Thirteen Digital Asset Predictions

Dec 23, 2023 - 13 min read

Thirteen Digital Asset Predictions What’s next?

It has been two years since the crypto market peaked, and while 2023 was somewhat convenient, anyone following the space is certainly wondering: what’s next?

Will history rhyme and ship yet another four-year cycle on the back of the Bitcoin halving? Will we finally see true crypto adoption based on product-market fit? Will we see an institutional bonanza triggered by a spot ETF approval? Is there a potential black swan looming? And not to forget, when supercycle?

The contents of this article are based on our combined knowledge and are generally available knowledge derived from historical evidence which might not materialize again even under similar or identical circumstances. The predictions in this article are purely conjectures on what might or might not happen. None of the following content is intended or to be understood to include any advice or recommendation for action or non-action in financial or other matters.

PLEASE NOTE: The content presented subsequent to this disclaimer should not, under any circumstances, be interpreted as investment advice.

Men Wanted: For hazardous journey. Small wages, bitter cold, long months of complete darkness, constant danger, safe return doubtful. Honour and recognition in case of success.

Ernest Shackleton

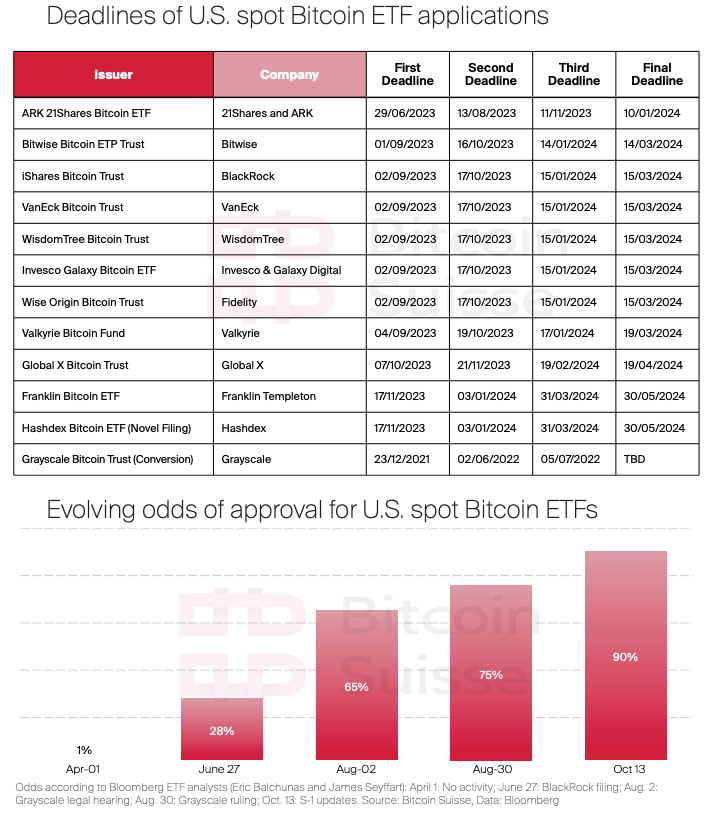

Prediction 1: Sticks out a mile: The SEC greenlights a U.S. Spot Bitcoin ETF in 2024

2023 saw a major increase of ETF spot applications and an emphasis towards BTC and ETH from financial powerhouses such as BlackRock, Fidelity or VanEck. It has been 6 years since VanEck first filed for a Bitcoin spot ETF, yet never in history were the odds higher for an approval than right now. We expect green lights in one sweep for all applications approaching January 10th, which is the final deadline for ARK. What changed in the recent months that supports our prediction?

Our predictions

- Revived momentum as renowned financial institutions, such as BlackRock with an impeccable application track record, Invesco, or Franklin Templeton applied for Bitcoin spot ETFs.

- The SEC meaningfully engaging with ETF issuers while facing sustained pressure from Congress and the federal court ruling against the SEC in resounding favor of Grayscale.

- Various proxies such as GBTC’s discount to NAV narrowing down to single digits (in line with the 90% projection of Bloomberg analysts) and the sustained bid on COIN (up 300% YTD, outperforming BTC; Coinbase filed as custodian for 9 of 12 Bitcoin ETFs) indicate high odds of approval.

- Caution however, rallies on the back of TradFi vehicles historically failed twice: with the launch of CME futures marking the top in 2018 and the launch of the Bitcoin Futures ETF marking the top in October 2021. Moreover, the SEC rejected all 33 ETF applications to date.

“We expect green lights in one sweep for all applications approaching January 10th, which is the final deadline for ARK.”

An ETF approval would be monumental for the digital asset space. Not only does Bitcoin mimic gold’s properties as a store of value and inflation hedge, but we do also identify major parallels to the transformative launch of the SPDR Gold Shares ETF (GLD) back in October 2004, the first U.S. gold ETF.

Our predictions

- GLD allowed access for many who could not easily acquire or store physical gold. It had a swift impact on the price of gold as inflows altered the physical supply and demand equilibrium. Ever since its introduction (price quadrupled to date), the supply held in ETFs heavily correlated with the underlying price.

- Like gold, Bitcoin has sound money properties, a fixed supply but is not accessible by most institutional and wealth managers in the U.S.

- Bitcoin emissions are hardcoded and its supply inelastic, even if you throw infinite hashpower at it, you will not be able to mine more, while you are certainly able to ramp up gold mining in case of spiking demand.

- The amount of ETF gold holdings equates to 1.5% of the supply. Yet gold has a 17x larger MCAP and ~36% less supply held in financial vehicles compared to bitcoin, hence every dollar flowing into a Bitcoin ETF will have a greater impact than in gold markets.

With the spot ETF, you’re going to be mainlining a Bitcoin-only exchange directly into the veins of every brokerage account holder in the U.S., including the registered investment advisors that have not been able to buy these futuresbased products.

Matthew Sigel, Head Digital Asset Research at VanEck

The U.S. ETF opened the door for gold to thrive and mature. We think that similar dynamics apply to Bitcoin and the digital asset space if the most capital-heavy market gets efficient access.

Our predictions

- An approval in January will give broad access to the youngest and most disruptive asset class since more than a century. It will bring more regulatory clarity, inclusion, legitimacy, maturity and prevent the industry from moving outside the U.S. bypassing the major miss experienced with semiconductors.

- It will provide a gateway for a new class of investors, including RIAs, pension funds and other money managers that could not access BTC at scale without an ETF wrapper.

- Compared to futures-based products that create efficient forward rates markets and yield price reducing mechanics, spot ETFs are more capital- and tax-efficient, simple, transparent, and ensure investor protection in a convenient and familiar way. Put simply, Bitcoin spot is limited, Bitcoin futures are not. They typically lead to a better performance especially for buy and hold strategies that suit portfolios with BTC exposure.

- NYDIG estimates demand for a Bitcoin spot ETF at around $30 billion, derived from the size of gold ETFs. Matthew Sigel from VanEck expects $1B+ within the first month. Galaxy estimates the inflows to hit $14.4B projecting +75% price performance in the first year, and $38.6B by the third year. At $35k per BTC, we currently face $11.5B in annual supply emissions via block rewards. $14.4B would wipe out the entire structural selling induced by mining. Matthew Hougan from Bitwise Investments expects ETFs to pull in $55B within 5 years based on demand in smaller markets such as Canada that operate spot ETFs already.

- The Canadian spot ETFs are a good primer for potential demand. They hold around $2B in BTC. The U.S. stock market, however, is 22x the size of the Canadian stock market. Plus, the U.S. may act as a role model for other countries that are hesitant to make an ETF move.

- The immediate impact upon approval might turn out to be moderate or to be a short-term sell the news event. The long-term gravity of an ETF approval however is substantial and will cause major second order effects in demand and other domains such as adoption across the industry.

Prediction 2: Bitcoin will continue to outperform any other asset class and print a new all-time high in late 2024

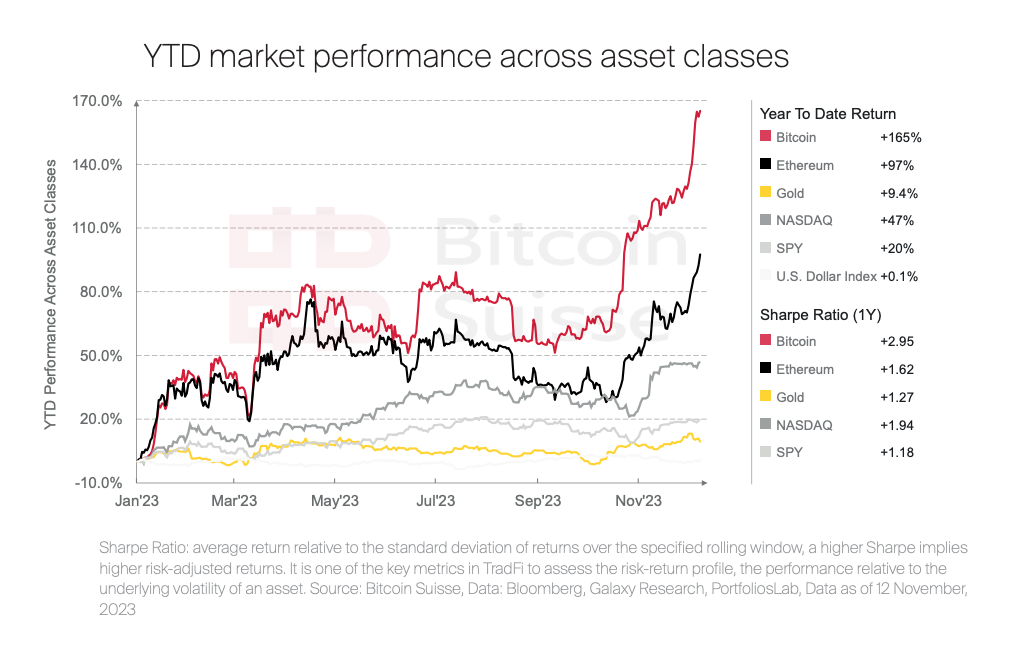

2023 was an exceptional year for digital assets and for the market leader Bitcoin in particular. Its unique properties become increasingly relevant in a period of high inflation, extreme fiscal policies and weaponization of global finance. Since its inception, the market performance reflects that the above is true and we believe that will continue into 2024 and onwards.

We have confidence in the idea that you can ignore the best performing asset class only for so long. The asymmetric returns of BTC and ETH leave the entirety of other asset classes look half-pie and market participants across the globe will certainly realize that.

Our predictions

- 2023 was a primer. Despite macroeconomic uncertainty, Bitcoin and Ethereum outperformed any other asset class by substantial margins, even on a risk adjusted basis.

- On an asset specific level, only individual stocks such as Meta or Nvidia came with a higher Sharpe ratio.

Our predictions

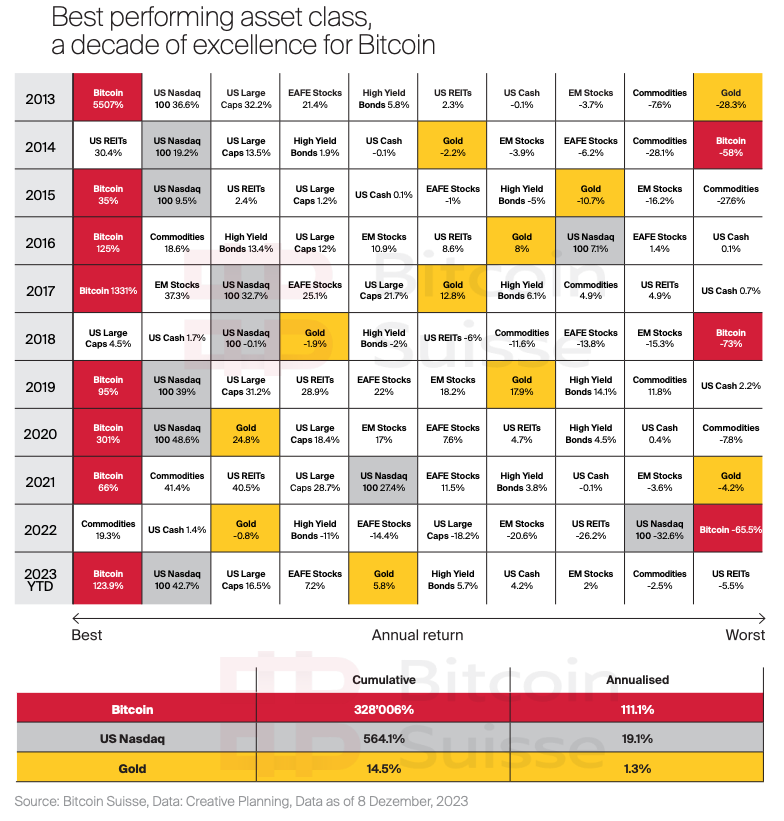

- Prior to Bitcoin, it was hard to pick the best per - forming asset class year in year out. Savvy people managed to, but most did not, which is why diversification is so crucial.

