Airdrops and Forks – Free Money?

Nov 10, 2020

29 September 2020

Uniswap, a decentralized exchange using an automated market maker (AMM) model, recently surprised the crypto community with the launch of their UNI governance token, airdropping it to all users that have used the protocol prior to September 1. Each Ethereum address that had interacted with the Uniswap contracts was eligible for claiming at least 400 UNI tokens, with loyal liquidity providers receiving much higher amounts. At UNI’s all-time high valuation of $8.40, this amounted to $3’360 worth of UNI tokens, and at current valuations is still worth around $1’800. The reasoning for this airdrop was that previous, unincentivized users of the protocol should constitute the best community to govern Uniswap in the future.

What is an Airdrop? An airdrop, in general, is the distribution of a token either through freshly minting it or directly from a treasury (such as a team’s reserve of their own token). Recipients can either be holders of other cryptocurrencies, or people who became eligible for the airdrop in other ways – such as interacting with the protocol in the past in the case of Uniswap. The goal of an airdrop is often to build awareness around a project, and to obtain a broader user base. Airdrops have been carried out both for already existing currencies (such as Stellar’s XLM) or as a mechanism to achieve the initial token distribution (UNI).

One crucial aspect that projects need to consider when airdropping coins or tokens is the prevention of “sybil attacks”. A sybil attack, in simple terms, is the creation of many identities by a single person, mostly in pseudonymous or anonymous systems (such as most public blockchains). This would allow them to obtain much more tokens during the airdrop than intended. In the case of Uniswap, this was subverted by keeping the distribution method of 400 UNI per address private, and then snapshotting a date in the past to check for eligibility. Other airdrops have attempted to prevent sybil attacks through identity checks – such as requiring participants to link their social media profiles, their GitHub account or even a full KYC check. On a cautionary note, potential airdrop participants should carefully verify the legitimacy of a project before undergoing full KYC due to the danger of identity theft.

Large Airdrops in the Past While most airdrops fail to accrue any significant value for the recipients, a few have managed to gain traction in the secondary markets and temporarily became fairly valuable.

Illustration 1: A selection of airdrops since 2016 that managed to attain significant value. The Decred (DCR) airdrop with an all-time high value of $36’500 stands out.

Besides UNI, another airdrop which was not tied to holding another cryptocurrency was the Decred airdrop, which ended on Jan. 18, 2016. Interested participants needed to sign up and shortly describe their interest in the project. In the end, 282.6 DCR were distributed to each participant. The coin attained its all-time high two years later, on Jan. 13, 2018, at $129.4/DCR – airdrop recipients who cashed out at this point got $36’500.

Bitcoin holders were eligible for two of the major airdrops listed above: Byteball (GBYTE) and Stellar Lumens (XLM). The Byteball airdrop took place on Dec. 25, 2016 and was available after signing up. 10% of the GBYTE coin supply was initially distributed, with additional airdrops afterwards, totaling 1.865 GBYTE per BTC. At all-time high valuations, this was worth around $2’200 per BTC. Stellar, on the other hand, distributed 19 billion XLM to BTC holders who signed up for it in two snapshots of the BTC blockchain (3 billion in July 2016, and 16 billion in June 2017). In total, BTC holders were able to obtain 1178 XLM per BTC, which was once worth around $1’000 (now $88). Since these two airdrops were relative to BTC holdings, they were especially lucrative for large BTC holders.

Holders of ETH also got a chunk of the pie when the OMG network (formerly OmiseGo) airdropped 140 million of their OMG token (5% of the total supply) in July 2017. Each address holding at least 0.1 ETH received an airdrop amount proportional to their share in the total ETH supply (93.1 million ETH at the time), without signing up for it. This results in 0.075 OMG airdropped per ETH – at ATH valuation worth close to $2.

Forks: A Special Form of Airdrops? Hard forks, meaning forks that are backwards-incompatible, can either take place in a contentious or non-contentious manner. The contentious variant, where part of the community disagrees on how the protocol should move forward, usually creates a second branch of the blockchain and leads to a new coin.

The Bitcoin forks are arguably the most famous ones. Bitcoin first split into BTC and Bitcoin Cash (BCH) on Aug. 1, 2017. Later, additional forks that created Bitcoin Gold (BTG) and Bitcoin Diamond (BCD) occurred in October and November 2017, respectively. Bitcoin Cash further split into BCH and Bitcoin Satoshi Vision (BSV) on November 15, 2018.

