The Year 2020 in a Nutshell

Dec 16, 2020

The year 2020 is slowly coming to an end. It has certainly been an extraordinarily eventful year, also for the crypto space. This episode recaps the most important events for the markets and highlights crucial fundamental developments – from “Black Thursday” (March 12) to the recent launch of phase 0 of Ethereum 2.

The Time Bitcoin Almost Went to Zero One of the most memorable moments this year clearly occurred on March 12/13, when the Bitcoin price (and that of most other cryptocurrencies) dropped by more than 50%. All markets globally were crashing, perhaps due to the realization that the pandemic would take a stronger toll on the economy than expected, and correlations moved towards 1 during this flight to safety. In the crypto market, the effects were exacerbated by leverage in the system: Bitcoin was collateralized, and dollars borrowed against it, either to fund operations (e.g. by miners) or to buy more Bitcoin (by speculators). When prices started their rapid descent, these collateralized BTC started to get liquidated and accelerated the downwards movement. At times, there were more than $200 million worth of Bitcoin long positions waiting to be sold into the market on derivatives exchange BitMEX alone – more than the entirety of the bid side of their orderbook down to $0. The market was visibly in shock, as illustrated by wide bid/ask spreads of up to $600-$700 and massive discrepancies between prices on different exchanges, a situation which only slowly recovered over the following days.

In hindsight, this event marked the bottom for the months to come. Excessive leverage had been purged from the market, and prominent investors, such as Paul Tudor Jones, used it as an opportunity to enter the crypto world.