- In the last 11 years, that changed somewhat as the new kid on the block altered the game. Looking at the ten most important asset classes, there is not much shuffling when it comes to annual top performers. From 2013, Bitcoin managed to dominate any other asset class on an annual basis in 8 out of 11 years. In that period, it managed to ship an annualized return of 95.4%, it is a performance unheard of. It is the best performing asset over a 1y, 3y, 5y, and 10y period, basically any timeframe one wants to pick.

- As the market matures, we will see diminishing returns, less intense blow-off tops, but also less severe drawdowns and overall a less volatile asset class. Data shows decreasing volatility peaks over the last 3 years, an overall contracting envelope, and since recently it is converging with the CBOE volatility index for U.S. stocks.

- Based on the cycle dynamics of Bitcoin and other analyses in this Outlook, we expect Bitcoin to print a new ATH and continue to outperform other asset classes in 2024.

Our expectation is that crypto will be dominated by ETH and BTC and it will scale from more than $1 trillion today to $25 trillion in 2030.

Cathie Wood, Ark Invest

Prediction 3: The era of institutional adoption is upon us

Digital assets are the first genuinely new asset class in the last 150 years. It inherits the most transformative potential across finance, tech and social after the invention of the internet and institutions are waking up to that fact. We expect 2024 to shift up gears in institutional adoption of digital assets and here’s why.

Our predictions

- Within the last weeks, BlackRock and Barclays used JPM’s blockchain infrastructure in a milestone collateral transaction, Euroclear and World Bank issued the first tokenized Eurobond, UBS launched ETF trading in Hong Kong, Japanese Bank Nomura launched an ETH fund, BlackRock filed for an ETH spot ETF, HSBC announced custody services for institutional investors, Thailand’s Kasikorn Bank bought $103M stake in crypto exchange, Standard Chartered’s Zodia Custody expanded to Hong Kong, CBOE announced margined BTC and ETH futures for January 2024, and the list goes on.

- Besides the above, we identified other key indicators reinforcing the odds of an institutional avalanche being imminent.

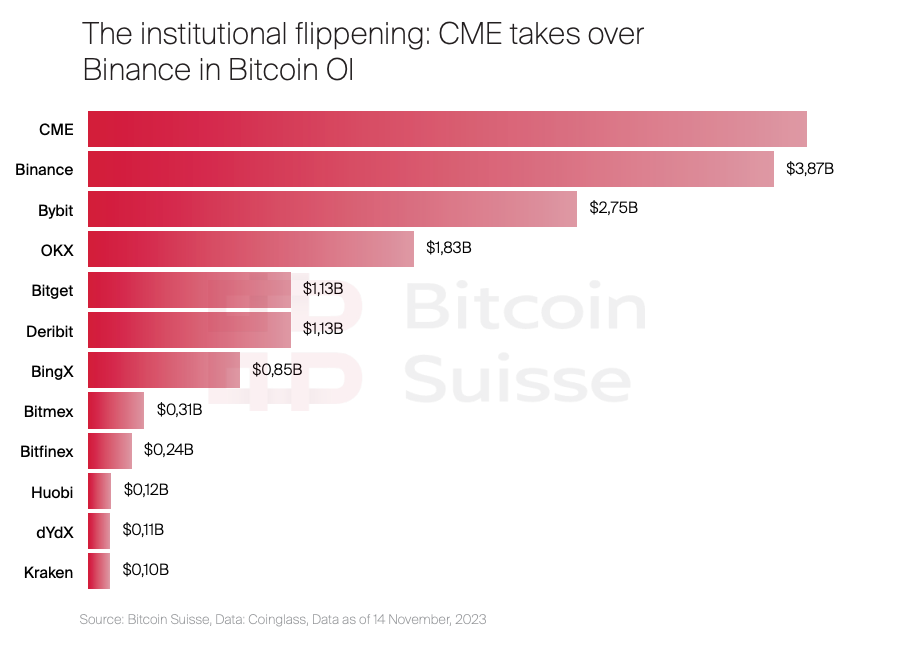

- The Bitcoin open interest on CME flipped Binance’s in a sustainable fashion for the first time in the past two years. Futures markets are the largest trading infrastructure available, and we believe it is an expressive metric to measure institutional interest. Moreover, Bitcoin open interest in options recently increased sharply and hit an alltime high of $15B on Deribit.

Our predictions

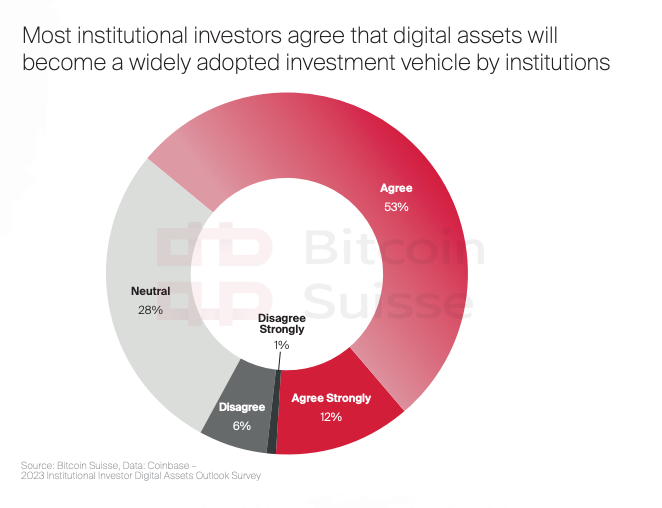

- The institutionalization of market structures is well underway. As such, we observe new ATHs in Bitcoin under management within ETPs, flashing institutional demand, increased institutional confidence and elevated sentiment. A recent survey conducted by Institutional Investor Custom Research Lab supports our view.

- They found that according to 250 surveyed institutional investors, digital assets are likely to become a widely adopted investment vehicle within 3-5 years.

- 64% that had previous exposure are doubling down on digital assets, 45% without exposure plan initial allocations, a material signal.

Our predictions

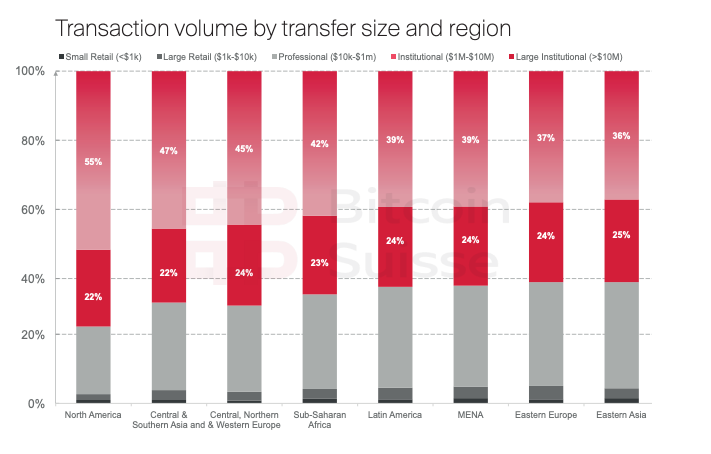

- Another key indicator in adoption metrics signals that most of the transactional volume in crypto is already happening via institutional channels. The U.S. in particular is highly driven by institutional activity, 77% of transaction volume stems from transfers above $1M, more than any other region.

- As the perception of Bitcoin transforms into an institutional asset, pensions, endowments, and other financial structures will likely bring passive and long-term buy-side flows, and it does not take large allocations of these capital heavy entities to move the needle.

- With a looming systemic threat from Binance being likely off the books, the digital asset space is ready for institutions.

Prediction 4: Digital assets enter traditional portfolios

Once perceived as a highly volatile asset, Bitcoin’s peak volatility lies in the past. With the rationale outlined in the previous predictions, we have high confidence in BTC and ETH becoming integral parts of conventional portfolios starting in 2024.

- With a spot ETF, traditional portfolios are enabled to fully tap into digital assets. A spot ETF will remove the bottleneck that constrained capital flows and substantially boost acceptance, legitimacy, and regulatory clarity for the asset class.

- According to the Digital Asset Council of Financial Professionals, 77% of financial advisors plan to recommend bitcoin to clients if an ETF becomes approved, instead of currently 12%.

- Neither JPM, Goldman Sachs, Morgan Stanley or any other major bank had BTC exposure in their model portfolios despite its unique properties and sustained performance.

- Bitcoin has emerged as a powerful source of diversification and a true unicorn in how it correlates with other asset classes. Sometimes it acts like exponential gold, sometimes like an S&P and growth stock beta, sometimes like the Dollar index. As we saw earlier, regardless of which asset class it currently correlates with, it tends to have a lead foot, outpacing its asset class peers.

We expect that digital assets with BTC at the forefront will continue to prove themselves as universal hedge with asymmetric returns. These properties will allow for the next generation of progressive portfolios that seek exposure to digital assets for good reasons.

I think if you’re trying to look at timeframe charts in BTC or ETH right now you’ve lost the plot. No indicator or deviation really matters here. Crypto is about to become a core part of every retirement portfolio. Your charts don’t matter.

Adam Cochran, General Partner at Cinneamhain Ventures

Our predictions

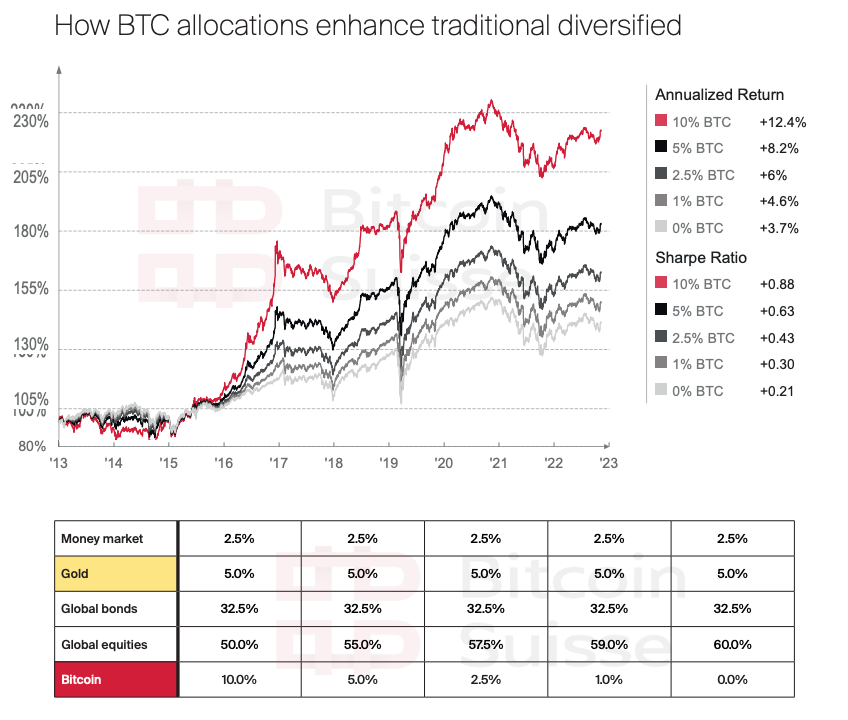

- According to our model portfolios, adding a bitcoin allocation to a traditional diversified portfolio that includes cash, gold, bonds, and equities yields significant benefits.

- Not only are we able to diversify from uncommon sources of systemic risks in balanced portfolios, but it also improves overall performance and enhances the portfolio’s overall risk adjusted returns. Notably, the largest marginal yield improvement is with BTC allocations between 1% and 2.5%, respectively, with only minor changes in volatility.

- Bitcoin’s historical impact on a traditional diversified portfolio is substantial across many timeframes yielding improved returns and improved Sharpe ratios.

