Onboarding the Next Wave to Crypto

Nov 9, 2020

The global adoption of cryptocurrencies continues at a rapid pace. Last week has seen another push, this time coming from fintech giant PayPal, who announced that they will bring cryptocurrencies to 26 million merchants in early 2021. Their 300+ million customers will also be able to purchase Bitcoin, Ether, Litecoin and Bitcoin Cash directly, and use them as a means of payment in their day-to-day transactions.

The cryptocurrency markets reacted positively to the news: Since the announcement, the total crypto market cap rose from ca. $370 billion to $405 billion at the time of writing (+9.5%).

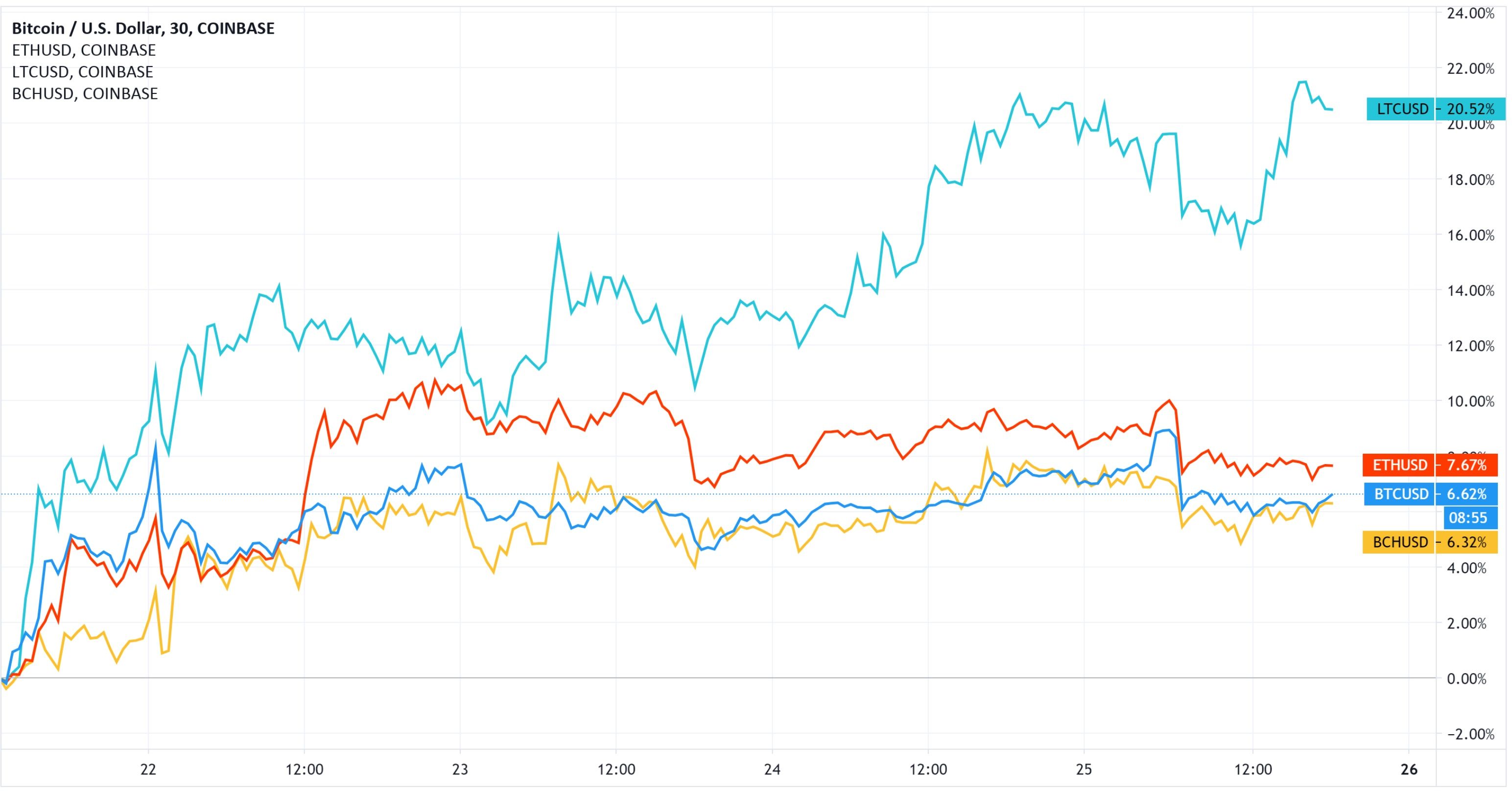

Illustration 1: All four currencies to be listed on PayPal initially have risen since the announcement just after noon on Oct. 21. Litecoin managed to outperform and is up +20.5% at the time of writing.

