lower than consensus rate cuts, he is strongly opposed to FED balance sheet expansion/QE, that can play a vital role in upside momentum. We overall view the new FED nominee as constructive for digital assets.

Market structure bill delayed as crypto industry continues to clash with banking lobby

Over the past two weeks, it became increasingly clear that a decision on the CLARITY Act will likely be pushed back several weeks as key lawmakers shift their focus to potential housing legislation in support of President Donald Trump’s affordability push. On January 14, Brian Armstrong, Coinbase CEO, announced that the company is pulling its support for the bill as written. He mentioned various amendments that would de facto ban tokenized equities or kill rewards on stablecoins as the reasoning behind the decision. Should stalled negotiations resolve and clarity be passed into law, it could serve as a potential catalyst for digital assets.

Bitcoin Hash rate is taking a hit as miner exodus accelerates

Bitcoin’s total network hashrate has dropped significantly over the past few months in its largest decline since 2021, after severe US winter storms forced major miners to shut down operations. The hashrate has fallen roughly 25 percent from its high. The winter storm has reinforced an existing trend, as mining firms are repurposing facilities for AI data centers, where margins are higher and revenue is more stable than in BTC mining. The recent decline in Bitcoin’s price has had a direct impact on the profitability of miners, and many of them are currently operating under stressed conditions.

Digital asset investment product flows

The last two weeks were accompanied by large outflows from digital asset investment products, flipping YTD flows to a net outflow of $1 billion and a decline of more than $70 billion in AuM since the October 2025 highs. Across the major crypto assets, the negative sentiment last week was broad, with Bitcoin seeing $1.32 billion in outflows, Ethereum $308 million, while recent favorites XRP and Solana also saw outflows of $43.7 million and $31.7 million, respectively.

Crypto liquidation figures

Over the past weekend, more than $2.5 billion was liquidated, mostly on the long side. While $2.5 billion is a large number of liquidations, the third largest since the beginning of 2025, it still does not come close to last October’s total liquidation amount of almost $20 billion on October 10, 2025. Nonetheless, Saturday’s liquidation event has entered the top 10 largest crypto liquidation events of all time. During the past 24 hours, an additional $2.6 billion were liquidated from the markets, again mostly long positions, with $2.1 billion in longs and $475 million in shorts wiped out by the correction.

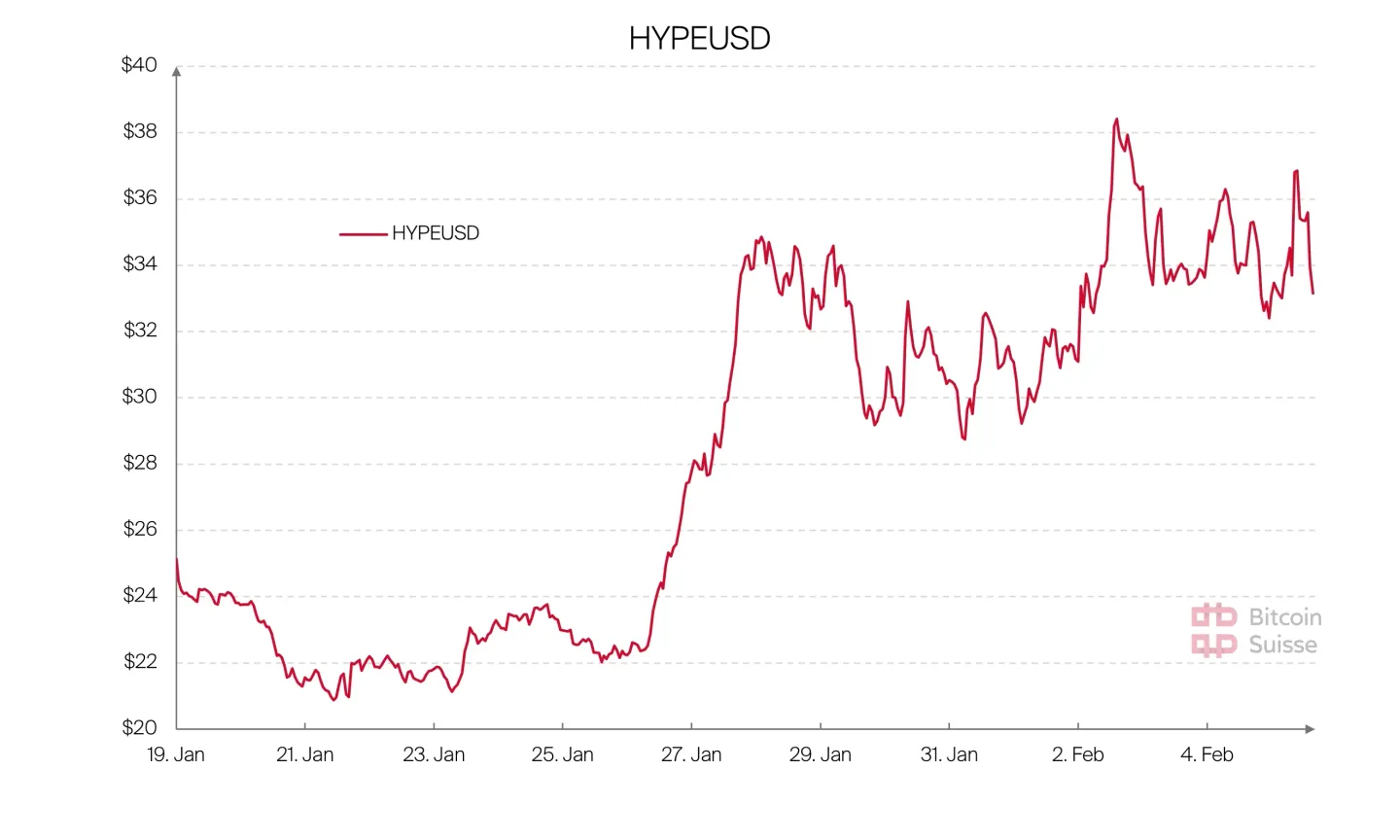

Chart of the Week: Hyperliquid

One of the projects standing out over the past two weeks is Hyperliquid, with the HYPE token up more than 60 percent since 21 January 2026. The Hyperliquid team has recently made headlines. For example, HIP-3 markets reached new all-time highs of $1B in open interest and almost $5B in 24-hour trading volume this week, up from the previous all-time high of $800 million in open interest last week. HIP-3 allows HYPE stakers holding a minimum of 1 million HYPE tokens to launch perpetual futures markets on the Hyperliquid blockchain. Providers such as Kynetiq, with their product Markets.xyz, have started launching various RWA perps, and the recent hype surrounding commodities and onchain stocks trading led to a significant increase in volume and open interest on Hyperliquid.

The recent market activity led to increased trading volumes on Hyperliquid, which in turn resulted in large amounts of fees on the platform, with $7.5M in 24-hour fees and $32.5M over the past seven days. Due to Hyperliquid’s revenue flywheel mechanism, most of these fees directly benefit token holders through the buyback and burn program