- At this point, it is hard to ignore Bitcoin. With the ETF opening the gateway, we project that BTC earns a distinct role in the long-term construction of balanced portfolios

Prediction 5: BTC and ETH become reserve assets for companies and governments alike while a next sovereign will make Bitcoin legal tender

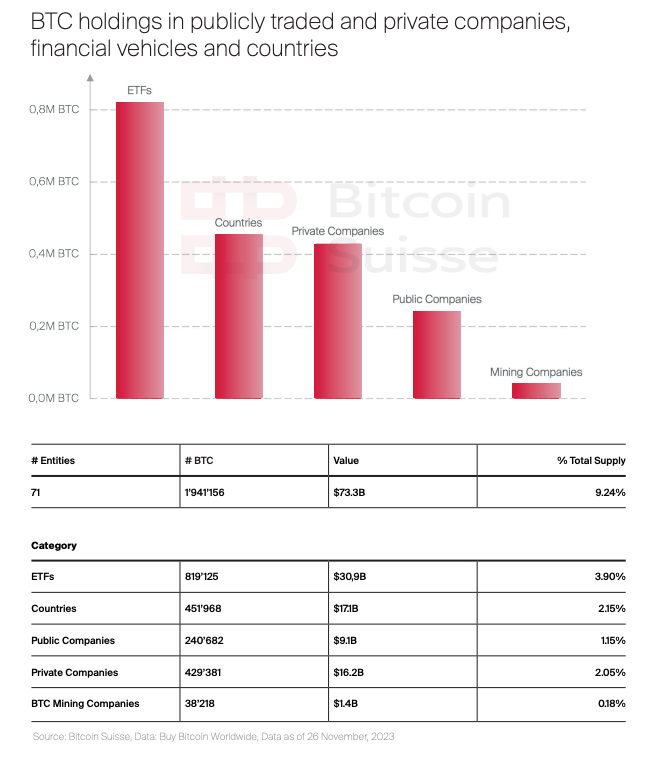

The amount of BTC in treasuries and ETFs hit almost 10% of the total supply, providing outsized returns, a hedge against monetary debasement and a neutral source of diversification to any company and any government globally. We expect to see a surge in digital asset embracing countries within 2024 inducing a fair amount of awareness, adoption, structural demand, and enhanced infrastructure.

Our predictions

- Via nation-state mining proxies, various energy-rich nations such as UAE, Oman or Bhutan signaled strategic fitness for reserve Bitcoin at the sovereign level.

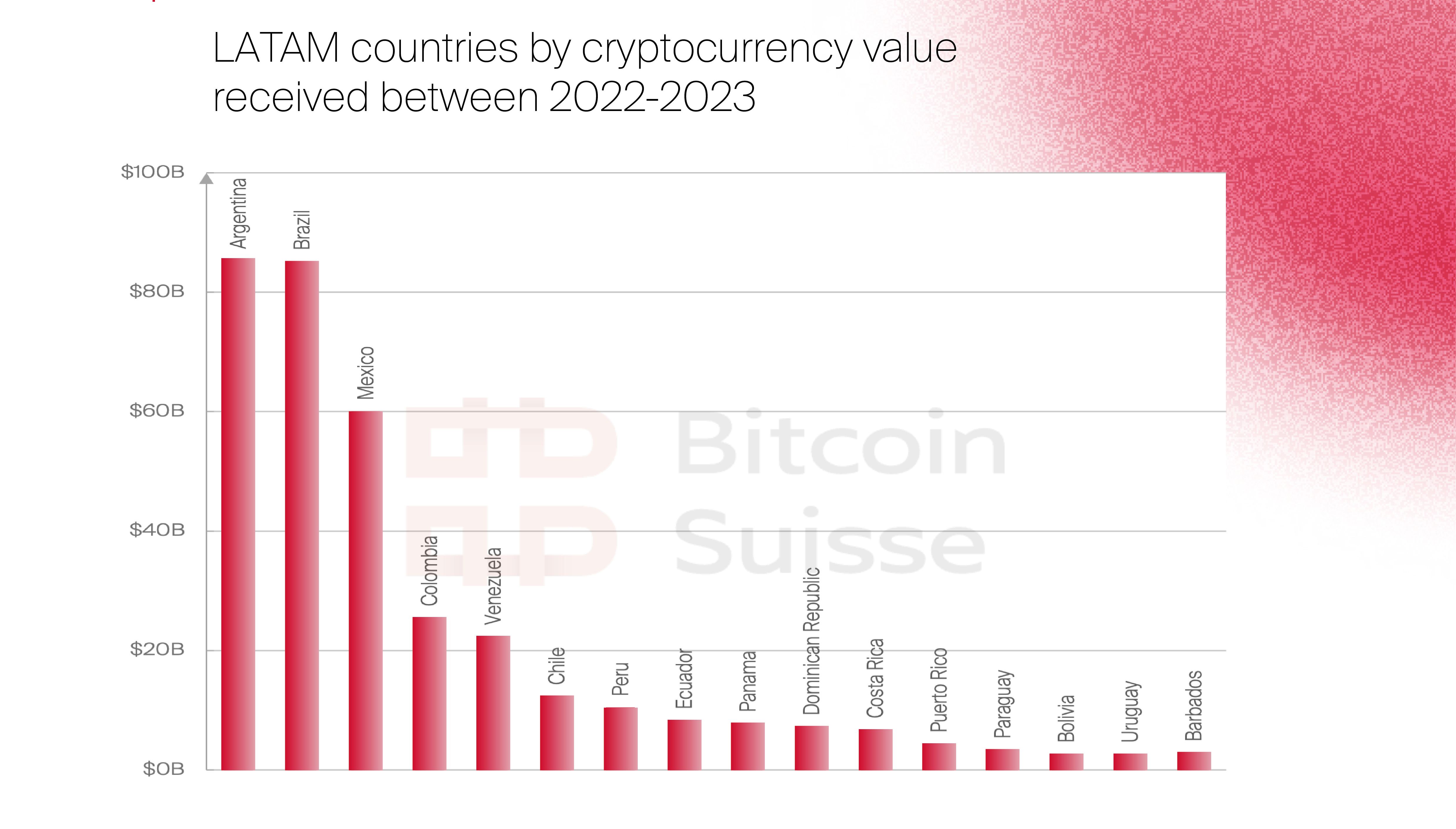

- We project the next sovereign following El Salvador’s legal tender path stems from the Middle East, LATAM, Sub-Saharan Africa or Central/Southern Asia. They host mostly emerging countries that rank high in global crypto adoption, face monetary debasement or substantially rely on trade.

- According to Chainalysis, Argentina ranks 15th in global crypto adoption, and 1st in cryptocurrency value received between 2022-2023 in LATAM. If Milei follows through, we might experience a landmark event in sovereign crypto adoption as Argentina bolsters almost 17x in GDP compared to El Salvador ($487B vs. $29B).

- Another area that we believe is warming up to digital assets is company balance sheets.

- The odds of Argentina making that move are elevated given the recent momentum of pro Bitcoin president-elect Javier Milei, persistent inflation, a rather young population compared to OECD countries and a high smartphone penetration rate.

Our predictions

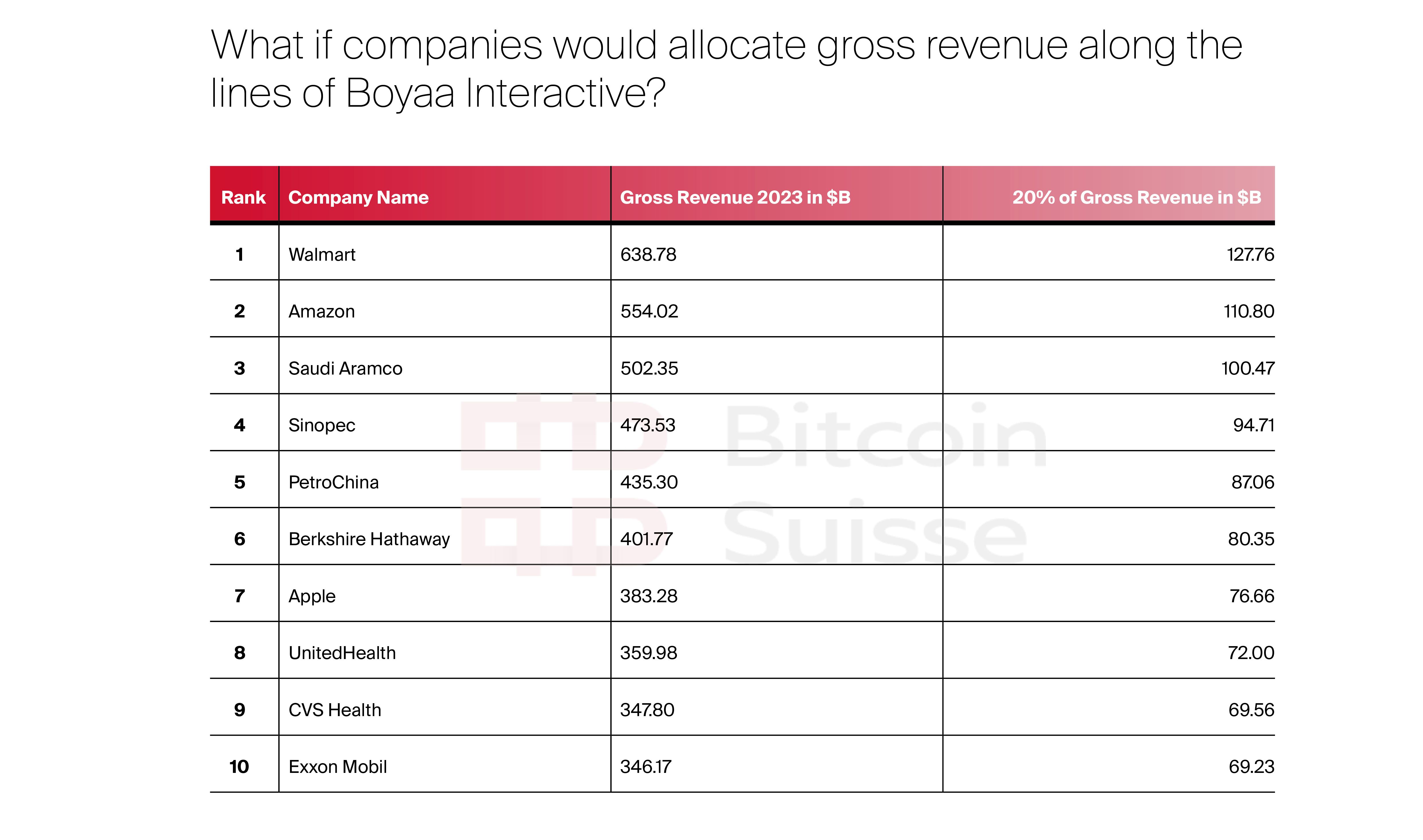

- Gaming giant Boyaa Interactive based in Hong Kong plans to invest $90M or 20% of their 2022 gross revenue into BTC and ETH.

- As digital assets enter mainstream mindshare, we expect more companies, even non-crypto affine, to take a more progressive approach towards this new asset class. ETFs will ease access as well as acceptance and these signals will not stop radiating at the leaden wall of companies.

Prediction 6: Stablecoins bottomed implying that liquidity is coming back

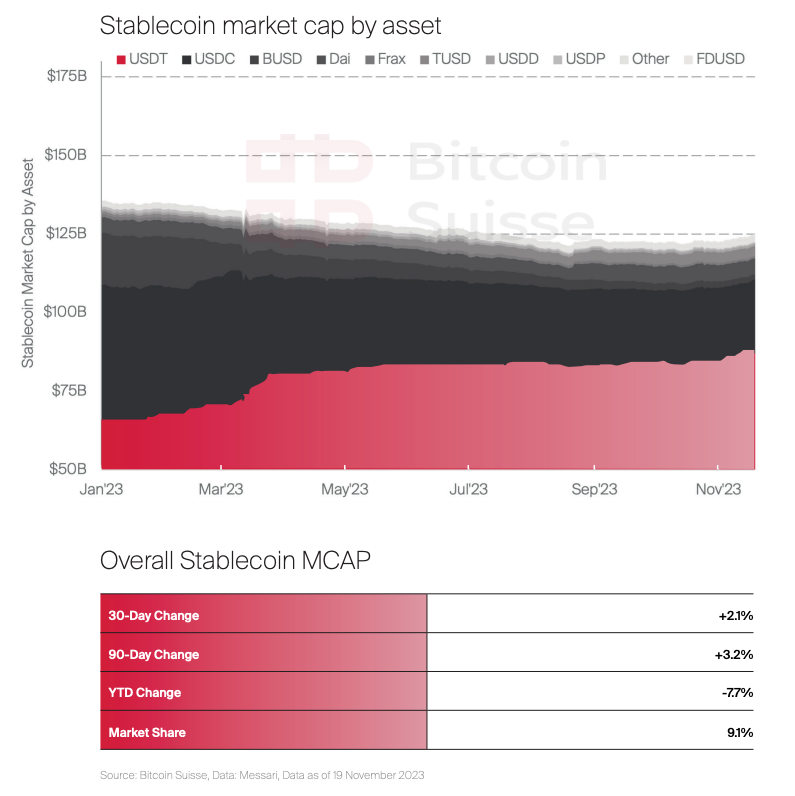

To date, crypto’s most adopted use case is tokenized dollars. By asset type, stablecoins bolster the major share of digital asset transaction volume across the globe. In the face of CBDCs, stablecoins provide a viable alternative to CBDCs and might help the U.S. to curb de-dollarization. Stablecoins are moreover a core component of DeFi, growing from a supply of $1B in 2018 to over $125B by 2023, 90% of which are deployed on Ethereum and Tron. We project that the stablecoin supply bottomed in 2023 and will from this point onwards only increase.