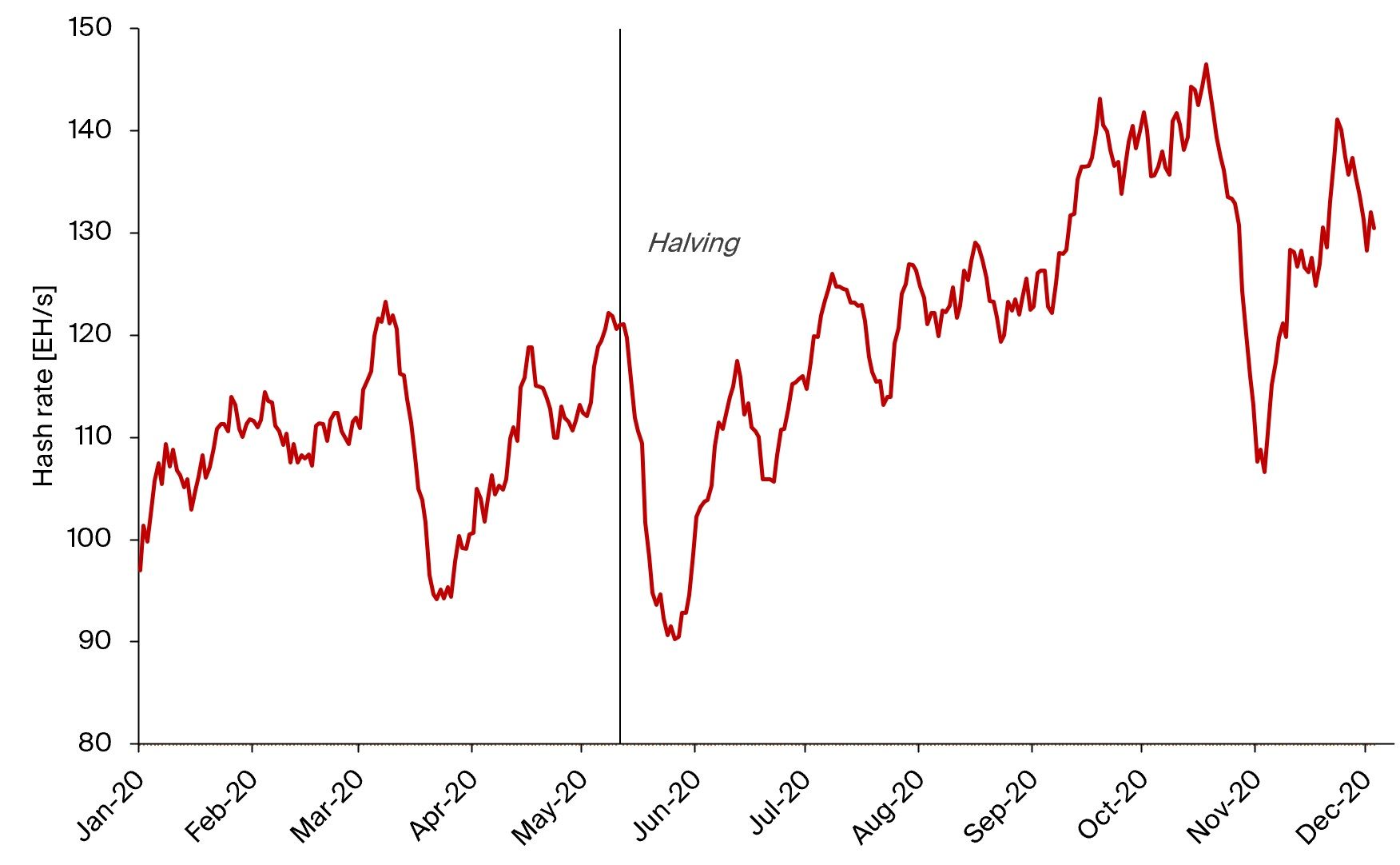

Bitcoin Block Reward Halving Soon after, on May 11, the Bitcoin “Halvening” took place and the reward for each block was reduced from 12.5 BTC to 6.25 BTC. As outlined in the Outlook2020 report, this had major implications for Bitcoin’s budget for network security and on the revenue of miners. One important factor in the analysis is the Bitcoin price – a higher price means that miners might remain profitable even post-halving without improving efficiency.

Illustration 1: After the block reward halving, unprofitable miners ceased operations and were quickly replaced by more efficient miners.

After this year’s halving, the hash rate initially dropped, but recovered and rose quickly as Bitcoin started to make yearly highs. So far, Bitcoin has rallied +120% since the halving. In comparison to the two previous halvings, this is more aggressive than in 2016-2017 (+55% over the same duration), but much less than in 2012-2013 (+700%).

Illustration 2: “Black Thursday” in March marked this year’s bottom, and since the block reward halving in May, Bitcoin has rallied +120%.

