Denis Oevermann

Investment Analyst / Crypto Researcher

Crypto David versus Macro Goliath (nur auf Englisch verfügbar)

19.12.2023 - 12 Minuten Lesedauer

Navigating the Crypto Horizon of 2024 and beyond

As we approach 2024, the crypto market stands at a crossroad of challenging macroeconomic conditions, and a promising bull market. After a modest recovery from its 2023 lows, we might see 2024 split into two distinct phases. The first one testing the crypto market’s resilience amidst a potential recession, tightening liquidity and monetary conditions, followed by a second phase, a full-fledged bull run fueled by easing macro conditi- ons as well as the halving and a potential Bitcoin spot ETF.

Our Crypto & Macro Outlook 2024 is anchored in the insights gained from our Crypto & Macro series which we established in the beginning of 2023 to navigate the crypto cycles. These insights successfully helped us to identify various low risk buying opportunities throughout the year amidst tightening macroeconomic conditions. Despite 2023 being a choppy year these low risk buying opportunities signaled a subtle yet overall pivotal shift towards a long-term bullish stance, while we navigated through growing headwinds and increasing odds of a recession.

Our Crypto & Macro Outlook 2024 starts by dissecting the current state of macroeconomics and why the overall macro conditions continue to tighten. However, we also find that crypto is looking bullish long-term nevertheless and that the current times are very attractive for positioning and weather proofing a portfolio for the next bull run. We back the aforementioned with our proprietary in-house risk metrics and cycle dynamics.

Of course, we do not just try to navigate and forecast the macroeconomic conditions, we want to provide a facts and data based, in-depth assessment of potential price projections for the upcoming crypto bull market. We explore the potential market capitalization for the crypto market, as well as peak bull market valuations and price targets for Bitcoin and Ethereum, based on our dynamic price risk metrics and general crypto market cycle dynamics.

As we delve into the most critical macro and crypto specific factors that impact the crypto asset class, we keep our focus on what 2024 holds, by supplementing each analysis step with projections and potential scenarios for the upcoming year and beyond. Our goal is to not only provide a prediction and an outlook, but an actual guide to help navigate the crypto market in 2024 and beyond.

As we approach 2024, the crypto market stands at a crossroad of challenging macro-economic conditions, and a promising bull market.

Denis Oevermann, Investment Analyst and Crypto Researcher

Monetary Conditions: Economic Cycles and Market Dynamics

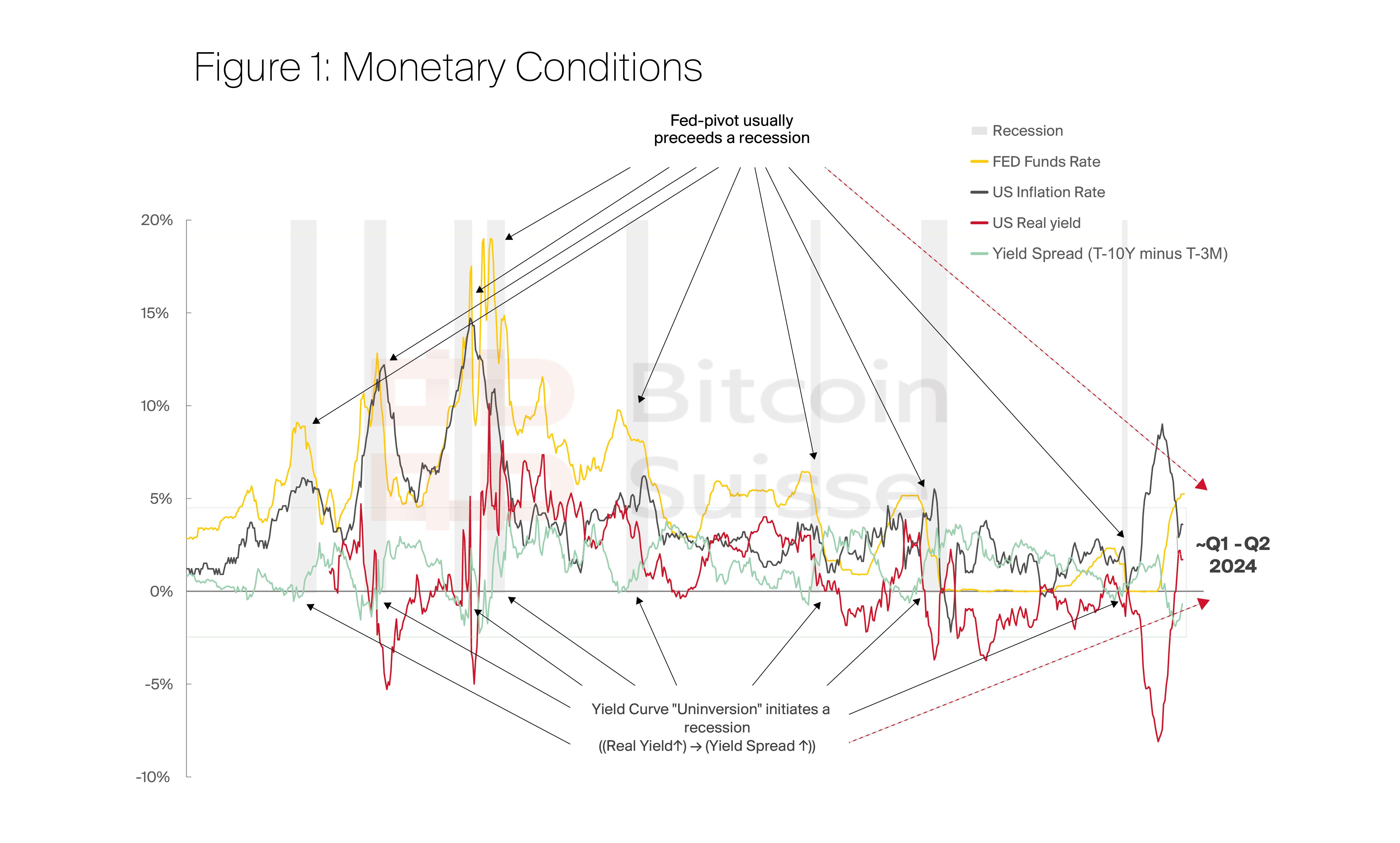

A major building block of macroeconomic conditions and a gauge for assessing the overall economic health are the monetary conditions, which dictate and affect economic fluctuations and price stability. Monetary conditions simultaneously reflect what is going on under the surface in the broad economy and in financial markets. On top of that, patterns in monetary conditions are repeating and almost always follow similar paths which lead to quite predictable outcomes.

We can observe that historically recessions occurred or have been declared retrospectively when the monetary conditions changed in the following manner. An initial spike in inflation, caused by excess liquidity and monetary easing, forces interest rate hikes in response. Short-term interest rates are hiked until inflation comes down sufficiently, while real yields recover and increase somewhat. In the meantime, however, due to the usually abrupt hiking of the short-term interest rate, yield spreads turn negative, implying that short-term interest rates (hiked by the central bank) yield more than long-term interest rates (their equilibrium pricing is determined by supply and demand in the fixed income market). This clearly unsustainable and in the long run “irrational” imbalance, of receiving less yield for long-term debt than the yield on short-term debt, has historically always been temporary. If the long end of the yield curve (long-term interest rates) is lower than the short end of the yield curve (short-term interest rates), the yield curve becomes inverted, which has historically always caused either a recession (in 90% of the instances) or an economic downturn (in the remaining 10% of the incidents) following every single yield curve inversion in the past century.

However, the economic turmoil or recession did not unfold upon the yield curve inversion, but rather once the yield curve un-inverts, which usually occurs an average 12-18 months post initial inversion. The current yield curve inversion occurred in July 2022. With the yield spreads, the difference between long-term rates and short-term rates, still being a moderate distance from turning positive, i.e., the yield curve un-inverting, a recession could still be a few months out, however.