For the last 1.5 years, the stablecoin supply was on a steady decline not only induced by the fatal blow up of Terra but also due to a risk-off environment and attractive off-chain yields as the FED funds rate kept climbing. This started to change with the emergence of yield-bearing stablecoins, that provide capital-efficient, and scalable improvements to the earlier generation of stablecoins. Stablecoin such as DAI, Lybra or Prisma do now inherit yield bearing off-chain assets and yield bearing on-chain assets.

The yield incentivization found in LST- and RWA-backed stablecoins helped bootstrap new supply, attracting more users to migrate back on-chain. In October, the stablecoin supply ratio to Bitcoin, the ratio relative to the aggregated market cap of all stablecoins, hit a two year high despite Bitcoin’s performance throughout 2023.

Our predictions

- However, in the last 2 months we had an overall increase of stablecoins which is a great indicator for an overall healthy market and sentiment. It is a precursor akin to global liquidity and M2 money supply but within the crypto microcosm. We expect this trend to be sustained. As this dynamic acts as a liquidity proxy, we view the regained uptrend as a positive change implying market strength for the next phase of the cycle.

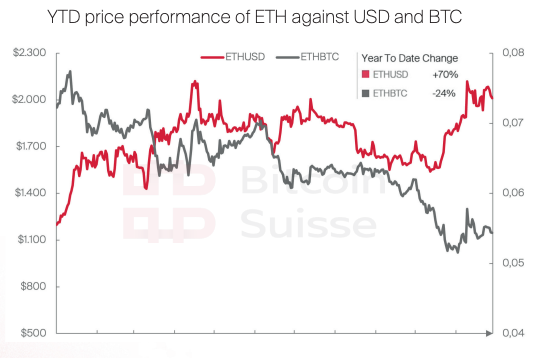

Prediction 7: The non consensus setup: ETH will be the fastest horse among institutionally available digital assets

BTC outperformed ETH for most of this bear market, in line with historical data. With the potential ETF approval in January, all eyes are on Bitcoin. In our opinion however, this arguably opens a potential non-consensus setup as outlined below.

Our predictions

- ETH was more resilient in this bear market, maintaining an ETH-BTC ratio 230% higher than previously. It bottomed first in June 2022 and did not set a lower low post-FTX collapse, while BTC did.

- BTC never outperformed ETH in the later stages of a bull market.

Our predictions

- From an investment perspective, ETH feeds a different rationale than Bitcoin as it represents a global computing platform that will likely host the new fabric of global financial markets. It derives value from cashflows, its network effects, large developer base and lindyness. It already blends into the physical world via tokenization, payments, commerce, and gaming.

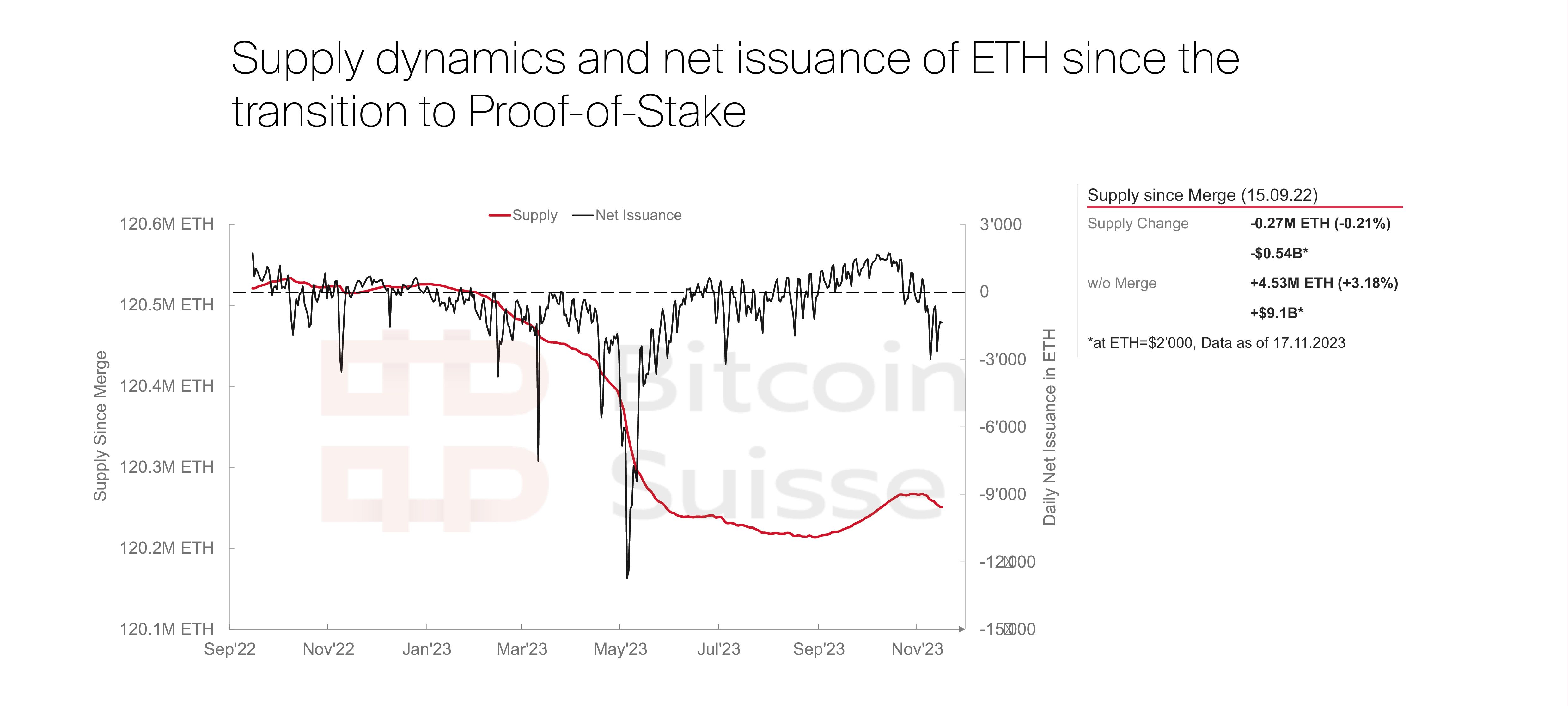

- ETH has not lost interest from a fundamental perspective. Blockspace demand is sufficient, the net issuance, accounting for new ETH emissions minus burned ETH, is deflationary and MEV burn might boost these dynamics. Bitcoin’s supply peaks in a century, Ethereum’s supply likely peaked already. We expect deflation to increase as on-chain activity heats up and real yield spikes.

- $450B and provides $60B in economic security (Bitcoin provides $10B according to Justin Drake), more than any other chain. It has best-in class client diversity, and soared past 100M addresses with balance recently. Ethereum’s L1 full time developer dominance rose above 50%. Plus, ETH is a great collateral asset, providing access to its flourishing ecosystem in a non-custodial fashion.

- It currently secures a total value of more than ETH is net deflationary, generated $2.1B in fees in 2023, $1.75B in revenue (supply burned). In its first 7 years, Ethereum surpassed $10B in overall revenue, outpacing most of blue-chip tech stocks including Microsoft and Meta. Remarkably, that revenue stems from a period of less than 3 years starting with the introduction of Ethereum’s burning mechanism.

Ethereum will act as benchmark for TradFi to cross the chasm into tokenized and digital assets, likely yielding a monetary and liquidity premium over other networks. With its unique feature set, ETH will likely become the second of two assets that meet institutional interest, making it one of the most compelling investor opportunities globally.

Our predictions

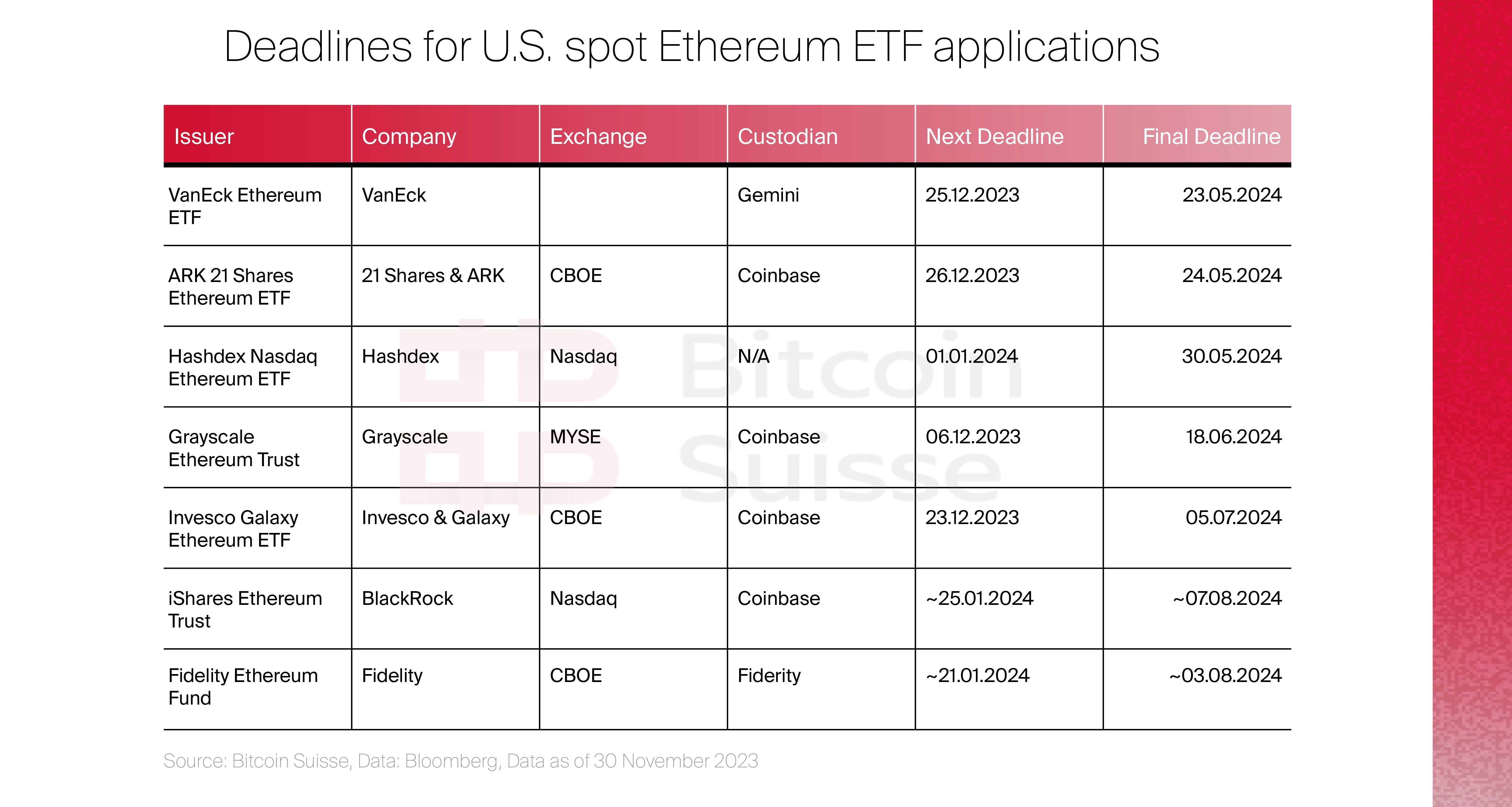

- Among others, Fidelity and BlackRock recently filed for spot Ethereum ETFs, indicating high conviction of financial powerhouses and demand from clients. We expect approvals to happen within 2024 following a BTC ETF approval. ETH would then achieve regulatory parity to BTC, a crucial puzzle piece that is still missing. Notably, while the SEC did not officially acknowledge ETH as a commodity yet, their prior actions implied accepting its commodity status.

