Cryptocurrencies for Corporate Treasury

Apr 20, 2021

By Tom Lyons and Dr. Raffael Huber

Introduction

We just had the awful realization that we were sitting on top of a $500 million ice cube that’s melting.

CEO MicroStrategy

Corporate treasury policies do not usually generate headlines. But when MicroStrategy – a large, publicly traded company – announced last August that it had purchased USD 250 million of bitcoin and planned to use the cryptocurrency as its primary treasury asset, it made waves around the world(2).

And the waves kept rolling as the company continued to announce sizable purchases at regular intervals. As of February, MicroStrategy held over 90,000 bitcoin, worth some USD 4.5 billion(3). According to Michael Saylor, MicroStrategy’s CEO, the decision to bet heavily on bitcoin was based largely on the company’s distrust of the current global monetary regime, and its belief that bitcoin “is a dependable store of value and an attractive investment asset with more long-term appreciation potential than holding cash.”(4)

Saylor is not the only corporate leader or institutional investor taking bitcoin seriously. After signalling its interest in the cryptocurrency last fall, Tesla announced in February that it had purchased USD 1.5 billion worth of bitcoin for treasury purposes and would consider accepting bitcoin as payment for its cars(5). That same month Jack Dorsey’s Square announced it had moved some five percent of its total cash and equivalent assets, worth over USD 220 million, into bitcoin(6). World-renowned investors like Paul Tudor Jones(7) and Stanley Druckenmiller(8) have expressed their belief in, and revealed their bets on, bitcoin. Even JP Morgan, whose CEO Jamie Dimon had long been notorious for his negative views on bitcoin, began advising clients to diversify into the crypto asset(9).

These headlines show no sign of abating. As this publication went to press, Coinbase, one of the largest cryptocurrency exchanges, launched a successful IPO on Nasdaq that valued the company at some USD 85 billion(10), while AXA, a Swiss insurance company, announced that its customers could pay their bills in bitcoin(11). All the while, the price of bitcoin has been skyrocketing, rising almost sixfold between August, 2020 and today.

For many, this marks a seminal moment: the long-awaited (in some circles feared) “mainstreaming” of cryptocurrencies via adoption by institutional investors. And for an increasing number of serious people, cryptocurrencies look like a new safe haven asset for the digital age. But are they really a viable option for corporations and other organisations? This question is the subject of this paper. We expressly do not offer an answer, nor make any recommendations(12). Assuming that cryptocurrencies are here to stay – an increasingly safe assumption based on the events of this year – we do however think it is time for CEOs, CFOs or anyone else tasked with ensuring the financial health of a corporation or other type of organisation to look more closely at what this means for them. With this paper we hope to help them get started on the journey.

To the moon – the case for bitcoin as a treasury asset

While the notion of corporate treasurers exploring an asset as volatile and immature as BTC could easily be dismissed, the severe dislocation in the global monetary system does make conventional treasury decision-making much more fraught than in previous years.

Smith & Crown (13)

There are many arguments in favor of a move into bitcoin or other cryptocurrencies as a treasury asset. Almost all of them boil down to some form of disillusionment with the current monetary system, fear of the consequences of current policies on cash and other previously reliable treasury assets, and a belief that cryptocurrencies offer a viable alternative(14).

On the monetary system front, a decade of extremely loose monetary and fiscal policies in the US, Europe and elsewhere since the great financial crisis of 2008, and reaching astronomical proportions during the current pandemic, has flooded the world with newly minted money. This has stoked fears of a massive rise in inflation in the near future. At the same time, governments have driven interest rates to record lows, driving yields on traditionally safe assets like cash and treasuries down to meaningless levels and so making them increasingly unfit as stores of wealth.

Changing global power dynamics, the multilateral nature of the post-cold war world, and the rise of highly disruptive new technologies are also causing major geopolitical and economic dislocations. As a result, belief in many of the foundations of the current system has been shaken. To take one example: the status of the US dollar as the global reserve currency is increasingly being challenged by rivals like the Chinese yuan and private digital currencies like Facebook’s Libra (now Diem). In the face of such shocks, it is no wonder that people are casting around for something new to hold on to.

As an independent, uncensorable, non-counterfeitable bearer asset, bitcoin fits the bill for many. Because bitcoin’s supply and monetary policy are fixed in the protocol – there can and will never be more than 21 million bitcoin minted, and we know more or less when and at what rate new coins will enter circulation – it is immune to inflation and the whims of policy makers.

And while bitcoin does not pay interest, if you believe its value will continue to rise or even just hold steady, then it will also provide a real rate of return that can easily outpace what is available today or in the foreseeable future in money markets or other traditionally safe yield-bearing assets.

With competition for the US dollar as a global reserve currency rising, we are likely to see increased volatility in forex markets as well. As a principal treasury asset, bitcoin could be used as a stable bridge currency to make managing multi-currency portfolios easier and more predictable. Bitcoin on the balance sheet could be used as collateral for companies seeking loans, a boon in difficult times when other types of collateral may lose their attractiveness.

