Leveraging Blockchain for Decentralizing Finance

Oct 8, 2019

Decentralized finance, or DeFi for short, encompasses services that are known from traditional finance such as trading assets and borrowing and lending. However, the services are implemented in a trustless manner on a public blockchain – and hence accessible to everyone at negligible costs. Most of today’s decentralized finance services are implemented on Ethereum. DeFi can be considered Ethereum’s next “killer (d)app,” after the blockchain attracted significant interest as a decentralized fundraising platform in 2017 with Initial Coin Offerings (ICOs).

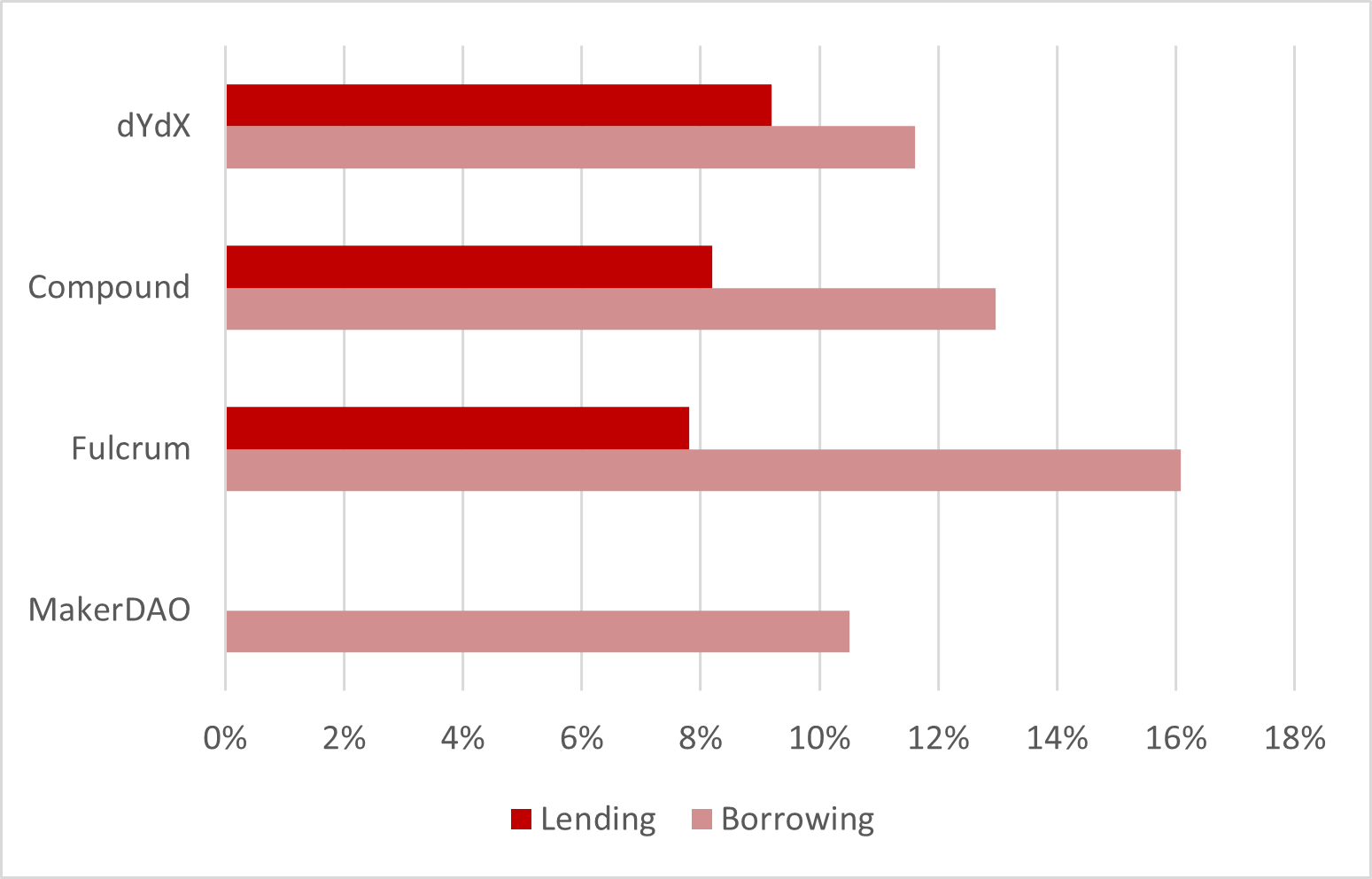

Currently, the major use case of DeFi is decentralized lending and borrowing. The largest player in the market is MakerDAO. At the time of writing, MakerDAO captures around 50% ($270 million) of the total USD value locked up in DeFi applications and more than 1.5 million Ether.

MakerDAO allows users to open collateralized debt positions (CDPs). Their USD-pegged, fully decentralized DAI stablecoin can be borrowed by putting up Ether as collateral. Loans on MakerDAO are overcollateralized: The minimum collateralization ratio stands at 150%. Dropping below this ratio leads to liquidation of the CDP, and the borrower incurs a 13% liquidation penalty on the deposit. A common complaint made against decentralized lending markets is the capital inefficient requirement of high collateral. This is because pseudonymous Ethereum accounts do not have reputations. So far, a decentralized credit rating system that tracks ETH addresses involved in DeFi contracts and awards a score based on their transaction history has not been created.

