Algorithmic Stablecoins

Apr 15, 2021

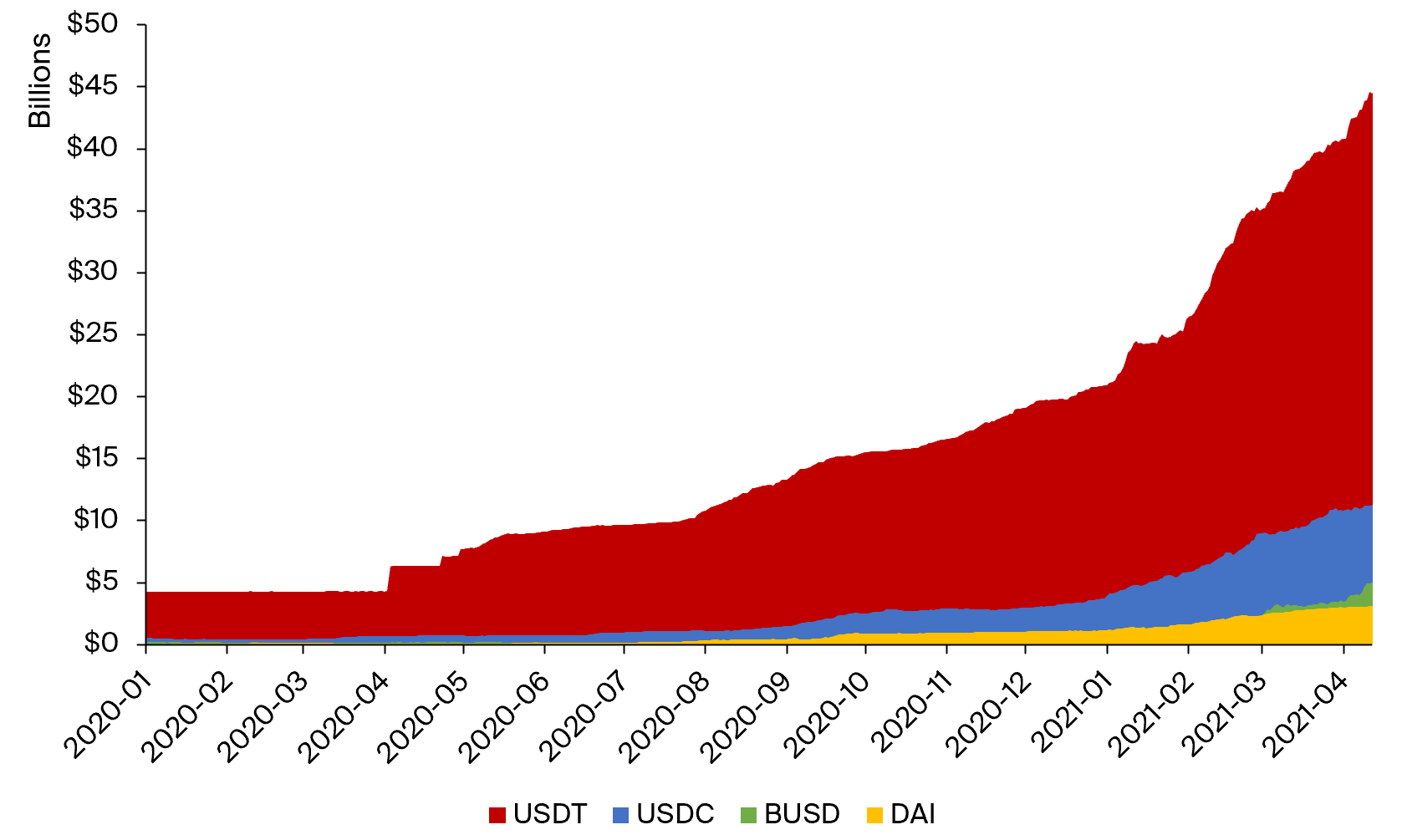

Stablecoins have shown tremendous growth since the beginning of 2020, increasing their total market capitalization from ca. $5 billion to almost $50 billion.

Illustration 1: The total market capitalization of stablecoins has increased 10x since the beginning of 2020, with Tether (USDT) being the largest and most used stablecoin.