Implications of the current regime of “higher for longer”, which has been common amidst similar economic and monetary conditions, are that the rates will unlikely be cut before economic weakness has materialized. This is required to sustainably bring down inflation and help reset the overall system to a healthy, balanced level, which will form a solid fundament for future bull markets across all risk assets. Currently, markets price in first rate cuts around spring 2024, which would align with our predictions for when economic turmoil might materialize, as well as our “second scare” scenario from our fifth Crypto & Macro edition. The rate cuts priced in by the market can be thought of as the aggregate expectation of market participants, for when a pivot in monetary policy might be necessary, thus when a major market weakness is anticipated.

Figure 1: Monetary Conditions

Outlook for 2024

- Monetary conditions will remain tight until Q1/Q2 2024, to sustainably reduce inflation. If the FED is forced or decides to pivot and ease prior to balancing inflation, there is a high likelihood of a resurge in inflation later, and a potential “lost decade” ahead in financial markets.

- High risk-free rates make the risk premium of most risk assets unattractive, so high- risk assets will give way to low-risk assets. Holding the blue chips out of the risk assets such as BTC and ETH is therefore to be preferred in such periods.

- Once economic weakness materializes, and markets witness steep short-term corrections, rates will be cut subsequently, marking the beginning of a new easing cycle and signal a new rally across all risk assets fueled by increasing liquidity.