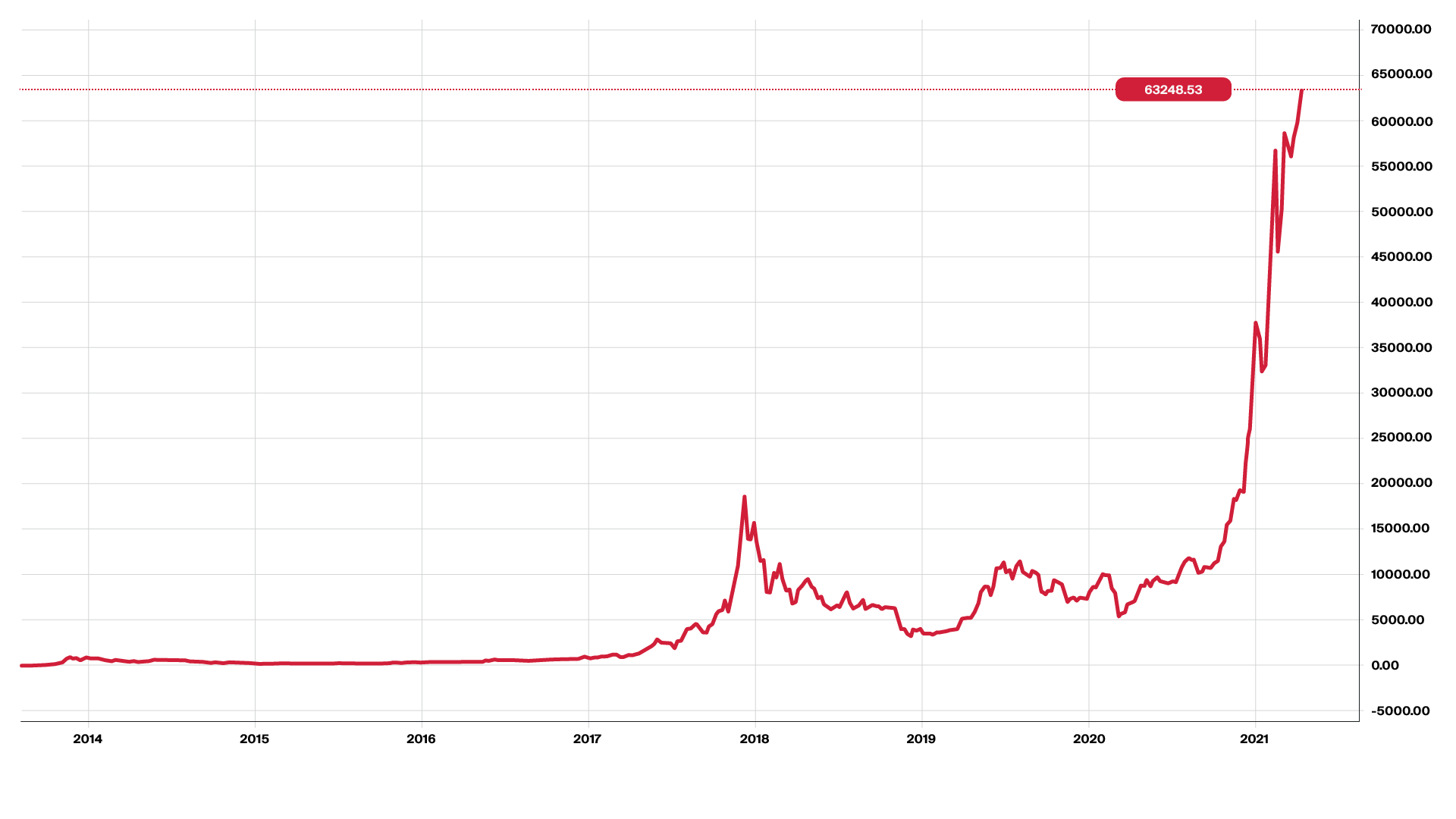

Perhaps more important than these corporate-treasury specific arguments is the overall investment case for bitcoin. Its historical price performance is certainly mind boggling. In the two years from March 1, 2019 to March 1, 2021, bitcoin has returned over 1,000% for an annualised ROI of 232%. In its latest run since last October the price has risen from USD 10,000 to over USD 60,000 per bitcoin.

While such asymmetrical returns have been one of the main drivers of interest, now that bitcoin seems to be mainstreaming, we cannot expect such performance to continue. When thinking about bitcoin’s potential today, and to help put its performance into perspective, one fruitful approach is to compare it to assets other than the dollar.