In general, these stablecoins can be classified in three categories: off-chain collateralized, on-chain collateralized, and algorithmic.

Types of Stablecoins

The two largest stablecoins, USDT and USDC, or smaller ones in other currencies such as EURT or XCHF, are examples of off-chain collateralized stablecoins. They are typically backed by bank deposits, which are regularly audited (including Tether as of this year), and minted by a centralized entity that maintains these reserves. Thus, they keep their peg to a fiat currency through trust in that entity to always honor creation and redemption requests of tokens versus bank deposits.

The second basket, on-chain collateralized stablecoins, include Maker’s DAI, Synthetix’s sUSD, or the newer LUSD by Liquity. They are minted permissionlessly through DeFi protocols by depositing high-quality collateral (for example ETH in the case of Maker). The peg is maintained through backing with enough cryptocurrency collateral – DAI and sUSD require collateralization ratios of 150% and 600%, respectively, and collateral is liquidated for the protocol’s stablecoins if this threshold is crossed. Both have managed to remain close to $1 during their lifetime (although it required tinkering with protocol incentives in the case of sUSD), and thus enjoy a relatively high level of trust. In total, they make up about $4 billion of the total stablecoin market cap, but this number might increase soon due a Maker governance vote to massively increase the debt ceiling of ETH and wBTC vaults.

The third category, algorithmic stablecoins, aim to achieve higher capital efficiency than collateralized stablecoins. They recently were moved back into focus with the launch of the Fei protocol, which attracted 639’000 ETH ($1.3 billion) in seed capital to collateralize FEI, but so far failed to establish a solid peg to the USD (see below). Algorithmic stablecoins aim to maintain a peg through dynamically controlling supply and demand of the stablecoin by the protocol. The protocol acts as the “central bank”, increasing supply when the token shows a deflationary tendency, and reducing it when the purchasing power of the stablecoin drops. The rules for doing so are embedded in a smart contract, and changing them is only possible through social consensus or more formal governance votes tied to a governance/seigniorage token.

The primary problem that such stablecoins have to solve is how to build trust in the system. The other two categories largely inherit their trust from the collateral backing them (except for protocol-specific risk, such as improperly handled liquidations).

What approaches have been used to solve this issue?

