On-Chain Derivatives and Insurance

Nov 26, 2019

Decentralized Finance (DeFi) on Ethereum has been one of the fastest-growing areas of blockchain use cases and has attracted considerable capital over the last year. The trustlessness of decentralized blockchains allows avoiding intermediaries, with the goal to reduce overall friction costs – contractual obligations are enforced by code instead of courts. However, this also bears the risk that the code is faulty or attackable. Various projects minimize these risks through smart contract auditing as well as formal verification to ensure that algorithms operate as intended. However, there is no 100 % guarantee that code is bug-free. How could investors protect themselves and insure against these risks?

In traditional finance, portfolios are often hedged against unwanted risks using derivatives such as futures, forwards or options. The size of the options market is considerable: The U.S.-based Options Clearing Corporation cleared 142 million equity options contracts in October alone. The size of the global OTC derivatives market stands at around $500 trillion. The importance of derivatives in cryptocurrencies has also been increasing, and much of the trading activity is now happening on exchanges that offer them.

“We are seeing things like hedging, shorting, derivatives, and more, all built on a decentralized platform where there are no intermediaries, no clearinghouses.”

– Fred Wilson

As such, it is only a matter of time until derivatives make their way onto the blockchain, circumventing intermediaries and eliminating counterparty risk. In mid-November, the Convexity Protocol was proposed by Zubin Koticha as a way to bring options to the Ethereum blockchain as fungible ERC-20 tokens, called oTokens. Having easily tradable options on-chain would offer additional opportunities to insure against smart contract risk. For example, investors could hedge their risk of critical bugs e.g. in MakerDAO’s DAI smart contracts by buying a put option on DAIUSDC with a strike of $1. In the unlikely case that DAI loses its peg to USD until expiration, the option would pay out the difference between $1 and the current DAI price. This way, the investor is protected against the risk of a DAI collapse for the duration of the option – paying the option premium as a fee. The option premia would also serve as an on-chain oracle for expected volatility in the markets.

One issue of structuring such options directly on-chain is their capital inefficiency. The options seller needs to put up enough collateral to cover the maximum possible liabilities that could arise from the option. Thus, for “black swan” events with a high financial impact, but a low probability, pooled insurance fund strategies (such as Nexus Mutual) covering uncorrelated smart contract risks might be more efficient.

However, the collateral currency can be different from the assets involved in the options contract: Ether might be used to collateralize a DAIUSDC option. This opens up a new way for investors to earn additional returns on their ETH holdings by selling such options and in return taking on the smart contract risk of a DeFi protocol. This should lead to significantly higher interest rates earned on ETH compared to the current rates in DeFi of about 0.03 % p.a. As such, it might become an attractive opportunity for ETH holders in the future as an alternative to lending their ETH out directly on decentralized lending platforms.

Overall, derivatives will add a new dimension to the DeFi space and could also give hesitant users more confidence by providing insurance against certain risks. Due to the potential size of an on-chain derivatives markets and the resulting transaction volumes, decentralized exchange tokens with burning mechanisms might stand to gain from this in the long run.

In Blockchains we Trust?