Liquidity Conditions: Ebb and Flow

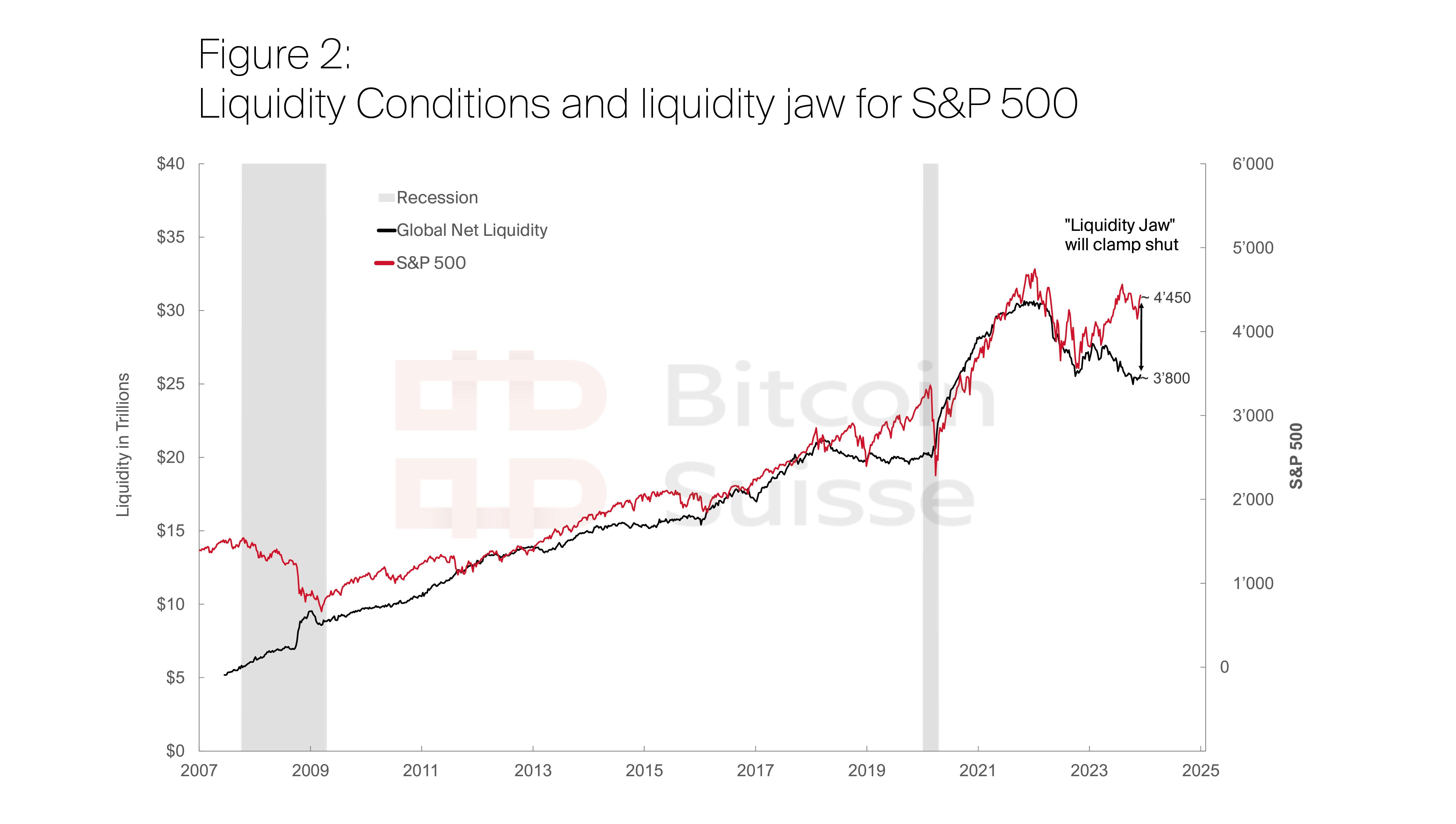

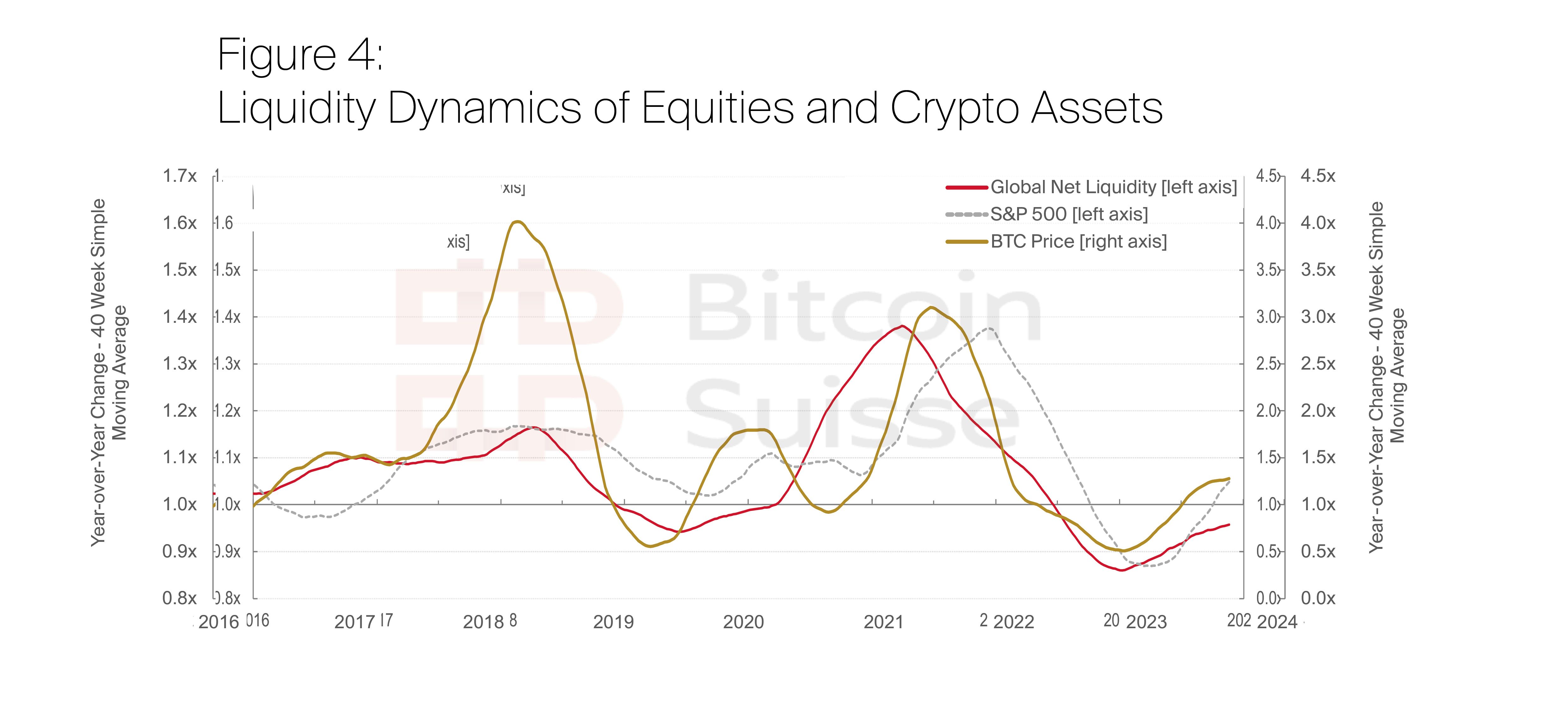

Though fundamentals matter in the longterm, the overall price action and market dynamics of asset markets and the crypto market are impacted and driven by changes in liquidity. Overall, liquidity is a major driver of asset performance and can be considered a compensation for “currency debasement”. Large in- and outflows of liquidity substantially boost or suppress price action and a close examination of Global Net Liquidity gives potential insights to short- to mid-term price action. Global Net Liquidity is the entirety of global central banks’ asset purchases and balance sheet expansions and thus, a major driver of available liquidity to financial markets. Contractions in Global Net Liquidity coincide with financial market downturns, while liquidity expansions fuel general economic growth and uptrends in asset prices. Given the close connection of asset returns, following the expansion in liquidity, a disconnect between the two can be, and has always been, only temporary. Currently, markets front run Global Net Liquidity substantially, creating a large gap between liquidity induced price levels and current price levels. This gap, between liquidity and asset prices, due to its appearance also called “liquidity jaw”, will close, as said market inefficiencies can only remain in the interim.

Figure 2: Liquidity conditions and liquidity jaw for S&P 500

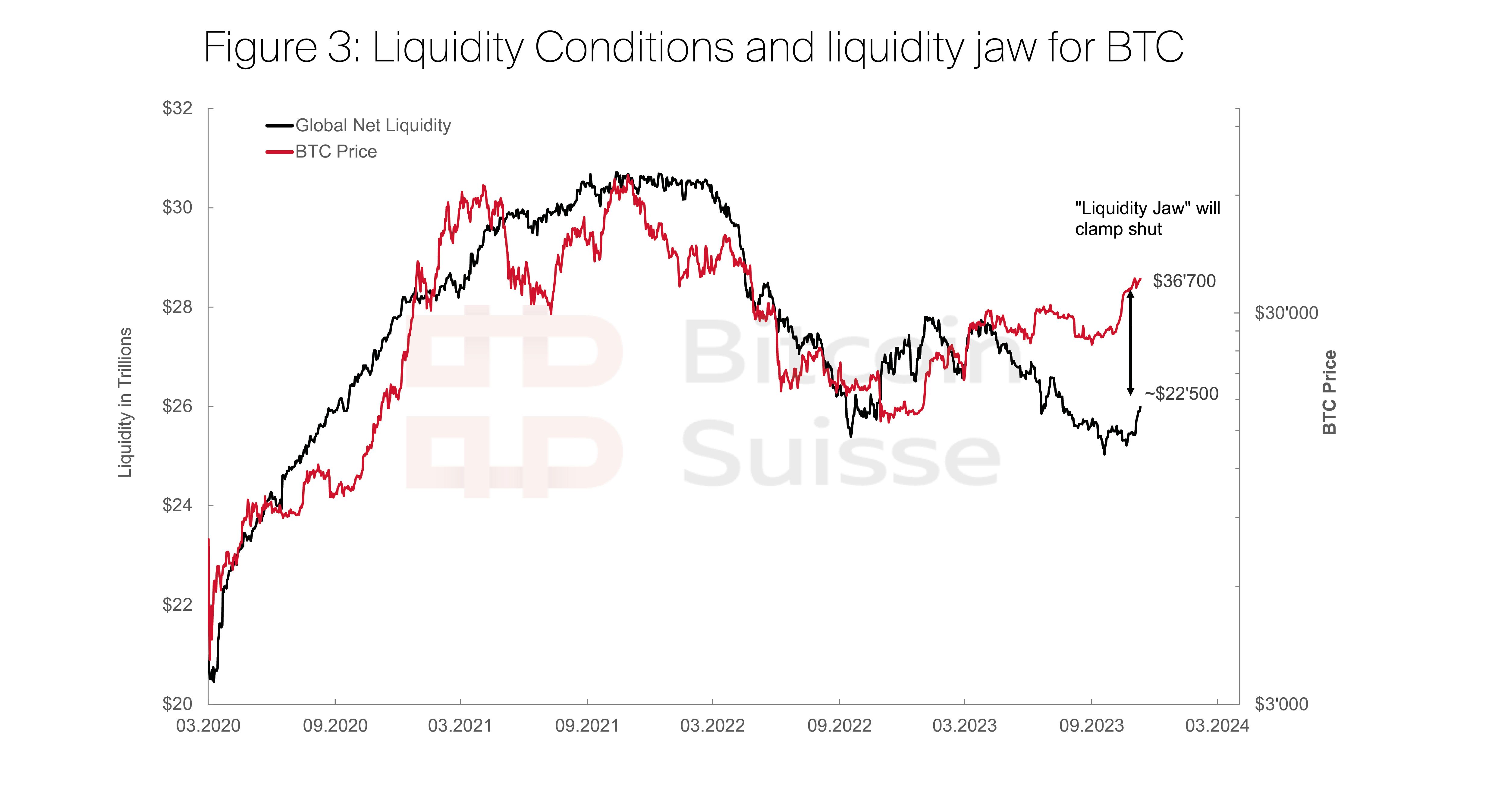

Figure 3: Liquidity conditions and liquidity jaw for BTC

Overall, global liquidity conditions are still relatively tight, though the general momentum shifts, implying liquidity tightening is slowing down. However, liquidity overall will continue to remain tight, until financial markets and economic conditions have declined sufficiently, to justify easing liquidity conditions again. Furthermore, Global Net Liquidity is mainly liquidity to financial markets. Therefore, only the liquidity provision to financial markets is tightening slower than prior. The overall trend and lagging impact on financial markets is still going to add downward pressure on valuations, it will just subside. The liquidity tightness and financial conditions for the economy and businesses itself on the other hand, are tightening even more, as measured by ease of access to loans, new loans granted and other means of liquidity.

A last point to consider regarding the recent spike and “easing” in liquidity is that a large part of the overall quantitative tightening has been offset by the FED’s Reserve Repurchase Agreements (RRP) account being reduced substantially. The FED borrowed more than $2 trillion from the financial system between 2021 and 2023 to absorb excess liquidity to control capital liquidity levels in the markets and maintain long-term monetary policy goals. With quantitative tightening currently ongoing, the FED can “finally” dispose the liquidity back into the system, resetting their RRP balance, while offsetting the effects of the ongoing quantitative tightening somewhat. This effectively reduced the initial repercussions of the quantitative tightening, as it cancelled out with a partial quantitative easing taking place in the meantime. In summary, the real effects of the reduction in Global Net Liquidity have therefore been artificially low, and distorted.

Despite the speed at which liquidity tightening slowing down, the bottom line is that liquidity is still tightening. The effects from that will materialize gradually, especially after the RRP is drained entirely and does not absorb the tightening liquidity anymore. Even though Bitcoin has had a remarkable rally of 130% year to date (YTD), the overall crypto market capitalization (CMC) has not followed suit, being up only around 80% YTD. This indicates that most of the rally is due to a reshuffling and re-allocation of liquidity that has been in the crypto market already. Net new money inflows to the crypto market have been modest overall, and after the most recent rally since September 2023, the CMC is just 7% higher than the levels observed throughout the interim rallies around summer 2022 as well as April and July of 2023.

In Summary, tight liquidity stacks upon stringent monetary conditions and causes the remaining liquidity to only flow into the top assets with the lowest overall risk, which is Bitcoin in the case of the crypto market.

See Crypto & Macro 5.0 where we analyzed the market cycle and macroeconomic conditions interlinking dynamics in close detail. The good news with respect to liquidity is that crypto tends to react first to changes in liquidity and sometimes even front runs the anticipated changes in liquidity, as depicted below. Though the crypto market also front ran its liquidity induced valuation, it still shifted to an overall upwards momentum once the tightening in Global Net Liquidity slowed down. We expect these two induced valuations to re-align in the future, either through a drawback in crypto valuations in the near-term, or through easing liquidity conditions in the short to mid-term. Once liquidity conditions ease, crypto markets will rally first, and the fastest of all risk assets.

