Collateral in DeFi

Jun 22, 2021

Over the past weeks, several headlines seem to have impacted the crypto markets. MicroStrategy announced their plans to raise more money from investors and use the proceeds to purchase BTC, and completed their purchase on Monday. On the other hand, China continues to make moves against crypto, and its central bank has instructed domestic banks to shut down accounts with crypto-related activity.

In the meantime, Bitcoin has held up stronger than the altcoin market, as illustrated by its rising dominance (percentage of overall crypto market capitalization) since mid-May. Altcoins also suffered more during the most volatile phases of the price drop, possibly due to worse liquidity in their markets compared to Bitcoin.

Illustration 1: Bitcoin’s share of the overall crypto markets has fallen throughout March and April, but started to recover in late May.

Volatility increased

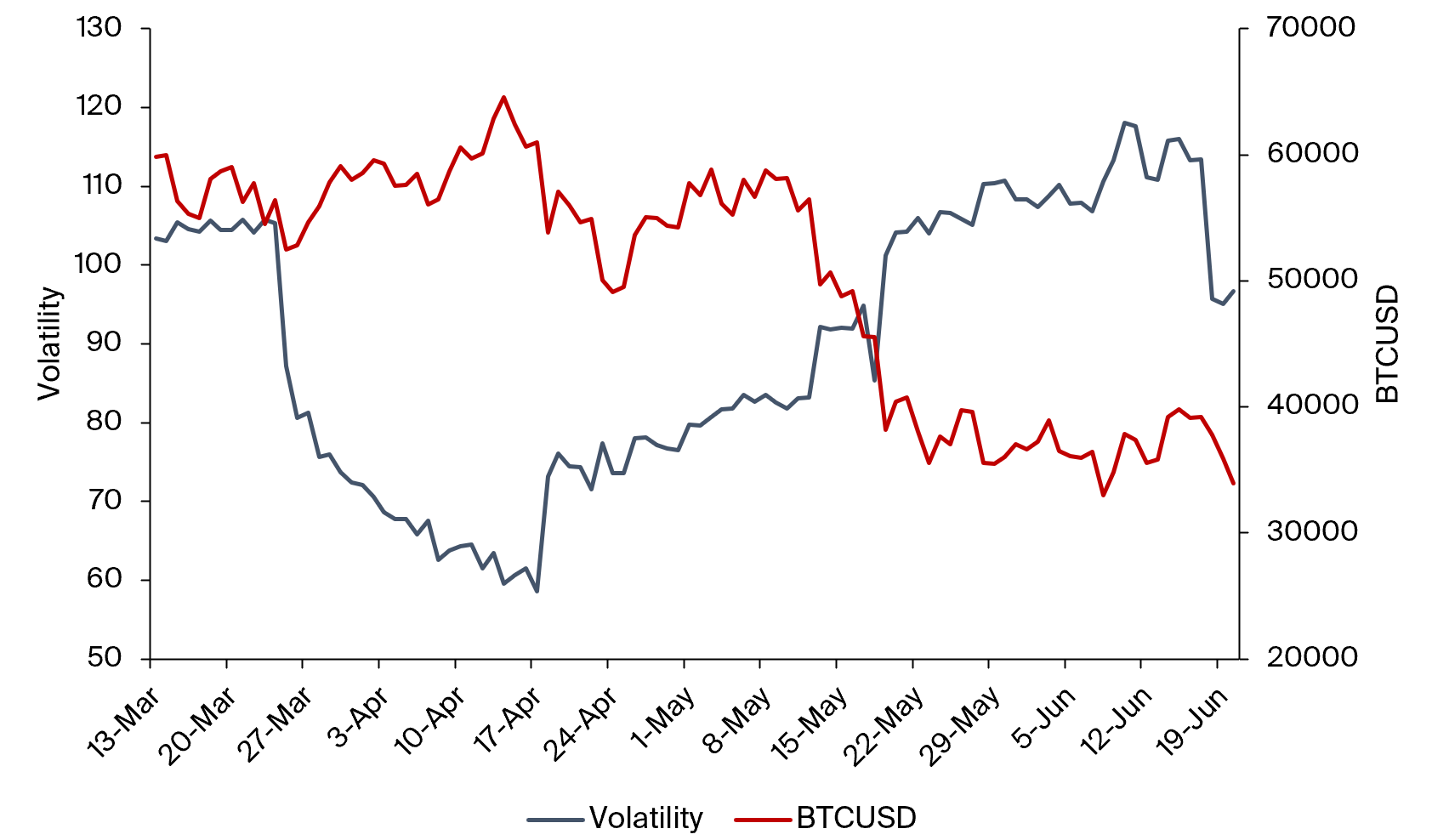

Volatility of the markets has also been on the rise since mid-April, as illustrated by Bitcoin’s annualized 30-day historical volatility.

Illustration 2: Bitcoin’s annualized 30-day historical volatility has been rising since mid-April and sustained high levels. Other cryptocurrencies show a similar trend.

Part of the sharp moves in price can be traced back to the liquidation of leveraged positions. During the drop in mid-May, almost $10 billion worth of positions were unable to meet their margin requirements and got liquidated, adding selling pressure to the market.

In the meantime, the DeFi ecosystem continues to grow, and now boasts over $50 billion in total value locked across protocols. Liquidations in DeFi due to lack of collateralization of positions happened as well, albeit to a much smaller extent than on centralized exchanges. Intuitively, this makes sense, as positions in DeFi are overcollateralized, whereas centralized exchanges often offer leverage above 1 (i.e. collateralizations below 100%). But what currencies are actually used in DeFi as collateral?

Collateral in DeFi

The three largest DeFi protocols in the borrowing/lending business are Aave ($10.4 billion), Compound ($6.4 billion) and Maker ($6.3 billion). Maker issues its own stablecoin, DAI, which can be minted against collateral and has proven resilient in the face of market volatility. Aave and Compound facilitate multi-asset money markets and accept a wide range of collateral types to borrow against.