A phenomenon that is occasionally seen in the cryptocurrency markets is that a coin or token experiences a sharp short-term price increase once it gets listed on a major exchange. One recent example of this are the listings of REN and BAL on Coinbase on Oct. 1 – the price of REN increased by +19.1% that day, that of BAL by +13.1%; however, the sustainability of these short-term price increases warrants closer inspection. In the future, it is not inconceivable to see volatility in the markets following “PayPal listings”.

Meanwhile, the crypto features that PayPal offers are very limited – crypto transfers in and out of an account or between users will be disabled, at least initially. This means that purchases there give no access to the trustless, disintermediated crypto ecosystem and transactions can always be censored (as opposed to on-chain transactions on public networks). Users will also not be able to explore the quickly growing DeFi ecosystem, as well as other crypto-native features and decentralized applications.

Escape the Walled Garden

In the end, what might arise is a situation similar to the early days of the Internet: Early providers, for example AOL, enabled going online through proprietary software, but the full depth of the web remained inaccessible. This familiarized users with the concept of using the computer to gain access to distributed information. Similarly, PayPal may familiarize users with the concept of holding cryptocurrencies as a means of payment/store of value.

If history is any indication, though, human curiosity will drive people out of the walled garden of the PayPal solution, and incentives such as a non-zero interest rate savings account in DeFi in a world where yield is scarce will encourage this.

Central Bank Digital Currencies

Also, the news might be relevant in light of potentially upcoming central bank digital currencies (CBDCs). Recently, Federal Reserve Chair Powell mentioned that the U.S. is looking closely into digital currencies, and that 80% of central banks globally are. As such, CBDCs might become a reality sooner than would have been thought possible a year ago, and the push that the online realm received through the pandemic may have been a supporting factor. The proposed models for CBDCs differ in their details, but perhaps the most important distinction is between “wholesale CBDCs” (serving mostly financial institution as a digital settlement currency) and “retail CBDCs” (accessible to the public, as an addition to or a replacement for physical cash), with a spectrum of hybrid solutions in between. While wholesale CBDCs might bring incremental efficiency enhancements to the financial sector, it is the retail CBDCs that would represent a paradigm shift and whose economic implications be far greater. To name one example, a retail CBDC might allow implementation of monetary policy measures on a broad scale much more easily – be it in the form of applying negative interest rates directly to a CBDC, or in the form of distributing “helicopter money” to all wallet owners/citizens.

Bitcoin’s Layer 2?

Bitcoin has long struggled to find consensus around a suitable way to scale the blockchain (the dispute over which has also spawned Bitcoin Cash and Bitcoin SV), and the Lightning Network has so far failed to gain any significant amount of traction.

The current global payments infrastructure could serve as an intermediate-term “second layer” scaling solution that still relies on trust. PayPal’s push towards cryptocurrencies may be an early, global step towards this (if/once crypto deposits are enabled), whereas in Switzerland and Europe, integration of cryptocurrencies with the payments infrastructure is advanced most prominently through Worldline.

This would also be aligned with one potential vision for scalability that early Bitcoin contributor Hal Finney had – Bitcoin would serve as a limited supply reserve currency, while day-to-day transactions are handled through existing infrastructure. However, there should still always be the option to transact in a permissionless, censorship-resistant fashion directly on-chain.

I see Bitcoin as ultimately becoming a reserve currency for banks, playing much the same role as gold did in the early days of banking. Banks could issue digital cash with greater anonymity and lighter weight, more efficient transactions.

