The Evolving Open Finance Ecosystem

Nov 10, 2020

4 August 2020

The decentralized finance (DeFi) craze continues, and the total value locked in DeFi protocols is now closing in on $3 billion. The success of Compound’s COMP token in attracting users has enticed other protocols to also issue their own tokens. Recently launched examples include YFI, the token of yearn.finance (a DeFi gateway and liquidity aggregator), and MTA, the governance token of the mStable protocol (which attempts to de-fragmentize the ecosystem and yields of “same-peg” assets, such as DAI, USDC, and TUSD, which are all pegged to the U.S. dollar).

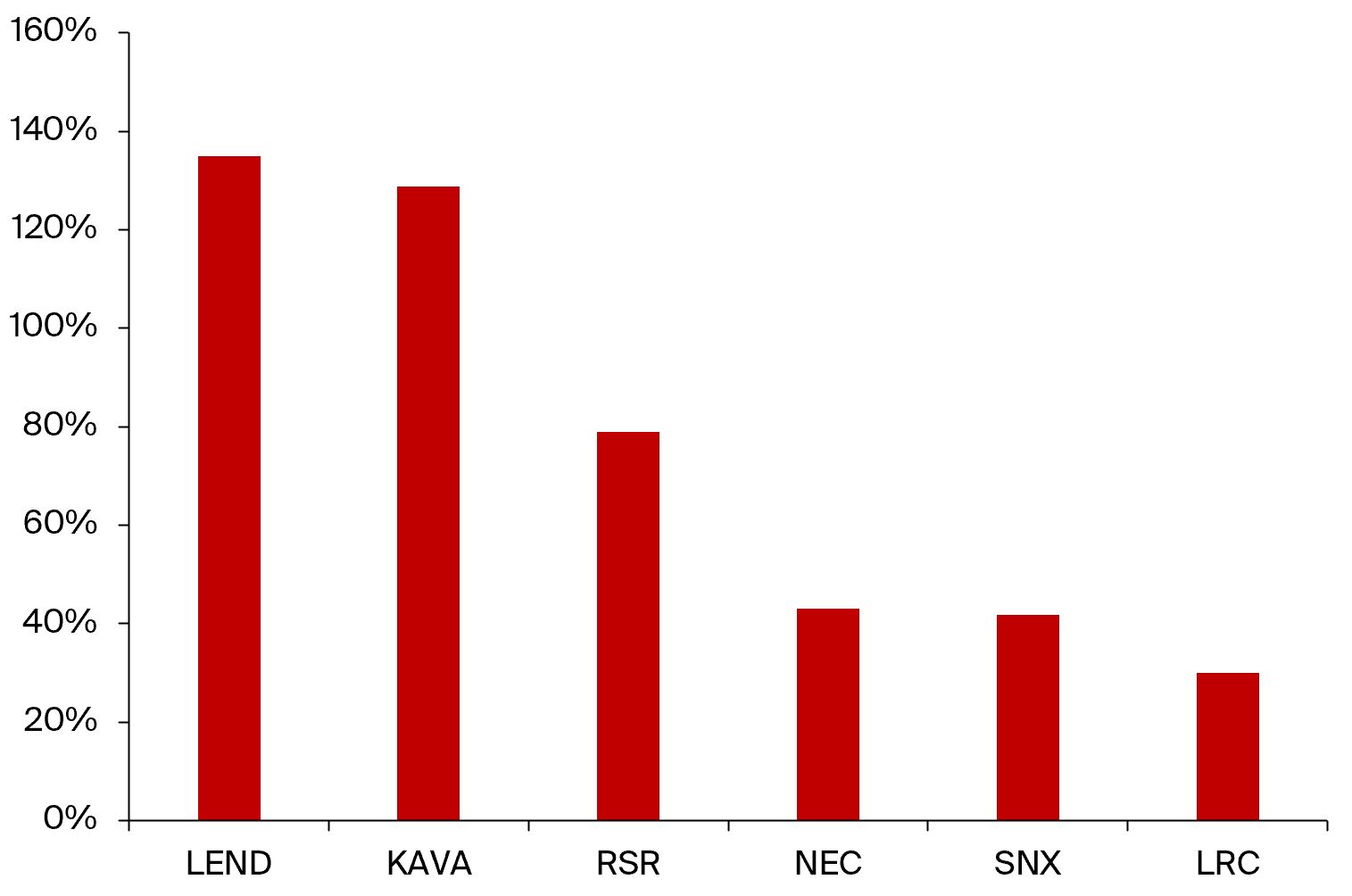

Illustration 1: 14-day returns of top performing coins of DeFi-related areas. Aave’s LEND token takes the number one spot with a return of 135% over the past two weeks.

The total value locked in DeFi is constantly increasing due to the high annualized yields that can be obtained using various protocols, ranging from 10% to >100% annualized percentage returns on USD-pegged stablecoins in some cases. This has generated a new group of crypto users that call themselves “yield farmers,” a concept which was outlined in detail in a previous episode. These yields are subsidized both by the high demand for stablecoins, as well as by traders bidding up the price of governance tokens (such as COMP) which are ultimately crucial for realizing said yields.