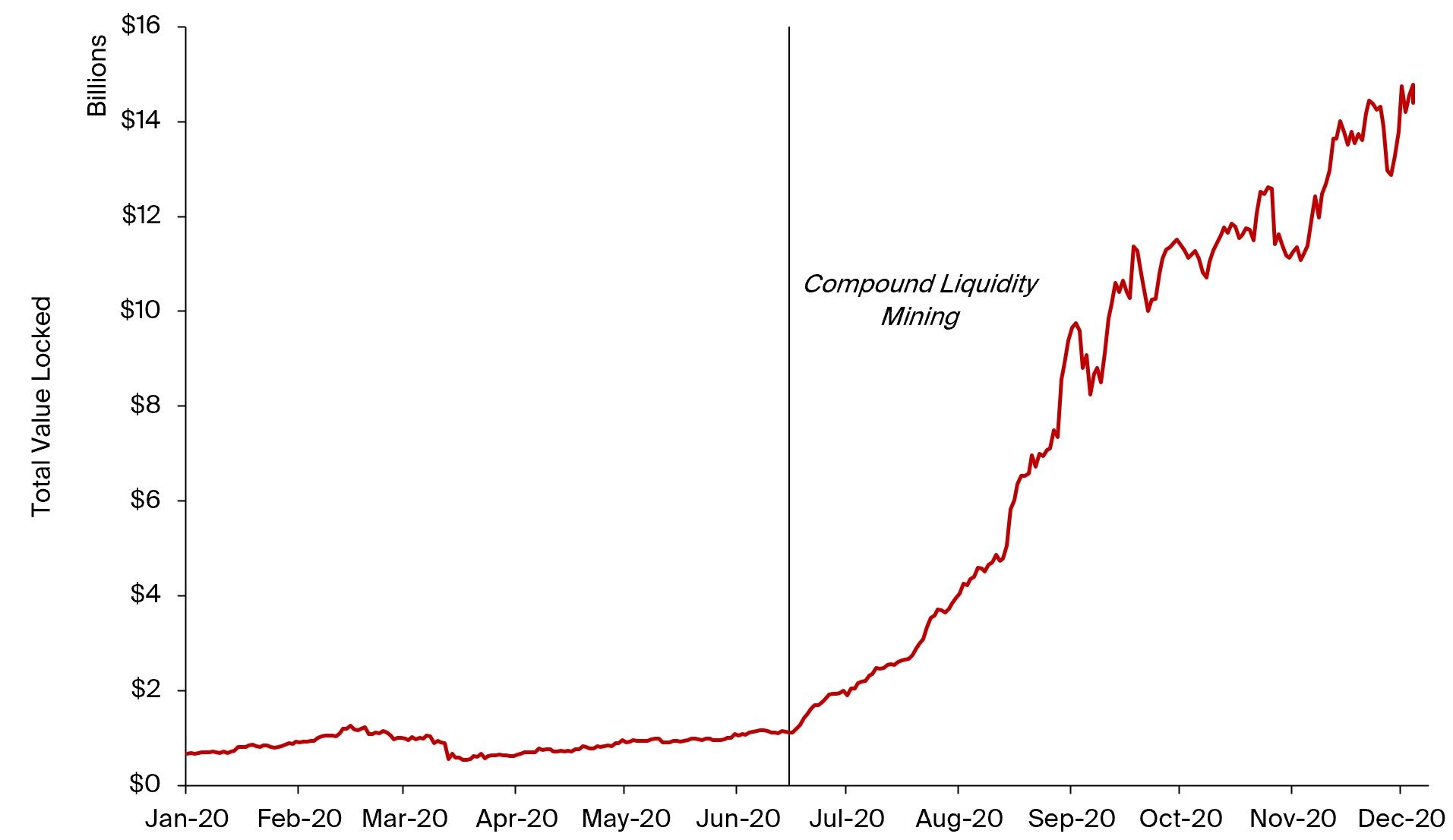

DeFi Summer Besides the halving, the focus during this summer has been on the decentralized finance (DeFi) space, where innovation happened at a breathtaking pace. The total value locked (TVL) in DeFi protocols has risen exponentially since the money market protocol Compound announced that it would hand out its native governance token, COMP, to users of the platform.

Illustration 3: Since the announcement of Compound’s liquidity mining program, the total value locked in DeFi has risen substantially and now stands at around $14.5 billion.

Compound did not remain the only protocol to announce the launch of a governance token, and the model of handing it out directly to users as rewards for participation gained traction. It also created the phenomenon of “yield farming”, in which savvy DeFi users quickly move from one protocol to another to maximize their yields and were often able to achieve yields of >100% annually. These activities did not come without risk, though, and smart contract exploits happened quite often – as such, it was (and still is) crucial to closely evaluate the security of a smart contract.

