Ethereum’s Path to Serenity

May 6, 2020

Ethereum’s “Serenity”, the last stage outlined in the launch process already in 2015, is getting closer. The proposal, whose major aspect is the change from Proof-of-Work to Proof-of-Stake, has taken on different shapes over the years and Ethereum core developers have been continuously working to improve it. Most commonly, this phase is now known as Ethereum 2 (or Ethereum 2.0).

Originally, the hope was to have Proof-of-Stake already implemented by now. However, architectural changes on the protocol level and unforeseen research challenges repeatedly delayed the launch. Another reason for the constant delays is that Ethereum has quickly transitioned from a pure experiment that hadn’t accrued much value (2015-2016) to a global blockchain infrastructure that stored billions of dollars’ worth of cryptocurrencies (mid-2017). Upgrading code that secures this many assets requires utmost care.

These delays may also have been one of the reasons for Ether’s relative underperformance compared to Bitcoin over the past two years.

Illustration 1: The ratio between the price of ETH and BTC currently sits at similar levels as before the major bull run in 2017.

The question is now: How much of the risk that Ethereum 2 does not launch soon is priced into the current price of ETH? While assessing this exactly is impossible and will only be known after the fact (i.e., after Ethereum 2 has launched), it is reasonable to assume that at least some of ETH’s bear market versus Bitcoin can be ascribed to the delays of Ethereum 2.

Ethereum 2 in 2020? Some developers of Ethereum 2 are “95% confident” that the launch will happen this year. There is one key factor that investors should look out for to get a more accurate grasp of when the launch is actually close: a multi-client testnet that runs smoothly for 2-3 months.

Testnets for Ethereum 2 have been running for quite some time now and have already been integrated to various block explorers. In another milestone, Prysmatic Labs recently introduced their Topaz testnet that features the full Ethereum 2 mainnet configuration. While this was not the multi-client testnet yet, it is capable of forming the base for multi-client experimentations. Topaz has been running with minor client bugs since its launch on April 18. Last but not least, just yesterday evening, a first multi-client testnet called “Schlesi” that is based on a slightly modified mainnet configuration has had its genesis event and successfully hosted both Prysm and Lighthouse validators.

As outlined in the Outlook2020 report, Ethereum 2 will also have an impact on the supply of ETH. Initially, the annual issuance rate of new Ether will increase to around 5-6% – but once Ethereum 2 can be used to secure the current Ethereum 1 chain, issuance will drop dramatically, most likely to below 1%. Given the current ETH issuance rate of around 4.8%, this would equal a “double halving” in terms of new supply coming to the market. The effect of this would most likely differ from halvings in Bitcoin, since the ETH issuance reduction comes with the switch to Proof-of-Stake and hence validators instead of miners. This fundamentally changes the incentive structures of the blockchain.

Higher Volatility and a Liquidity Premium After the launch of the deposit contract and the beacon chain of Ethereum 2, ETH that have been sent to the deposit contract will not immediately be transferable in the early phases of Ethereum 2. This will have an effect on the markets – how much exactly depends to some extent on how much ETH will be locked up in staking. Generous estimates assume that around 30 million ETH will be staked fairly quickly after the launch.

However, the initial market influence might be smaller than some people expect. Investors willing to stake large amounts at the beginning might not have been active market participants, but rather passive holders. In this case, whether the ETH are held in a cold storage wallet on Ethereum 1 or in validator nodes on Ethereum 2 does not matter. On the other hand, if active market participants decide to move their ETH to staking, this might decrease liquidity in the primary market as well as in the lending markets, driving ETH lending rates up. One consequence of the decreased liquidity could be an increase in volatility.

Due to the initial non-transferability of ETH2, it is also conceivable that an ETH2 futures market will develop. ETH1 and ETH2 do not need to trade at the same price until transferability and full convertibility is established. In fact, in such a futures market it is highly likely that investors demand a liquidity premium for ETH2 – meaning that ETH2 is initially cheaper than ETH1 due to the forced lockup period of ETH2 until the later phases of Ethereum 2. Such liquidity premia are well-known, for example in the yield curves of traditional bond markets or from token sales discounts that are tied to vesting periods.

