From Creating the ‘Creator Economy’ to Useful NFTs

Dec 21, 2021

Fungible or not, that is the question

Defining things by negations is a bit clumsy, but here we are: “non-fungible tokens” are first and foremost tokens that are not fungible (duh!). So, what is fungible? Fungibility is one of the properties an asset needs to possess – next to portable, durable, and divisible – to be a candidate for good money. Fungibility means the asset is of homogeneous texture and can be portioned in equally looking pieces. For example, your Dollar bill is as good/the same as my Dollar bill, they are fungible. However, the two bills are not identical, but clearly distinguishable because they have different serial numbers. Just, usually, nobody is tracking the serial numbers as it very hard to do in the analog world.

Despite much talk about pseudonymous and anonymous crypto currencies, it is essentially the same in crypto. For most practical purposes, your 0.1 ETH is the same as my 0.1 ETH – or any other fungible token on Ethereum. That is what the ERC20 token standard indeed represents. However, the equivalent of the serial number – the Ethereum (or Bitcoin) address – is very closely tracked on the blockchain, and it needs to because that is how we can track transfers without a bank. Traceability of crypto currencies (as addresses or unspent transaction outputs, etc.) and how to achieve/avoid it, is a large privacy topic of its own. If you like to dig deeper, we invite you to read the 4th edition of Themes on “Privacy in the era of cryptocurrencies”, which also looks at traceability and privacy implications of Central Bank issued Digital Currencies.

Coming back, a Non-Fungible Token (NFT) is a unique digital representation of a digital or analog item that contains its origin and history and, in most cases, also contains code governing its behavior, for example actions when it is transferred between holders. In that context, holding an NFT in a wallet is considered the equivalent of being the rightful owner of the underlying item.

How do you create an art NFT, for example? You first create the image (JPG file). Second, you define metadate (author, date, description, tokenURI, etc.). Third, you create the (copy/paste) the NFT smart contract or use an existing one. Fourth, you “mint” one or more of your tokens using the smart contract’s mint() function. Fifth, you make you new tokens available on a marketplace. Six, you wait for a solvent buyer taking an interest in you token(s).

Market structure

Typical NFT markets are much more akin to art markets: only one or few items exist that one or a few collectors want to own, which can lead to pricing that is subjective and potentially reach very high levels as “value lies in the eye of the beholder.”

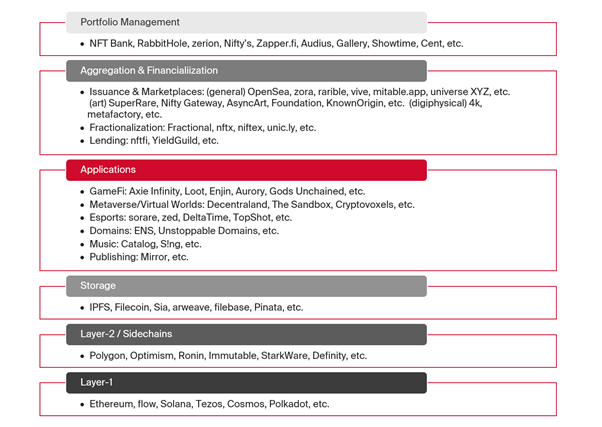

Illustration 1 gives an overview of the NFT space, structured in layers. (1, 2) While Ethereum-based NFTs dominate the space, you can see that different Layer-1 platforms (and different Layer-2 solutions) are active in the space. Each chain maintains their own technical standards and platforms. In the case of Ethereum, most NFTs used to be ERC721 smart contracts, while today ERC1155 is considered the default contract type as it can handle multiple token types in one deployed contract (c.f. comparison).

(3) The punk/ape/kitty look of the artwork is defined in metadata that is not part of the contract, but resides elsewhere. An ERC1155 contract stores metadata by pointing to a web resource (“tokenURI”) that hosts all the colorful pixels. This raises the interesting question of how the availability of metadata is secured to always show the actual/correct artwork and how it is governed. Many storage solutions in use are web3 applications like IPFS for example.