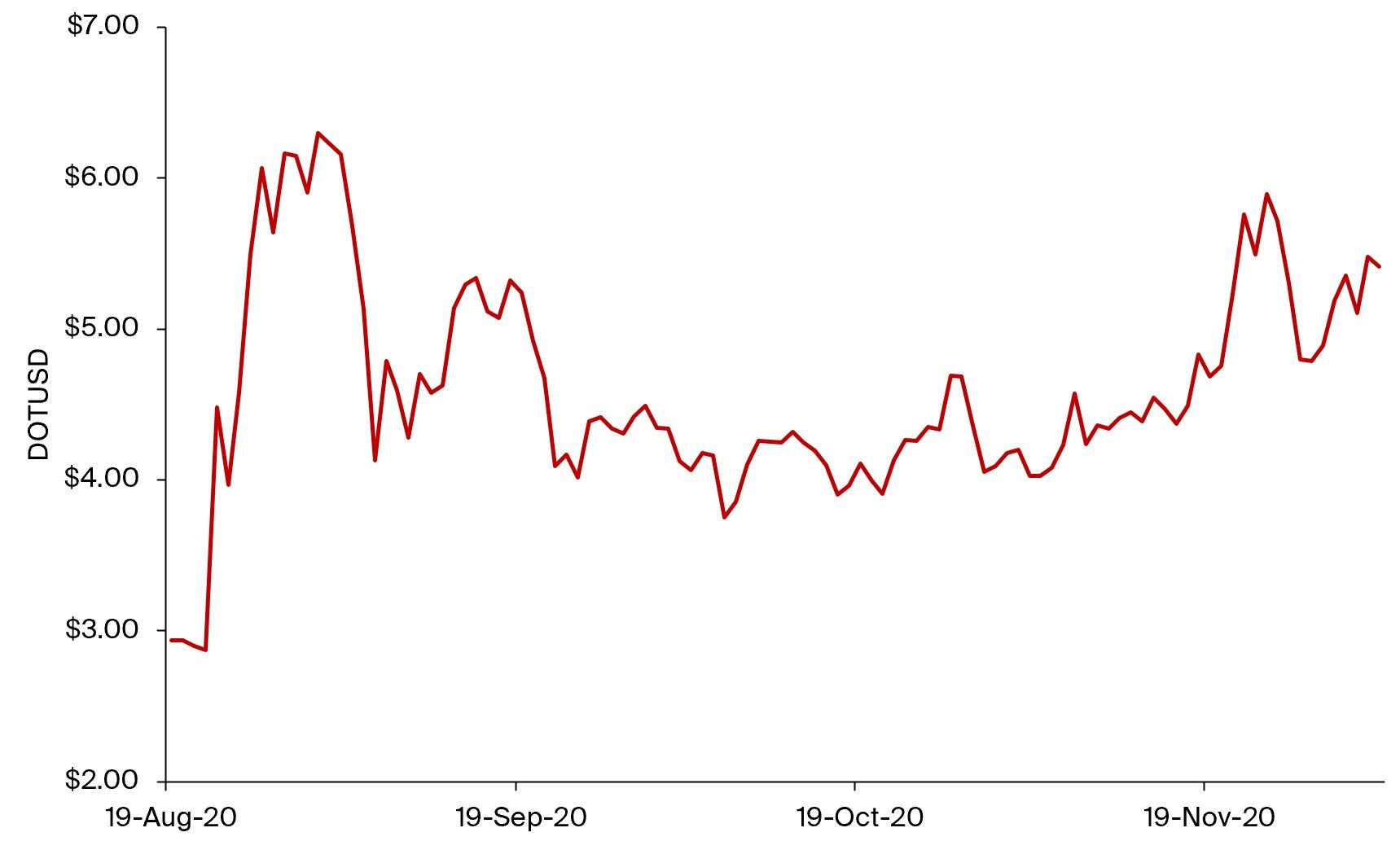

Polkadot Launch Another significant milestone from a fundamental side was the launch of the interoperability-focused blockchain Polkadot in May, which had been anticipated by many in the crypto community since 2017. As a first on-chain community vote, a redenomination of DOT and Planck (its smallest unit, similar to a Satoshi for BTC or Wei for ETH) by a factor of 100 was successfully conducted.

DOT immediately secured itself a spot in the top 10 by market cap, and has so far shown a low correlation to BTC and ETH.

Illustration 4: DOT became a top 10 coin by market capitalization immediately after the start of trading.