Hal Finney

Institutional Market Grows

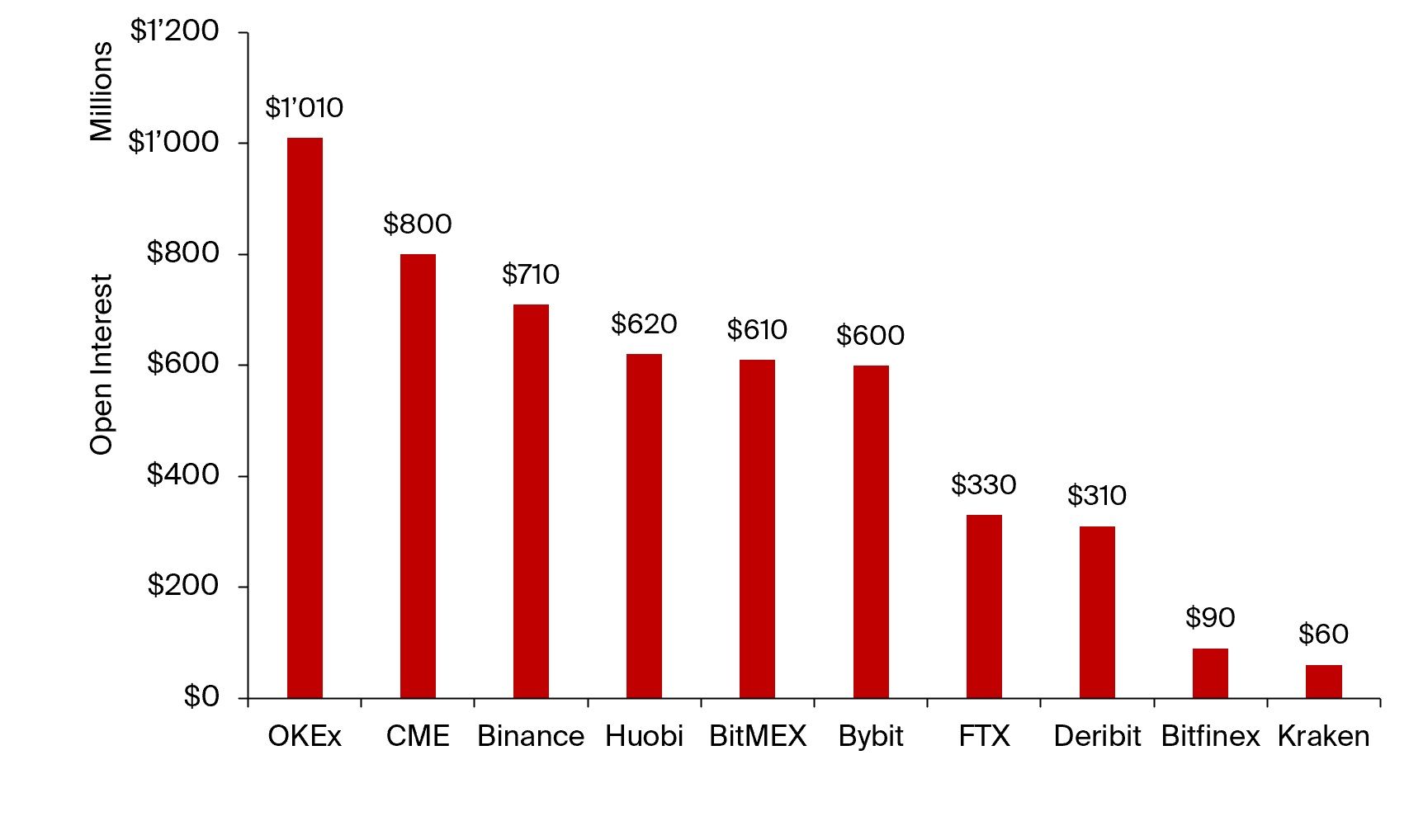

The attention the crypto space received from well-known financial institutions and investors is growing. In fact, the CME Bitcoin futures market, which is often seen as an indication of institutional participation due to its accessibility through the traditional financial infrastructure, is now the second largest in the market as measured by open interest (representing the amount of current positions in a derivative).

Illustration 2: The total open interest in derivatives now stands at over $5 billion across exchanges. The CME Bitcoin futures have recently claimed the number 2 spot, with $800 million in open interest.

Prominent investors have reaffirmed their investment hypothesis for Bitcoin as an alternative asset class or an inflation hedge. Paul Tudor Jones, an American billionaire hedge fund manager, reiterated on his small single digit percentage allocation (originally disclosed in May) to Bitcoin; JP Morgan noted Bitcoin’s “considerable upside”; and Fidelity published a report on Bitcoin’s role as an alternative investment. The stance of central banks towards monetary policy that may have led to people thinking more in detail about the value of money remains largely unchanged, and talks of additional stimulus have been occupying traditional markets. If worries around inflation down the road grow, Bitcoin may present a credible alternative way to store wealth.

I’ve never had an inflation hedge where you have a kicker that you also have great intellectual capital behind it. So that makes me even more constructive on [Bitcoin]. If you think about it, if you’re long [the US] 2s30s [yield curve] you’re effectively short the bond market, that’s your inflation hedge. You’re really betting on the fallacy of mankind rather than its ingenuity and entrepreneurialism.

Paul Tudor Jones