The Aftershock of Governance Tokens

Nov 10, 2020

18 August 2020

The hype around decentralized finance (DeFi) continues as the total value locked in DeFi protocols has reached $6 billion, and innovation is happening at a breathtaking pace. For example, money market protocol Aave (LEND) has recently announced a series of upgrades, such as fixed rate deposits (allowing users to earn a stable rate for lending) and gas optimizations to bring down the overall cost of interacting with the protocol. Additionally, yield aggregators such as yearn.finance continue to attract interest, since they simplify the optimization of yield farming by providing “Vaults” with pre-defined strategies. One of these strategies involves yield farming on Curve, a decentralized exchange designed specifically for swapping assets with similar value, such as various USD-pegged stablecoins or different kinds of tokenized Bitcoin on Ethereum. The governance token of Curve, CRV, has recently been launched, and is the main reason why high yields of currently around 90% can be achieved by farming the protocol.

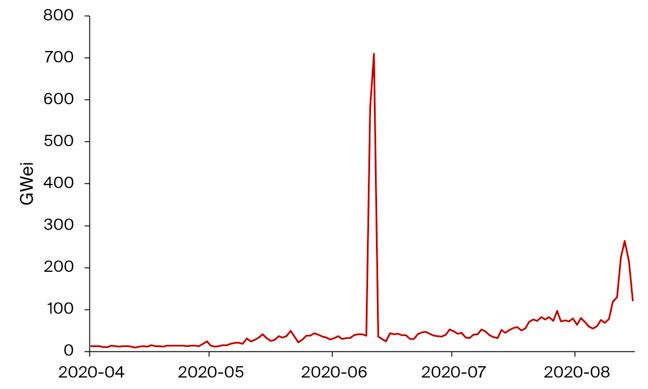

High Ethereum Fees Volumes on decentralized exchanges have also exploded. The largest one, Uniswap, has processed on average around $250M per day over the past week, or about half of that of major centralized exchanges. Gas usage through decentralized trading on Uniswap has increased considerably and played a part in Ethereum fees skyrocketing.

Illustration 1: Daily average gas fees (in GWei) for transactions on Ethereum have strongly increased over the past month. The spike in June was an anomaly mostly due to two transactions that were submitted with absurdly high gas prices.

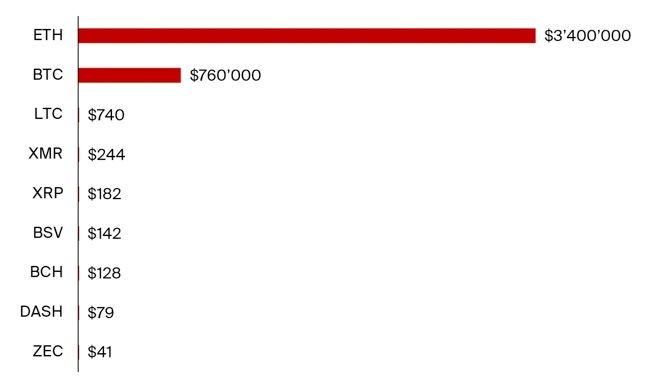

Overall, total fees paid per day on Ethereum are now significantly more than those paid on Bitcoin. The two largest chains by market capitalization share the vast majority of fees collected among all public blockchains.

Illustration 2: Ethereum and Bitcoin capture the majority of fees paid on public blockchains. Over the past 24 hours, Ethereum and Bitcoin have collected $3.4M and $760k in transaction fees, respectively.

This shows that block space in these two chains is perceived as valuable, and users are willing to pay the steep fees associated with transacting on the chains. On the other hand, it also highlights the need for better scalability. For Ethereum, this may lead to a gradual shift from layer 1 to layer 2 using scaling solutions such as zk-rollups in the short to medium term. Eventually, the switch to Ethereum 2 should also bring additional scalability – however, a full implementation of all phases of Ethereum 2 is still likely more than two years out.

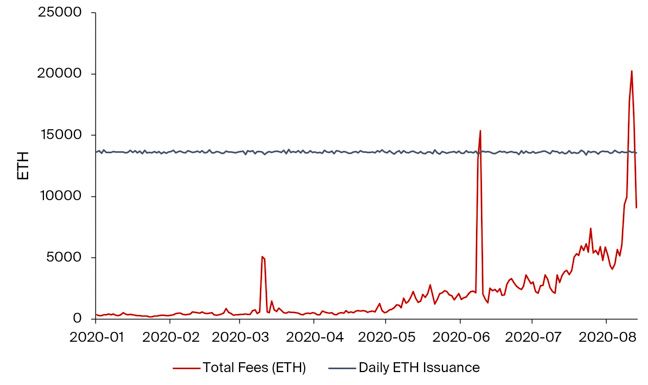

Potential for Negative Net Issuance? The massive amount of transaction fees paid on Ethereum also bring up the thought of Ethereum Improvement Proposal (EIP) 1559 again. EIP-1559 aims to transfer the volatility of gas prices and hence transaction costs to the volatility of the block size. This would strongly improve the user experience since fees would become much more predictable. On top of that, a large portion of transaction fees would be burned – which would bring down the overall supply inflation through issuance of new coins to miners (PoW) or validators (PoS). This may even lead to a decreasing ETH supply in times of high demand, as would have been the case during several of the last days were EIP-1559 already implemented.

