1. Bitcoin’s high-fee-season continues to receive mixed reactions

The Facts:

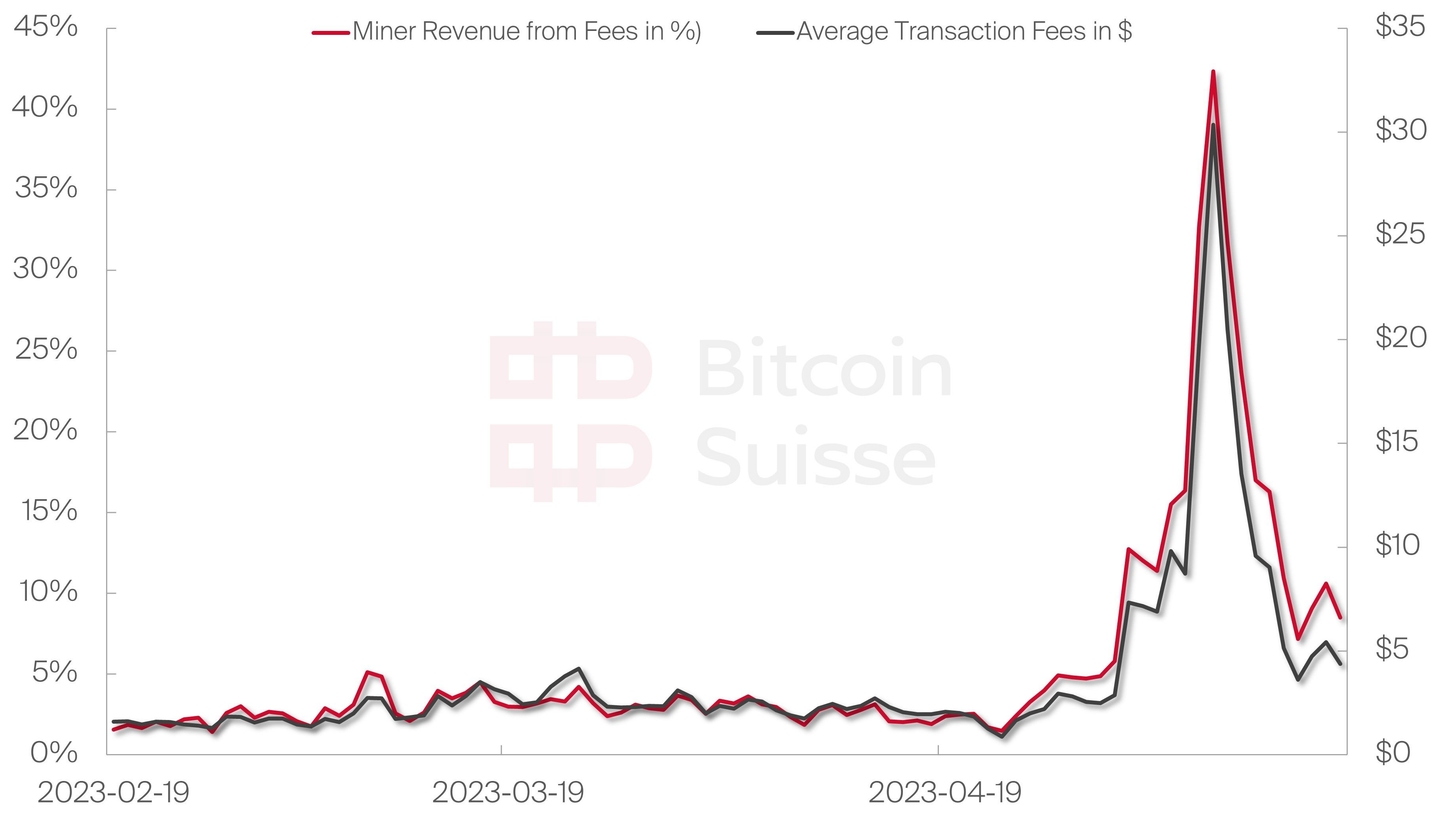

- Glassnode reports on a “Bitcoin Blockspace Boom” triggered by high demand for Ordinals and BTRC-20 tokens, which is provoking further debates in the community. While Ordinals mainly used images, BRC-20 tokens are text-based. While they made the average size of a transaction to collapse close to an all-time low, the average number of transactions per block exploded from 2000 to 4000. Despite that increased throughput, the backlog of unconfirmed transactions still stands at around 267’000 at time of writing, which would take more than 11 hours to fully clear.

- Lightning Labs, critiquing the technical approach taken by Ordinals and BRC-20, announced version 0.2 of the Taproot Assets Protocol (formerly ‘Taro’), emphasizing the efficiency gain when issuing assets on Bitcoin and Lightning by avoiding writing “directly into block space.”

- Another source of demand for Bitcoin, the asset, will come from Tether. Tether International Ltd. announced that, starting May 2023, they will allocate up to 15% of its net realized operating profits towards purchasing BTC. Tethers 23Q1 net profit was $1.48b, which would mean a bitcoin allocation of ca. $222m (8283 BTC) per month, starting May 2023, with a current reserve in BTC of $1.5b as of March 2023.

Our take:

- The recent developments highlight once more the underlying core question about the security of the Bitcoin network: What will happen many years in the future when the block subsidy for miners will have further dropped towards zero? Will the incentive for miners to continue securing the network and processing transactions be enough?

- The path to solve the security problem is to have demand for transactions and thus for blockspace. Sceptics worry that users will not be doing a sufficient regular amount of transactions over time because Bitcoin as a non-inflationary cryptocurrency aligns economic incentives differently. With most users “hodling”, i.e., stacking satoshis but not spending them in transactions, miners may face insufficient economic incentives to continue mining, which will put the security model of the network in jeopardy.

- Where does additional demand for transactions come from? Well, from functionality – new features, users do make use of. In that sense, proponents of Bitcoin should welcome the recent high-fee season caused by Ordinals, BRC-20 tokens and the like as the fees have massively increased because of the high demand and the respective high amount of new transactions. Miners have experienced an extra boost through fees – up to the point where the sum of fees per block nearly equaled the block subsidy (approaching 50% miner revenue from fees).

- The problem is that the technical choices made to implement Ordinals and BRC-20 tokens are clogging the transaction queue in the mempool, causing transactions to be delayed. A much better approach would be to use Layer-2 solutions as the Ethereum ecosystem is experimenting with (Arbitrum, Optimism, etc.). An early-stage yet promising approach are validity rollups on Bitcoin, a topic we will explore in the upcoming Decrypt.

- Finally, Tether’s move to further diversify its reserves by increasing the Bitcoin share by 15% each month, is remarkable. Overall total reserves consist of cash, cash equivalents, and short-term deposits (85%), gold (4%) and Bitcoin (2%). Tether does what some central banks should be doing: diversifying and strengthening their reserves with a non-fiat bearer asset that is designed as a store of value for the digital age – they even self-custody these large amounts with their own wallets and keys.