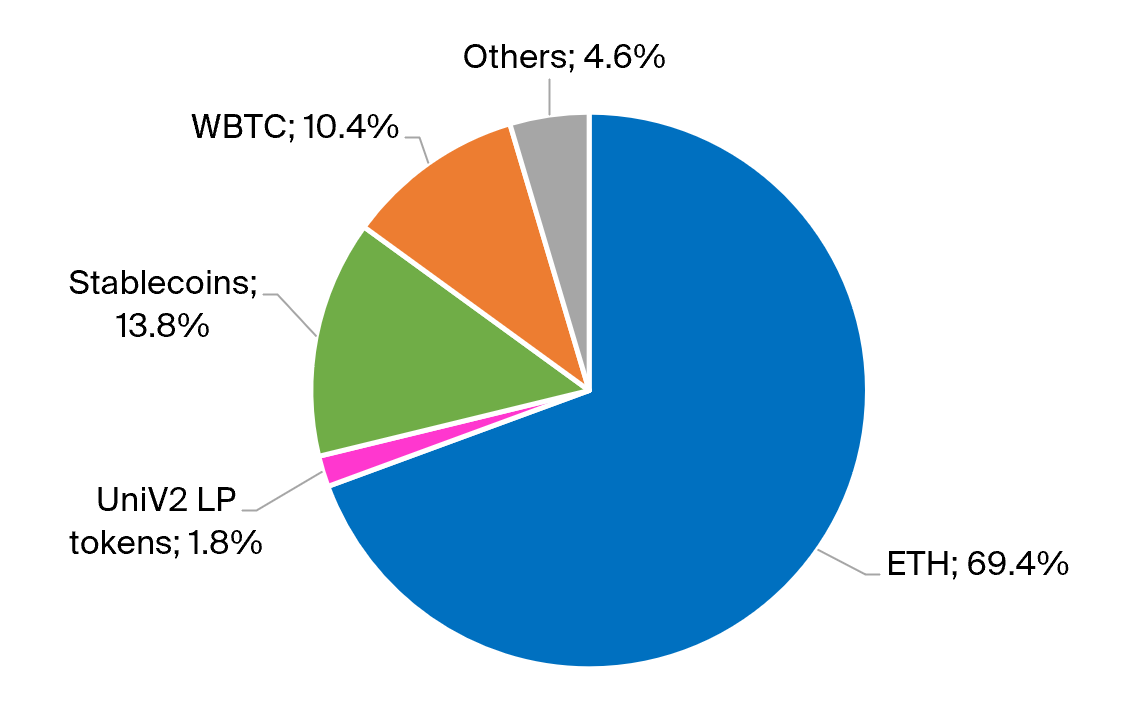

Illustration 3: Collateral in Maker is mostly composed of ETH (close to 70%), and stablecoin collateral (mostly USDC) aimsto be a temporary solution to satisfy DAI demand.

The most frequently used collateral to mint DAI is ETH, at close to 70%. Stablecoins were introduced with the goal to act as a temporary fix for high DAI demand last year. Additionally, wrapped BTC (WBTC, 10.4%) also makes up a decent share of the protocol collateral. Last but not least, Maker also allows Uniswap V2 liquidity provider tokens to be used as collateral, from which 1.8% (44 million) of the total DAI have been created.

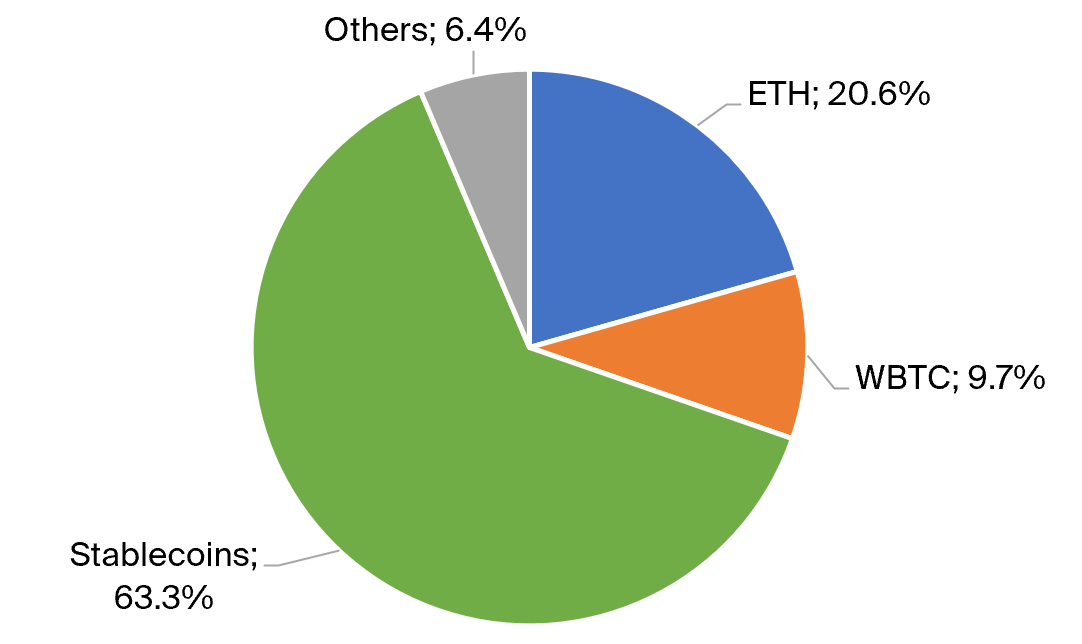

Illustration 4: Almost two-thirds of the total supplied tokens in Compound are stablecoins. ETH and WBTC make up most of the remaining third.

Compound, on the other hand, does not issue its own stablecoin and thus relies on outside stablecoin liquidity. Stablecoins make up 63.3% of the collateral supplied to Compound. ETH and wrapped BTC account for another 20.6% and 9.7%, respectively.