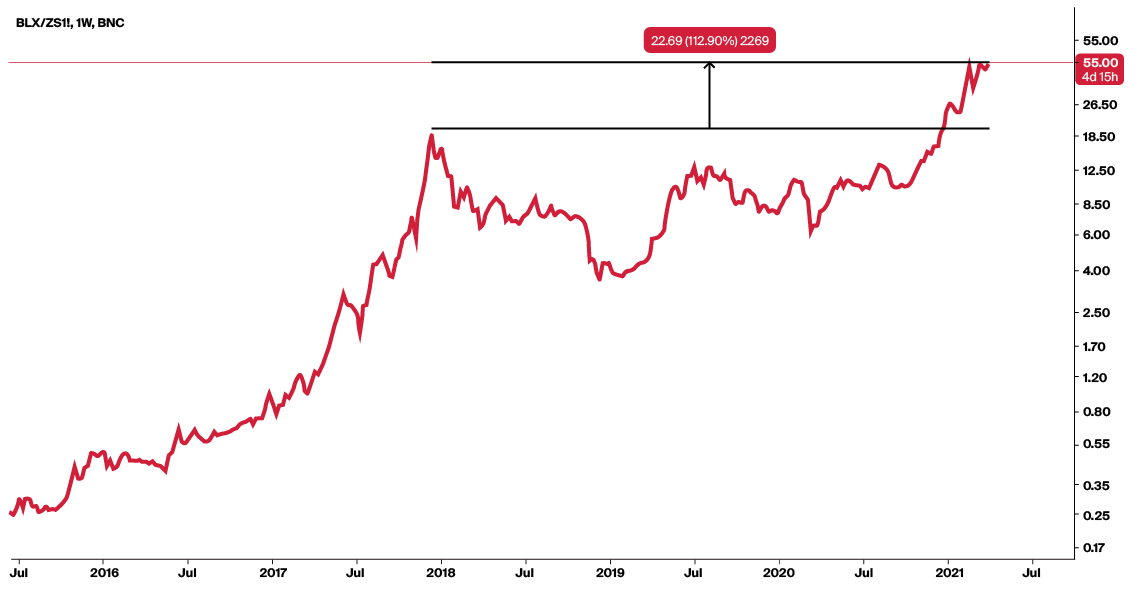

Consider for instance returns on a highly successful startup. A very early investor in Facebook who held on to his or her shares would have enjoyed bitcoin-like returns as well, far more than can be expected by post-IPO investors. Taking a date in bitcoin’s more recent past as a loose proxy for an IPO, for example by starting at its previous all-time high at the end of 2017, reveals still spectacular, but far more plausible, returns. Similarly, we have been witnessing a boom in the price of many commodities lately (see chart “The price of bitcoin vs soybeans”). Here too bitcoin’s performance, while still astounding, seems more plausible – and more indicative of bitcoin’s potential future purchasing power.

Digital gold rush

Another popular argument in favor of bitcoin as a treasury asset is its role as a store of value – the gold of the digital age.

As a non-counterfeitable, digital bearer asset not under the control of a sovereign or any organisation, bitcoin certainly has gold-like qualities. Like gold, it can be held in privacy: possession of the private key to bitcoin is the digital equivalent of possessing the key to a vault. Like gold, it offers a predictable and limited supply, one which is not affected by the vagaries of monetary policy or the economic performance of any given country. Like gold, it can be traded and exchanged globally. And while many people tend to forget this, like gold (or fiat currencies for that matter), bitcoin’s value is not intrinsic. It is based solely on collective faith. In gold’s case, this faith stretches back millenia. For bitcoin, only about a decade. That is certainly a point in gold’s favor. On the other hand, bitcoin has some qualities that make it superior to gold. It is much easier to transport and store, for instance. It can be exchanged more easily as well. And its supply is more predictable. Bitcoin is mined according to the immutable laws of mathematics, and we know that there will never be more than 21 million minted. Gold is mined in the ground, so it’s true total supply is not known with the same certainty. If the gold price rises significantly, it could spur a search for new sources, as has happened in the past.

Finally, many people are bullish on bitcoin because of its growing mainstream acceptance. In a recent report, Citi pointed out that bitcoin is mainstreaming as a currency: PayPal and Visa now accept cryptocurrencies, people can donate to the American Cancer Society in bitcoin, there are some 12,000 bitcoin ATMs in operation all over the world, and Visa has a card that lets customers earn bitcoin as a reward(15). The ecosystem around bitcoin is also maturing and professionalising, with exchanges offering bitcoin borrowing and lending, OTC markets arising for large orders, derivative products emerging, brokers offering best execution, and custodians helping companies safely store large holdings.

In other words, it looks very much like bitcoin and other cryptocurrencies are here to stay. If there were no other reason, this is one strong argument in favor of corporate treasurers taking a serious look at this new asset class.

In a (tinted) glass house – transparency in crypto markets

One of the main areas of confusion about cryptocurrency markets has to do with the anonymity of transactions. It is true for instance that bitcoin transactions are not necessarily directly associated with a person or entity. There is no onboarding process to use Bitcoin, and transactions on the Bitcoin ledger are only associated with a public key. That said, they are far from anonymous. Because the Bitcoin ledger is public and immutable, it is possible to analyse it in some detail – all the way back to the first transaction.