Figure 4: Liquidity dynamics of equities and crypto assets

Outlook for 2024

- Global Liquidity will remain tight in the interim and suppresses risk asset performance in the short term. This downward pressure will remain until risk assets corrected or liquidity conditions begin to ease.

- The crypto market is the most sensitive to liquidity, so once liquidity conditions ease, it will rally first and the most substantial of all risk assets. This will fuel the early bull-market stage even further.

- We see increased liquidity in asset and financial markets around mid2024, which will boost risk asset prices and close the liquidity jaw gradually.

Soft Landing, Soft Upside: Constrained Growth for Risk Assets

The solution to economic turmoil and an imbalanced economy and financial/monetary system is either a sharp reset through a recession, or a so-called soft landing, which slowly re-balances the economy over an extended period. The former quickly and abruptly resets the system, with harsh economic pain and weakness in financial markets, whereas the latter tries to slowly and “softly land” the economy into a more balanced equilibrium state, with less severe economic pain being felt by market participants. However, the downside is that soft landings do not manage to sufficiently reset the equilibrium initially, causing stagnation and economic tightness over an extended period until a reset materializes, such as in the 1970s. During this period inflation kept on flaring up repeatedly, because the monetary tightness was lifted too soon, in attempts to not cause the economy to crash abruptly. Consequently, equity markets did not achieve any noteworthy growth for more than a decade, while fluctuating, and neither achieving new all-time highs or lower lows. On the contrary, getting into a recession in the near term implies more economic pain and a correction in financial markets sooner, and more substantial upside potential sooner for market participants. The economy and markets will recover and move towards new all-time highs more easily on the back of a healthy, reset, and balanced economy than uncertainty and imbalanced conditions. A soft landing would have the likely tendency to delay either scenario while risk assets “climb the wall of worry” even further, not achieving noteworthy upside in the long run amidst non ideal macroeconomic conditions. A recession on the other hand would yield the necessary vent that markets require to correct and rebalance towards an equilibrium instantly and abruptly. A crash and recession get markets to a healthy state faster and more effectively than a soft landing would. For a healthy and sustained bull market in the crypto markets a soft landing is thus not the preferred outcome in the long run. In the interim, a recession would cause more potential headwinds and a short-term correction in crypto markets. However, such scenarios have in the past provided opportunities to accumulate further crypto asset exposure at more favorable prices, at a time when the crypto market cycle overall transitioned to its bullish phase.

Outlook for 2024

- A soft landing would stall the subsequent bull run for risk assets and crypto substantially, and markets will not repeat the same upside of prior years.

- In case of a recession, traditional risk assets will correct sharply, and drag down crypto alongside, followed by a long-term rally supported by a “healthy” reset. Recession equals volatility but also opportunity.

- In a recession scenario, crypto assets will likely be the first asset class to recover and rally, given their sensitivity and dependency on liquidity.

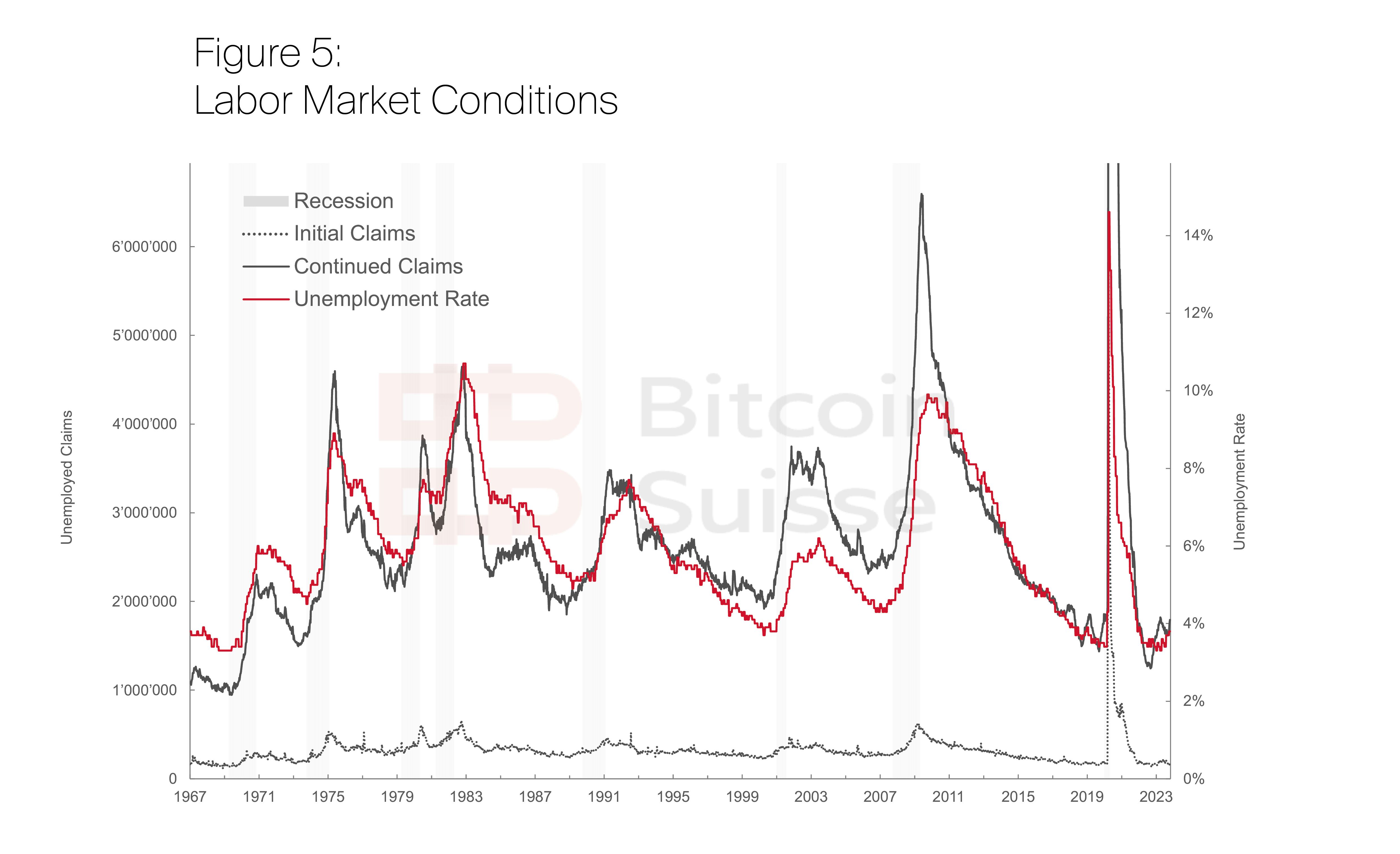

The Labor Market: A final threshold

Given the materializing weakness and economic repercussions due to stringent monetary conditions, tight liquidity conditions and stalling economic activity, the logically induced question would be why we have not seen a recession or economic downturn just yet. A major threshold that stands in between the aforementioned worsening conditions and an economic downturn is, at large, the labor market. As long as people remain in employment and do not drop out of the labor market, an economy can be quite resilient, and absorb a lot of headwinds before faltering.

The unemployment rate has not yet picked up substantially, and remains relatively flat as depicted below, while initial claims, i.e., people that become newly unemployed, did not increase at all over the past period. On the contrary, continued claims, i.e., people that dropped out of the labor market and struggle to find new employment and thus constitute the unemployment basis, continue to grow. A crucial observation is that it is not the initial claims or newly unemployed that drive and lead the unemployment rate, but continued claims, so those that fail to get back into employment. The continued claims have been rising consistently over the past periods, which only now, with a delay, is starting to slowly materialize and add upwards pressure to the unemployment rate. Historically, the unemployment rate tends to have sustained downwards trends at the end of which it reverses upwards sharply, with a recession occurring subsequently. Historically, the continued claims and subsequently the unemployment rate have never increased off their lows without a recession occurring afterwards.