Protocol Security Increases While such high yields on USD-pegged stablecoins may persist for some time, they are certainly surprising given that the USD interest rates outside of the crypto space are at record lows of about 0%. Part of the higher yields can be ascribed to the smart contract risk that is inherent to achieving the yields through DeFi protocols. However, given that any large DeFi protocol presents honeypots for hackers to the tune of hundreds of millions of dollars’ worth of collateral, the security of these protocols becomes a function of time. The longer they exist and are out in the wild for anyone to access and review or exploit, the more unlikely it becomes that they have critical vulnerabilities that would put funds at risk. This is one of the powers of open, permissionless technologies. Thus, on a multi-year horizon, the amount of yield that can be explained by smart contract risk will diminish.

The “Impossible Trinity” Additionally, in the long run, the yields on USD in DeFi and in the traditional financial markets should converge by force of the “Impossible Trinity”. This macroeconomic concept states that it is impossible to have all of the following three parameters at the same time:

- A fixed exchange rate (such as a peg to the USD)

- Free capital movement

- An independent monetary policy

The most spectacular example of the problems that might arise from this in practice occurred in 1992, when the British Pound came under pressure from speculators, eventually leading to a break of the peg to the German mark and devaluation of the GBP, as well as the exit of the UK from the European Exchange Rate Mechanism after a day dubbed “Black Wednesday.”

In DeFi, the exchange rate of stablecoins is pegged to another currency or asset by definition. Free capital movement is also a given in the blockchain world, due to its permissionless nature, and introducing government-issued currencies to the crypto space through fiat on-ramps is becoming increasingly efficient.

Hence, the monetary policy of stablecoins such as DAI cannot be independent (which it also does not try to achieve – the task of Maker’s governance is simply to read the market for the correct rate). Deviations of the interest rate for (synthetic) USD in DeFi is subsidized by traders and stablecoin users that are willing to pay a premium for access to USD-pegged tokens. This imbalance opens up arbitrage opportunities, which will be exploited once sufficient liquidity is available in the crypto markets, and this will bring down yields.

Credit delegation Another DeFi innovation that has attracted a lot of interest is the introduction of credit delegation by Aave. Credit delegation essentially enables undercollateralized loans: Person A deposits assets in the DeFi protocol and signs an agreement with Person B that allows them to draw a loan against the collateral of person A. The agreement is automated, in this case, through OpenLaw, which aims to bring legal contracts to the blockchain through smart contracts.

Such types of loans have long been the “holy grail” of DeFi since they combat the current restrictions of capital inefficiency that arise from the need for overcollateralization of loans. A typical collateralization ratio in today’s DeFi landscape would be the one from MakerDAO Vaults, where a 150% minimum collateralization is required – meaning, for example, that for $300 worth of ETH, only $200 worth of DAI can be generated.

Credit delegation does not remove the need for collateral, it merely shifts the collateral type from a tangible asset (money in the form of cryptocurrency) to an intangible asset, namely the reputation of the borrower. Early agreements will likely be signed between wealthy crypto holders and trustworthy counterparties with high liquidity needs, such as market makers.

The cost of building up this reputation or (opportunity) cost that is associated with losing the reputation must be at least as high as the potential gain from exploiting such an undercollateralized loan, thereby capping the amount that can be lent out.

Decentralized Identities This also brings up the topic of decentralized identity. A decentralized, undercollateralized lending and borrowing market needs identifiable borrowers that can be held accountable for the loans they take out. As such, initiatives that connect real-life identities (individuals or companies) to on-chain addresses may become a crucial component for future on-chain lending markets.

Such initiatives can take two forms. The first is through a trusted third party that verifies currently used identity documents such as passports and government-issued IDs. This would simply port the legacy system onto the blockchain, but introduces a centralized point of failure (the third party ID verifier).

The second, more progressive form is through “social graphs” (as, for example, developed by BrightID), which means that a network of social connections is established, and people within a small group can vouch for each other’s uniqueness. Being more connected to other groups strengthens the legitimacy of a group, since the denser a network becomes, the harder it is to manipulate it.

A trusted, decentralized identity system would unlock a swathe of new use cases. One of them would be decentralized credit scores to determine the amount of an undercollateralized loan that an on-chain identity can take out. Another obvious use case of verifiably unique identities is voting, where it is paramount that sybil attacks (one person creating multiple identities) are prevented.

Given that controlling such a digital identity that is strongly linked to one’s real life identity would likely come with a great deal of power, safeguarding access to the digital identity will be of utmost importance. Similar to the management of a private key that holds significant amounts of cryptocurrency, losing access to the identity would be a major disaster for the individual. Social graphs can also help here via social recovery mechanisms, such as the ones implemented in crypto wallets like Argent or Tatoshi. If a user loses access to the wallet or identity, friends and family can restore it, without being able to access the wallet on their own.

Conclusion More and more pieces of the puzzle that might eventually represent the decentralized economy are coming together. The vision of where this is heading is to empower people to autonomously take control of their finances, their identity, their social networks, and their access to protocols supporting this. The recent Twitter hacks further highlighted the danger of identity theft and the case for decentralization to avoid single point of failures.

The role of the blockchain in this is to serve as a source of immutable truth. Along the way, permissionlessness will lead to efficiency enhancement in credit and other markets, since anyone is allowed to build and innovate (maximizing competitiveness) and rent-seeking is minimized.