Variants of Algorithmic Stablecoins

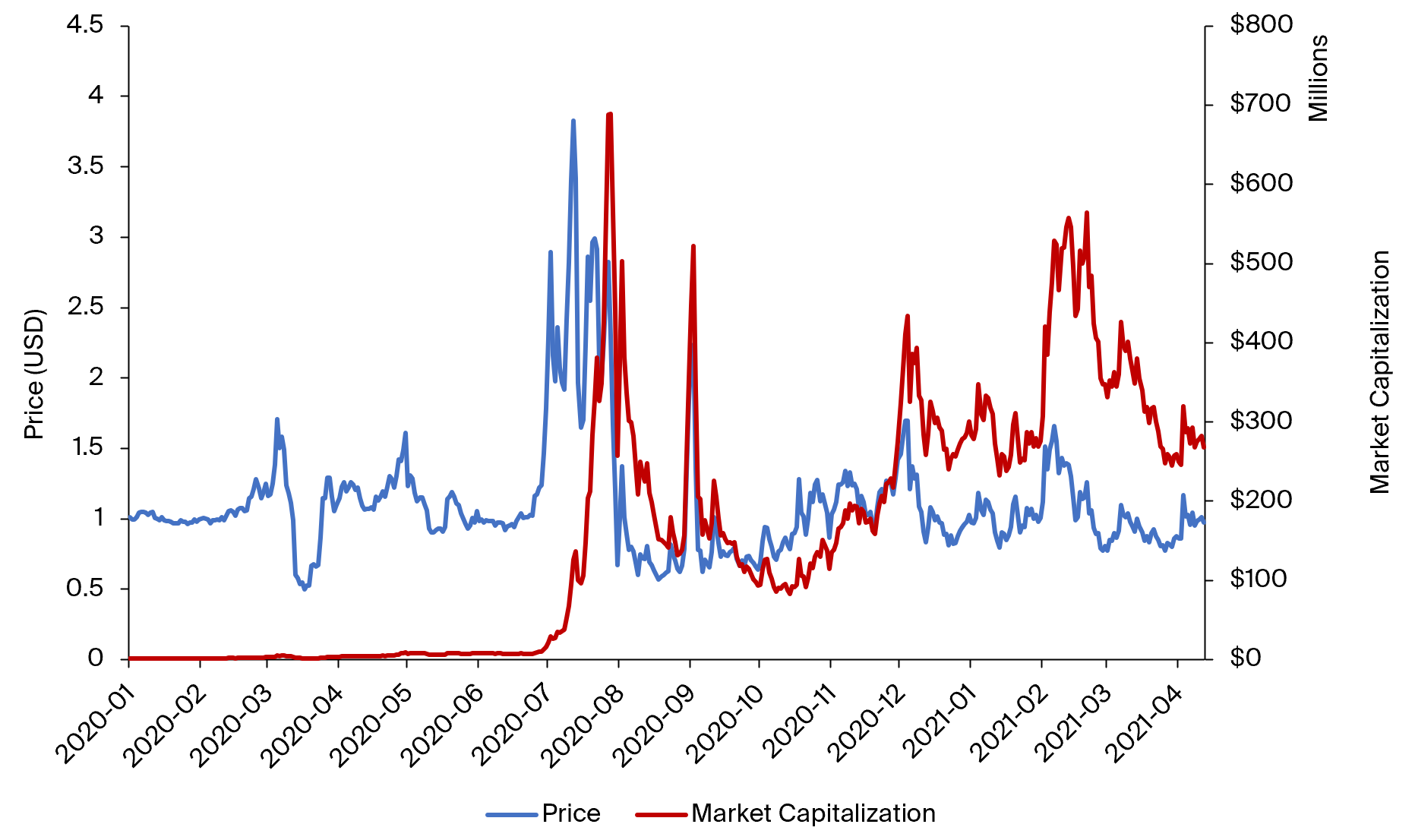

Early attempts at algorithmic stablecoins are “rebase” coins such as Ampleforth (AMPL). Rebase coins adjust the supply based on the going market rate for AMPL. If AMPL trades higher than $1.05 or lower than $0.95, new tokens are issued to holders (if price is above $1.05) or destroyed from holders (if price is below $0.95) to reset the price back to $1. This effectively transfers volatility from price to market cap: Instead of the price changing with varying demand for a rebase token, the market capitalization does. As such, AMPL effectively serves as a speculative vehicle rather than a powerful stablecoin.

Illustration 2: While the price of rebase tokens such as AMPL trends towards $1, their market cap is just as volatile as that of other cryptocurrencies.

AMPL uses a single-token model in which holders of the token benefit from an expanding supply (seigniorage) due to increasing demand, but also have to finance a re-peg if demand shrinks and AMPL trades below $0.95 through supply contraction.