(4) The largest and most dynamic layer is the application layer. NFTs are used across an ever expanding spectrum of application domains, ranging from digital items in games and virtual worlds (metaverse) like weapons or virtual land to domains that represent crypto addresses, to new royalty mechanisms for musicians, writers, and many more.

Here, the possibility to reliably remunerate creators in the secondary market is a key innovation for the art market – and a historical first. A smart contract can, for example, stipulate that the NFT creator receives a percentage of each transfer of the NFT on the secondary market. One way to implement royalty mechanisms in Ethereum-based contracts is defined in EIP-2981.

(5) Aggregator services on the next layer make NFTs created in these applications discoverable and tradable. For example, a NFT market place like OpenSea displays the metadata plus the NFT contract address in a searchable manner and thus facilitates trading. Aside from normal marketplaces, the “reverse” use case also exists. Fractionalization means that several owners share (fractions of) one particularly expensive NFT, thus democratizing access and ownership in a sense.

(6) Finally, tools are emerging that allow users to manage an entire portfolio of NFTs across different protocols and token types.

Illustration 1: Layered overview of crypto space for Non-Fungible Tokens

Concentrated markets

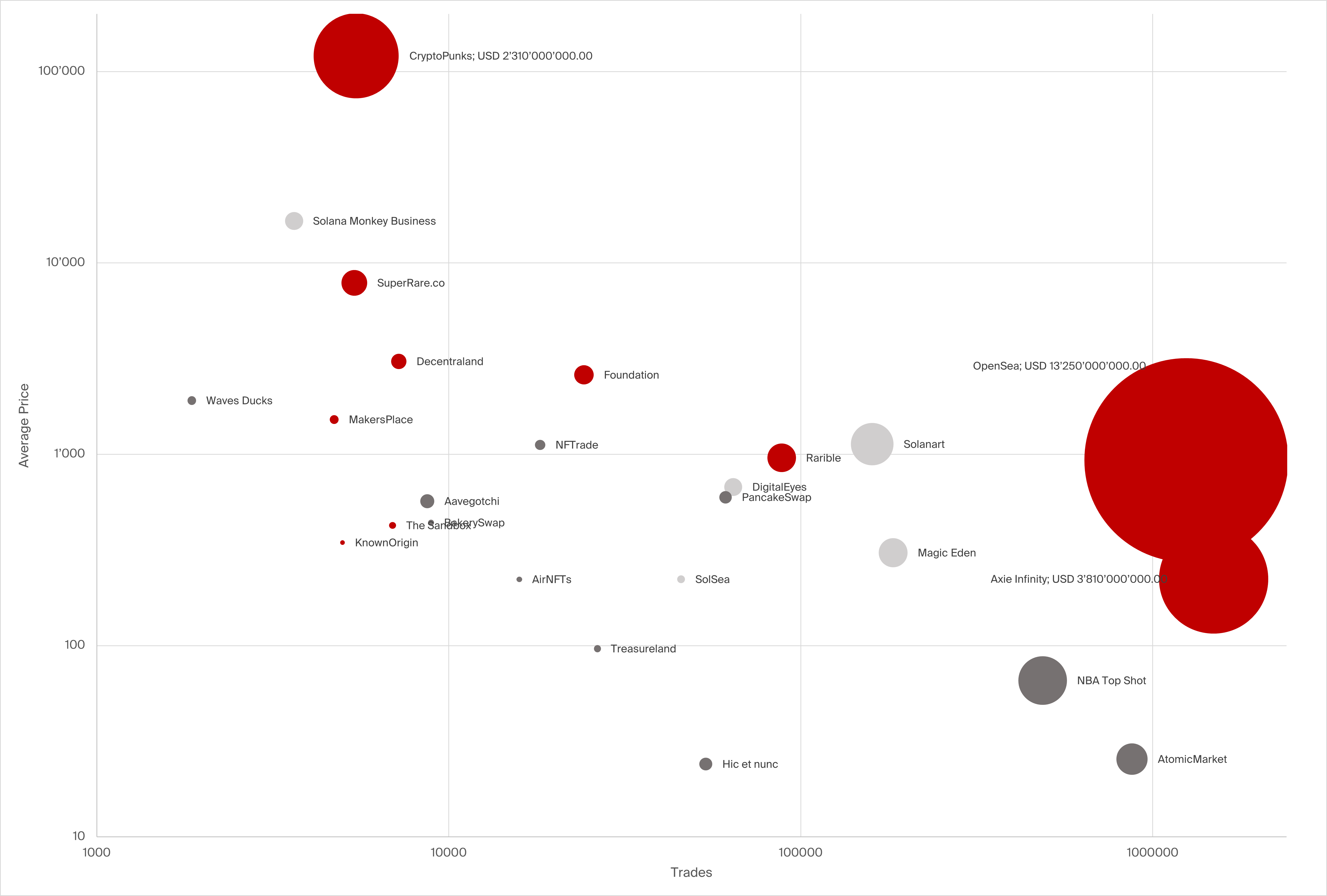

Getting at an encompassing view over marketplaces is challenging as they are scattered across different protocols and each protocol has several marketplaces. Illustration 2 offers an analytic view of the NFT space by showing the top 25 marketplaces (by trading volume in USD).

The top 3 “marketplaces” (naming used by DappRadar.com) all run on Ethereum and together constitute 86% of the total trading volume. The closest contender protocol used for NFTs, Solana, reaches 4.8% of trading volume, and the remaining protocols (flow, wax, Polygon, Tezos, and BSC) together reach less than 10%.

One can also clearly see that some marketplaces cater for high-end priced NFTs while others have much lower average prices for an NFT. The picture also seems to confirm the intuitive assumption that high priced NFTs and low trading numbers go together and vice versa.

Illustration 2: NFT marketplaces by trading volume (circles), number of trades (x, logarithmic) and average prices (y, logarithmic); color coding: red = Ethereum-based, light grey = Solana-based.

Discussion

We have seen the first wave of mainly “artsy” NFTs in 2021. NFTs offer creators and art lovers new ways for self-expression and identity through art objects. They carry the promise of better economics for creators in which they have much more control of the monetization and trading than in traditional art markets. Combined, NFTs offer creators, their audiences, and developers who build for them an alternative to platform-driven monetization. This is all most welcome.