Overall, the aggregate macroeconomic conditions start to show their effects on the leading labor market indicators, suggesting that the final threshold that keeps an economic downturn at bay might fall in the near future. At the current pace this scenario would be likely to unfold in early 2024, unless the labor market recovers and reverts in the opposite direction. Such a scenario would only push out “the inevitable” further, while increasing the likelihood of a soft landing. Given that the unemployment rate reached a 50-year low, on the back of monetary stimulus amidst an economic boom, this seems unlikely in the current regime.

Figure 5: Labor market conditions

Outlook for 2024

- The economic repercussions of stringent monetary conditions and tight liquidity conditions will continue to weaken the labor market.

- A recession in early 2024 is likely to be caused subsequently, following sufficient weakening of the labor market.

Yield Curve Inversion: Implications for Risk Assets

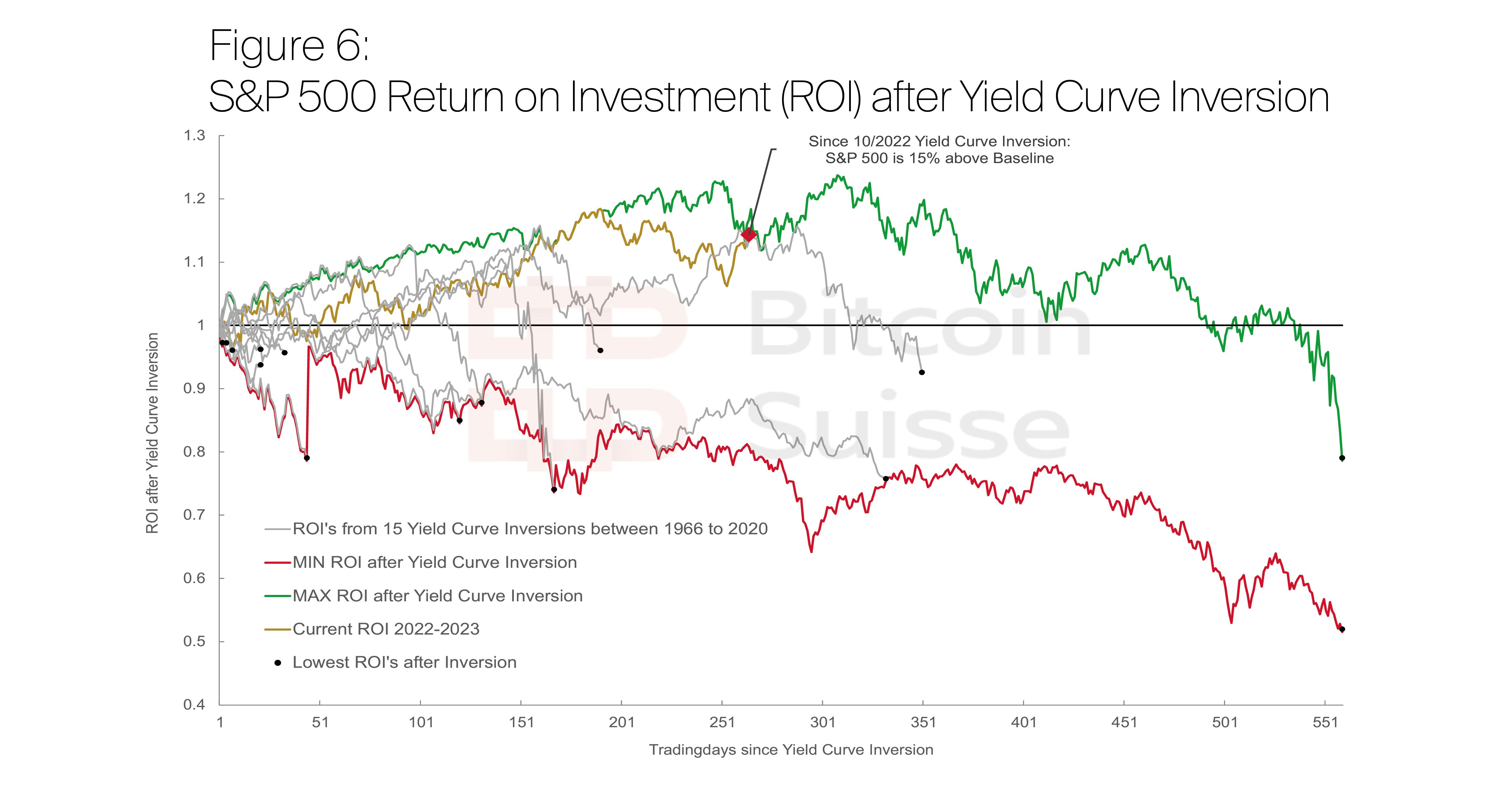

We have been observing and analyzing the yield curve closely throughout the year in our Crypto & Macro series due to its high significance in reflecting aggregated macroeconomic conditions. An inverted yield curve implies that interest rates of shorter duration treasuries are having a higher yield than those of longer duration treasuries, which is a clear market inefficiency, caused by mistrust and imbalances in the system. As mentioned previously, an inverted yield curve has led to either a recession in 90% of the incidents, and an economic downturn in 10% of the incidents in every yield curve inversion since the Great Depression almost a century ago. Though an inverted yield curve is thus a high certainty indicator that economic turmoil is ahead, the market dynamics of risk assets are somewhat detached from it in the interim.

As plotted below, markets have a high tendency to rally and “climb the wall of worry” into a recession or economic downturn once the yield curve inverted. However, the S&P 500 always turned lower in every single incident of a yield curve inversion, no matter how short or long-lived, despite its initial rallies. Out of 16 inversions since 1966, markets rallied substantially a total of eight times, yet in all cases markets closed below their valuations from the time of the yield curve becoming inverted. The average downturn for the S&P 500 post yield curve inversion in the past has been 16.7%. In the current cycle, the S&P stood at 3’859 when the yield curve inverted in October of 2022, and is up 16.6% ever since, valued at 4’500. Every single historical precedent indicates that the S&P would close below the 3’859 level at some point, while the average historical drop of 16.7% would imply an S&P valued at around 3’211, a roughly 30% drop from current levels. The S&P 500 not closing below the yield curve inversion level of 3’859, roughly 13% below current prices, would be the first outlier in the entire history of available data and be the only 1 out of 16 incidents where a yield curve inversion did not lead to subsequent lower valuations in equity markets.

The crypto market overall follows monetary and liquidity dynamics quite closely, being a risk asset such as the S&P 500, making it a reasonable assumption that it will show similar dynamics following a yield curve inversion. A drop below yield curve inversion levels would thus imply that BTC would drop below ~$20’000 and could even revisit the cycle lows. Such a scenario would require a 50% correction to the downside which seems less likely in our opinion, because even though crypto does get impacted and driven by monetary and liquidity conditions, the overall implications and economic repercussions of an inverted yield curve are largely confined to equities and traditional risk assets. Crypto, on the other hand, is likely less affected by these general macro factors. The overall impact of the inverted yield curve, and the inevitable un-inversion, will still impact crypto price dynamics negatively in the interim, though we project these to be short lived and crypto to recover from such an external hit as the first risk asset. An un-inverting yield curve could be seen as a short-lived opportunity to enter the crypto market at a lower valuation right at the start of the subsequent crypto bull run, as indicated by our research.

Figure 6: S&P 500 return on investment (ROI) after yield curve inversion

Outlook for 2024

- Risk assets such as equities and crypto are likely to rally into a potential recession.

- Equity markets will potentially correct in 2024 to the downside and the S&P 500 will drop below $3’859, its level from when the yield curve inverted.

- Upon the eventual yield curve un-inversion, the crypto market, together with other risk assets, will likely correct to the downside in the short-term, potentially offering long-term accumulation prices based upon historical evidence for risk assets.

Outlook for 2024: Overcoming Recession – Embracing the Rally

Overall, 2024 will be a very bullish year for the crypto market and we would generally classify it as an accumulation and buying opportunity based on our research. Still, we see some headwinds in early 2024 that could cause short-term corrections. The macro conditions are continuously tightening, and there is a low confidence that inflation will be under control very soon with rate cuts not priced in before spring/summer 2024. On top, markets remain reluctant to acquire treasuries at current interest rates, implying the average market expectation is still bearish on markets in the short-term and a correction is unlikely to occur very soon, but rather around the yield curve un-inversion.