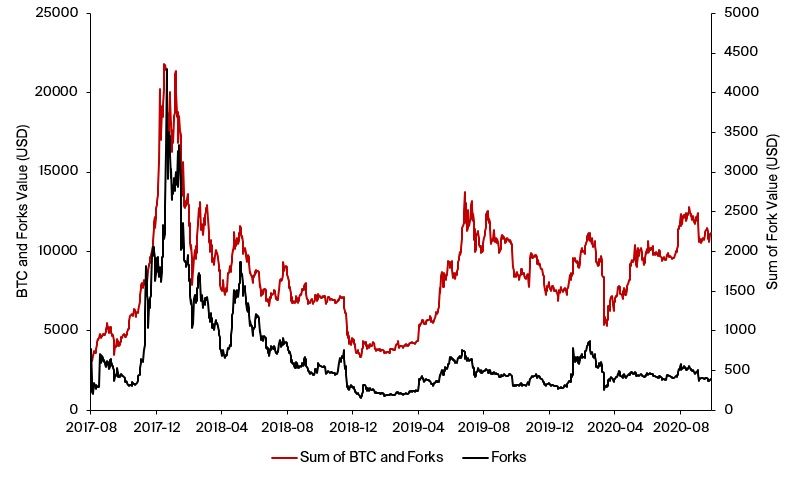

Illustration 2: During the heights of the 2017 bull run, the cumulative value of BTC forks (rhs) amounted to $4’300 per coin. Currently, the forks are worth around $400 in total.

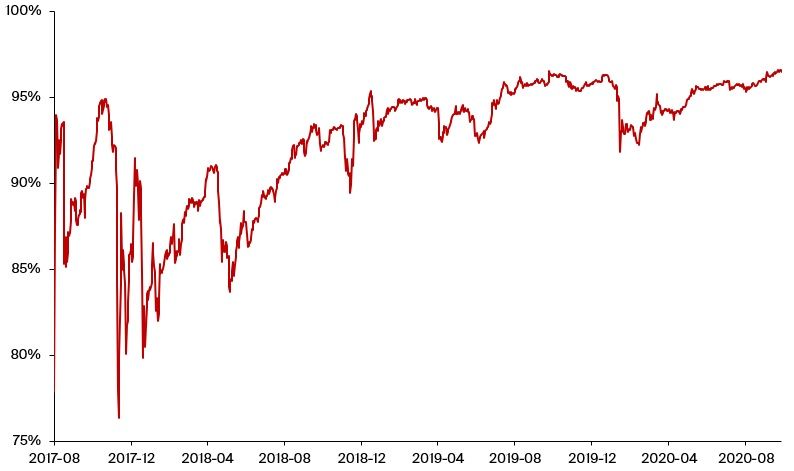

The sum of BTC and forks can be considered to be the value of a pre-August 2017 (before the BCH fork) “untouched” BTC coin, since the controller of the corresponding private key can claim her or his share of the forked coins. Another way to look at this data is to study the “BTC fork dominance”: What is the share of the value of BTC with respect to all forks?

Illustration 3: While periods following a fork appear to be more volatile (late 2017, Nov. 2018), over time, most value has accrued to BTC so far. Currently, BTC’s fork dominance stands around at 96.6%.