Whether the models are viable longer-term remains to be seen. Some artists definitely were lucky in creating (much) income for themselves and the fact that the digital art market is also much more open than traditional structures offers hope to the ‘long tail’ of artists who do not easily land on the radar of the Christie’s or MOMA’s of the world.

From another point of view, critics may say that creating a large number of ‘cryptopunks’ in an automated way with algorithms that create heredity with a spark of randomness is not what one expects from ‘art’ when one is brought up with masterworks that take years of skilled manual labor to create and finish, like the Sixtine Chapel or the Mona Lisa. But then, like in every other industry, digitization not only disrupts the user/consumer side but also the creator/production side of things. If users can make copies, why should producers not use copies in the production process?

A more serious issue is fraud in the form of “wash trading” – the practice of purchasing and selling assets in a manner that is intent on manipulating or misleading the market. For example, any user can create their own NFT series and sell/auction it to themselves, from the left hand to the right, so to say. A new frontier for regulation is emerging here.

Finally, while having new mechanisms for artwork monetization is a good thing, we are looking forward to seeing much more “useful” or “utility NFT” that go beyond creating more or less scarce digital objects to sell/auction off and that’s it. In a second NFT wave, we hope to see projects along the lines of proof of attendance mechanisms (like the POAP protocol) for achievements, certificates, events, etc. that are not bound to the issuer anymore, like the one for ETH validators. Or NFTs to be issued for funding of scientific projects like STEM Genesis that also eliminate intermediaries that direct and control the research. We also expect “NFT DeFi” to become a thing like using NFTs as collateral for loans, etc. And many more.<

Conclusion

In many ways, non-fungible tokens have been the latest hype in the crypto world, especially in 2021. They offer entirely new mechanisms for monetizing art and collectibles and promise a new creator economy with more balanced power relations between creators, traders, and users/collectors. We hope to see a second NFT wave to bring “useful NFTs” more into focus as we have only been scratching the surface in terms of their potential.

The author thanks Felix Nielsen for review and feedback.

Marcus Dapp

Head of Research