Clever analysis of flows can reveal a great amount of information, and today there are a number of on-chain data providers like Chainalysis or Glassnode that provide a number of analysis and forensic services based on study of the public ledger. This includes for example mapping bitcoin addresses to various exchanges and monitoring flows from them, information that can be very useful for corporate and institutional investors.

Below we provide two examples.

On February 8 of this year, Tesla revealed in an SEC filing30 that it had purchased 48,000 bitcoin at an aggregated purchase price of USD 1.5 billion, or some USD 31,000 per coin. We can see that Coinbase – one of the largest crypto exchanges in the US – saw a number of large outflows of BTC in January. While we cannot be certain that these outflows belonged to Tesla, such large movements can be an indication of larger transactions or activity by institutional players. At the same time, we can see that bitcoin traded at a premium on Coinbase compared to other exchanges during various periods of the run-up in the bitcoin price from USD 30,000 to its USD 60,000 high. This can indicate buying pressure. Similar behavior was spotted during MicroStrategy’s bitcoin purchases.

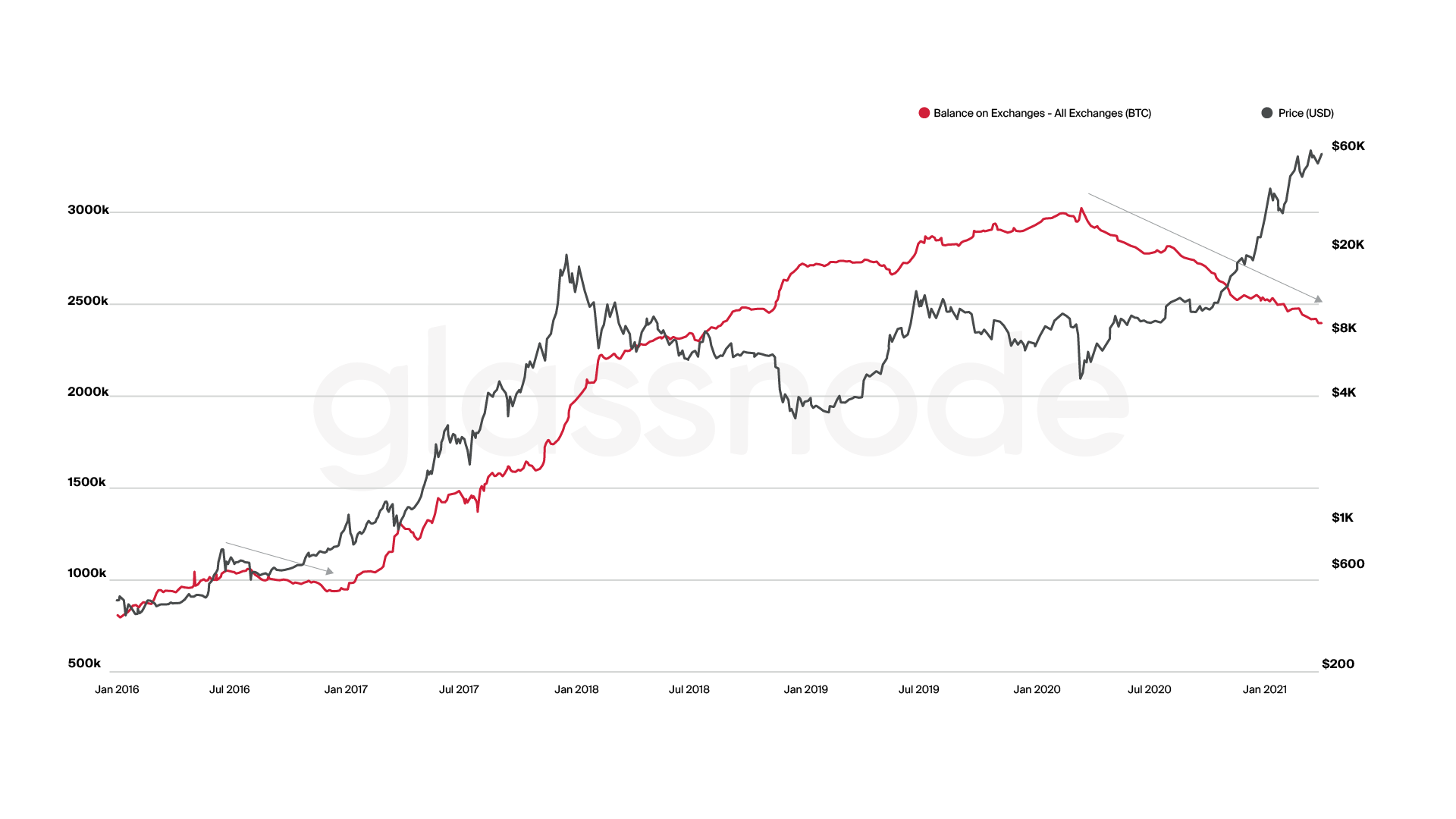

Another interesting metric indicating increased institutional interest in bitcoin is the amount of bitcoin held on exchanges. Since March, 2020 we have seen some 600,000 bitcoin withdrawn, worth some USD 30 billion at current prices. The presumption is that these coins are being put into cold storage or some other type of custody because the owners intend to hold on to them and not trade them. Considering the amounts, this too speaks for institutional involvement. Such a reduction in supply could also indicate more fuel for the current bull run. While there is no guarantee that history will repeat itself, similar behavior was seen in the early stages of the 2016-2017 bull run (see red arrow on chart).