- Once the dust of the Bitcoin ETF and the halving event settles, we project the mainstream focus to shift to Ethereum, capturing flows that previously went to BTC with the difference that Ethereum has a way lower market cap. We expect that Ethereum’s yield bearing properties will play a decisive role here, likely following the stock lending model in traditional equities yet with the crypto equivalent of dividends.

- Simply holding ETH in these ETFs won’t be enough. Institutional staking and fixed yield strategies are fields we expect to fly in 2024. ETH’s productive cashflow properties will bring additional yield enhancement through staking and hence a higher return on ETF holdings in addition to Ethereum’s vanilla growth potential. We saw first products like the 3iQ Staking ETF already launching in Canada.

- We have a high conviction that asset managers will capitalize on additional fees and thus put serious effort into a product with intrinsic yield that fits the ESG narrative. A story that is easy to sell and not priced in yet.

- We expect the entirety of the outlined properties and conditions to act in favor of ETH as an asset.

Investments can be explained with a 2×2 matrix. On one axis you can be right or wrong. And on the other axis you can be consensus or non-consensus. Now obviously if you’re wrong you don’t make money. The only way as an investor and as an entrepreneur to make outsized returns is by being right and non-consensus.

Andy Rachleff, co-founder and Executive Chairman of Wealthfront

Prediction 8: Functionality will enter Bitcoin: a first glimpse into a sustainable security model

Bitcoin’s current security model is not sustainable as it mostly runs on native issuance. However, there is a maximum supply hardcoded into Bitcoin after which miner compensation runs solely based on transaction fees. While ‘tail emissions’ are sometimes discussed as a last resort, they aren’t a satisfying option. It would harm Bitcoin’s sound money properties being a scarce, fixed supply asset. With recent developments, we expect that improved functionality will enable a sufficient and sustained security model.

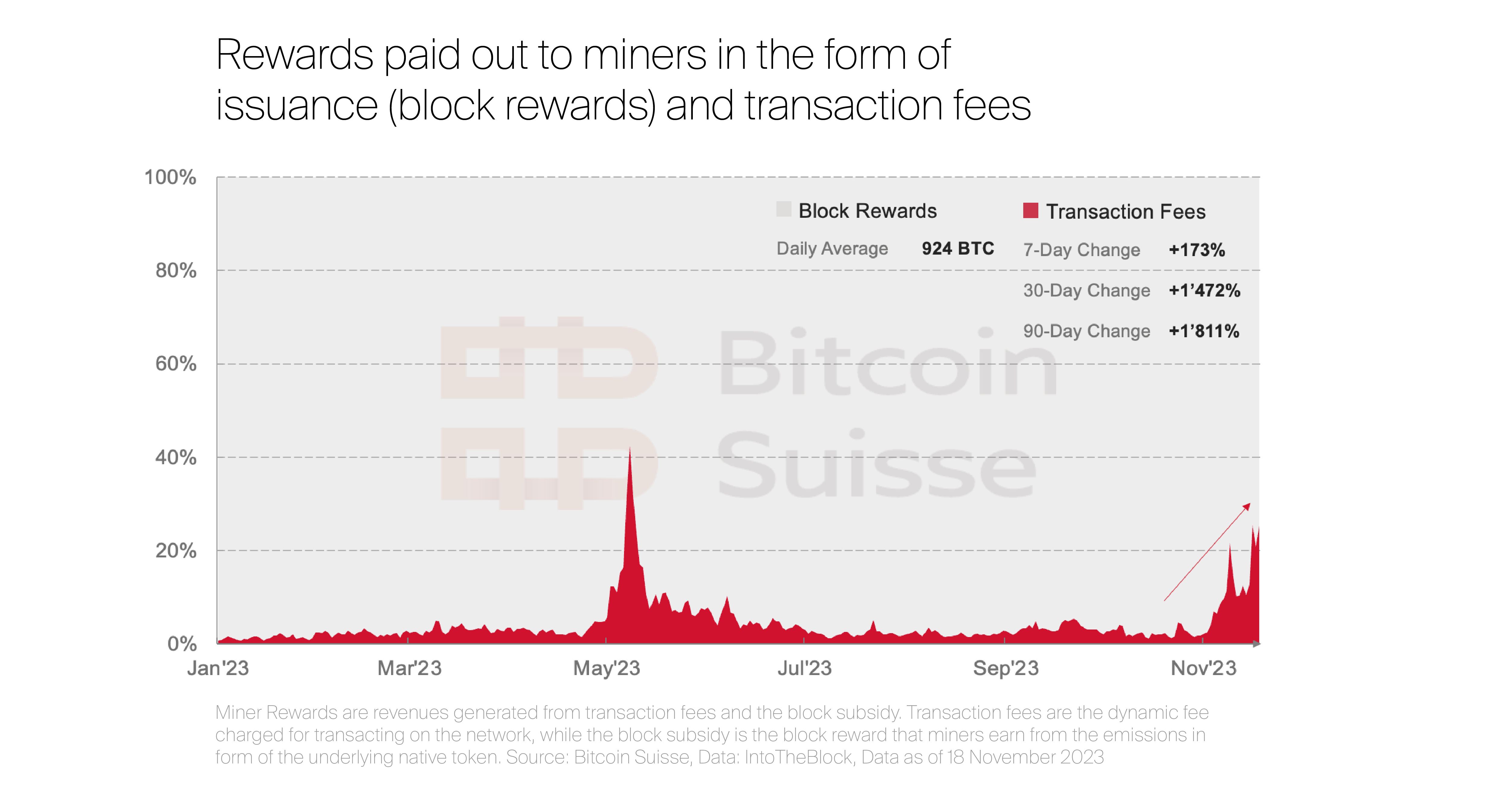

Transaction fees were supposed to substitute waning block rewards. To date however, transaction fees did not amount to a sufficient ratio, causing headaches around Bitcoin’s long-term security. With the emergence of Ordinals, new momentum entered with effects evident throughout the ecosystem. Bitcoin had its best year in blockspace demand since a decade.

Bitcoin’s 7-day average transaction fees hit $7M, closely chasing Ethereum, marking a 6-month high. It is now the third most popular network for NFTs by volume next to Ethereum and Solana. As mining profitability increased via the recent surge in activity and the price performance of bitcoin, hash rate managed to print yet another ATH. Ordinals and BRC20s continue to prove how functionality creates blockspace demand and as a result, yields transaction fees that will become an integral and essential part of miner compensation. Inscriptions have also sparked more interest in other areas such as sidechains (Stacks), zk-rollups, proof systems such as ZeroSync or new execution solutions such as BitVM.

Our predictions

- We predict that 2024 will see a major vortex of innovation hitting the Bitcoin network. Post halving, we expect that transaction fees exceeding 50% of the overall miner rewards will not be outliers anymore.

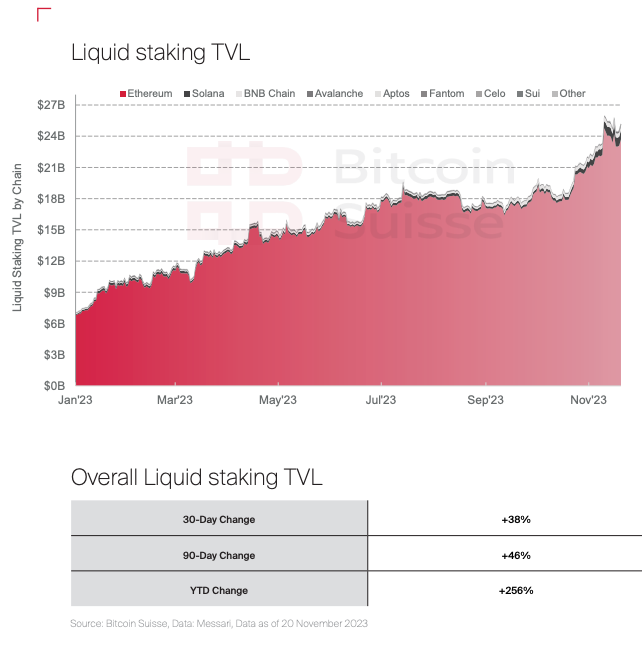

Prediction 9: Liquid staking will record the highest growth rate in DeFi sparked by institutional staking and restaking

Staking and liquid staking took off in mindshare, innovation and mostly TVL post Merge. In line with our predictions from last year, liquid staking protocols saw consistent inflows, outpacing withdrawals after Shapella was deployed on mainnet. In our view, the sector is primed for growth because a multitude of verticals line up.

Our predictions

- While staked ETH increased by more than 100% since the Merge and is now ranging above 24% of overall supply staked, we expect that ratio to substantially increase moving forward.

- Externally, the rate cycle topped, and the Fed will very likely loosen its monetary policy in the coming months, bringing the interest rates back below the on-chain “risk-free” rate: Ethereum’s staking rewards. That alone will create substantial demand as investors migrate back to on-chain opportunities.

- Internally, we expect staking rewards to increase over 5% despite an increase in validators for two reasons. On-chain activity picks up and execution layer rewards (transaction fees, MEV) will spike alongside. Restaking is next in line to bring momentum and on-chain yield back into fashion. We expect it to disrupt the entire staking landscape in 2024 and will yield significantly higher rewards for validators that decide to opt into services.

- EigenLayer will bring permissionless innovation and unconditionally interoperable systems. It will amplify Ethereum’s decentralized trust network to a plethora of applications such as decentralized sequencers (Espresso), data availability layers (EigenDA), RaaS (AltLayer), bridges (Polyhedra, Hyperlane) or risk mitigation protocols (Drosera). It will furthermore introduce another domain known as liquid restaking with the same benefits known from liquid staking.

- In our view, the approval of an Ethereum spot ETF will represent the advent of institutional liquid staking as it allows for a more flexible management of redemption cycles. Please note, institutional staking can become a concern given the mechanics of Proof of Stake.