The fees for borrowing, called stability fees due to their role in controlling supply and demand of the DAI tokens, were recently voted by MKR holders to be lowered to 10.5%. MakerDAO currently only allows DAI to be borrowed by depositing ETH, although multi-collateral DAI is included in their future roadmap. Other DeFi platforms, such as Compound, offer competitive rates for lending and borrowing crypto assets.

With global interest rates on bank savings at record lows, the rates offered by DeFi protocols are appealing. As such, efficient market theory dictates that there must be additional risks that investors take on by lending out funds on DeFi platforms. These risks are, for example, related to vulnerability in the smart contracts that form the backbone of the systems. Depending on the degree of decentralization, there may also be a certain amount of counterparty risk such as price feeds from centralized oracles. Hence, it is necessary to carefully study the platform and its security audits before lending or borrowing large sums of money.

The Eight Most Important Decentralized Finance Business Models

The DeFi landscape is constantly evolving. Currently, DeFi makes up around 3.4% of Ethereum’s total market capitalization of approximately $18.6 billion. Despite being a relatively small amount, there is burgeoning landscape of innovative business models that entrepreneurs are bringing to the market. Here are the top eight DeFi business models that are currently gaining traction:

1.) Decentralized Leverage and Lending Markets – $408 Million

MakerDAO, Compound, dYdX, and Fulcrum are examples of decentralized lending markets. Due to their increasing importance, third-party user interfaces that simplify interactions with these protocols have also been established. For example, InstaDApp’s protocol bridge enables assets that are locked in one DeFi platform to be transferred to another and is thus a way to take advantage of the best rates offered in the lending and borrowing markets.

With the growing size of MakerDAO CDPs, tools to improve management of loans have been developed. For example, DeFi Saver allows users to easily monitor their CDPs and take actions such as borrowing additional DAI or repaying part of the debt to improve the collateralization ratio. A beta version of an automated CDP saver that prevents liquidations has also been released and battle-tested for a first time during the large drop in cryptocurrency prices two weeks ago.

2.) Decentralized Exchanges (DEX) – $28 Million

0x, Bancor, Kyber, AirSwap, and Uniswap are all examples of decentralized exchanges. Due to the current state of blockchain technology, DeFi applications are limited in terms of speed and transaction throughput. The decentralized exchange 0x is estimated to have a total trading volume in 2019 equivalent to one day on Coinbase, of around $200 million.

3.) Decentralized OTC Markets – $2 Million

The decentralized P2P over-the-counter software called Bisq saw a spike in use after Localbitcoins.com cancelled their P2P cash trades. Localbitcoins executes between 40,000 and 50,000 trades per day with approximately half a million users per month. Removing in-person cash trades forced approximately 12,000 transactions per month onto other P2P services. Localbitcoins officially states that they abandoned cash trades because they made up such a small percentage of their business. However, there are also reports that they faced pressure from regulators in various countries for enabling people to meet and trade Bitcoins without complying with Know-Your-Customer and Anti-Money Laundering policies.

4.) Decentralized Prediction Market – $509,000

Augur is a decentralized prediction market that enables investors to bet on the outcomes of events. As discussed in Episode 8 of Bitcoin Suisse Decrypt, Augur is a collection of smart contracts that are built on Ethereum that allow anyone to create a prediction market about anything.

5.) Decentralized Autonomous Organizations – $788 Million

Decentralized Autonmous Organizations (DAOs) like the Dash Masternode Network with $342 million staked and the Moloch DAO with $1 million staked allow users to make decisions regarding the future of the network by buying the right to vote with vested capital. In MakerDAO, MKR token holders have the right to vote on network governance decisions such as changing the stability fee.

6.) Decentralized Escrow Accounts

Arwen allows cryptocurrency investors to trade on centralized exchanges without sending their coins to the hot wallet of a centralized exchange. Instead, investors send their coins to a blockchain-based escrow account that is linked to an exchange’s order book.

7.) Decentralized Asset Management – $127,000

Open-source softwares like the Melonport Protocol allow asset managers to manage funds on the behalf of other investors. The investors must send their Ethereum to an escrow account. The investment manager can then make decisions regarding which ERC-20 tokens to buy and sell. However, the investor keeps control of his or her private keys and does not need to give the private keys to the investment manager.

8.) Decentralized Payments – $90 Million

MakerDAO DAI fits into both the lending category and the stablecoin category. If one includes the market capitalization of DAI, this DeFi dApp is managing approximately $82 million worth of assets. An often forgotten DeFi payment DApp is Bitcoin’s Lightning Network that is managing approximately $6.5 million worth of Bitcoin. Another payment coin is WBTC, which stands for wrapped BTC. This is an ERC-20 token that is backed 1:1 by bitcoin, and has approximately $4.6 million locked up.

In the future, borrowers will be able to choose between borrowing from traditional financial intermediaries like banks or from decentralized lending protocols like MakerDAO or Compound. On the one hand, decentralized finance loans are lent on non-discriminatory terms meaning that the same rates are available to any borrower regardless of that individual’s characteristics. On the other hand, DeFi loans are capital inefficient and more onerous to pay back than fiat loans because cryptocurrencies generally have lower inflation rates than fiat currencies. Since cryptocurrency loans would still mostly need to be converted into fiat in order to purchase real goods and services in the economy, it is fair to assume that for the foreseeable future, DeFi will be used primarily by crypto traders in order to speculate. However, as illustrated by the various areas where the DeFi ecosystem is already developing, its potential goes far beyond that.

“DeFi creates a more Austrian-economics version of finance and lending.”

– Jake Brukhman