To the dogs – the case against bitcoin as a treasury asset

Every country treasures its monopoly on controlling the supply and demand [of money]. They don’t want other monies to be operating or competing, because things can get out of control. So I think that it would be very likely that you will have it under a certain set of circumstances outlawed the way gold was outlawed.

Above we sketched the case for bitcoin and cryptocurrencies as a treasury asset. Corporate treasurers and institutional investors should consider the risks as well.

Of these, perhaps the most significant is the risk of bitcoin and other cryptocurrencies being banned by governments keen to protect their monopoly on coinage. There is ample precedent – those who believe in bitcoin as digital gold might keep in mind that the US banned the private ownership of gold bullion and coins between 1933 and 1974(17). More recently, in 2017 China effectively banned cryptocurrencies by outlawing their exchange for fiat(18). While this has not happened in the West, recent negative remarks by both US Treasury Secretary Janet Yellen(19) and European Central Bank head Christine Lagarde(20) make clear that bitcoin’s increased popularity is bringing increased regulatory scrutiny as well.

A less discussed, but equally plausible, threat to bitcoin is competition. Cryptocurrencies are very easy to create, and thousands of them exist today(21). If some of these become accepted as stores of value alongside bitcoin, the effective supply of cryptocurrency “safe haven” assets would rise, putting downward pressure on prices. (That said, despite current competitors, including a few direct variants of bitcoin like Bitcoin Cash, BTC’s market capitalisation today dwarfs that of all other cryptocurrencies.) Another risk is bitcoin’s volatility, which has historically been very high. That makes its purchasing power at any given moment in the future hard to predict, a potentially serious problem for holders who need to liquidate at a specific time in order to meet an obligation.

There are also risks to Bitcoin as a technology. Before going into these, it should be noted that the protocol itself has proven to be extraordinarily robust. In the 12 years of its existence it has never failed, and the Bitcoin ledger has never been successfully hacked. (If you see a headline about a bitcoin hack, it is always an exchange or a wallet or an individual whose private keys have been compromised; such events are cyber security failures and have nothing to do with the Bitcoin protocol itself.)

That said, there are technological threats that need to be considered. The one most often cited is from quantum computing. Thanks to Shor’s algorithm(22), we know it is theoretically possible for powerful enough quantum computers to crack the encryption that underlies the Bitcoin protocol. This could be used to steal private keys and the associated bitcoin. While real, the quantum threat has to be kept in perspective. First off, it does not apply to most bitcoin holdings. According to one study, only about 25% of bitcoin held in wallets today is exposed to quantum decryption – mostly due to shoddy security practices by the holders of the private keys(23). This, however, only applies to bitcoin held in storage. All bitcoin could theorectically be vulnerable to quantum key pilfering during transactions, when keys are exposed. That prospect is certainly worrisome. The good news is that people are already looking at ways to update the Bitcoin protocol to harden it against quantum attack. It should also be noted that quantum computers able to crack Bitcoin’s cryptography would be a threat to the security of the Internet as a whole. In other words, while quantum codebreaking is a major threat for bitcoin, when it arrives society may find itself facing far more serious problems than the collapse of a few cryptocurrencies.