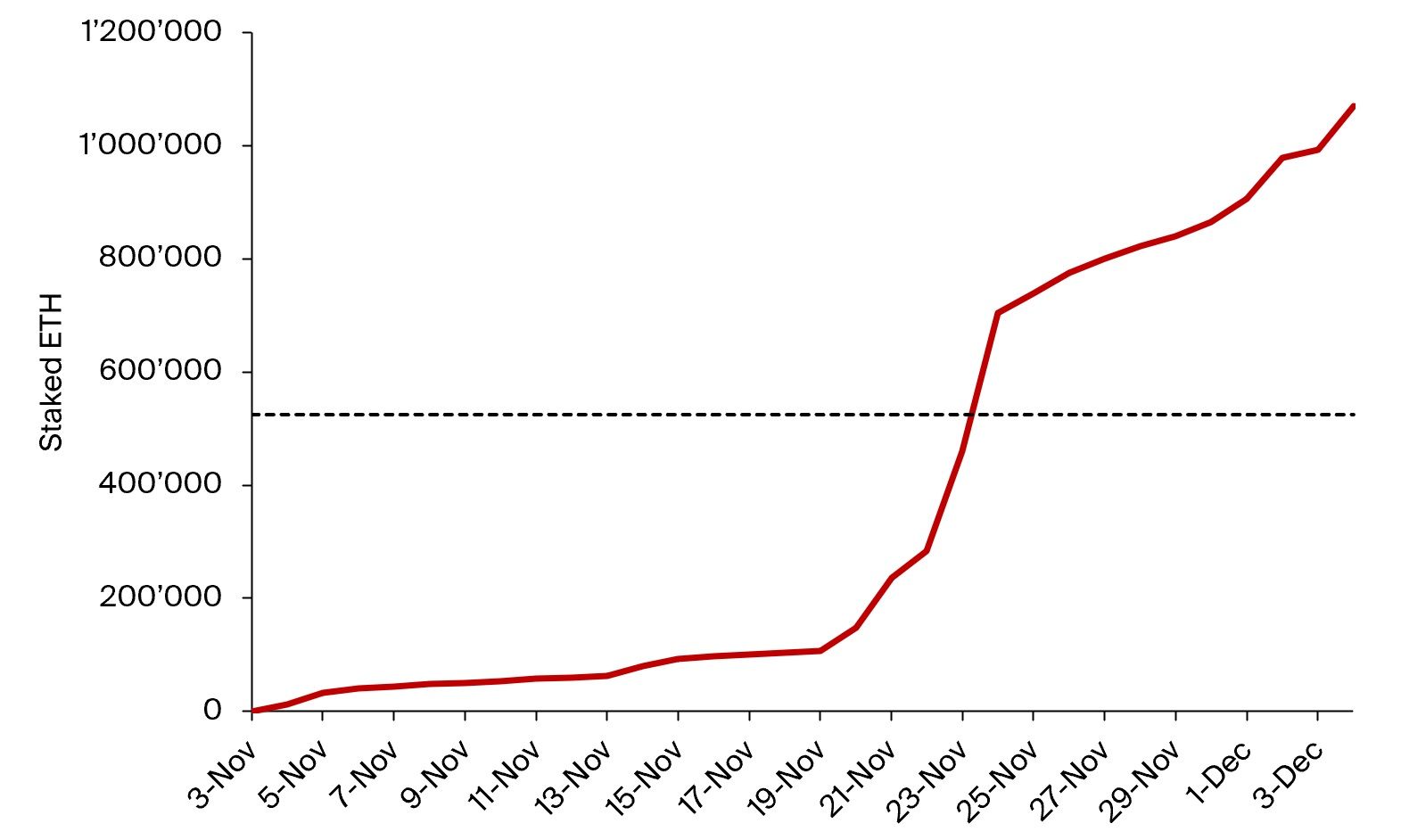

The Beacon Chain – Ethereum 2 Phase 0 Last but not least, Ethereum also managed to take its first step towards the network upgrade Ethereum 2. The Beacon Chain, or phase 0 of Ethereum 2, which represents the coordination and consensus layer for later stages of the upgrade, had its genesis block on Dec. 1, at 12:00:23 UTC. More than 1 million ETH has been staked so far, with a return (denominated in ETH) of around 15-16%.

Illustration 5: The amount of ETH sent to the deposit contract has crossed 1 million, and more ETH is staked daily at a rate of ca. 36’000 ETH/day (or more than 1’000 additional validators per day).

Which Tokens Performed Best? Cryptocurrencies outperformed other asset classes by a fair margin this year so far. Bitcoin and Ether managed to return +163% and +353%, respectively. For comparison, the S&P 500 stands at a year-to-date return of +14.2%, whereas the Nasdaq 100 achieved +43.6%. Precious metals also had a good year, with gold up +20.9% and silver up +34.5%.

Of the top 10 coins by market capitalization, decentralized oracle platform Chainlink (LINK) continued to outperform other cryptocurrencies and received a lot of attention from investors, as weak oracles were often the source of DeFi exploits.

Illustration 6: The top 3 performers of the coins in the top 10 by market cap this year so far were LINK, ADA, and ETH.

Looking a bit further, into the top 100 by market capitalization, the range of returns achieved year-to-date (or launch-to-date) was quite wide and varied from more than +5000% (AAVE) to -52% (FIL). It is noteworthy, however, that for some of the worst performers, the cost basis for many holders is much lower, as they obtained them through liquidity mining programs (BAL, SUSHI), in a public sale (FIL), or airdrops (UNI).

Illustration 7: Of the top 100 coins, Aave (LEND/AAVE), Kusama (KSM), and yearn.finance (YFI) performed best, whereas Filecoin (FIL), Sushi (SUSHI) and Balancer (BAL) showed the worst performance.

Conclusion

Seasonally speaking, December has historically shown to be rather calm. Developments on other fronts not covered explicitly in this episode – such as new regulations or prominent investors and companies allocating part of their portfolios or treasuries to crypto – certainly deserve closer evaluation as well.

In short, the year 2020 has been great for the crypto markets, both from a fundamental as well as a performance perspective. Many exciting breakthroughs have been achieved, such as the launch of the Ethereum 2 beacon chain or that of Polkadot, and cryptocurrencies have yielded attractive returns to investors in comparison to other asset classes.