Illustration 3: Total transaction fees have briefly surpassed issuance of new ETH to miners in August.

An additional phenomenon that DeFi has brought about is a rapidly increasing amount of BTC tokenized on Ethereum. In total, there is now more than $500 million worth of Bitcoin tokenized in the form of various ERC-20 tokens, such as wBTC (a custodial solution with around 70% market share) or renBTC (a trustless variation with around 20% market share). These tokens are then used, for example, to mint DAI through MakerDAO – in fact, the Maker wBTC contract is the largest holder of wBTC and stores about 11’400 wBTC (around 42.8% of all wBTC tokens). Another popular option is to provide liquidity to Curve, which accounts for another 6’500 wBTC (24.6% of all tokens).

Role of Governance Tokens The issuance of governance tokens to protocol users to attract liquidity has kickstarted the current hype around DeFi and attracted large amounts of capital. Their value, however, is still unclear and depends on the governance rights that come with it.

From a game-theoretical perspective, the value of a well-designed governance token is tied to the overall success of the protocol, aligning the incentives of token holders and promoting good governance. However, at the current stage, not all protocols have implemented such mechanisms in their governance tokens. For these, the value of the token is purely based on the possibility of future monetization, e.g. the power to vote on the implementation of a protocol fee that flows to token holders. As such, it is also critical what governance can do, meaning which aspects of the protocol that may relate to the token value they can influence.

For example, in MakerDAO, the main parameter that governance can change that should affect the price of their token (MKR) is the stability fee for opening Maker Vaults. Stability fees are charged on outstanding debt to the Maker protocol, converted to MKR tokens, which are then burned to decrease the overall supply. Additionally, governance can approve new assets as collateral (e.g. MANA at the end of July) and change the maximum allowed debt per asset to scale the system and potentially increase the stability fees earned in total, leading to more MKR being burnt. As for most protocols, governance also has the duty to approve upgrades to the protocol and new functionalities.

On the other hand, the token of Compound, COMP, purely serves governance functions and has no mechanism for (in)direct value accrual yet, so its value is closely linked to speculation that this will change in the future. So far, 19 governance proposals have been voted on, of which 16 were passed. Mainly, the changes implemented through the on-chain voting process were related to protocol stability changes, such as setting collateral factors (i.e. how much debt can be borrowed against a specific asset). Governance also has the power to change reserve factors: Compound sets aside a small portion of interest paid by borrowers as reserves. These reserves are controlled by the token holders. By changing this amount and distributing part of excess reserves to COMP token holders, an implicit spread on the lending / borrowing rate could be collected for COMP holders in the future.

Money Markets and Governance Tokens Another aspect of fully on-chain governed protocols that may seem irrelevant today, but become more important if these protocols grow (much) more in size is the possibility of “hostile protocol takeovers” through a combination of buying tokens and borrowing them from money markets such as Compound or Aave. If sufficient governance tokens are available for borrowing, a malicious actor could try to obtain a majority share of governance tokens through borrowing (driving up lending interest rates in the process and enticing more people to offer their tokens in the money market protocol) and exploit the protocol in her or his self-interest. This may present a problem especially for smaller protocols with cheaper governance tokens, which potentially require posting less collateral overall. However, many protocols already have mechanisms in place that make such an attack harder or at least less profitable, such as time delays on protocol changes through governance.

Conclusion The current excitement about DeFi continues to drive innovation. The world of DeFi is one of the first examples of why composability matters: While, for example, MakerDAO is a powerful protocol on its own and created the first fully decentralized USD-pegged stablecoin, its full potential gets unlocked through the interaction with other protocols such as decentralized exchanges (DAI trading against other assets) or money markets (to lend DAI or post it as collateral). The importance of governance tokens will increase for two reasons: Holders will want to find a way to monetize the protocol, and due to the intertwined nature of DeFi, governance decisions can have effects far beyond just one protocol. Network effects are in the process of being established, and – perhaps a remarkable difference to the ICO mania in 2017 – protocols are often mutually reinforcing and adding value to each other instead of fighting for a share of the same pie.