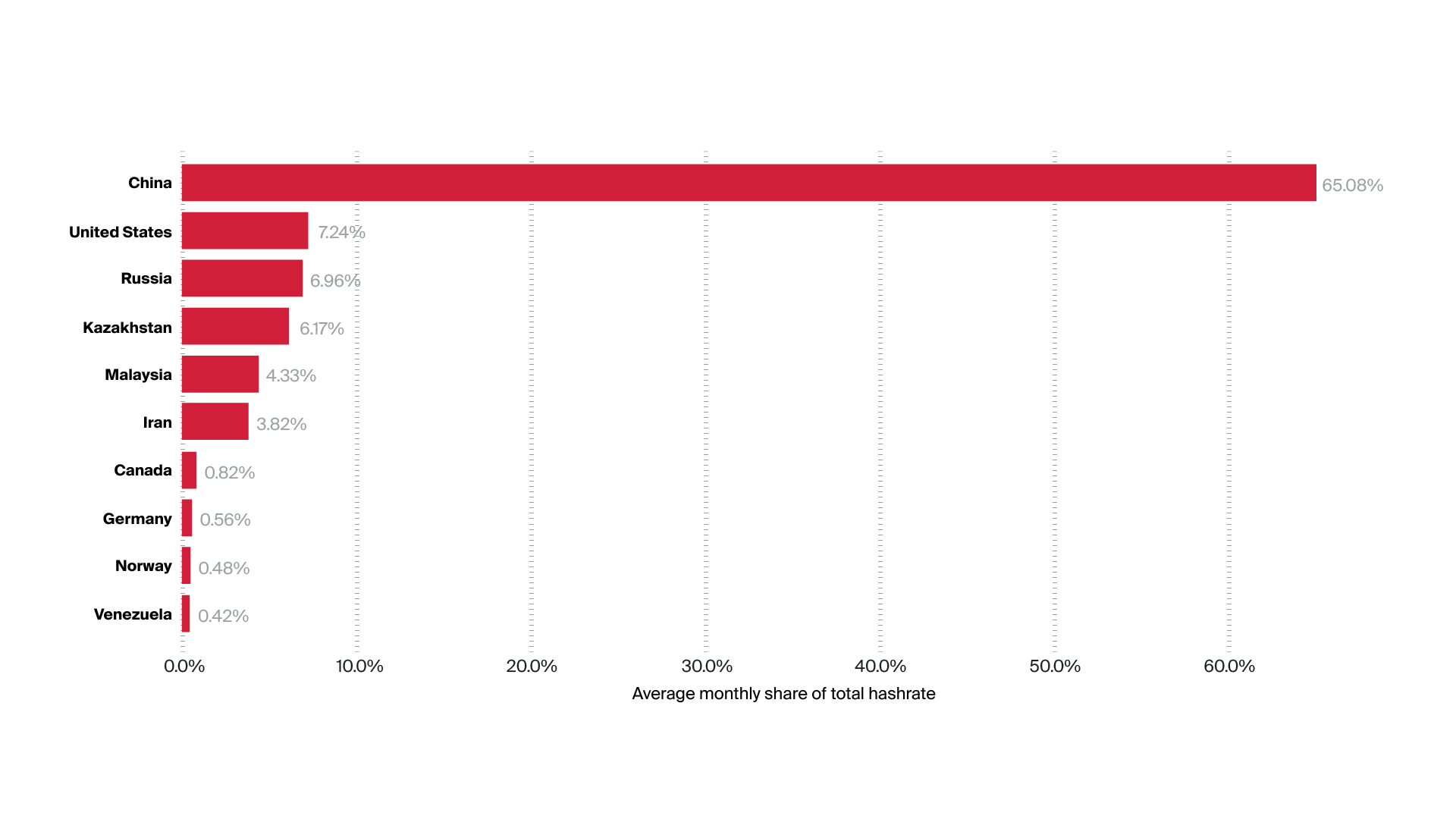

Another technology-related threat to Bitcoin comes from the centralisation of mining. Bitcoin and other decentralised cryptocurrencies rely on miners to do the work of processing transactions. They do so in competition with each other, so that

the fastest miners – meaning those with the most computing power – tend to win the fees. Any miner however who attains more than half of the mining power on the network could theoretically alter the ledger to award itself other people’s bitcoin (this is referred to as a “51% attack”). It is true that most of the mining power in Bitcoin today is concentrated in large mining pools based in China (where energy is cheap) and using specialised hardware (ASICs) manufactured by only a handful of companies. Such geographical and technological concentration is certainly a cause for concern. But here too there are caveats. A successful 51% attack would very likely be a Pyrrhic victory, destroying trust in the currency as a whole and leaving the thief with loads of expensively acquired but otherwise worthless bits and bytes. Considering the cost of such an attack, it is hard to see the incentive.

Lastly, companies could face reputational risks if they move treasury assets into bitcoin. Cryptocurrencies are still controversial to a lot of people, and important stakeholders – including shareholders, investors or even customers – might react negatively to the news. There are generally two areas of concern. One is that Bitcoin is associated with high use of energy. As we have discussed in detail elsewhere(24), there are many misconceptions around Bitcoin’s energy use and carbon footprint, both of which are not as severe as many people think. Bitcoin specifically, and cryptocurrencies generally, are also widely associated with the darknet and criminal and terrorist activity. Here too perceptions are far more negative than the reality. In truth bitcoin transactions are highly traceable, as many criminals have discovered to their chagrin (see our section “Transparency in crypto markets”). That said, these negative perceptions are hard to shake. Companies will need to take this into account in their messaging.

Playbook – what to consider when making the move to crypto

Having weighed the pros and cons and decided in favor of adopting bitcoin as a treasury asset, companies will find themselves with a new challenge: how to go about actually doing it. Buying, selling and safekeeping cryptocurrencies is very different than with traditional financial assets, and it will be unfamiliar ground for most corporate treasury departments.