Throughout 2023 the macro risks have materialized only slowly, but at some point, they will materialize abruptly, which has a high likelihood of occurring in early 2024. However, once the yield curve uninverts to its normal state and the anticipated macroeconomic conditions materialize in early 2024 falls in place with past seasonal corrections in crypto markets. Once sufficient economic pain has been caused to reset the system, monetary conditions will be eased, and liquidity subsequently injected into the system. Once the actual pivot and rate cut is imminent, bonds will be the first to bottom. Afterwards risk asset prices will recover quickly and move upwards again, driven by easing monetary and liquidity conditions. Because crypto assets are highly sensitive to liquidity, it will be the first risk asset to recover and rally substantially. Equities will still be lagging during this period as their prices are somewhat stickier and not only dependent on liquidity increasing, but also the economy recovering and improving.

Thus early 2024 will be the early stage of the next bull market. The only bearish catalyst we see for the crypto market is the macro side, which our research suggests to only materialize as a temporal correction phase in hindsight. This might be an opportunity amidst the early bull market, however, as indicated by the overall very bullish cycle dynamics predicted for 2024. Despite the recession risk which will cause the crypto market to witness a temporal correction, there might be opportunity costs linked to not being invested and exposed to the tremendous upside crypto potentially offers in the long-run, by not acquiring crypto assets in potentially lower risk price territory around the final stage of the bear market. Overall, a recession will see monetary and liquidity conditions ease in return, and since crypto bottoms first of risk assets it will rally even faster.

We do not see a cycle top in 2024 yet, unless something changes substantially on the macro end or crypto industry factors change dramatically. Based on our research and analysis, 2024 could be a buying and HODLing year before we approach the potential crypto cycle top in 2025. In summary we view 2024 as a potentially very bullish year longterm, implying that low prices and market corrections could support further accumulation.

Outlook for 2024

- Q1/Q2 of 2024 will see the economic turmoil play out – a recession is the most likely scenario.

- Crypto markets will correct simultaneously, and not revisit these lows again for the remainder of 2024, nor in the next bear market in 2026 and beyond.

- 2024 is likely a buying and HODLing year , it will mark the first half of the bull run – we do not expect a cycle peak before 2025.

Crypto Market Cap Projection

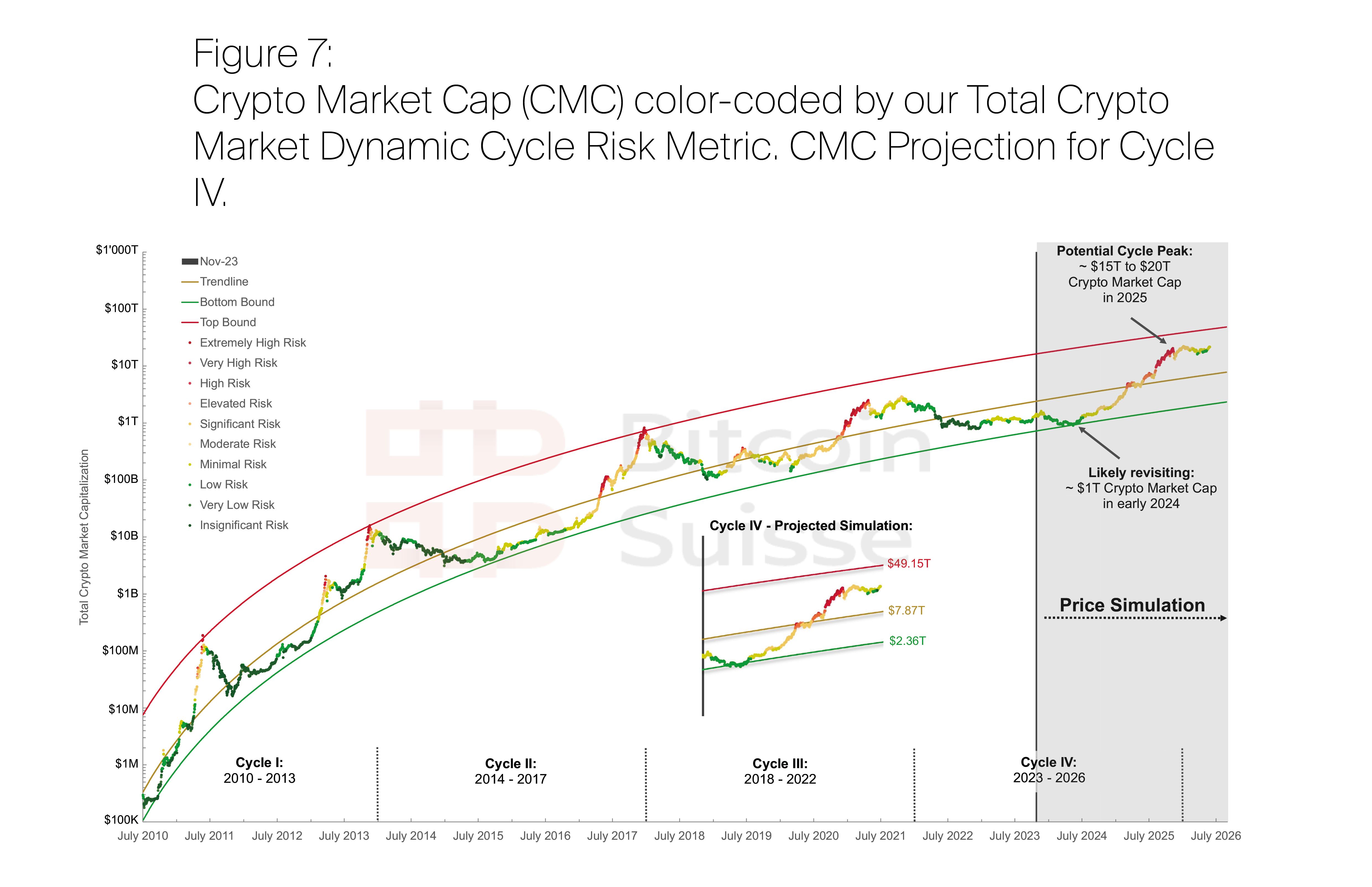

With the crypto market following an almost perfect logarithmic growth trend, due to its exponential growth and S-Curve adoption, it is easy to model and predict the general dynamics of its seasonal trends and overall cyclicality with relatively high confidence. Plotted below is the total crypto market capitalization (CMC) color coded by our Total Crypto Market Dynamic Cycle Risk Metric which gauges whether the crypto market, based on a specific market cap observation is classified as high risk or low risk. The risk metric considers factors such as momentum, trend, relative market strength and relative inter crypto market cycle dynamics. If prices move up moderately, the risk stays relatively constant, whereas prices moving sideways or declining will reduce the implied risk of the Total Crypto Market Dynamic Cycle Risk Metric. Fitted to the overall growth trend of the CMC are its logarithmic trend channels for cycle tops and cycle bottoms as well as the overall total crypto market cap trendline. The risk metric ought to be used in conjunction with the trend channels to generate a reliable buy or sell signal; the risk itself can be indicated as relatively low, due to tremendous declines in price, while the overall price itself might still be substantially above the trendline. Consequently, dark red, high-risk indications, way above the trendline and close to the top bound function act as a quite reliable sell signal, whereas green and dark green, low risk indications, below the trendline, close to the bottom bound function as reliable long-term entry prices and dollar cost average (DCA) price levels. We can use these metrics and characteristics to model and simulate the potential progression of the present market Cycle IV and the upcoming bull market. Considering past crypto cycle dynamics and the external headwinds from macroeconomic conditions, there is a potential revisiting of the lower bound and a CMC of around ~$1T in early 2024. Throughout this phase the overall risk remains relatively low and offers quite optimal long-term entry prices to position for the next crypto cycle and upcoming bull market. The remaining risk for altcoins is still relatively high, as also the intra cycle dynamics of crypto induce that they will on average decline against BTC and ETH. This phase could be followed by a moderate and consistent early bull run phase upwards of ~$5T by year-end 2024, based on historical cycle dynamics. This early bull market rally will be largely confined to BTC and ETH, while the large share of altcoins will likely underperform on a relative basis, and be the reason the CMC does not grow as rapidly initially as BTC and ETH. The final bull market phase and Cycle IV peak is projected to be in mid-2025 at a potential peak CMC of up to ~$15T to $20T overall. The Top Bound for Cycle IV in late 2025 stands at $49T with the overall Trendline supporting a CMC of $7.9T. During this final market phase of Cycle IV CMC could grow almost exponentially, while BTC and ETH profits are funneled down to altcoins and further out the risk curve, seeing altcoins outperforme across the board on a relative basis.

