Seasonality of Bitcoin

Nov 12, 2019

A popular way to invest in an asset for the long term is to dollar cost average into it. This means that investors buy an asset in specific time intervals, regardless of the price – which has a smoothing effect on the average entry price and attempts to circumvent short-term volatility. Dollar cost averaging into Bitcoin has so far been a great strategy: Even the unluckiest investors who started the strategy on December 17, 2017, when Bitcoin briefly cracked $20k, would be up 28 % by now with weekly purchases. However, the question that one will inevitably ask is: When exactly should I buy?

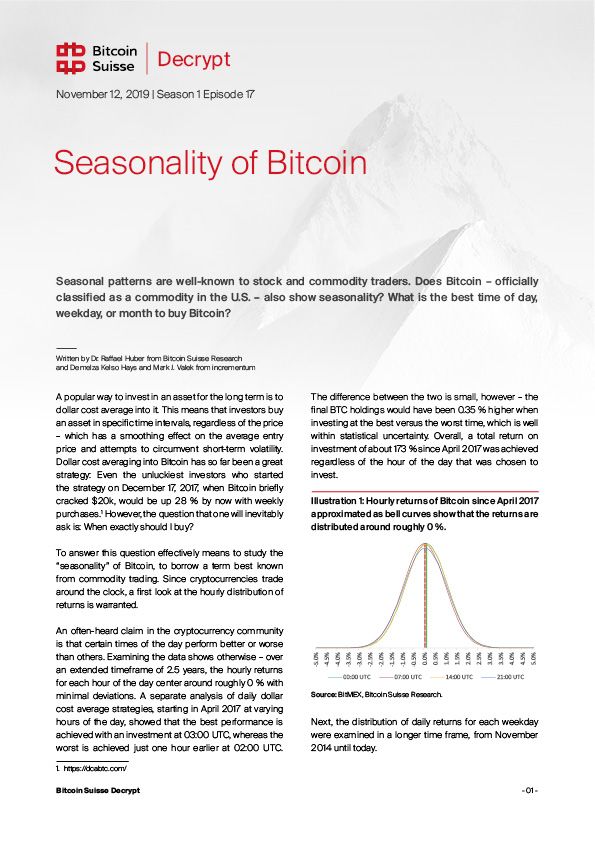

To answer this question effectively means to study the “seasonality” of Bitcoin, to borrow a term best known from commodity trading. Since cryptocurrencies trade around the clock, a first look at the hourly distribution of returns is warranted.

An often-heard claim in the cryptocurrency community is that certain times of the day perform better or worse than others. Examining the data shows otherwise – over an extended timeframe of 2.5 years, the hourly returns for each hour of the day center around roughly 0 % with minimal deviations. A separate analysis of daily dollar cost average strategies, starting in April 2017 at varying hours of the day, showed that the best performance is achieved with an investment at 03:00 UTC, whereas the worst is achieved just one hour earlier at 02:00 UTC. The difference between the two is small, however – the final BTC holdings would have been 0.35 % higher when investing at the best versus the worst time, which is well within statistical uncertainty. Overall, a total return on investment of about 173% since April 2017 was achieved regardless of the hour of the day that was chosen to invest.

