Token Incentives in Decentralized Finance

Nov 10, 2020

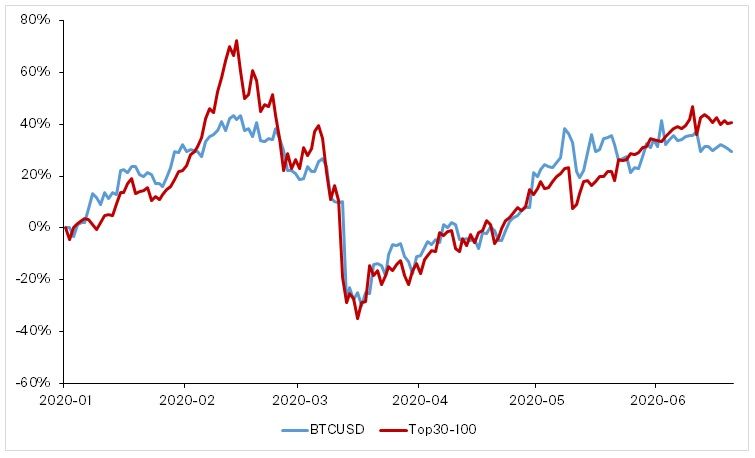

So far in this year and especially since the large price drop on March 12th-13th, many small caps have outperformed Bitcoin. An index of the top 30-100 cryptocurrencies (Bitwise 70) achieved a return of 40% since March 12, whereas Bitcoin yielded 30%.

Illustration 1: Small cap altcoins have outperformed Bitcoin both year-to-date and since March 12/13.

This suggests that investors are comfortable again taking on more risk and speculating on the less liquid small cap coins. Particularly from May to June, when Bitcoin entered a consolidation period in a large price range of about $8.5k to $10k, the attention shifted towards altcoins.

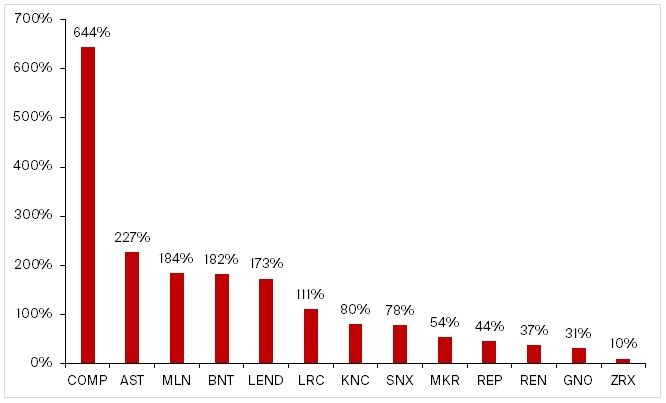

Contrary to the state of the market in 2017, though, price increases in smaller altcoins appear to be more selective – indicating that the market is potentially in the process of separating the wheat from the chaff. Among some of the best performers over the last month have been tokens that are related to decentralized finance (DeFi).

Illustration 2: DeFi tokens have provided outsized returns over the past 30 days (or since initial trading launch in the case of COMP).

The benefits of holding these tokens vary, and the jury is still out on how to properly value them. Typical advantages include the right to participate in the governance of the protocol that underlies the token (such as MKR or COMP), fee-based token burn mechanisms as an attempt to correlate long-term platform growth with the token value (e.g. KNC or MKR), and other incentives such as the ability to stake the tokens (e.g. ZRX or SNX).

As outlined in the last episode of Bitcoin Suisse Decrypt, the scalability of Ethereum’s second layer has vastly improved during this year, using solutions such as zk-rollups. This enables more efficient decentralized exchanges, whose speed can now even rival some of their centralized counterparts. However, one issue of decentralized exchanges remains liquidity.

To address this issue, new concepts of liquidity mining and “yield farming” have been introduced and led to a wave of new participants in DeFi. The demand for block space was high enough to encourage Ethereum miners to raise the block limit from 10 million to 12 million gas.

Liquidity Mining

Liquidity mining is a concept that was first mentioned in a whitepaper by the Hummingbot team, outlining how decentralizing the market making industry could lead to higher efficiency and cost savings both for liquidity buyers (such as exchanges and token issuers) as well as liquidity sellers (the market makers). The goal is to create an incentive structure for decentralized liquidity provision, and reward a large number of market makers through direct subsidies based on their performance, as evaluated through liquidity measures such as average bid-offer spread and order book depth.

However, since each interaction – such as submitting or cancelling an order – with a decentralized exchange has so far required an on-chain transaction, the limited scalability and speed of popular blockchains has hampered the development of a liquid market. Market makers want to be rewarded for the risk they take on, and long delays to order cancellation increase their risk, making spreads (their “reward”) larger. With the increased scalability and short settlement times provided by layer 2 solutions, these decentralized markets are set to become more liquid. Additionally, incentive structures such as liquidity mining competitions (as recently announced by zk-rollups pioneer Loopring) may help to accelerate the process.