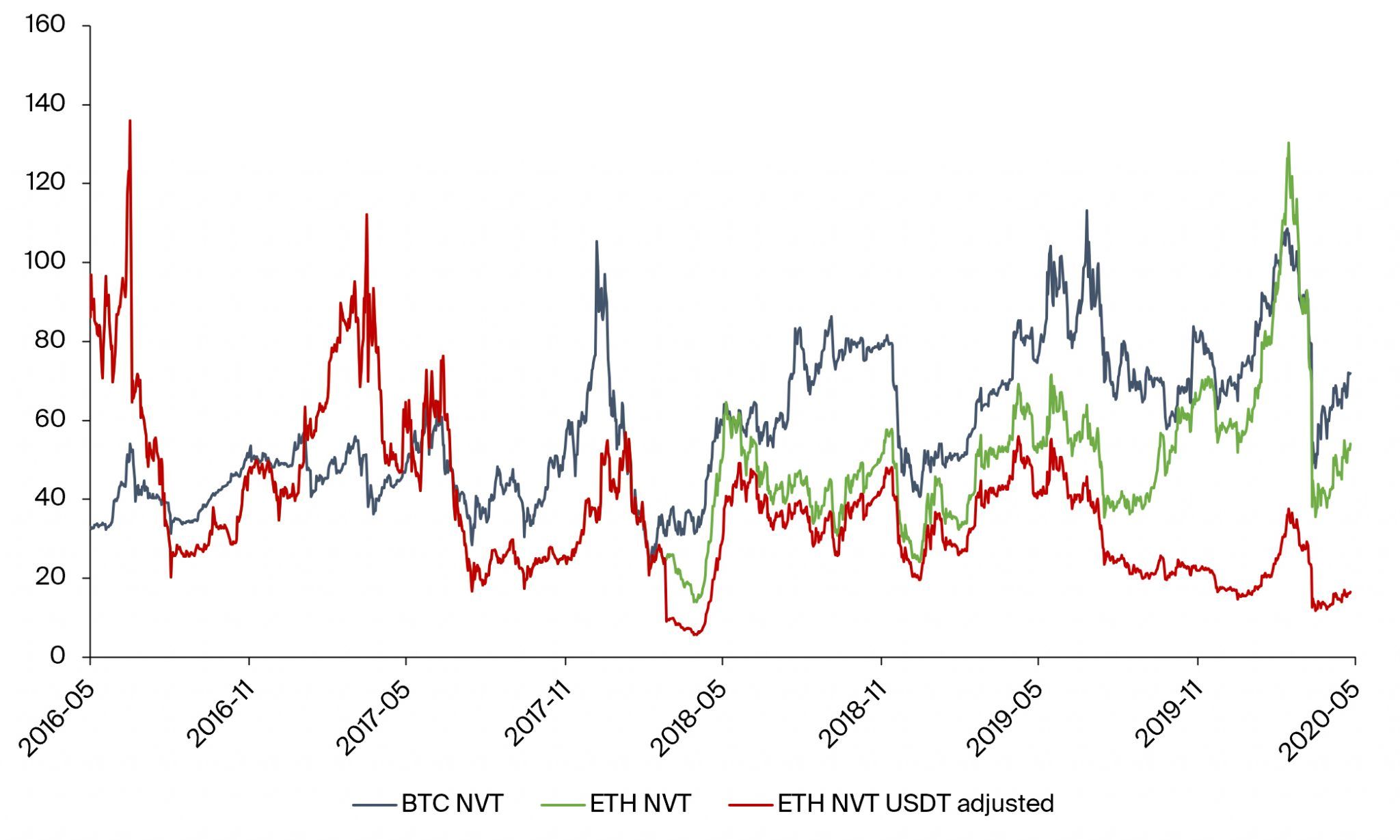

Rise of Stablecoins on Ethereum 1 Stablecoins had one of their best years so far in 2020, and stablecoin growth is one of the trends to watch in the crypto space during this year. Their total market cap has surpassed $8 billion, and they contributed majorly to total value transfers on Ethereum reaching parity with that of Bitcoin. Today, about 80% of the value transferred on Ethereum involves a stablecoin. This justifies revisiting a key on-chain metric called “Network Value to Transaction volume”, or NVT for short. Often called the “crypto P/E ratio”, NVT is a ratio between the market capitalization of a cryptocurrency and the transaction volume of that cryptocurrency.The idea behind NVT is to make sense of a cryptocurrency’s valuation in light of how much value is actually transferred through the network.

Its most used form today involves an adapted form that smooths transaction volumes with a 90-day moving average to eliminate spikes that are related to temporary price spikes, since such price spikes often coincide with increased transaction activity to and from exchanges.

Illustration 2: Ethereum’s NVT ratio is below Bitcoin’s, and even more pronouncedly so if value transferred in the largest ERC-20 stablecoin USDT is also considered.

Typical NVT calculations do not take token transfers into account, but given their recent significance, it makes sense to add at least the largest ERC-20 based stablecoin USDT into account. While USDT was originally launched on Bitcoin’s Omni Layer, Tether has migrated most of it to Ethereum, a process which started in early 2018. The NVT adjusted for USDT (red line in Illustration 2) shows that based on this metric, Ethereum is attractively valued in comparison to Bitcoin.

The rise in stablecoin activity also brings up the topic of whether a “cryptodollar” could have a macroeconomic importance. The current global crisis has shown that US dollars are in high demand. This is because much of the world’s debt is denominated in USD ever since it emerged as the dominant reserve currency after WW2.

The USD infrastructure on Ethereum fostered by stablecoins thrives, and one potentially large use case of Ethereum today and in the future could be to facilitate access to dollars as well as cheap cross-border payments. For this to reach a massive scale though, the increased throughput of Ethereum 2 of multiple thousand transactions per second is needed.