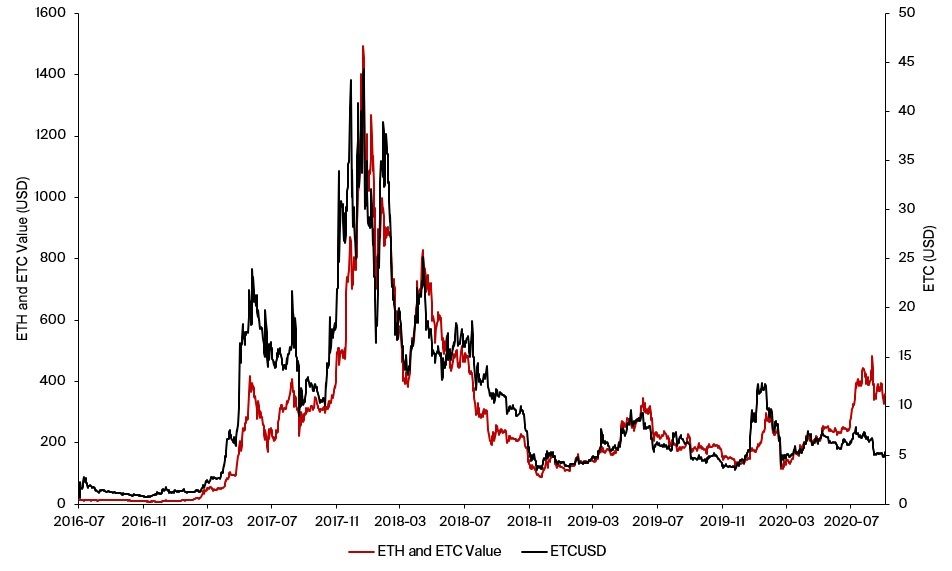

Another significant fork that led to great disputes in the community was the split of Ethereum after TheDAO in July 2016, an early experiment in building a decentralized autonomous organization (DAO). The smart contract involved was susceptible to a reentrancy attack, and 3.6 million ETH were stolen from the contract. The Ethereum community decided to do a hard fork to return this ETH, but not everyone agreed: Out of this incident, Ethereum Classic (ETC) was born, where the hacker remained in possession of the ETC.

Illustration 4: Prices of ETH and ETC have been relatively strongly correlated throughout their existence, although ETC never managed to achieve meaningful share of the overall Ethereum market cap.

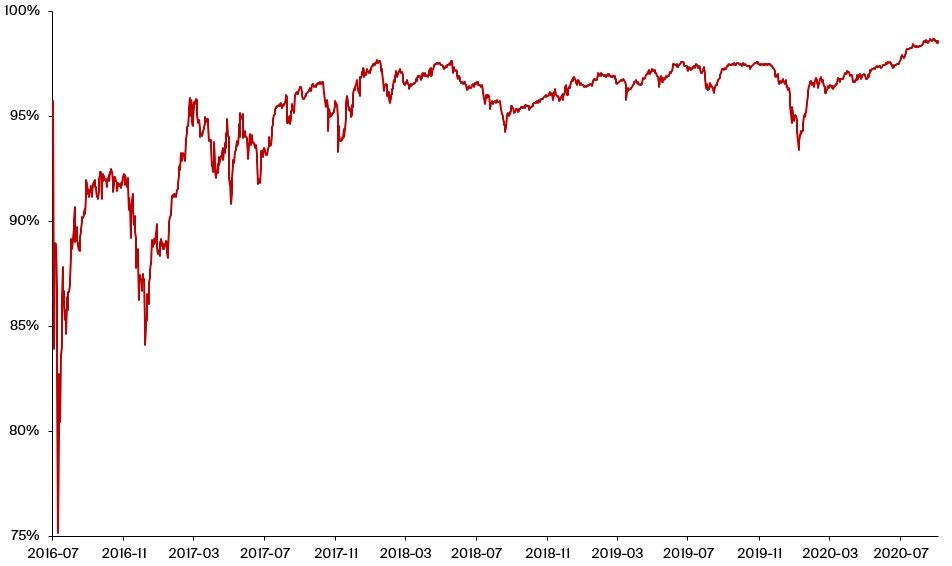

This can again be expressed differently, and perhaps more elegantly, by looking at the “ETH fork dominance”. It denominates how much of the value of a pre-July 2016 ETH coin is now captured by the current ETH.

Illustration 5: After an initial volatile phase where the ETH fork dominance dropped down to almost 75%, ETH has now captured almost all of the Ethereum market cap (currently around 98.5%)

Looking at the performance of forked coins overall, so far, the majority of the value has accrued to BTC and ETH.

Are Airdrops and Forks Printing Money Out of Thin Air? Whether airdrops and forks have value is in the hands of secondary market participants. They can be thought of similar to the recent yield farming craze for governance tokens, where APRs of >100% could be achieved that were essentially subsidized by secondary market buyers. As in any market, sustainably high prices can only materialize if long-term investors decide to provide buyside liquidity, otherwise “free money” sellers will quickly depress prices.

Not all airdrops and forks are equal, though – while many end up losing the majority of their market cap, those that can create actual value and build strong communities may lead to a justified increase in the total cryptocurrency market capitalization.