Orderbooks vs. Liquidity Pools

While orderbooks are commonly known from traditional and centralized finance, the DeFi space has brought about another innovation: pooled liquidity and automated market making. For example, on Uniswap, investors looking to exchange one token for another trade against a pool of tokens. The price is not defined by a bid-offer spread, but instead by the composition of the pool (called the “constant product market maker model”). Similarly, money markets such as Compound allow lending to and borrowing from a pool of tokens, and the interest rates are set algorithmically depending on the degree of pool utilization.

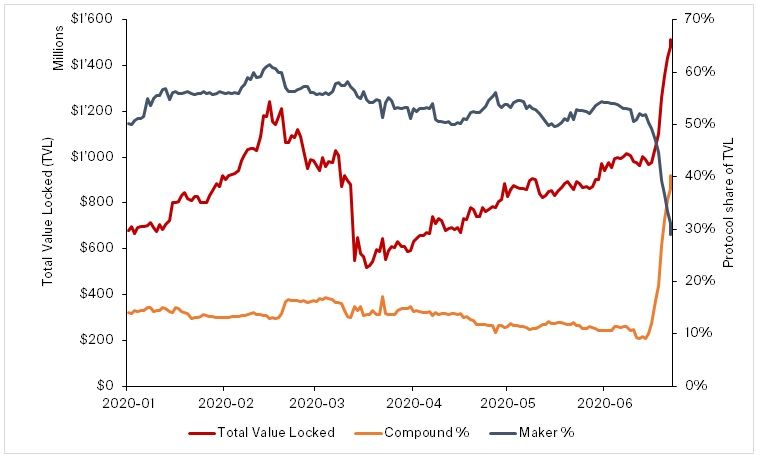

In June, providing liquidity on Compound was further incentivized through the distribution of their governance token, COMP. About 4.2 million COMP tokens (ca. 2880 per day) will be handed out to borrowers and lenders on the platform. COMP has seen considerable interest on the secondary markets: It started to trade on Uniswap on June 15 just above $30 and has since risen to a high of $369 over the past week, more than a tenfold increase. This also had the effect that both borrowing and lending became profitable, since COMP rewards are more valuable than the interest paid. The total value locked (TVL) in Compound has gone parabolic since then, and the platform dethroned Maker as the largest DeFi project (by TVL).

Illustration 3: Compound has overtaken Maker in terms of total value locked on the platform. Overall, the USD value locked up in DeFi protocols has increased strongly over the past two weeks.

Along the success of Compound’s token, other parts of the DeFi ecosystem have also started to incentivize liquidity through platform governance tokens. Balancer, a decentralized index fund creation protocol with automated index rebalancing, started handing out BAL tokens to platform participants. Similarly, pools of various forms of tokenized Bitcoin on Ethereum, such as WBTC, sBTC and renBTC can earn various governance tokens associated with the involved protocols.

“Yield Farming”

The various ways to earn yield by participating in DeFi protocols has led to a wave of speculators that attempt to maximize their yield by combining various DeFi protocols. One way to do so that was very popular over the last week goes as follows:

- Obtain a certain amount of stablecoin, such as DAI or USDC, either by buying in the open market or by

collateralizing cryptocurrency (e.g. ETH or WBTC) and borrowing against it,

for example with a Maker Vault, taking advantage of the currently low stability fees. - Deposit to Compound and borrow another stablecoin against it, such as USDT.

- Swap the borrowed stablecoin for the original one, for example using Curve,

a pool-based decentralized stablecoin exchange. - Redeposit this stablecoin back to Compound and repeat the procedure.

Essentially, this is leveraging up stablecoin exposure in order to maximize both the interest paid on Compound and in return the share of newly distributed COMP tokens. Other ways to participate were through spillover effects to protocols involved in the procedure, such as providing liquidity to Curve stablecoin pools – which has seen record volumes of >$40M over the past days. Through such methods, annualized returns of >200% were achievable. Such returns never come without risk, though.

No Free Lunch: Risks

Achieving these yields is only possible through a combination of various protocols and smart contracts. Thus, the exposure to smart contract bugs or exploits is magnified. On top of this, the yields are highly unpredictable – it is unlikely that the high current yields persist over a longer period of time, and for example on Curve, yields have already come down to more reasonable levels of 6 to 25% annually. COMP, as a key factor in determining the yield from liquidity mining on Compound, has also retraced from its highs and currently trades around $270.

A collapse of the leveraged stablecoin lending and borrowing cycle may also put the peg of some stablecoins against USD under pressure. In the example above, if USDT were to appreciate in value, some highly leveraged “yield farming” positions may get liquidated and disrupt trading on the secondary markets – in the worst case, leading to a cascade of liquidations. However, Compound has a token reserve (between 10-20% of interest paid by borrowers) that functions as a safety mechanism in the case of liquidations.

Conclusion

Distribution of tokens to platform users appear to be a powerful incentivization mechanism that can help to kickstart a platform or DeFi protocol. As a new user and even for seasoned veterans, cutting through the jungle of protocols and understanding all the ways to earn yield is a complex process. DeFi aggregator platforms like InstaDapp make it simpler for the end user, but the danger is that the investor does not fully understand the protocol interactions happening in the background and hence is unaware of the risks.

The parabolic growth that is seen at the moment in the DeFi space is likely unsustainable – however, the initial hype may well lead to a wave of new DeFi users, and it will be interesting to see at what activity levels the space settles over the next months.