Luckily, as with many new technologies, early adopters are keen to see the community grow and so to share their experiences. MicroStrategy, which was arguably the first major corporate to go all in on bitcoin as a treasury asset, has also been going out of its way to help others do the same, with a dedicated web page, free documentation and webinars(25). Others have been doing similar things. Square, for instance, has published a short white paper explaining how it made its BTC treasury acquisitions(26). It has also open sourced some of its documents as well as its cold storage solution.

With these and other testimonials in mind, as well as our own experience catering to our clients’ needs, below we present some of the most important things companies need to do when considering making the move into crypto.

Develop a crypto treasury strategy and policies. Having made the decision to get in, companies need to first develop their strategy. One fundamental choice, according to MicroStrategy, is whether to pursue a P&L-based or a balance sheet strategy, the former geared towards investment in crypto for profit, the latter more as a long-term store of value for treasury reserve purposes. Companies will need to consider how much money they want to commit, who in the organisation will be responsible

for the project, and who will be responsible for day-to-day execution (including, importantly, who has access to the private keys and so can initiate transactions). Companies will have to start thinking about how they want to invest, whether through a fund or directly through brokers and custodians. Trading policies (how much to invest, when, and how to do so in a market that can still be moved by large transactions) need to be worked out. All of this should then be codified in a Treasury Policy and a Trading Policy document, and signed off on (usually at Board level).

Do a lot of research, and prepare to make the case and educate both internally and externally. As already touched upon, bitcoin and cryptocurrencies remain controversial in many quarters. The decision to move part or all of a company’s

wealth into this new asset class is likely to raise a lot of questions. Companies should therefore do their homework thoroughly, researching and learning as much as they can about this new industry. Unlike with other types of projects, they should also take the time to document the journey – preparing detailed educational dossiers and/or presentations that explain the rationale behind the move and educate on crypto in general. These can then be used internally, for example to make the case at Board level in order to get signoff and/or among staff to get buy-in. And they can provide a basis for external communications, PR and investor relations campaigns aimed at making the case and answering any and all concerns. Reactions may be intense, so companies should be prepared to face some tough grilling. The more homework they have done, and the more sure they are of their own convictions, the easier it will be to weather the storm.

Work with legal, finance and tax experts who are familiar with crypto. Bitcoin and cryptocurrencies are not only new

technologies. They also raise a large number of sometimes quite thorny legal, regulatory, financial, accounting and tax questions. Many of these are still not settled. In such a new environment, companies cannot expect to have the requisite knowledge available in-house, and so should consult specialists. The good news is that the industry is growing rapidly. Not only is there an increasing number of specialist providers, many traditional advisory firms are opening cryptocurrency and blockchain departments.

Work with crypto execution experts. When it comes time to buy and sell crypto assets, companies used to traditional financial markets will find themselves in unfamiliar territory. Here too it makes sense to work with experts, for example cryptocurrency brokers or exchanges. Companies should start researching who these are in the planning phase and learn about their offerings with an eye to finding the right partners for their particular strategy. As we discuss in detail in our section on “Transparency in crypto markets”, buying bitcoin in large amounts presents unique challenges compared to other assets. The market is extremely volatile, so it can be tricky to lock in a price. While there is plenty of liquidity, large orders can still move the market and, depending on the circumstances, it can be fairly easy for observers to discover who is behind them. Using specialists can help mitigate some of these problems.

Custody. Asset custody in the crypto world is quite different than in the traditional one. In crypto, safeguarding assets means safeguarding cryptographic keys. For large amounts of bitcoin a cold storage solution is highly recommended. This is the storage of the keys in safe locations not accessible by any computer network – much like a traditional bank vault. Companies can do this themselves, or they can make use of professional custodians. If the latter, for risk management purposes companies should consider using more than one, and should carry out careful due diligence on all potential partners. Contrary to what many believe, there is insurance available in the crypto world. Many custodians offer insurance themselves or work with specialist providers. That said, these policies are not cheap, and companies should be prepared to pay a premium.

Be prepared on the IT/Infosec side. Adopting bitcoin as a treasury asset is as much an IT project as a treasury one.

Companies going heavily into crypto will find that their IT security needs have become exponentially more complex, since once news gets out that they hold bitcoin, they will be at increased risk of a targeted attack. Companies should prepare early and have

their IT and Infosec departments involved in the process from the beginning. As with other stakeholders, there is likely to be an educational element involved here too. Companies should therefore take pains to get buy-in from their IT departments as early as possible, and make sure that they have the necessary technical skills to oversee the project. Negotiate service agreements with an eye to discounts. Last but not least, companies will want to negotiate with their preferred service providers as soon as they can. As

MicroStrategy among others has pointed out(27), there is good news here. This is still a very new industry, and providers are hungry for business. Companies may find they have a fair amount of leverage in price negotiations.

Conclusion

A few years ago people wondered if crypto would cease to exist, but that existence question is no longer valid. The longer something stays in existence the less likely it’s a fad. If it is not going away, everyone needs to figure out how to interact with it.