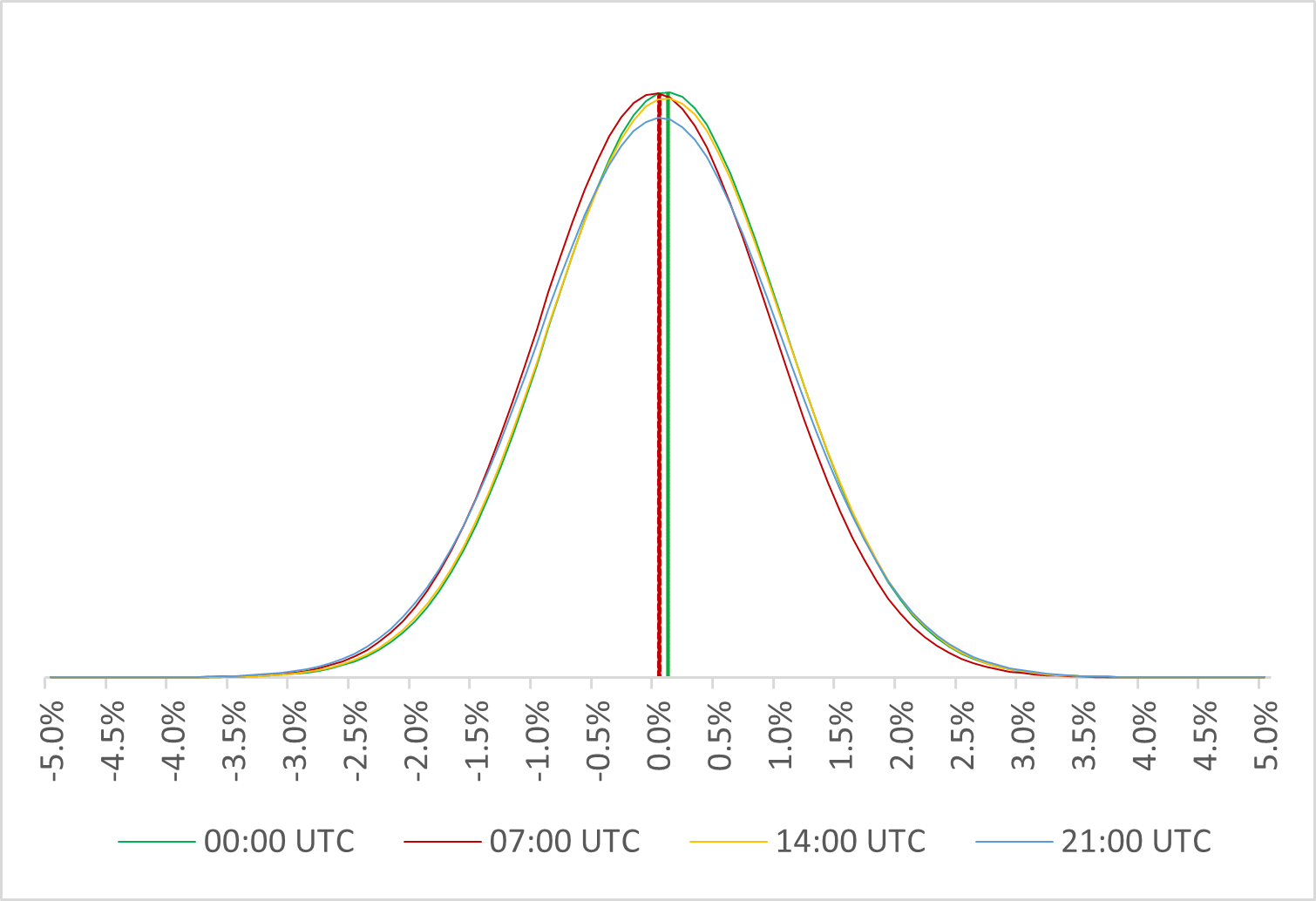

Next, the distribution of daily returns for each weekday were examined in a longer time frame, from November 2014 until today.

Comparing the distributions shows that on average, returns were highest on Mondays and lowest on Wednesdays. Thursdays showed the broadest distribution of returns. Performing an analysis of a weekly dollar cost averaging strategy, starting in November 2014 on varying weekdays, showed that the best weekday to invest during this time period would have been Friday. The worst weekday to buy would have been Tuesday, ending up with 0.61 % less BTC than an investor who always bought on Friday. However, both strategies yielded an overall return on investment of about 1’200 %.

In summary, both distributions of hourly and daily returns tend to center around 0 %. This makes sense in the light of the Random Walk Theory, which says that asset prices follow a random path – at least in the short run. Any efficient market should not have easily exploitable patterns, such as consistently outperforming hours or weekdays. While cryptocurrency markets are still nascent and lack broadly accepted valuation models, the continuous professionalization of the space – for example, the introduction of both cash settled and physically delivered Bitcoin futures, or increased market participation by arbitrage funds and high frequency traders – will slowly eradicate any remaining inefficiencies in the markets.