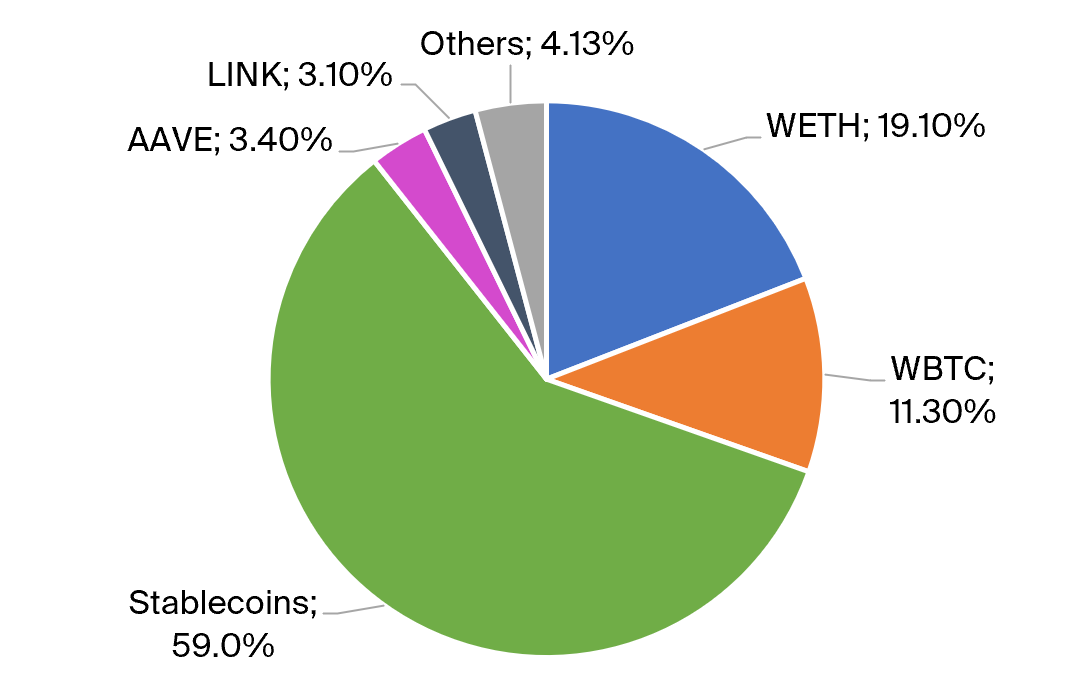

Illustration 5: The picture for Aave is similar as for Compound, with roughly a 2:1 mix of stablecoins and ETH/WBTC as collateral. AAVE and LINK also represent significant parts of the total liquidity.

Aave, the largest protocol by total value locked, has a similar mix of 59% stablecoins and 19.1% ETH/11.3% WBTC. Additionally, its native AAVE token accounts for 3.4% of the total assets supplied to Aave, and LINK makes up another 3.1%.

Protocol Collateralization

The ratio of total assets supplied as collateral versus the total borrows gives insight into the overall protocol collateralization, and – combined with the types of collateral supplied – into the “systemic risk” present in DeFi should a quick and large move to the downside happen for the prices of collateral.