Head of DLT and Digital Assets at Citi

Depending on your point of view, the above account of the pros and cons of cryptocurrencies as a treasury asset may come across as compelling, chilling or simply confusing. It could very well be a combination of all three. That is understandable. Discussions around crypto assets tend to be complex and sometimes heated. It can be hard to find one’s bearings. If we can leave the reader with one thought, it is that the time has come for CEOs, CFOs and corporate treasurers to make the journey of discovery, wherever it may lead. One of the best ways to start is by following those who have already trod the path. While there are many examples to choose from, recently Seetee, a new subsidiary of Aker (one of Norway’s largest industrial conglomerates) published a remarkable letter that provides an excellent example of knowledgeable and thoughtful people from a traditional industry going down the rabbit hole with eyes wide open and coming back to tell the tale. We highly recommend it as a good example how to approach when coming to crypto for the first time. As Aker Chairman Kjell Inge Røkke writes, what’s most important is an open mind and as few preconceptions as possible:

“Aker is the first major company in Scandinavia to allocate capital to bitcoin. We’re not going to be the last. We don’t claim to know everything about the subject. And as we have learned something, we realise that the concept of money is in essence somehow unknowable and constantly changing. … We are always curious and eager to learn. And more importantly, when we believe in something or someone, we are prepared to look like idiots for extended periods of time. In the words of the late Norwegian politician Einar Førde … “you have to put yourself in the position to be labeled an idiot now and then—or else life would become too boring!” (29)

1. Bitcoin CEO: MicroStrategy’s Michael Saylor Explains His $425M Bet on BTC, CoinDesk, 15 September 2020.

2. World’s Biggest Business Intelligence Firm Buys 21K Bitcoin for $250M, CoinTelegraph, 11 August, 2020.

3. MicroStrategy buys more than $1 billion worth of bitcoin, adding to massive holdings, CNBC, 24 February, 2021.

4. MicroStrategy Adopts Bitcoin as Primary Treasury Reserve Asset, press release on BusinessWire, 11 August 2020.

5. Tesla buys $1.5B in bitcoin, may accept the cryptocurrency as payment in the future, TechCrunch, 8 February, 2021.

6. Square, Inc. Announces Fourth Quarter and Full Year 2020 Results, Square website, 23 February, 2021.

7. Paul Tudor Jones says he likes bitcoin even more now, rally still in the ‘first inning’, CNBC, 22 October, 2021.

8. Billionaire Hedge Fund Investor Druckenmiller Says He Owns Bitcoin in CNBC Interview, CoinDesk, 9 November, 2020.

9. JPMorgan Says Investors Could Make Bitcoin 1% of Portfolios, Bloomberg, 25 February, 2021.

10. Coinbase’s Public Listing is a Cryptocurrency Coming Out Party, The New York Times, 14 April, 2021

11. New payment option: Bitcoin, AXA Insurance website

12. We would like to stress that nothing in this paper is meant as investment advice in any way, shape or form, and should not be taken as such.

13. Examining the Role of Cryptoassets in Corporate Treasury Management, Smith and Crown, 4 December, 2020

14. In this paper we tend to refer to bitcoin for convenience sake, and because bitcoin is currently by far the most widely held crypto asset. Many of the arguments here can be made for cryptocurrencies generally.

15. BITCOIN: At the tipping point. Citi GPS: Global Perspectives

16. Dalio sees ‘good probability’ bitcoin gets outlawed, Yahoo!Finance, 24 March, 2021.

17. Executive Order 6102, Wikipedia.

18. Why China had to “Ban” Cryptocurrency but the U.S. did not: A Comparative Analysis of Regulations on Crypto-Markets Between the U.S. and China, Washington University Global Studies Law Review, Volume 18, Issue 2, 2019.

19. Yellen sounds warning about ‘extremely inefficient’ bitcoin, CNBC, 22 February, 2021

20. ECB’s Lagarde calls for regulating Bitcoin’s “funny business”, Bloomberg, 13 January, 2021.

21. As of this writing, CoinMarketCap is tracking over 4,000 cryptocurrencies.

22. Shor’s algorithm, Wikipedia.

23. See Quantum computers and the Bitcoin blockchain, Deloitte, undated. The exposure occurs when someone reuses the same address for more than one transaction, a practice that is highly discouraged, yet still unfortunately done.

24. Bitcoin’s Energy Consumption, Bitcoin Suisse Decrypt

25. This section relies heavily on the excellent content from MicroStrategy, which is highly recommended. See above all Bitcoin Corporate Playbook with Phong Le and Jeremy Price, MicroStrategy, 4 February 2021

26. Square Inc. Bitcoin Investment White Paper, October 2020.

27. Op. cit. Bitcoin Corporate Playbook with Phong Le and Jeremy Price, MicroStrategy, 4 February 2021.

28. Op.Cit. BITCOIN: At the tipping point. Citi GPS: Global Perspectives & Solutions, March 2021.

29. Aker Shareholder Letter Announcing Seetee, March 2021.

Bitcoin Suisse