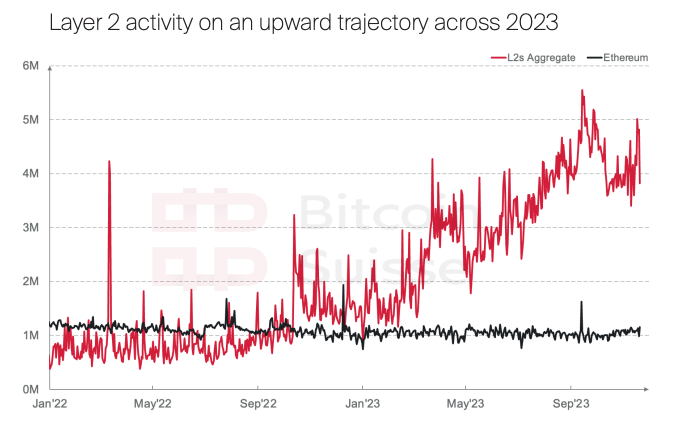

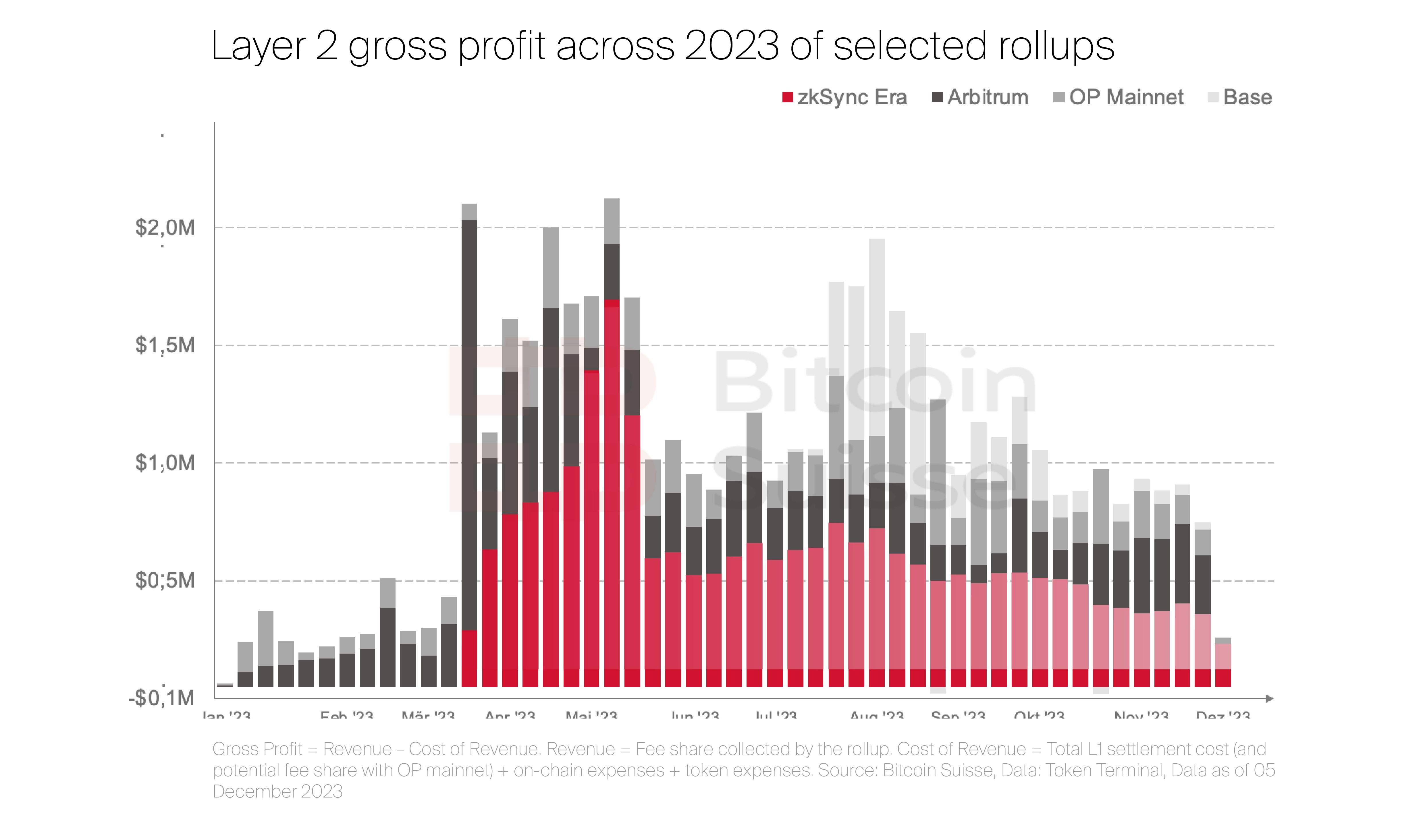

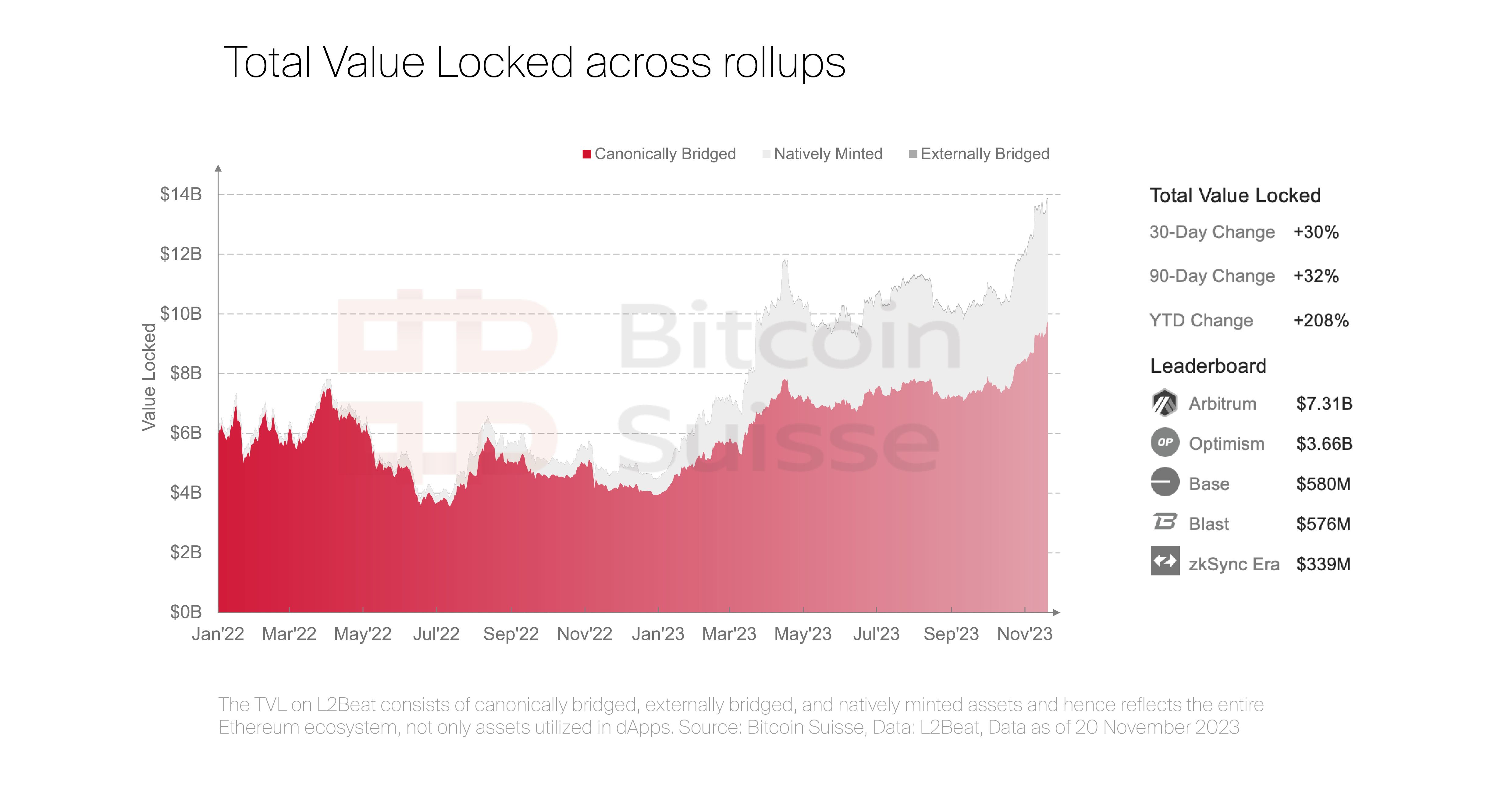

Prediction 10: Rollups will become the primary liquidity hubs supercharged by data availability solutions and EIP4844

The rollup centric roadmap of Ethereum continued to materialize throughout 2023 and surpassed Ethereum in tps in a sustainable fashion (scaling factor at 4.5x). The rollup ecosystem now hosts more than 2.3M weekly users overtaking Ethereum at ~1.5M (1.52x dominance). While risks around state validation, data availability (DA), upgradeability, and sequencers are still present, we expect the rollup space to thrive in 2024.

Our predictions

- In a bull market, high transaction costs will increasingly drive users to rollups and stimulate adoption, increasing sequencer revenues. An overseen yet material aspect. Arbitrum, for instance made $6M in fees in November, yielding a gross profit of $1.5M after accounting for sequencing and DA cost (90% of expenses). This margin can easily increase to 70% with EIP4844 (Proto-Danksharding, tenfold 10fold DA cost reduction) and even higher with Celestia/EigenDA and improved data compression (zero-byte compression, signature aggregation, and stateless compression). In our view, this will lead to a re-evaluation against L1s as soon as rollups redistribute profits via staking.

- The above incentivizes rollups to seriously consider alternative DA solutions to boost their margins and become leaner. Multiple protocols announced to integrate with EigenDA such as Celo, Mantle, or Layer N, or Celestia such as Manta or Caldera. However, it begs the question on how much value is leaking from Ethereum being on track to become a pure settlement layer. The answer is: it’s a short-term concern as full Danksharding (recapturing the DA crown), parallelized EVM, based rollups (sequencing handled by the base layer) and enshrined rollups are on the horizon. Moreover, ETH is used as money and will likely develop a more pronounced monetary premium.

- Hence, in our view, rollups will overall drive value back to Ethereum, solidifying its dominance while fresh rollups such as Base opening up DeFi to 100M Coinbase users or Blast democratizing yield on the native rollup level will ensure momentum.

Our predictions

- On the risk side, we expect further development progress and stage 2 maturities (see L2Beat). Arbitrum leads these efforts with operational fraud proof systems and a broad validator base.

- Another trade-off introduced with the Cambrian explosion in distinct rollups is composability, liquidity fragmentation and a UX burden on users that are forced to navigate across various ecosystems. We predict that sufficient solutions will be available in time. Among them are based rollups, L3 communication hubs aggregating proofs across chains (e.g. zkLink, Polyhedra, Succinct Labs), shared sequencing, IBC enabled rollups (zk-IBC, Polymer Labs). The friction involved on the user surface level will be abstracted away.

In line with our predictions from last year, liquid staking protocols saw consistent inflows, outpacing withdrawals after Shapella was deployed on mainnet.

Finally, it’s worth having a look at the com - petition brewing between monolithic giants like Solana offering composability or dense liquidity and the modular stack that allows for tailored optimizations.

Our predictions

- We observe that rollups innovate and iterate faster than their less flexible L1 hosts, resulting in a competitive advantage. On the innovation side for 2024, we are excited about new VMs (Eclipse), UTXO based DeFi (Fuel), new pro - gramming languages (Arbitrum Stylus), native account abstraction, decentralized sequencing (Espresso), Risc Zero proof systems allowing for adaptive challenge periods, hybrid zk proof systems like Metis or fast finality solutions like MACH from AltLayer.

- While the monolithic and modular approach are distinct paradigms of trust-minimized execution, we project that rollups will eventually dominate in throughput, latency and cost.

- Lastly, the demand-side network effects around developers, dApp deployments (Arbitrum 491 protocols vs. 115 on Solana), users, or liquidity maintained by players such as Arbitrum are hard to negotiate.

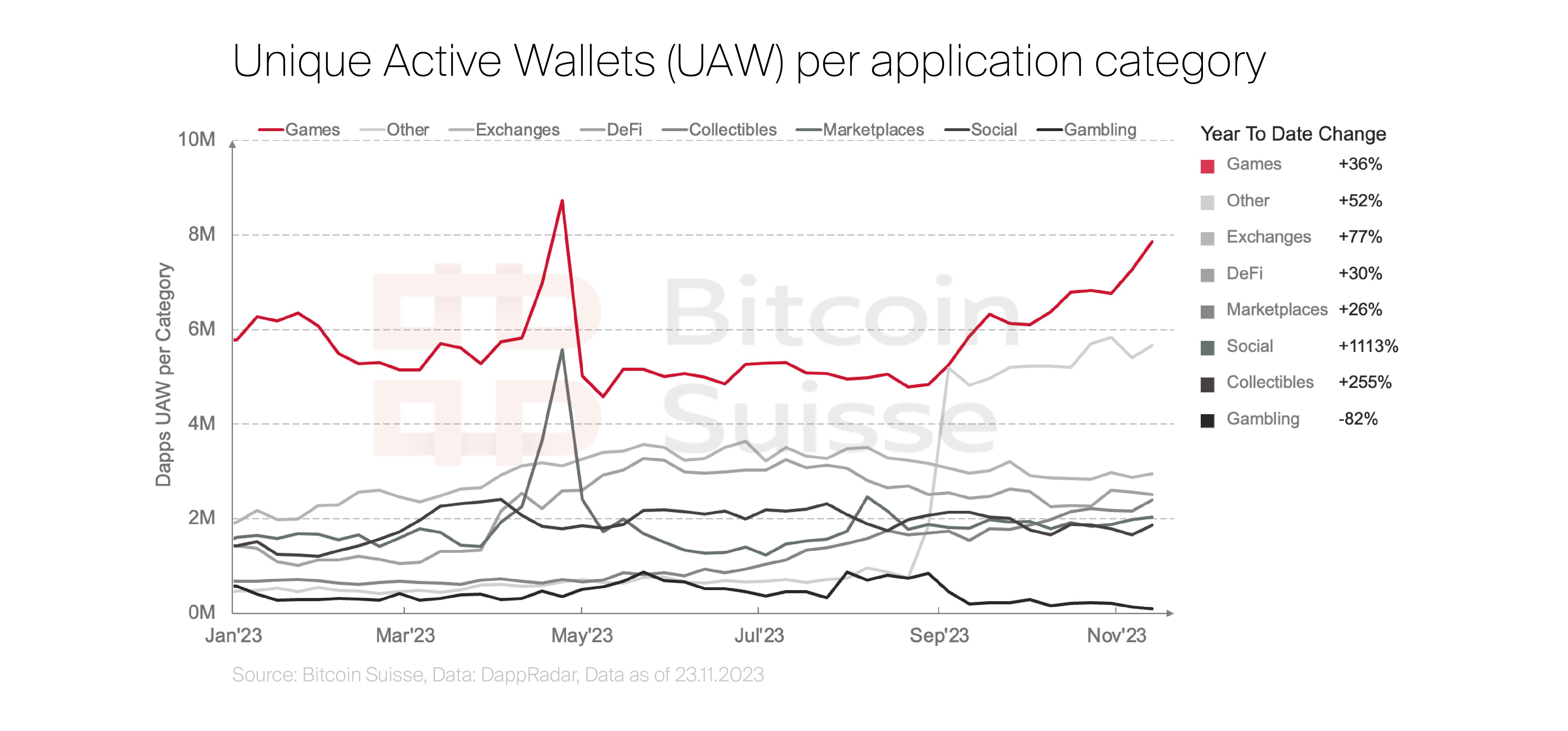

Prediction 11: Mainstream applications bring 50 million new on-chain users

The space has been building for more than 13 years now, but outside of speculation and tokenized dollars did not yet manage to ship an application that organically pulls in retail. We believe that time has come, we believe this will change in 2024.