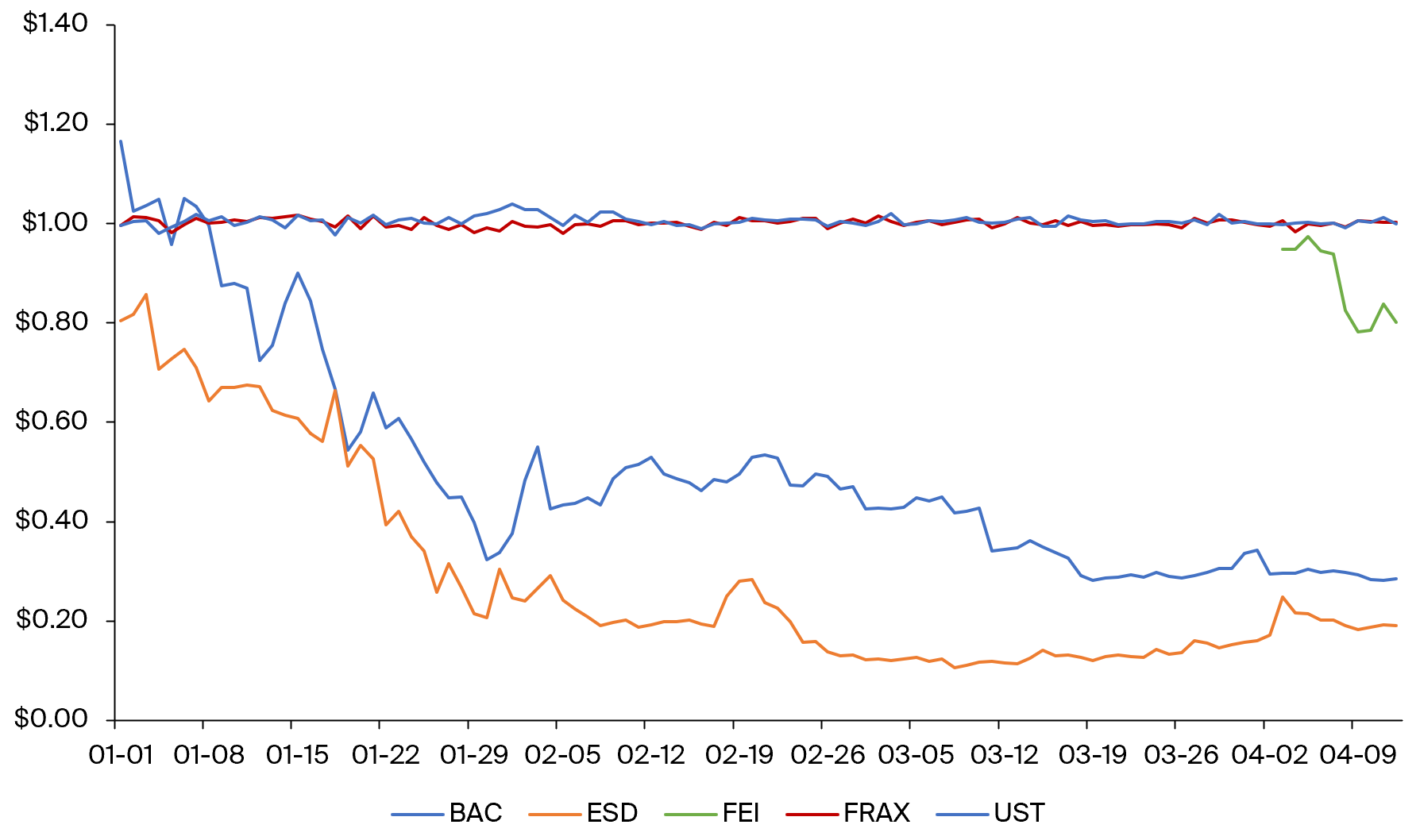

Other algorithmic stablecoins use multi-token models. These separate the stablecoin function from other protocol features, such as governance or value accrual. One of the early designs stems from Basis, which raised $133M in 2018, but was shut down for regulatory reasons. In that design, which was later picked up again by Empty Set (ESD) in a slightly modified version and Basis Cash (described here), three tokens exist: Basis Cash (BAC), Basis Shares (BAS), and Basis Bonds (BAB). Basis Cash is the stablecoin and aims to maintain a peg to $1. Basis Bonds are always redeemable at par for Basis Cash from the protocol treasury as long as it has BAC available. Basis Shares are most closely related to the protocol value and BAS holders benefit from minting of new BAC by the protocol. If the price of BAC drops below $1, users can buy BAC for that discounted price and redeem them for BAB. Once price rises above $1, new BAC is minted and bond holder can redeem their tokens for BAC.

A multi-token model is also used by TerraUSD and Frax, both of which have been vastly more successful in maintaining their peg than Basis Cash or the Empty Set Dollar. TerraUSD outsources volatility to LUNA tokens. Frax, on the other hand, targets variable, fractional collateralization ratios depending on the market price of FRAX, and is governed by Frax Shares (FXS). The newest algorithmic stablecoin on the market, Fei protocol’s FEI (governed by TRIBE token holders), slipped lower almost immediately after start of trading, which may however have been an artifact of the launch format.

Illustration 3: Of five different algorithmic stablecoins, only FRAX and UST managed to consistently remain at peg.

Conclusion

Creating an algorithmic stablecoin that manages to maintain its peg is hard – it requires well-balanced protocol incentives and a credible stability mechanism. Both Basis Cash and Empty Set Dollar do not seem to meet these requirements. On the other hand, FRAX and UST have been remarkably stable.

One major problem to solve before the protocol can sustainably expand the supply is to build trust – this took years even for fully on-chain collateralized stablecoins like DAI.