Seasonal Patterns in Bitcoin and Gold

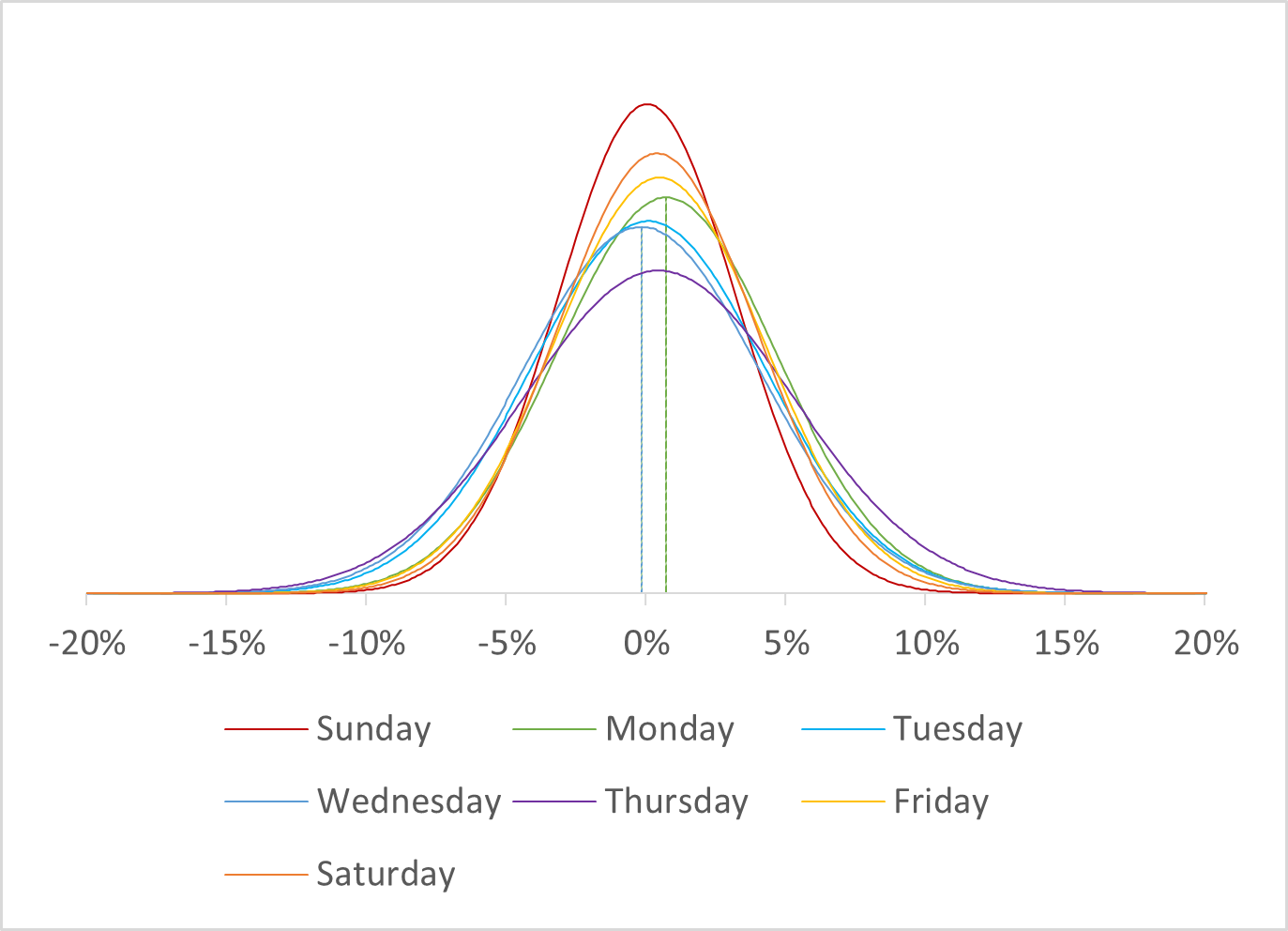

Gold has revealed patterns in half-year, monthly, and even intraday data. Between 1985 and 2018, gold’s price followed a seasonal pattern two-thirds of time. In the second half of the year, between May 5 and January 21, gold saw gains averaging 5 %. Over the same 38-year time span, the first half of the year averaged 0 %.

On the monthly chart, gold prices have historically gone up in August, September, November, and January, which matches the half-year trend data.