Though there is a high confidence of these dynamics playing out in a similar manner, there are potential unaccounted external factors that might skew these dynamics to the upside or downside. A soft landing and lagging economic performance, uncertain monetary and liquidity conditions amidst refiring inflation and a delayed macro crash might reduce the upside of the cycle. On the other hand, a potential super cycle due to abnormal adoption and net funds inflow into crypto assets could cause a tremendous blow-off top peak to the upside, seeing higher valuations and higher volatility outside our models and projections.

Figure 7: Crypto Market Cap (CMC) color-coded by our Total Crypto Market Dynamic Cycle Risk Metric. CMC Projection for Cycle IV.

Outlook for 2024

- The crypto market capitalization (CMC) is likely to see lower valuations around $1T in early 2024 due to cycle dynamics and macro headwinds.

- The CMC will rally to roughly $5T by year end 2024 in an early bull run, while BTC and ETH outperform most altcoins on a relative basis.

- The CMC will have its final bull run stage in mid-2025, seeing its potential cycle peak valuation of ~$15T to $20T, which will be primed by altcoins outperforming both BTC and ETH on a relative basis.

The CMC will have its final bull run stage in mid-2025, seeing its potential cycle peak valuation of ~$15T to $20T, which will be primed by altcoins outperforming both BTC and ETH on a relative basis.

Denis Oevermann, Investment Analyst and Crypto Researcher

Bitcoin Price Forecast and Cycle Dynamics

Bitcoin is the crypto asset which follows its modelled logarithmic growth trend most closely, due to its exponential growth and S-Curve adoption making it the easiest to model and predict the general dynamics of its seasonal trends and overall cyclicality with high confidence. Plotted below is Bitcoin’s price color coded by our Bitcoin Dynamic Cycle Risk Metric which gauges whether Bitcoin, based on a specific price observation is classified as high risk or low risk. The risk metric considers factors such as momentum, trend, relative market strength and relative inter crypto market cycle dynamics. If prices move up moderately, the risk stays relatively constant, whereas prices moving sideways or declining will reduce the implied risk of the Bitcoin Dynamic Cycle Risk Metric. Fitted to the overall growth trend of Bitcoin are its logarithmic trend channels for cycle tops, and lower cycle top bound, as well as its bottom bound and bottom channel trend. The risk metric ought to be used in conjunction with the trend channels, to generate a reliable buy or sell signal; the risk itself can be indicated as relatively low, due to tremendous declines in price, while the overall price itself might still be substantially above the trendline. Consequently, dark red, high-risk indications, way above the trendline and close to the top bound function as quite reliable sell signal, whereas green and dark green, low risk indications, below the trendline, close to the bottom bound function as reliable long-term entry prices and dollar cost average (DCA) price levels.

Considering our risk metric and the cycle dynamics we can model and simulate the likely bull market progression for BTC. Given the current transition of Cycle IV from late-stage bear market to early bull-run, there remains the tail risk of BTC having a final correction. However, BTC fully reset its price in this bear market already, contrary to most other crypto assets, so it will likely be more robust on the downside. A potential macro recession or overall market correction should therefore see its prices stay above $20-$25’000 on the lower end in such a scenario. Any significant deviation of Bitcoin’s price to the downside from current price levels could be considered as a strategic entry position to capture the maximum upside for the upcoming cycle phase, as indicated by our cycle dynamics and risk metrics. Based on our research, BTC offers the lowest relative risk based of the Bitcoin Dynamic Cycle Risk Metric and might thus be the major outperformer for the early bull run phase throughout 2024, with new all-time high prices for BTC being likely near year end of 2024. The projected Cycle IV peak for Bitcoin is in early 2025 to mid-2025, as BTC tends to peak as the first crypto asset, before profits are realized and funneled out the risk curve to ETH and altcoins. Bitcoin’s potential cycle peak in 2025 could be around $180’000 to $200’000 based on past cycle dynamics and a price simulation in line with our risk metric. The Bottom Bound for the Cycle IV final phase stands at $65’400, while the Bottom Channel ranges from $42k to $101k. On the upside Bitcoin’s Top Bound is $357’000 with a Top Lower Channel of $260’000.

Bitcoin is positioned best within its cycle dynamics and according to its Bitcoin Dynamic Cycle Risk Metric out of the major crypto assets. Yet also BTC would be subject to external risk factors and an overall macro crash that has a non-negligible likelihood of materializing in early 2024. However, Bitcoin is the most robust on the downside, and such market corrections are historically relatively short lived. Given the current setup of Cycle IV such an event could be seen as an additional opportunity in the late-stage bear market/early bull market to expand the BTC position for the early bull run, as the majority of upside price performance will be confined to BTC at large. Furthermore, the final Cycle IV peak could be skewed to the upside in case of a mega catalyst that would send prices upwards of the simulated price and closer to the Top Bound even. A macro fallout event, or general macroeconomic tightness might stall Bitcoin’s price action on the other hand. Still, certain macro crash events might also support the case for Bitcoin and crypto in the long run, in case of a sovereign default, or further nation state adoption to mitigate macroeconomic conditions.

Figure 8: Bitcoin price color-coded by our Bitcoin Crypto Dynamic Cycle Risk Metric. BTC price Projection for Cycle IV.

Outlook for 2024

- Bitcoin will see its lowest prices for Cycle IV in early 2024, and not revisit these lows again thereafter. Bitcoin reset its cycle dynamics on the downside and is the most robust out of all crypto assets in the current cycle phase – in a final downturn or amidst macro headwinds its price should remain above $20-$25’000.

- Bitcoin will make a new all-time high in late 2024, with its final Cycle IV peak occurring in early to mid-2025.

- Bitcoin’s Cycle IV peak will be around $180’000 to $200’000, with some mega catalyst having the potential to drive valuations closer to the Top Bound of around $357’000.

Bitcoin will make a new all-time high in late 2024, with its final Cycle IV peak occurring in early to mid-2025.