Our predictions

- The crypto ecosystem is hosting an astonishing ~440,000 smart contracts and ~15,000 dApps on 53 chains. NEAR gave a primer on mass adoption on the application level with Sweat Economy, hitting almost 1M in Unique Active Wallets in the previous 30 days.

- We expect to see at least one breakthrough solution hitting mainstream adoption across the following domains: Social, Gaming and Gambling. In contrast to web2, value accrues to users, builders, creators, and communities that contribute to the game, platform or application running on blockchain rails.

- Scalability and usability, the necessary preconditions for an application frontier need to be met. With consistent innovation, the crypto industry managed to bring a plethora of scaling solutions across L1s, L2s, L3s (Hyperchains, Madara, Orbit), VMs, RaaS’, data availability solutions, and compression. We furthermore observed usability improvements across the stack with AA, WaaS, or PWAs (Progressive Web Apps) enabling web2-esque UX.

Our predictions

- 3.1B people or 39% of the global population play games. The total gaming space is estimated to hit $610B by 2032, while crypto gaming is valued at ~$15B today. More than $100B of which is estimated to be captured within GameFi at a CAGR of more than 27%. We have high conviction that there is no bigger trojan horse for crypto adoption, it is a superset of all other crypto narratives. Messari confirms, that the game segment is also becoming the leading sector by investor attention.

- We observe major enthusiasm from gaming companies like Ubisoft or EpicGames, that could boost the industry’s expansion from the traditional shore. The hyped launch of GTA VI with along with rumors of a potential crypto integration will put the gaming narrative into focus.

- Games with underlying blockchain technology enable true ownership of in-game items. There are massive markets trading such items from e.g. World of Warcraft or Counterstrike that would benefit in efficiency, cost, price discovery, ownership, liquidity or provenance. In a first ever. they would allow for cross-platform utility, a future that even Roblox CEO David Baszucki is an advocate of. Others like game publisher Square Enix (Final Fantasy) announced the launch of its first NFT game, Symbiogenesis. If these players move, we believe that most AAA publishers will follow suit.

- We expect gaming to finally meet longstanding expectations, likely attracting the major share of new on-chain citizens.

The timing could not be better as it coincides with a vortex of gaming funding within 2021 and 2022. 2024 will be the 2-3 mark, a typical timeframe needed for game development. Games leaving stealth mode that we are excited about are Shrapnel, Hytopia, Matr1x Fire, Parallel TCG, Altered State Machine, Sidus Heroes, Illuvium, Sipher, Oh Baby Kart, Off the Grid, Portal, Domi Online, or Nounish Punk and Treeverse. On the platform, network and ecosystem side, one should watch out for Immutable X, Treasure DAO, Beam and Nakamoto Games. We expect at least one of these projects to go viral.

- Fortnite: 243M MAU | $5.8B Revenue

- Roblox 214M MAU | $2.4B Revenue

- Minecraft 163M MAU | $380M Revenue

Decentralized gambling and betting are another area to watch. After the ICO era, and the first two waves of DeFi protocols, the industry desperately seeks real yield and sustainable cash flows. Protocols such as Rollbit (P/S =0.69 annualized based on November revenue of $56M,) and WinR (P/S=1.3 annualized based on November revenue of $0.13M) a fully decentralized platform with no operators nor owners running on immutable smart contracts, provide just that. They essentially allow you to become the house. In our view, the next expansion cycle of these platforms is close. Mostly because fully homomorphic encryption (allows computation on encrypted data) and zk technology now enables games like on-chain Poker with code-level fairness in a truly decentralized fashion.

Prediction 12: Strong early stage, strong late stage

Historically, projects that provided outsized returns in late bear market and early bull market stages kept momentum throughout full-fledged bull markets. We curated projects that match this paradigm and provide insights on underlying fundamentals.

Our prediction

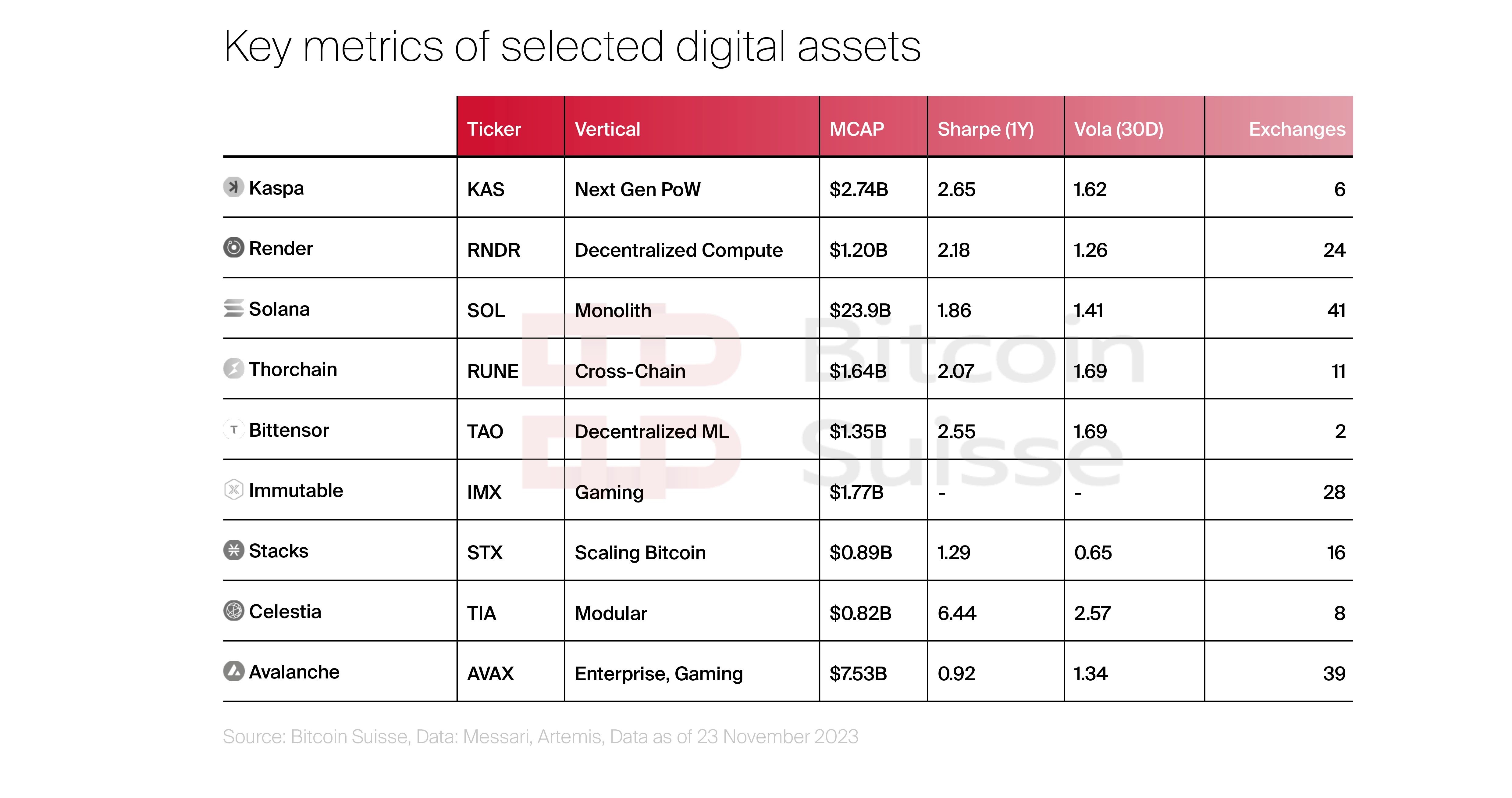

- Avalanche, almost losing the race against Ethereum’s network effects, came back with a bang. They have been cooking on the institutional shore (Request for Streaming PoC with Citi and JPM, Republic Note via INX), on the gaming shore (e.g. Shrapnel, Beam) and on the tech stack side with IBC integration (Landslide) and Subnet-Only Validators. Avalanche’s overall total addressable market extended substantially, and usage metrics indicate already what we expect to be a sustained trend.

- Solana, the monolithic powerhouse, heavily oversold after FTX went belly up, finally managed to liberate itself from the stain. While the ecosystem experiences a revival in users (occasionally flipped BTC in active addresses) and TVL, there is crushingly good tech under the hood and in the pipeline (compressed NFTs, localized fee markets, firedancer, async execution, dynamic base fees and storage pricing, multiple concurrent leaders). A convincing setup for bets outside Ethereum based on fast and cheap transactions without fragmentation issues.

Our predictions

- Opposite of Solana sits Celestia, the first production ready alternative DA solution fostering the modular paradigm. It allows rollups to thrive on cheap, scalable data availability based on innovations such as data availability sampling. The market agrees on its relevance while other projects such as NEAR join the race with their DA layer. On our DA watchlist: Celestia, NEAR, EigenDA and Avail.

Our predictions

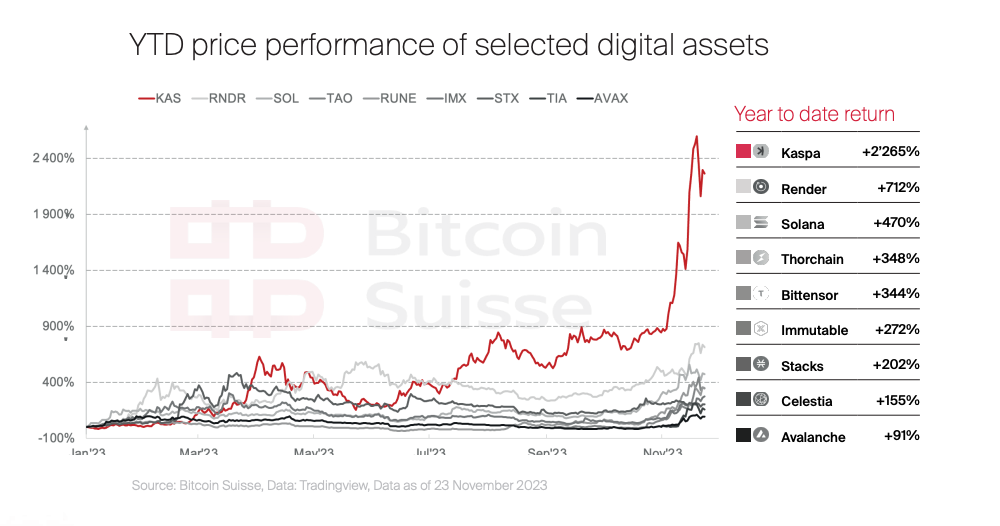

- Kaspa popped with an efficient PoW and GhostDAG consensus mechanism trying to follow the steps of Bitcoin. Meanwhile, Stacks, a Bitcoin L2, made noise as the only protocol to offer native Bitcoin yield. Its milestone Nakamoto upgrade expected in early 2024 brings sBTC and major optimizations across the stack. Both projects are worth monitoring, providing a potential beta play on BTC.

- Lastly, fundamentally attractive projects that lean into the AI narrative will likely not lose steam in the months ahead as computing and storage becomes a bottleneck and debates around decentralizing AI ramp up. This affects most components in the decentralized machine learning supply chain from storage to data pre-processing and model training. Projects worth mentioning are Render, Bittensor, Filecoin or Akash.