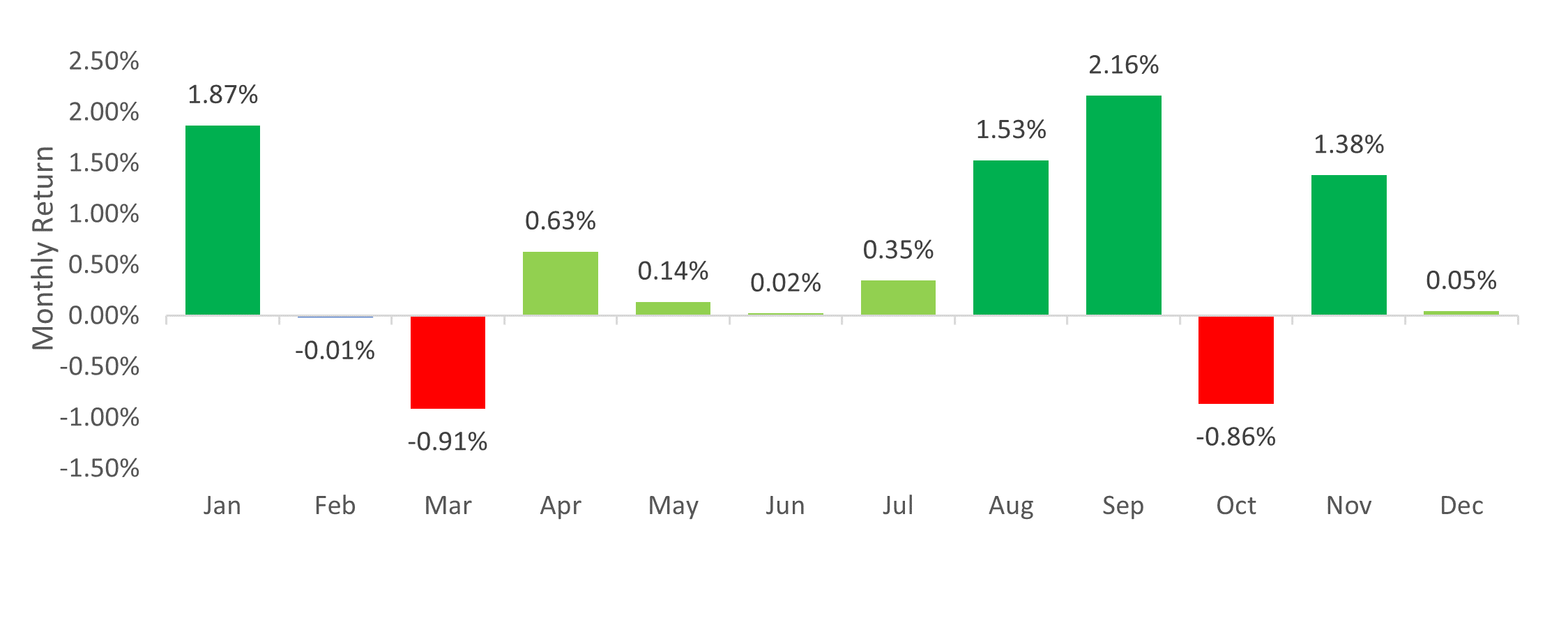

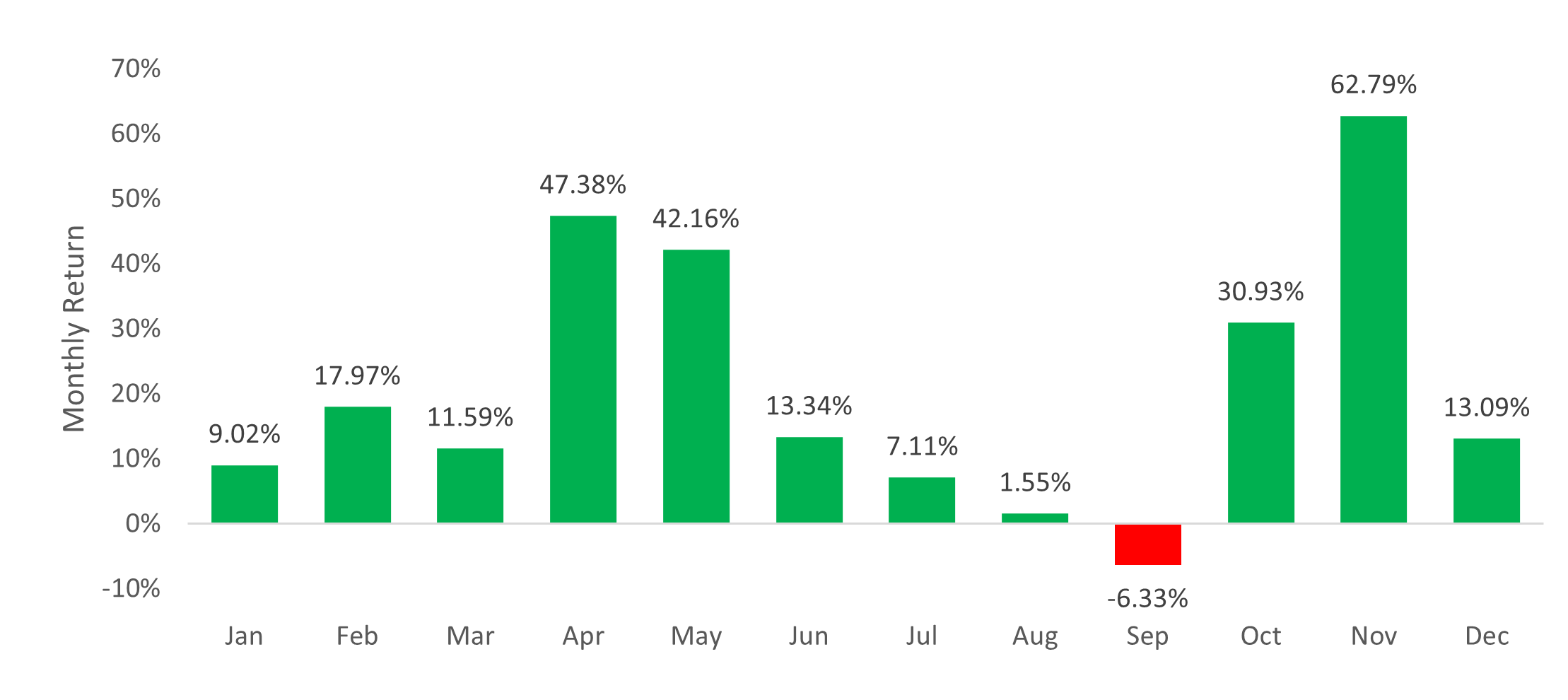

Unlike gold’s pattern of rising in the second half of the year, Bitcoin’s bull markets have occurred in spring and fall. Gold’s best month was September whereas Bitcoin’s worst month was September on average. Gold’s worst month is usually March, and Bitcoin’s best month has been November.

Using one-minute intraday prices of gold over a five years span from 1998 to 2002, German gold analyst Dimitri Speck found that the gold price typically fell during the first two hours of trading in New York, particularly at the time of the London PM fixing at 10:00 am EST. However, Speck’s analysis used over 1,000 days of trading and millions of individual prices. The statistically significant results could only point in one direction: manipulation. Famous for using data to uncover the Libor manipulation, “Libor-Hunter” Rosa Abrantes-Metz published Speck’s charts on Bloomberg in 2013, and lawsuits began piling up against Deutsche Bank. Deutsche Bank made a private monetary settlement with plaintiffs. US courts accused Bank of Nova Scotia, Barclays Plc, HSBC Holdings Plc and Societe Generale of conspiring to manipulate gold prices; however, accusations against UBS were dismissed.

The original idea of the gold fixing was to bring the largest bullion banks together in order to aggregate their order books based on trading volume. In the cryptocurrency market, this is not done behind closed curtains with an oligopoly of banks. Instead, this is done by third party companies that use weighted averages of exchange trading volume. The only caveat is that exchange traded data is often accused of being manipulated towards the upper bound. However, the digital nature of cryptocurrency makes them easy to remove from one exchange and onto another exchange. Unlike the spot price for physical gold, the spot price for cryptocurrencies is relatively robust to manipulation.