Denis Oevermann, Investment Analyst and Crypto Researcher

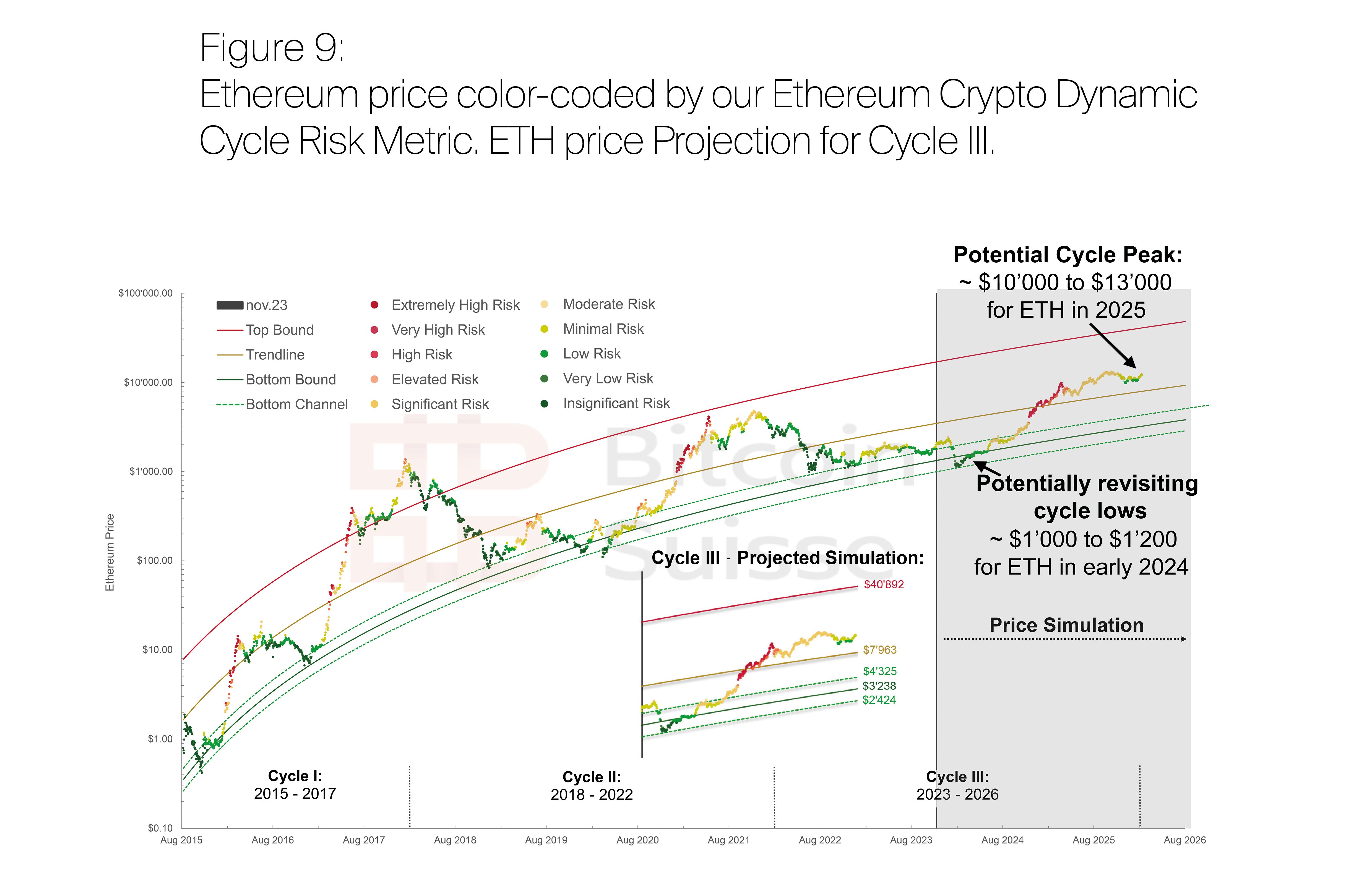

Ethereum Price Forecast and Cycle Dynamics

Due to Ethereum’s rapid “catch-up” adoption in its Cycle I it does not follow its logarithmic growth trend as closely as BTC or the crypto market capitalization (CMC). Nevertheless, it shows a consistent exponential growth and S-Curve adoption and therefore the general dynamics of its seasonal trends and overall cyclicality can be modelled and predicted with relatively high confidence. Plotted below is Ethereum’s price color coded by our Ethereum Dynamic Cycle Risk Metric which gauges whether ETH, based on a specific price observation is classified as high risk or low risk. The risk metric considers factors such as momentum, trend, relative market strength and relative inter crypto market cycle dynamics. If prices move up moderately, the risk stays relatively constant, whereas prices moving sideways or declining will reduce the implied risk of the Ethereum Dynamic Cycle Risk Metric. Fitted to the overall growth trend of ETH are its logarithmic trend channels for cycle tops and cycle bottoms as well as the overall Ethereum price trendline. The risk metric ought to be used in conjunction with the trend channels, to generate a reliable buy or sell signal; the risk itself can be indicated as relatively low, due to tremendous declines in price, while the overall price itself might still be substantially above the trendline. Consequently, dark red, high-risk indications, way above the trendline and close to the top bound function as quite reliable sell signal, whereas green and dark green, low risk indications, below the trendline, close to the bottom bound function as reliable longterm entry prices and dollar cost average (DCA) price levels.

Combining logarithmic trends and overall cycle dynamics we can simulate the likely progression of ETH for the remainder of Cycle III. Contrary to BTC, ETH has not fully reset its price for the current cycle as much as BTC has, so it has a higher likelihood of declining in the short-term and a higher downside risk and volatility to the downside. An overall crypto market correction or macro recession scenario could therefore cause it to revisit its lows in early 2024 of around $1’000 to $1’200 making it reset its cycle lows in the Bottom Channel. Ethereum can be considered the altcoin market leader, though itself it is a blue-chip, and tends to underperform against BTC in these stages of the market cycles. Overall Ethereum’s Dynamic Cycle Risk Metric is still relatively low, nevertheless, so despite its higher volatility to the downside it still offers a generally noteworthy risk-reward ratio for its projected bull run ahead.

Ethereum will likely make its Cycle III lows in early 2024, and rally subsequently in the early bull-run, chasing Bitcoin, while outperforming altcoins across the board. Any short-term correction in ETH could serve as a chance to acquire ETH at a lower price in order to profit from a potential subsequent bull run . Near the year-end 2024 ETH could be close to its former all-time high of around $4’500. Throughout early 2025 to mid-2025 Ethereum is projected to reach its peak valuations of Cycle III of up to $10’000 - $13’000. At this cycle phase ETH will outperform Bitcoin, while some of the price gains will be realized and funneled out the risk curve into altcoins, which will mostly outperform ETH subsequently. The Top Bound for Ethereum is at $40’900 at the end of Cycle III, while the Trendline supports ETH prices of roughly $8’000. Ethereum’s Bottom Bound is at ~$3’200 and the Bottom Channel ranges from ~$2’400 to ~$4’300.

Figure 9: Ethereum price color-coded by our Ethereum Crypto Dynamic Cycle Risk Metric. ETH price Projection for Cycle III.

Outlook for 2024

- ETH will see its Cycle III lows in early 2024 of around $1’000 - $1’200 as it is more volatile to the downside and will reset its cycle to the downside.

- ETH will rally close to its former all-time high of ~$4’500 near the end of 2024.

- The Cycle III peak for ETH will occur in early to mid-2025, with peak valuations of up to $10’000 - $13’000.

ETH will rally close to its former all-time high of ~$4’500 near the end of 2024

Denis Oevermann, Investment Analyst and Crypto Researcher

Navigating the year ahead and beyond

Outlook for 2024

- Given the tight monetary and liquidity conditions, coupled with the current late-stage bear market / early-stage bull run in crypto markets, historical crypto market dynamics show that limiting major crypto holdings to BTC mainly, ETH to a lesser extent, proved itself to have been beneficial. Altcoins might be selectively confined to high confidence bets only, because those select few altcoins that end up outperforming their BTC or ETH pair usually do not achieve a substantial outperformance to justify the excessive risk taking in the current market conditions.

- Q1 and Q2 of 2024 have the highest chance of a macro recession and downturn occurring, and once it materializes, we likely see the lowest prices for 2024, while not revisiting these lows going beyond 2024.

- While a recession is a large tail risk for crypto, once the economic downturn materializes will coincide with easing liquidity and monetary conditions which will cause the crypto market to rally and recover first and add to the bull run momentum. Historically, recessions have therefore been generally excellent buying opportunities in the long run.

- Despite the almost certainty that a crash and correction might come, the riskiest strategy in the current market conditions is to be divested from markets entirely, as we already face relatively low risk long-term accumulation prices for crypto assets as according to our risk metrics. Furthermore, markets tend to go up most of the time, and we are nevertheless in the transitioning phase to an early bull market.

- The downside risk of a recession is best mitigated by limiting exposure to blue chips within the crypto market, such as BTC which gives sufficient exposure to the upside while covering the downside risk best within the crypto market.

- Our research suggests that 2024 will be a bullish year. We might have short corrections as in any bull market, but those could be seen as further buying opportunities. We do not see a top in 2024 occurring unless some major substantial change on the macro end or regarding the crypto industry materializes.

- In our opinion, going further out the risk curve from end 2024 and early 2025 onwards might allow gaining maximum upside on the final phase of the crypto bull run through altcoins, before gains are usually consolidated into BTC and ETH again.

Denis Oevermann

Investment Analyst / Crypto Researcher