Prediction 13: Final assembly line: too much demand, too little supply

Digital assets are the most vibrant, most disruptive, most dynamic, most performant, and most transformative asset class available to mankind. We enter an era where digital asset exposure becomes the norm, where a lack of exposure equates to risk. In this prediction, we look at the law of supply and demand and outline why we believe that the price equilibrium of BTC should arguably be substantially higher some months down the line. Comparing the upcoming demand and supply domains with a cocktail, we are dealing with a well-meant long island iced tea and here’s the recipe:

DEMAND

Our predictions

- Macro: rate cycle peaked, possible QE measures upon yield curve un-inversion, global liquidity is coming back (M2 bottomed), expansionary fiscal policies, federal debt service at ATHs, election year with multiple pro crypto candidates, an overall risk-on setup is looming.

- Institutional: a potential ETF does not just mean significant inflows upon approval, but it elevates digital assets in acceptance, legitimacy, and regulatory clarity. This aligns with the plain benefits of having digital assets in diversified portfolios. Adoption: gaming, betting, social applications, tokenized dollars in countries tortured by inflation, DeFi and RWAs attract millions of new users.

- Risk mitigator: digital assets as a solution to looming threats from CBDCs (3.7 billion people are living under authoritarian regimes experimenting with CBDCs), deep fakes, privacy (FHE, zk), decentralized and democratized AI, data ownership.

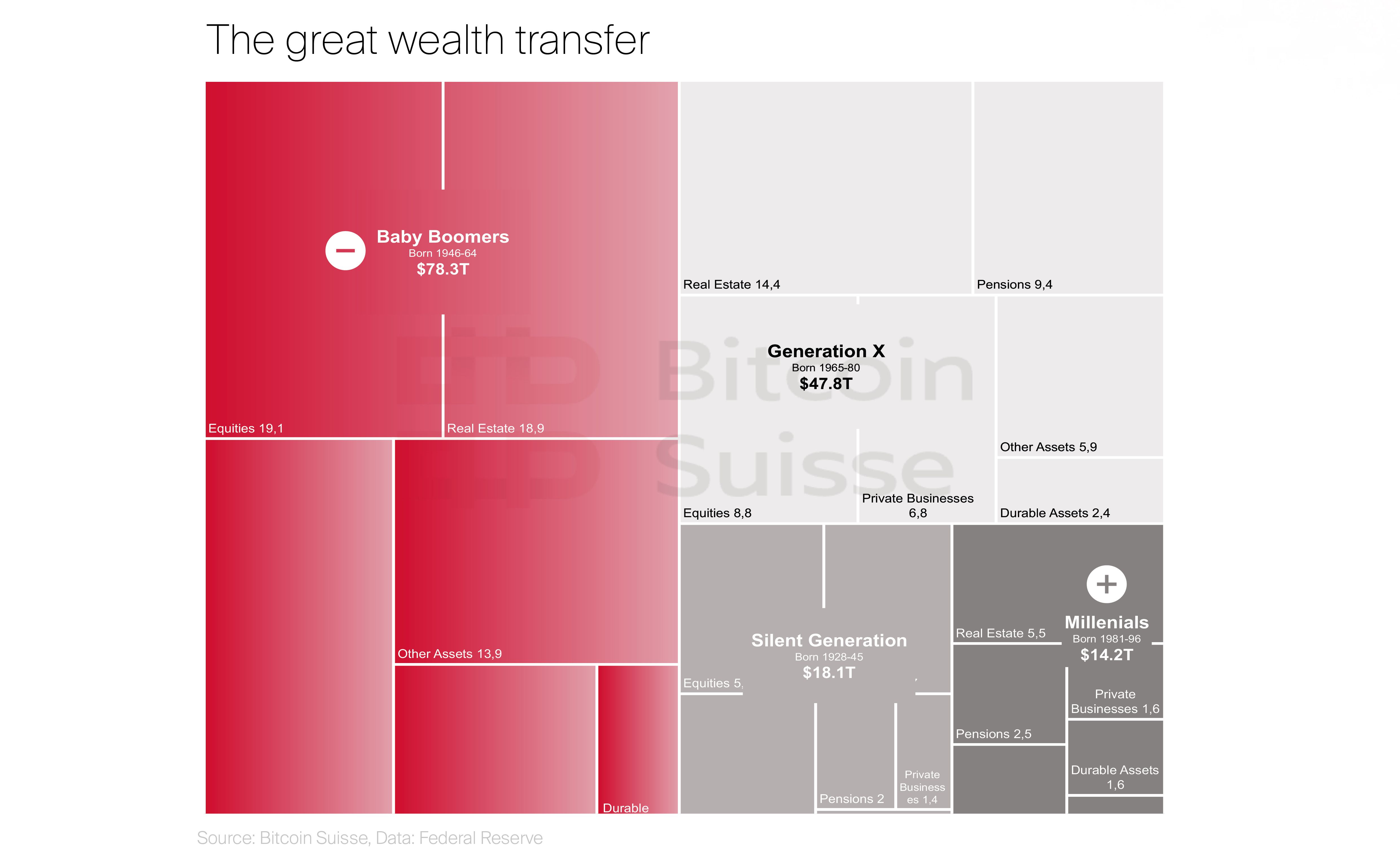

- Demographics: the great intergenerational wealth transfer is the most overseen component. The wealthiest generation, baby boomers, will retire through 2045, transferring more than $70t in assets to younger generations, mostly millennials, a wealth transfer eclipsing any in the past. By 2030, millennials will hold 5 times more wealth than today. So what? The digital asset adoption rate of millennials is factors higher than that of baby boomers, on average 5x. One in five Americans hold digital assets, 60% of which are millennials and gen Z. It is reasonable to assume that a fair share of that wealth is flowing into digital assets. Galaxy estimated a resulting capital flow of $20M-$28M daily over the next 20 years.

SUPPLY

Our predictions

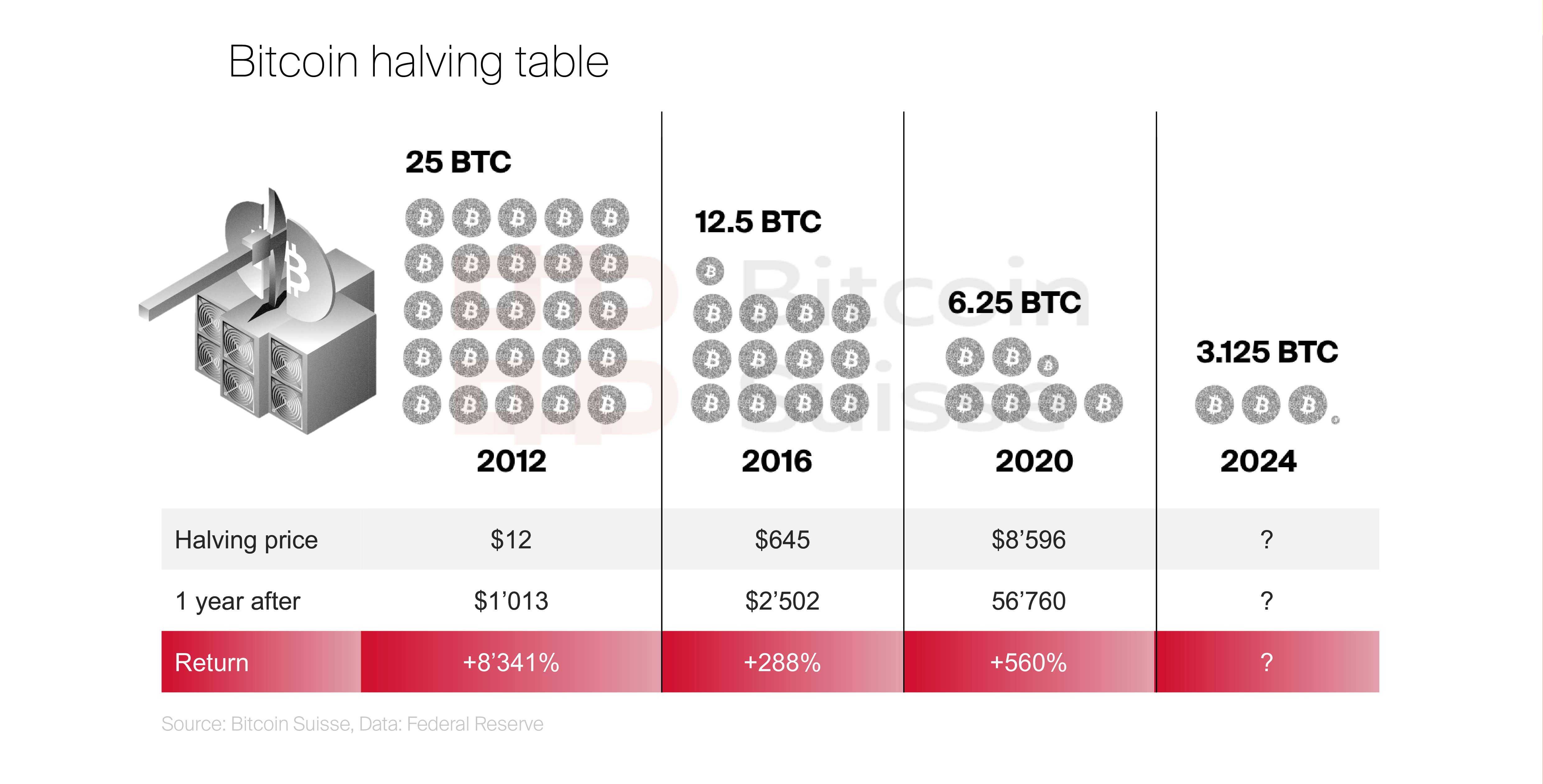

- Halving: the 4th Bitcoin halving is estimated for April 2024. Post-halving, there is $5.75B less structural supply hitting the market (calculated based on BTC at $35k). Historically, Bitcoin yielded strong gains in the year that followed the halving and early trends of this 4 years cycle echo past patterns.

- Long term holders: the supply dynamics indicate that long-term holder supply is on a sustained upward trajectory (BTC ATH at 70% not moved in >1Y, ETH ATH at 76% not moved in >1Y). The short-term holder supply flashes exhaustion and mid-term holder supply is ranging at multi-year lows. We derive strong signs of holder conviction, leaving ample room for growth as increasing supply age is a proxy for illiquidity. Historically, cycle tops are skewed towards short- and mid-term holder supply. There are no signs however of a trend inversion and long-term holder supply distribution. Note that supply held in TradFi vehicles such as spot ETFs is increasing too.

- Exchange reserves: showing a sustained multi-year decline, recently hitting an ATL of 2M BTC. It suggests that BTC is migrating towards more illiquid and less speculative venues that puts the available supply at historical lows, another strong signal of elevated long-term positioning and accumulation. Note that supply leaving exchanges is also subject to institutional and TradFi vehicles like custody.

Combining the above, there is a major supply crisis assembling. For a fair number of holders, Bitcoin is a one-way street, a buy and never sell asset held by a community of believers with high conviction. The potential solution to debt money in a world that seeks safe haven alternatives. Meanwhile, regulatory derisking and major streams of adoption will materialize, bringing multiple demand verticals that stumble into the halving event. Never in digital asset history did we have such a textbook setup for price discovery.

Please note that there is a chance of macroeconomic turmoil in 2024 and there is a chance of the SEC rejecting ETFs. Such events may however be considered as an opportunity. The overall odds are heavily in favor of digital assets. And while this entire article focuses on dynamics that may influence performance, it is key to understand context. Vehicles such as ETFs are solely tools. The core primitives of digital assets provide the substance, offering a disruptive emerging monetary technology in a permissionless, inclusive and immutable fashion. Price is only a lagging indicator of fundamentals.

To sum up, we project that liquidity will chase strong narratives. And since digital assets are a very rhythmic and reflexive asset class, we might face the culmination of catalysts engineered for more than a decade. This could result in an endless twap into digital assets with ever reinforcing feedback loops while institutional demand runs into supply constraints. Digital assets are ready for prime time. In our view, the supercycle is closer than ever.

Has anyone ever seen an asset that gets smoked -80%+ multiple times but comes back stronger each time over multiple cycles across 15 years?

Alex Thorn, Head of Research at Galaxy

The author thanks Marcos Benvenuto for the valuable support creating model portfolios.

Dominic Weibel

Head of Research, Bitcoin Suisse