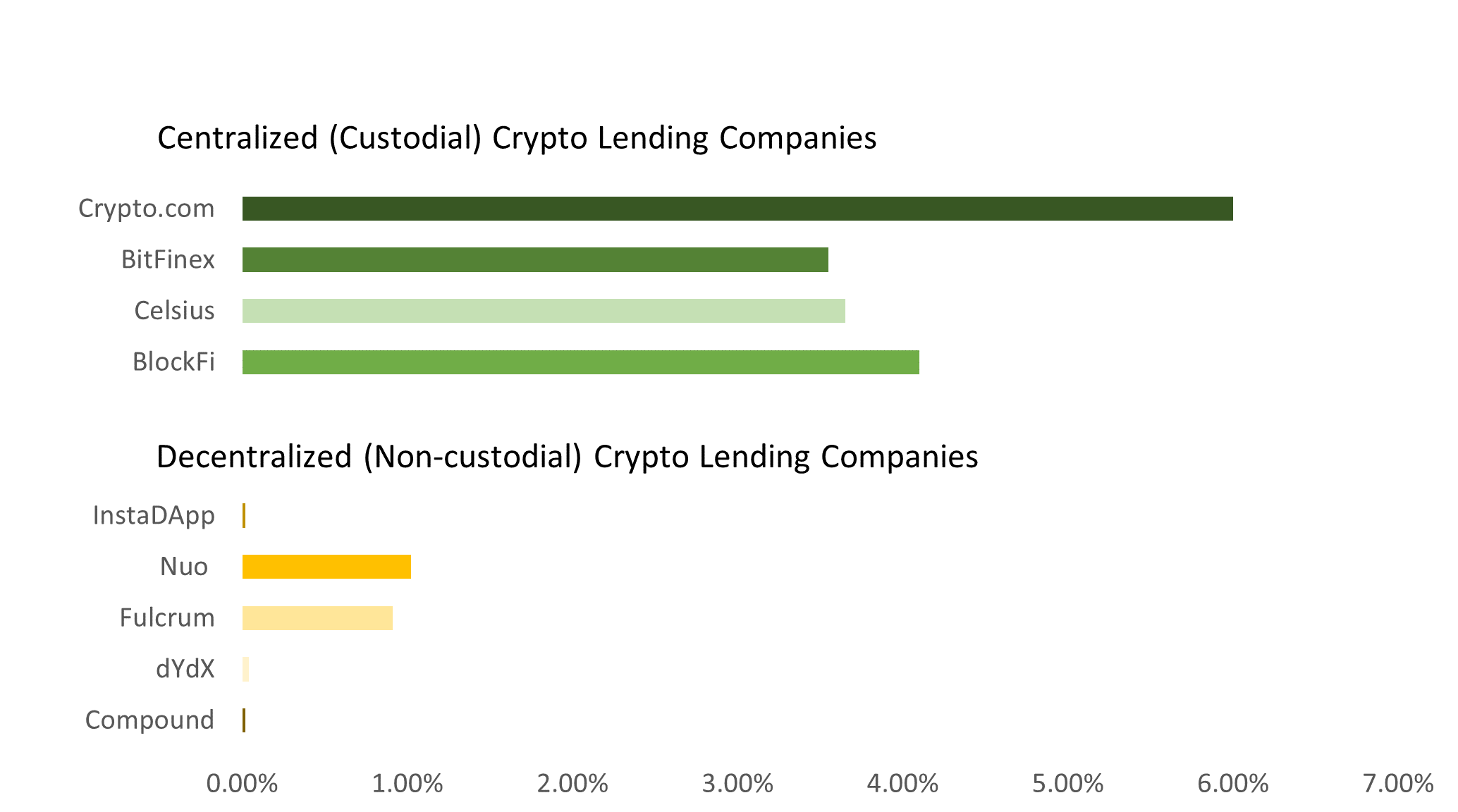

Sometimes it is hard to distinguish between fully decentralized finance blockchain-based smart contract markets and similar services offered by centralized companies. For example, cryptocurrency lending platforms such as Salt, Celsius Network, Crypto.com, and BlockFi all require users to give up control of their private keys. This means users must trust these companies with safe storage of their cryptocurrencies. When an investor deposits cryptocurrency into one of these apps, they are effectively giving a loan to that company. For example, Crypto.com’s 6 % annual return on Ethereum deposits partially represents Crypto.com’s credit risk associated with losing the cryptocurrencies or defaulting on the loan.

However, there are many decentralized markets that operate entirely on the blockchain and offer the same service of crypto lending without taking control of an investor’s private keys including Compound, dYdX, Fulcrum, and Nuo Network. Interest rates for truly DeFi lending platforms such as dYdX have much lower interest rates (0.03 % p.a. for ETH) than centralized crypto lending platforms like Celsius Network (3.40 % p.a. for ETH). This could signal that people trust more in smart contracts and blockchains than in centralized counterparties. Although, other interpretations exist as well, such as KYC/AML and tax implications of using a centralized party and the fact that decentralized smart contracts are often over-collateralized.

Since the industrial era, we have gradually been transferring trust away from manual human labor and more towards automated advances. For example, autopilot in planes is used to minimize risk from human error. Even though statistics argue that we should trust math and machines slightly more than other humans, many of us still want insurance in place just in case.

Insuring against tail-end risk, such as a smart contract failure, is still a developing part of the infrastructure of the cryptocurrency ecosystem. However, most of the non-custodial solutions to insurance are also capital inefficient in the sense that sellers of insurance plans will have to put up 100% or more collateral. In a decentralized market for insurance, insurance contract sellers would need to lock up collateral in a type of escrow account in order to publish insurance products on the market. DeFi is working on solutions to its own capital inefficiencies, such as the rehypothecation of collateral for multiple insurance products as long as the default correlation risk of products is low enough.