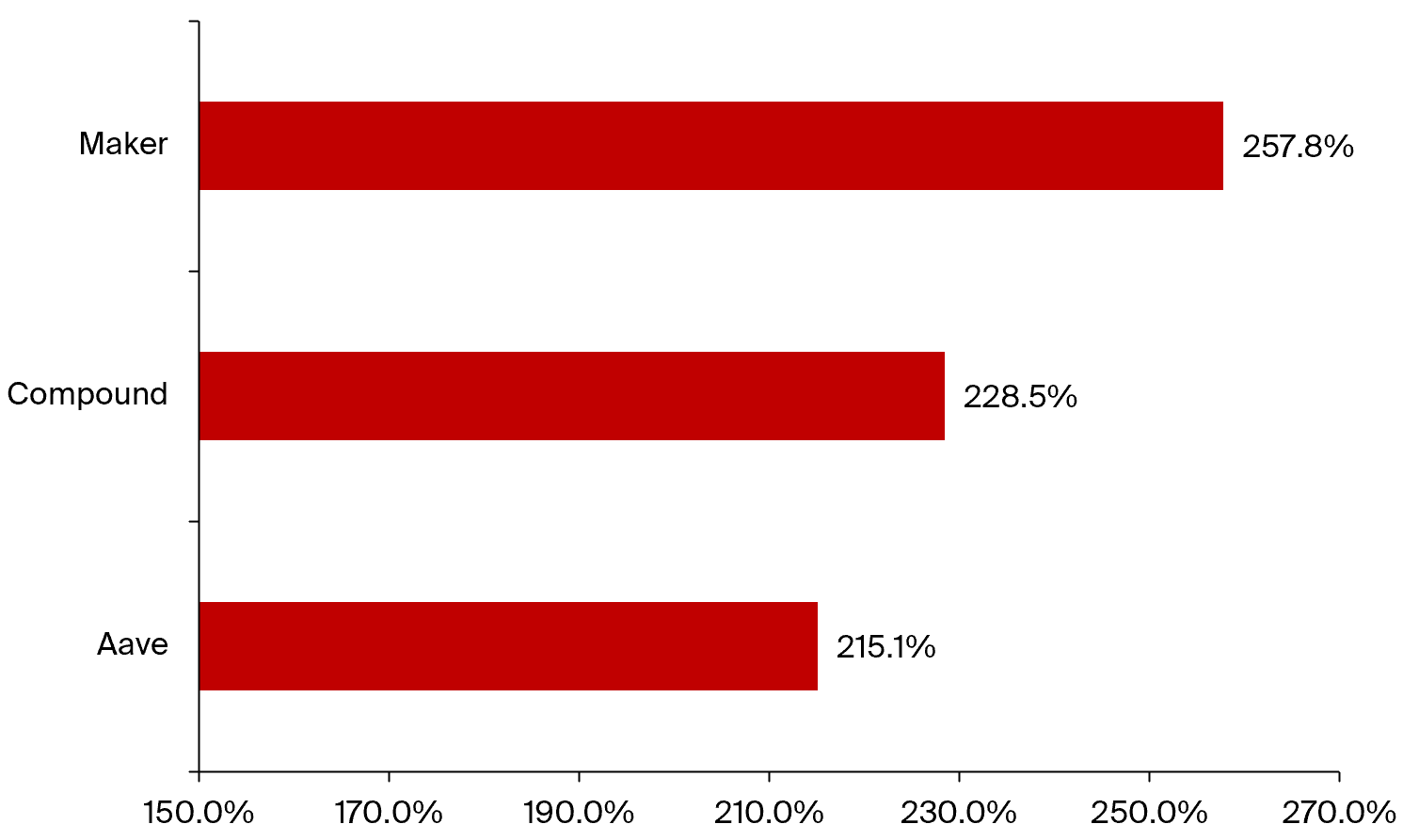

Illustration 6: The Maker protocol has the highest collateralization ratio at 257.8%. No protocol has a ratio below 200%.

Of the three protocols shown here, Maker has the highest collateralization ratio at 257.8% which makes sense, given that its proportion of non-stablecoin collateral is much higher (ca. 70%) than for Compound and Aave (both ca. 30-40%). However, all three protocols have ample room to withstand market volatility, with collateralization ratios above 200%.

Conclusion

By design, DeFi protocols remain well collateralized, and the liquidation methods employed in various DeFi protocols have shown to ensure that it remains that way. Even during high volatility periods, liquidation incentives (resp. penalties from the point of the view of the borrower) will prevent the accrual of debt. However, the soundness of the tokens accepted as collateral is crucial, and protocols can be left with bad debt otherwise, as a recent case showed. It is in the hands of the DAOs governing each protocol to prevent such cases.